JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

BNP Paribas (OTC:BNPQY) (EPA:BNP) presented its first quarter 2025 results on April 24, showing solid revenue growth of 3.8% year-over-year, though net income declined by 4.9%. The French banking giant continues to benefit from its diversified business model, with particularly strong performance in its Corporate & Institutional Banking division amid Europe’s reinvestment initiatives.

The bank’s performance broadly aligns with its 2024-2026 strategic growth trajectory, balancing revenue growth against increased operating expenses and higher cost of risk. BNP Paribas also announced a share buyback program of €1.08 billion for the second quarter of 2025.

Quarterly Performance Highlights

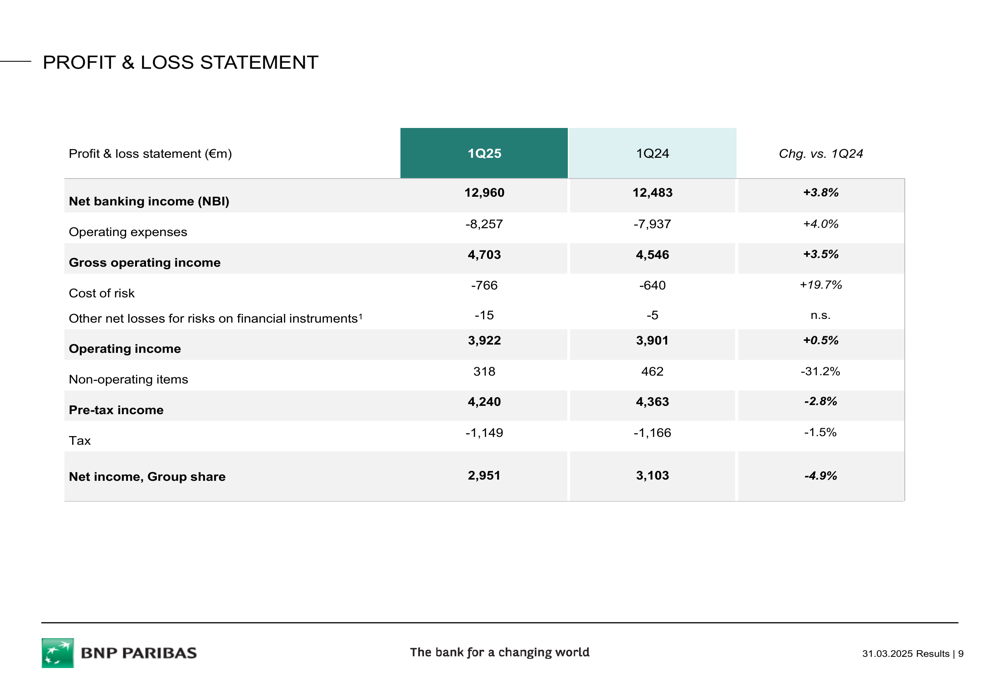

BNP Paribas reported Q1 2025 revenues of €12,960 million, representing a 3.8% increase compared to Q1 2024. However, operating expenses rose at a slightly faster pace of 4.0% to €8,257 million, resulting in a negative jaws effect of 0.2 percentage points at the group level.

As shown in the following comprehensive profit and loss statement, net income attributable to shareholders decreased by 4.9% to €2,951 million, primarily due to higher cost of risk and operating expenses:

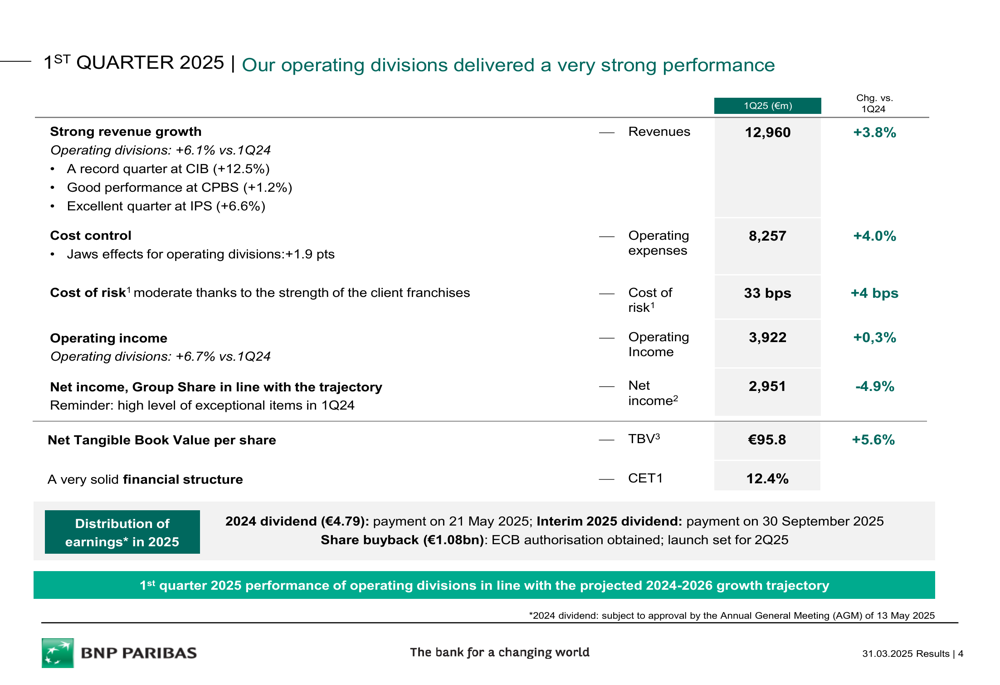

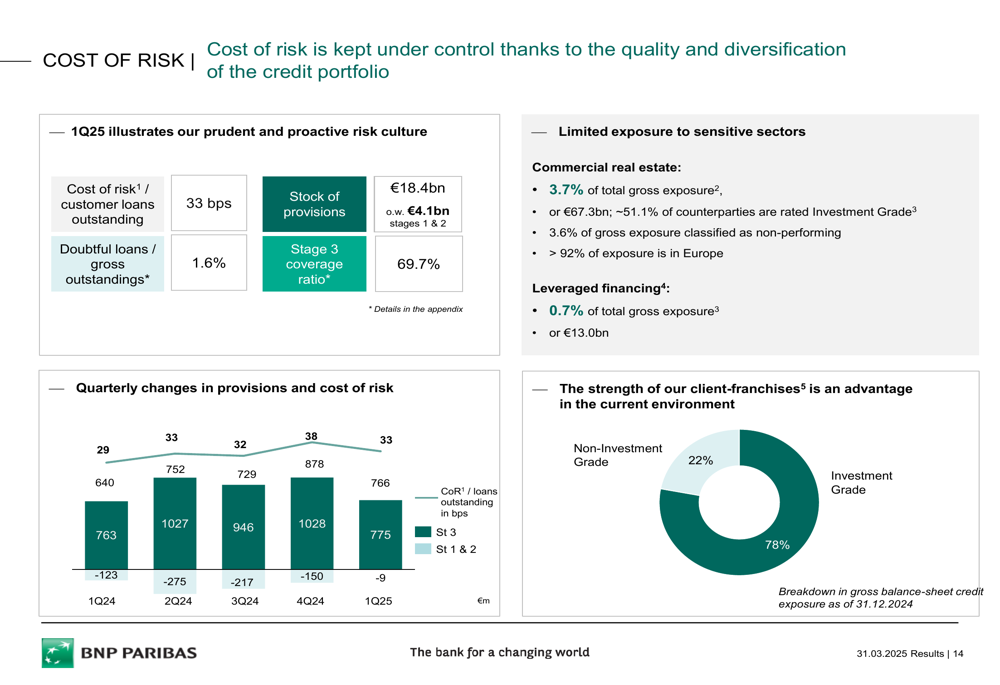

The bank’s cost of risk increased to 33 basis points, up 4 basis points from the previous year, reflecting prudent risk management in the current economic environment. Despite this increase, BNP Paribas maintains a strong capital position with a CET1 ratio of 12.4% and a net tangible book value per share of €95.8, up 5.6% year-over-year.

The following chart illustrates the bank’s key performance metrics for Q1 2025:

Divisional Performance Analysis

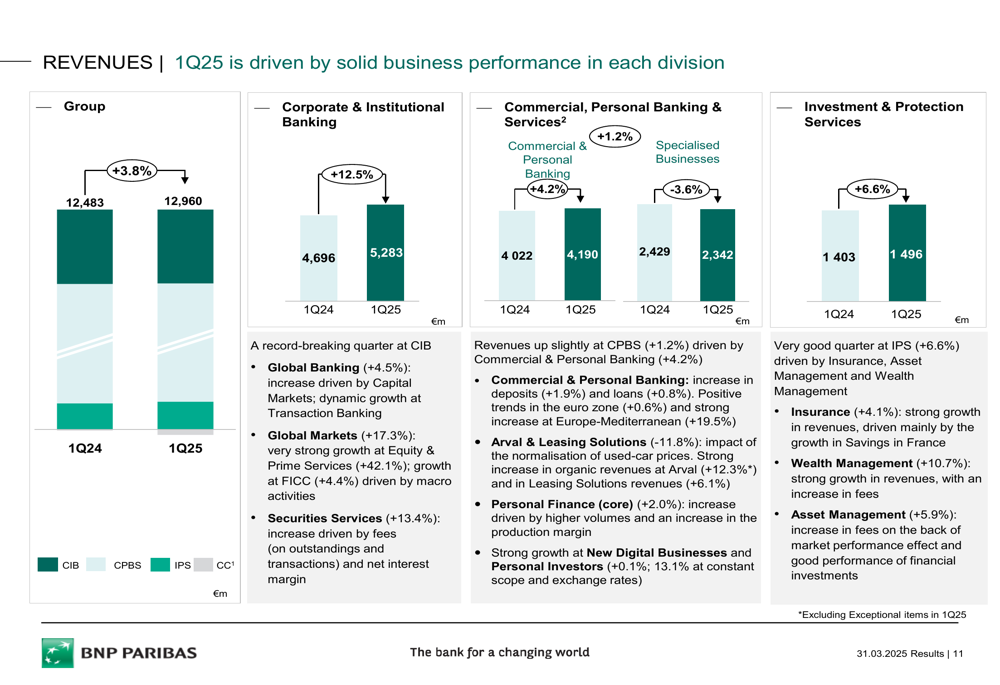

The Corporate & Institutional Banking (CIB) division was the standout performer, with revenues increasing by 12.5% to €5,283 million. This growth was primarily driven by Global Markets, which saw a 17.3% revenue increase, while Global Banking revenues grew by 4.5%.

The divisional revenue breakdown clearly shows the strong contribution from CIB, which accounted for approximately 41% of total group revenues:

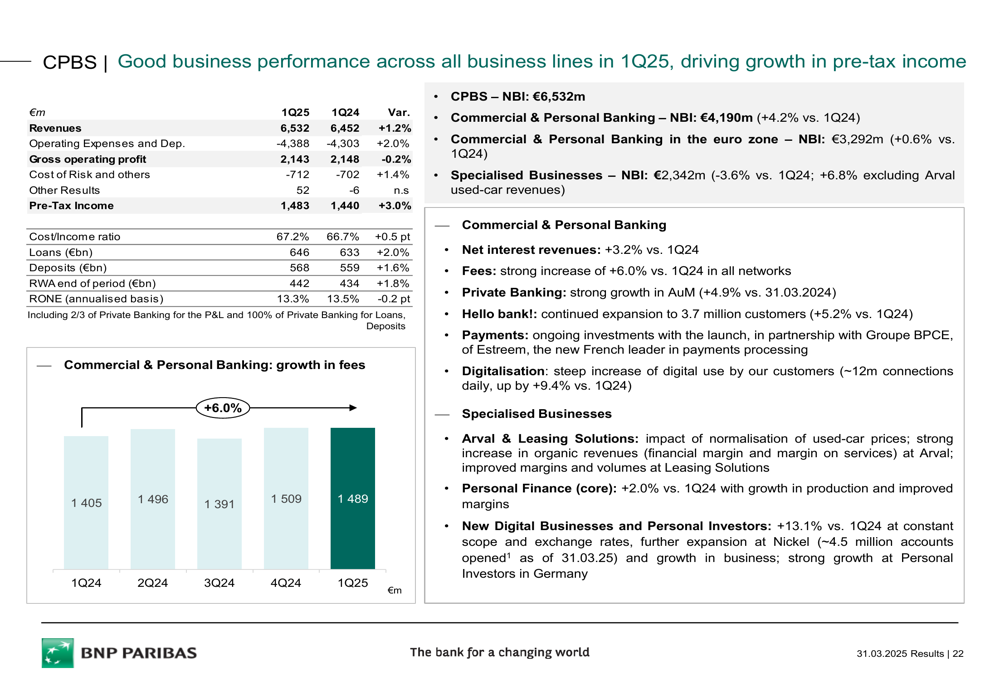

The Commercial, Personal Banking & Services (CPBS) division, which represents the largest portion of the bank’s revenue at approximately 50%, posted a modest 1.2% growth to €6,532 million. Within this division, Commercial & Personal Banking revenues increased by 4.2%, while Specialized Businesses revenues declined by 3.6%.

The following chart details the CPBS division’s performance metrics:

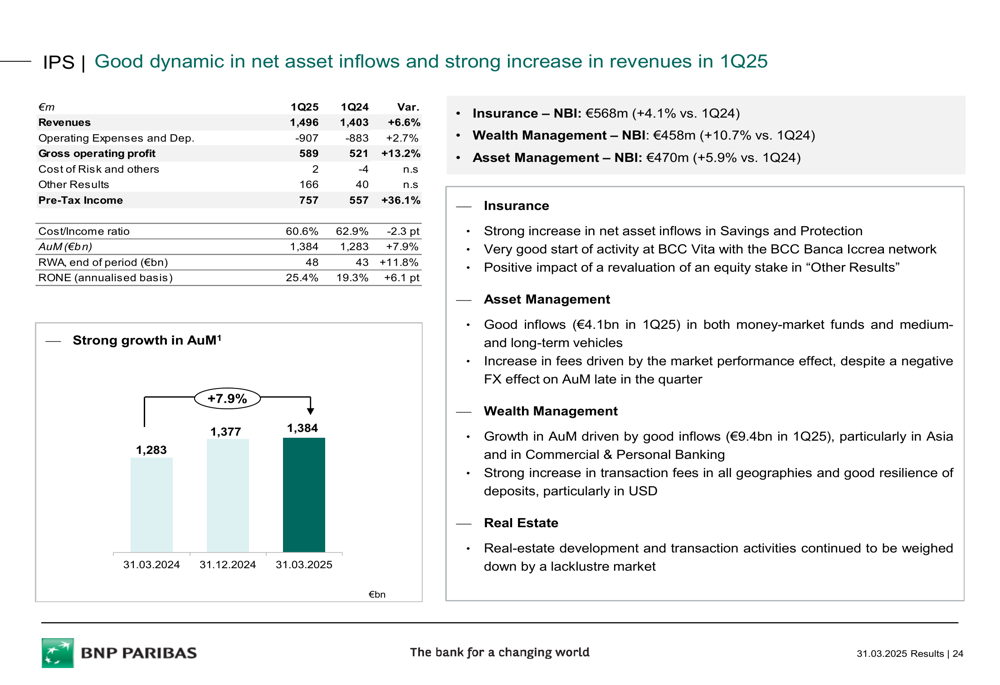

The Investment & Protection Services (IPS) division delivered strong results with revenues increasing by 6.6% to €1,496 million and pre-tax income surging by 36.1% to €757 million. This performance was driven by growth across all business lines, with Wealth Management leading at 10.7% revenue growth.

The IPS division’s performance is illustrated in the following chart:

Strategic Initiatives & Outlook

BNP Paribas reaffirmed its 2024-2026 strategic outlook, projecting revenue growth exceeding 5% CAGR, net income growth above 7% CAGR, and EPS growth exceeding 8% CAGR. The bank also targets a positive jaws effect of approximately 1.5 percentage points on average per year.

A key strategic initiative is the planned acquisition of AXA Investment Managers, which is expected to strengthen the bank’s IPS division. Additionally, BNP Paribas is focusing on supporting Europe’s reinvestment plans, positioning itself to benefit from Germany’s €1,000-1,500 billion reinvestment plan (2025-2035) and the Readiness 2030 Plan (€800 billion, 2025-2030).

The bank’s operational efficiency program is progressing well, with approximately €190 million of the targeted €600 million in additional cost savings for 2025 already realized in the first quarter. These savings are being implemented across all divisions, with a particular focus on the Personal Finance adaptation plan and optimization of shared service centers.

The following chart outlines the bank’s prudent risk management approach, highlighting its limited exposure to sensitive sectors:

Capital Position & Shareholder Returns

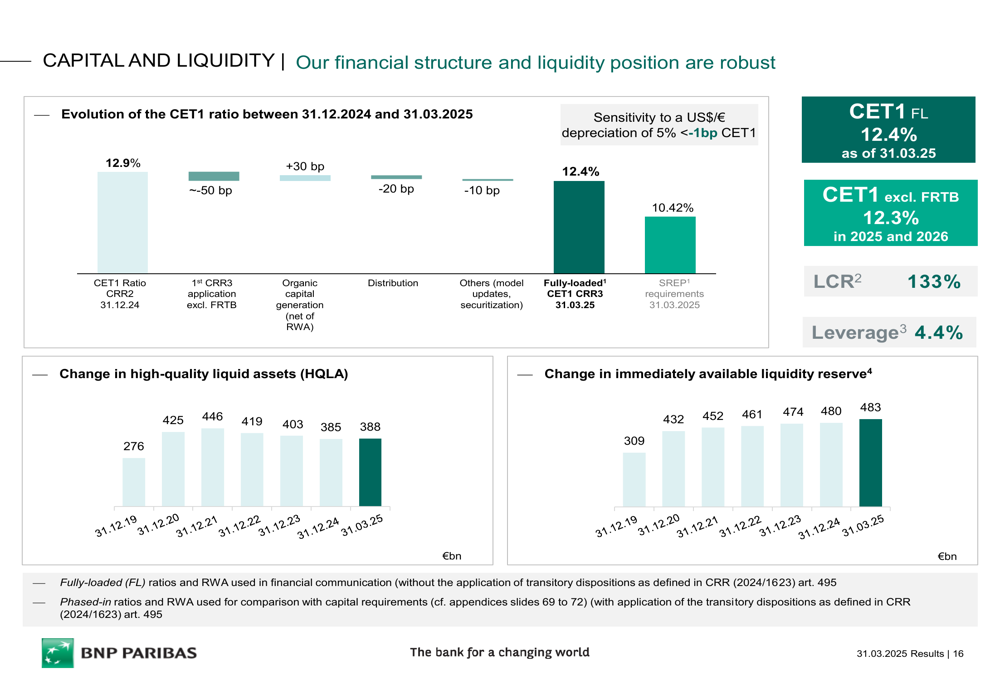

BNP Paribas maintains a strong capital and liquidity position, with a CET1 ratio of 12.4% and a leverage ratio of 4.4%. The bank’s liquidity coverage ratio stands at 133%, indicating robust short-term resilience.

The bank announced a 2024 dividend of €4.79 per share and launched a share buyback program of €1.08 billion for the second quarter of 2025. This reflects BNP Paribas’ commitment to shareholder returns, with dividends showing a compound annual growth rate of 10.2%.

The following chart illustrates the bank’s capital structure and liquidity position:

BNP Paribas continues to demonstrate resilience through economic cycles, with a diversified credit exposure across sectors. The bank’s through-cycle performance is reflected in its consistent dividend growth and increasing net tangible book value per share, which has grown at a CAGR of 5.0%.

Overall, BNP Paribas’ Q1 2025 results demonstrate the bank’s ability to generate revenue growth in a challenging environment, though increased costs and risk provisions have impacted bottom-line performance. The bank’s strategic focus on European reinvestment opportunities and planned acquisitions positions it well for future growth, supported by a strong capital position and commitment to operational efficiency.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.