Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Introduction & Market Context

Bank of Montreal (NYSE:BMO) released its second quarter 2025 financial results on May 28, 2025, revealing strong revenue growth but more modest bottom-line improvement. The bank, which recently saw its stock trading near $104.81 (close to its 52-week high of $106), reported mixed performance across its business segments as it continues to execute on its ROE improvement strategy.

BMO’s presentation follows a strong first quarter where the bank significantly exceeded analyst expectations with EPS of $3.04 versus a forecast of $2.44. While Q2 shows continued revenue momentum, the pace of earnings growth has moderated compared to the previous quarter.

Quarterly Performance Highlights

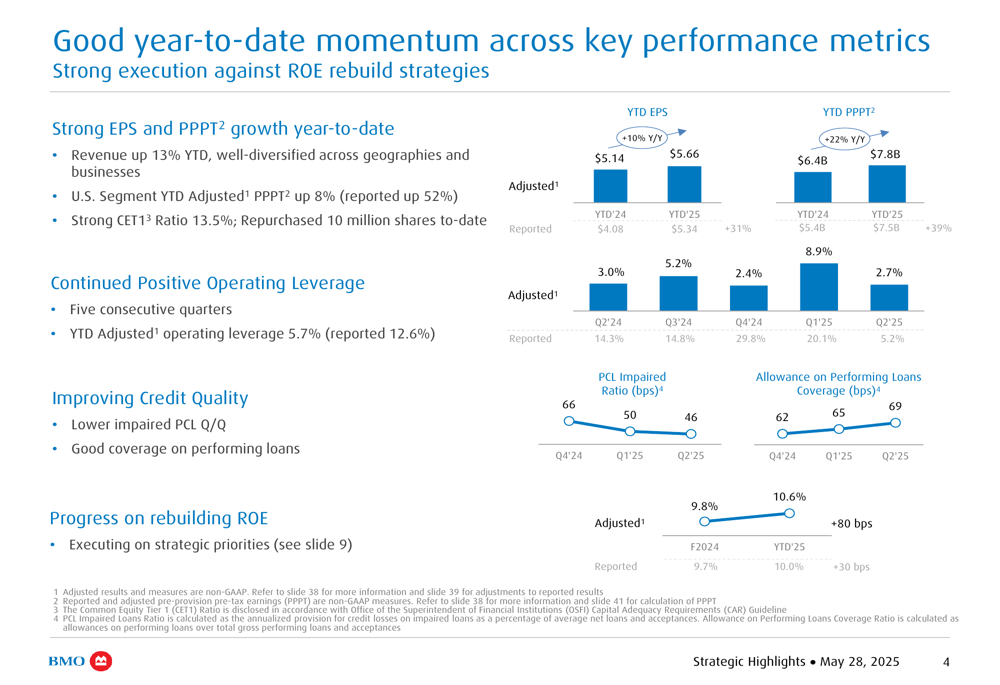

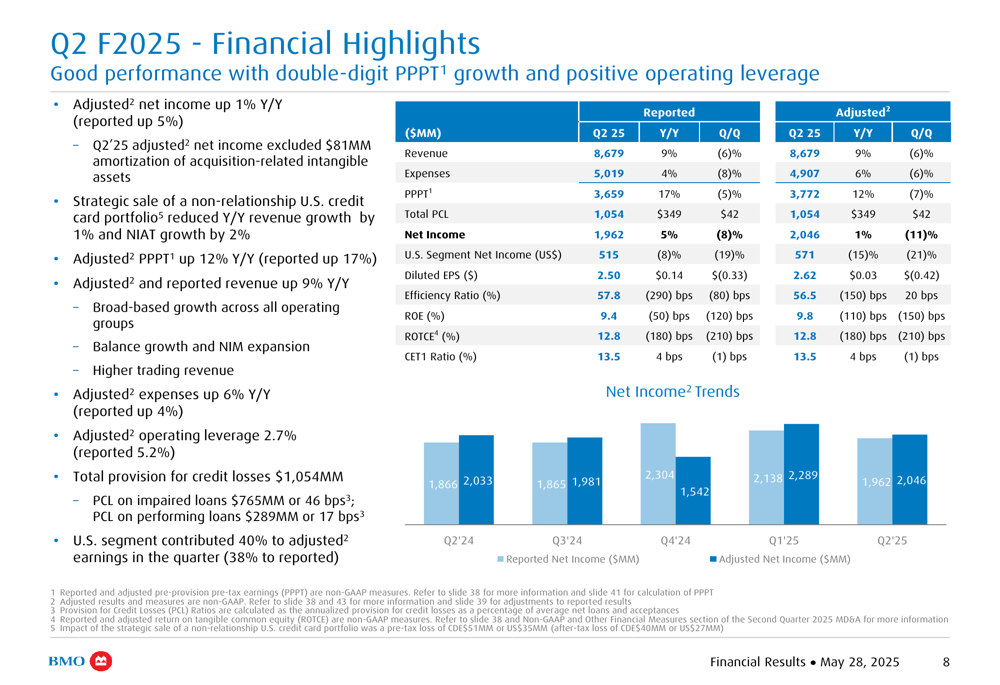

BMO reported year-to-date revenue growth of 13%, well-diversified across geographies, with adjusted net income up a modest 1% year-over-year for Q2 2025. The bank’s pre-provision, pre-tax earnings (PPPT) showed stronger growth at 12% year-over-year, indicating that provisions for credit losses are impacting bottom-line results.

As shown in the following performance metrics overview, BMO’s year-to-date EPS increased from $5.14 in 2024 to $5.66 in 2025, while PPPT grew from $6.4 billion to $7.8 billion over the same period:

The bank maintained a strong capital position with a CET1 ratio of 13.5% and has repurchased 10 million shares year-to-date, demonstrating confidence in its financial position and commitment to returning capital to shareholders.

BMO’s Q2 highlights show the contrast between strong PPPT growth and more modest net income improvement, with total provisions for credit losses reaching $1,054 million in the quarter:

Detailed Financial Analysis

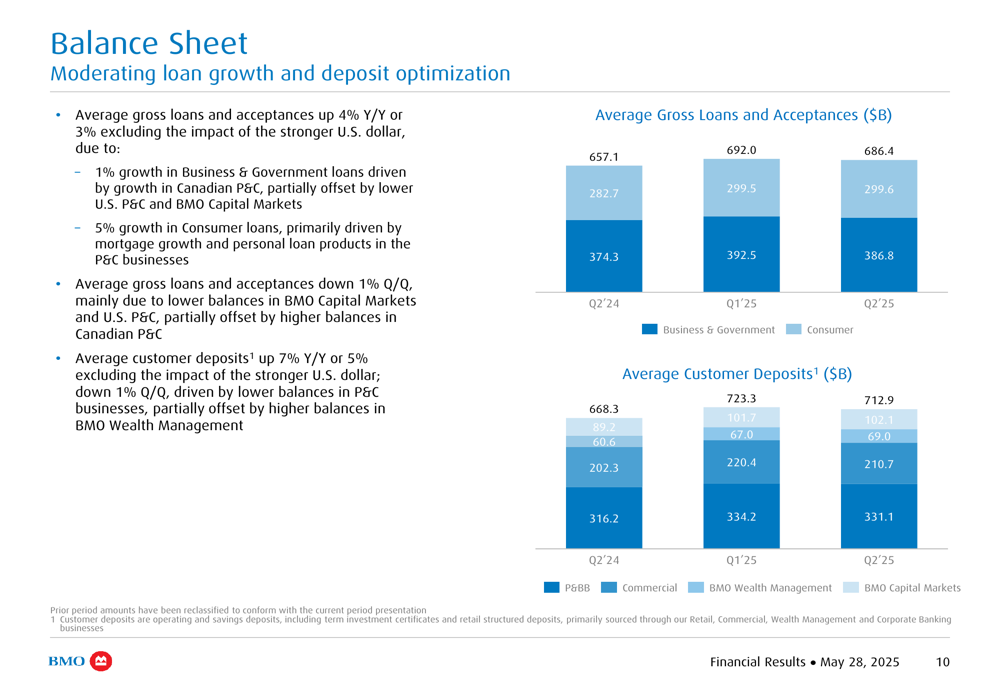

BMO’s balance sheet continues to show healthy growth, with average gross loans and acceptances up 4% year-over-year and average customer deposits up 7% year-over-year. The following chart illustrates this balance sheet expansion:

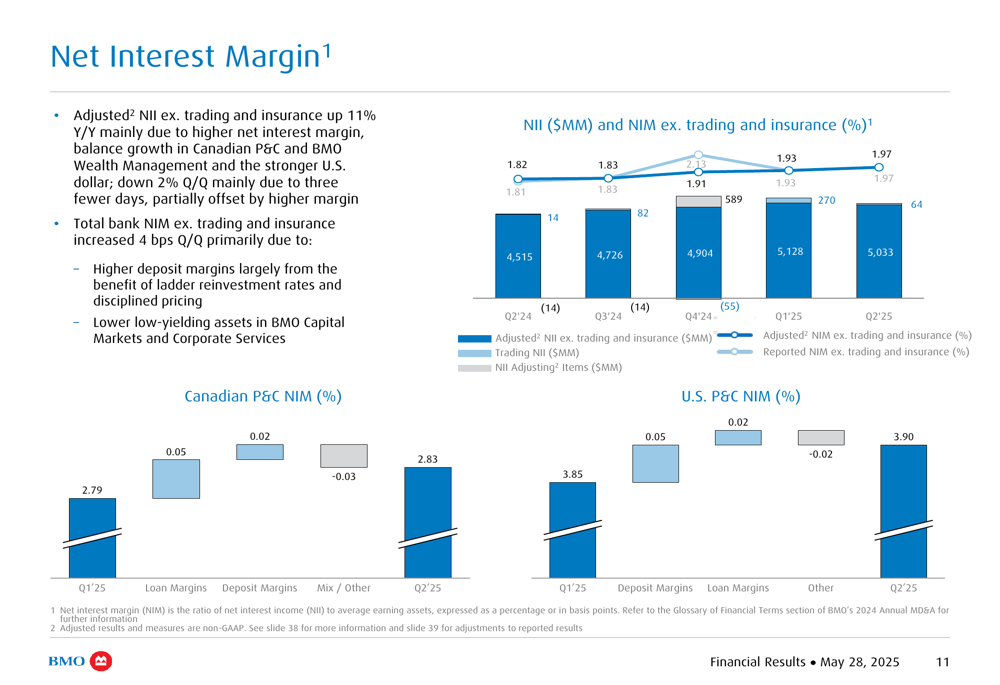

Net interest income excluding trading and insurance increased 11% year-over-year, with total bank net interest margin (NIM) excluding trading and insurance improving by 4 basis points quarter-over-quarter:

Non-interest revenue grew 4% year-over-year, though it declined 3% excluding trading. Trading revenue was particularly strong, up 37% year-over-year, contributing significantly to overall revenue growth:

On the expense side, adjusted expenses increased 6% year-over-year, with the stronger U.S. dollar and higher performance-based compensation contributing 4% to this increase. Despite rising expenses, BMO improved its adjusted efficiency ratio to 56.5%, a 150 basis point improvement year-over-year, demonstrating effective cost management relative to revenue growth.

Credit Quality and Capital Position

BMO’s credit quality showed improvement in Q2 2025, with the provision for credit losses (PCL) ratio on impaired loans decreasing to 46 basis points, down from 66 basis points in Q4 2024. However, the bank increased its allowance on performing loans from 65 basis points to 69 basis points over the same period, suggesting some caution regarding future economic conditions.

The bank’s capital position remains strong, with a CET1 ratio of 13.5% in Q2 2025, as illustrated in the following capital analysis:

Segment Performance

BMO’s business segments showed varied performance in Q2 2025. The bank’s presentation highlighted the strength of its diversified business model, with PPPT growth across all segments:

Canadian Personal & Commercial Banking reported adjusted and reported net income down 10% year-over-year, despite PPPT growth of 5% year-over-year. This divergence reflects the impact of higher provisions for credit losses, which totaled $608 million in the quarter:

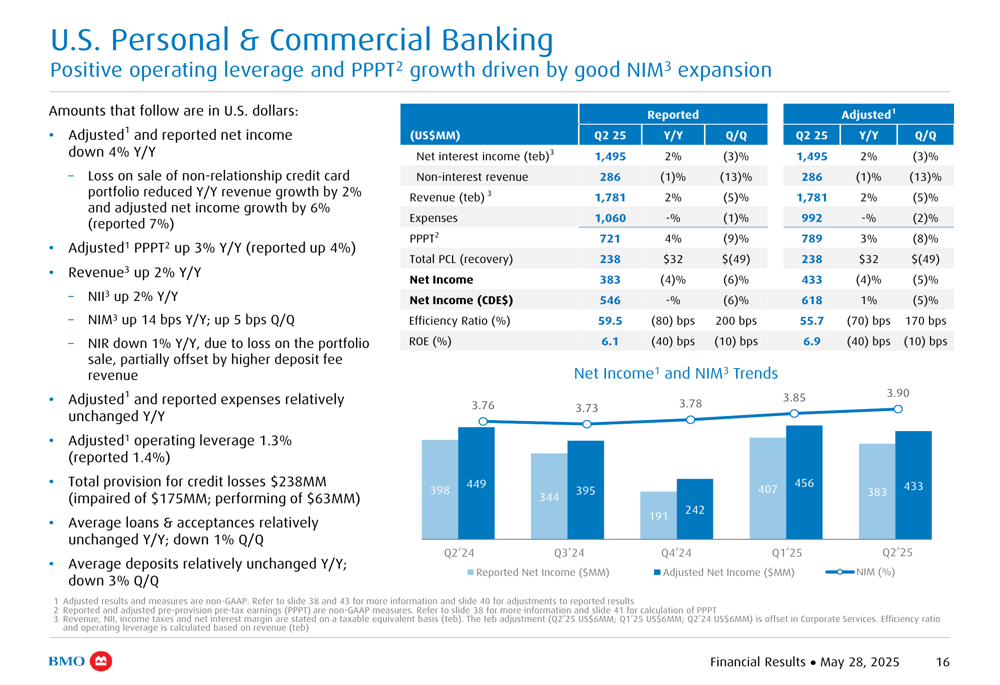

Similarly, U.S. Personal & Commercial Banking saw adjusted and reported net income decline 4% year-over-year, while PPPT increased 3% year-over-year. Revenue grew 2% year-over-year, and total provisions for credit losses were $238 million:

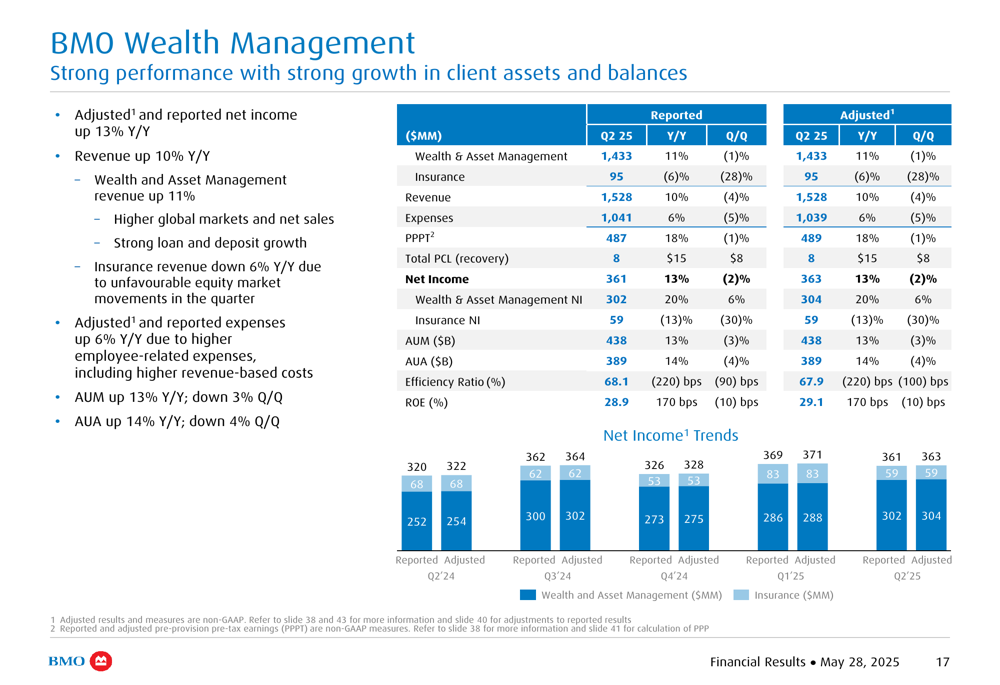

BMO Wealth Management was a standout performer, with adjusted and reported net income up 13% year-over-year and revenue up 10% year-over-year. Assets under management (AUM) increased 13% year-over-year but declined 3% quarter-over-quarter:

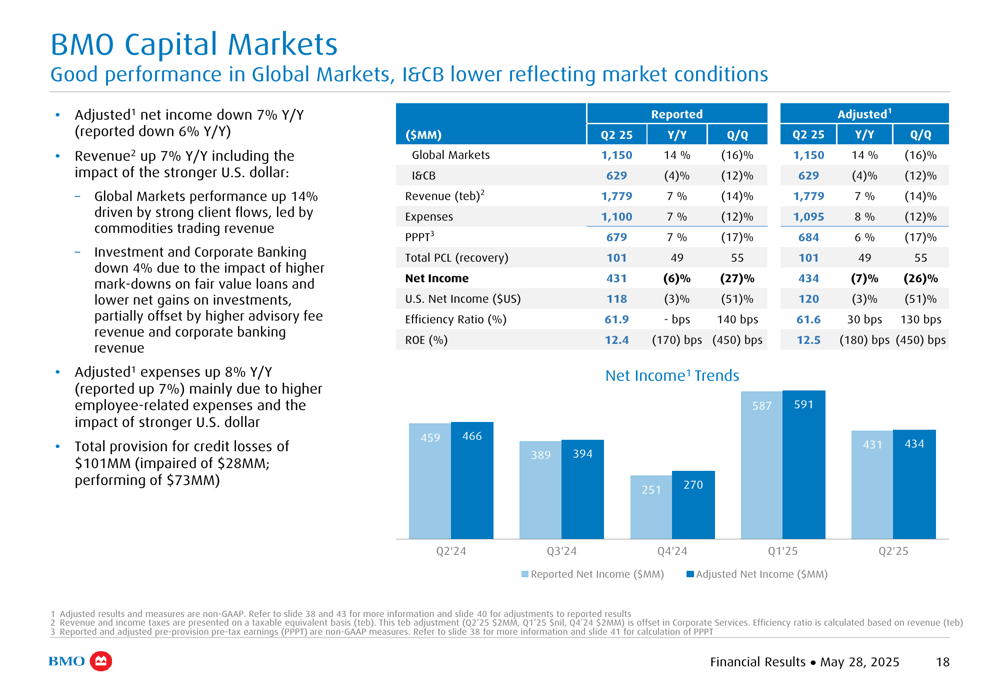

BMO Capital Markets showed mixed results, with adjusted net income down 7% year-over-year despite revenue growth of 7% year-over-year. The segment recorded total provisions for credit losses of $101 million:

Strategic Initiatives & Outlook

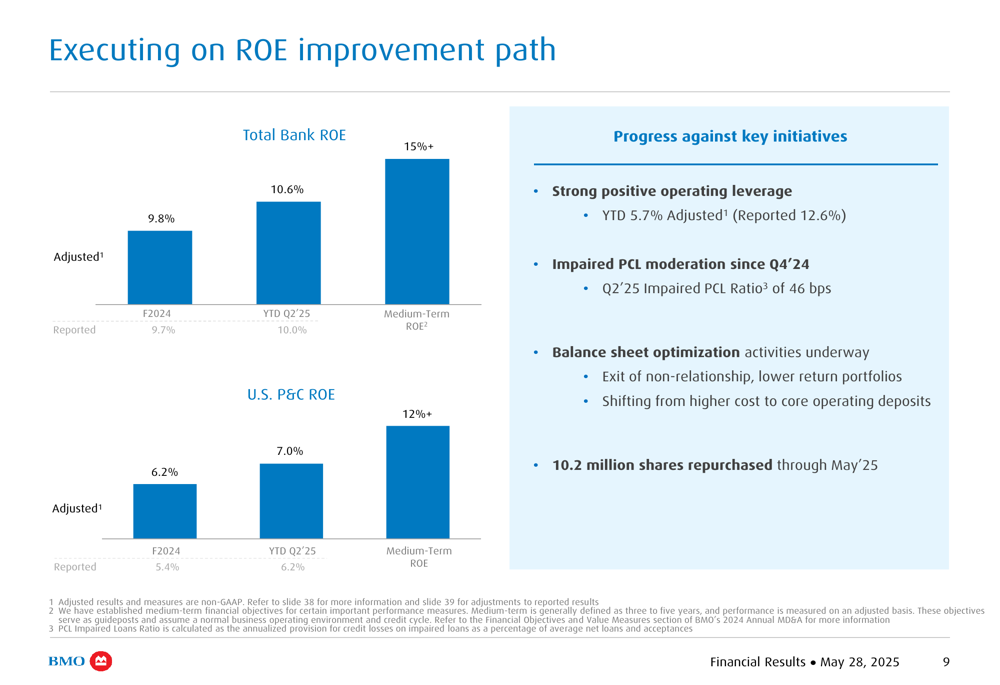

BMO continues to execute on its ROE improvement strategy, with total bank ROE reaching 10.6% in Q2 2025. This represents progress toward the medium-term target of 15% mentioned in the Q1 2025 earnings call:

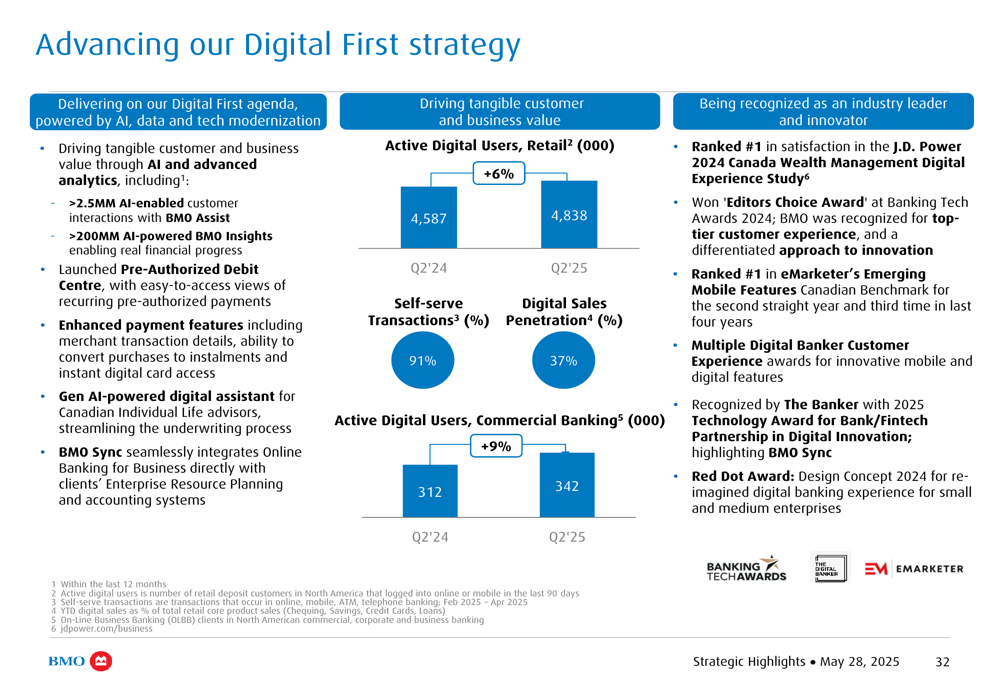

The bank’s Digital First strategy is showing tangible results, with active digital users in retail banking up 6% year-over-year to 4.84 million, and active digital users in commercial banking up 9% year-over-year to 342,000:

BMO’s presentation emphasized its purpose of "Boldly growing the good in business and life," highlighting its commitment to a thriving economy, sustainable future, and inclusive society. The bank was recognized as one of the World’s Most Ethical Companies, and its Annual Employee Giving Campaign raised $39 million.

Summary and Outlook

BMO’s Q2 2025 results demonstrate the bank’s ability to generate strong revenue growth across its diversified business segments. However, the modest net income growth compared to PPPT growth suggests that provisions for credit losses are impacting bottom-line performance.

The bank’s strong capital position, share repurchase program, and improving efficiency ratio indicate effective capital and cost management. While credit quality is improving as evidenced by the declining PCL ratio on impaired loans, the increased allowance for performing loans suggests caution regarding future economic conditions.

As BMO continues to execute on its ROE improvement strategy and Digital First initiatives, investors will be watching to see if the bank can translate its strong revenue growth into more substantial bottom-line improvement in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.