Still betting on Nvidia? Our AI picked this stock instead; it’s up 96%+ THIS MONTH

Introduction & Market Context

BNP Paribas (OTC:BNPQY) (OTC:BNP) released its second quarter 2025 results on July 24, showing solid operating performance with revenue growth of 2.5% compared to the same period last year. The presentation highlighted the bank’s continued operational efficiency and positive jaws effect across all divisions, despite a 4.0% decline in net income. The bank also announced an interim dividend of €2.59 per share, to be paid on September 30, 2025.

The results come after a challenging first quarter where the bank reported a revenue miss but still saw its stock price rise, indicating investor confidence in its strategic direction. The Q2 performance reinforces this confidence, with the bank projecting strong acceleration in the second half of 2025.

Quarterly Performance Highlights

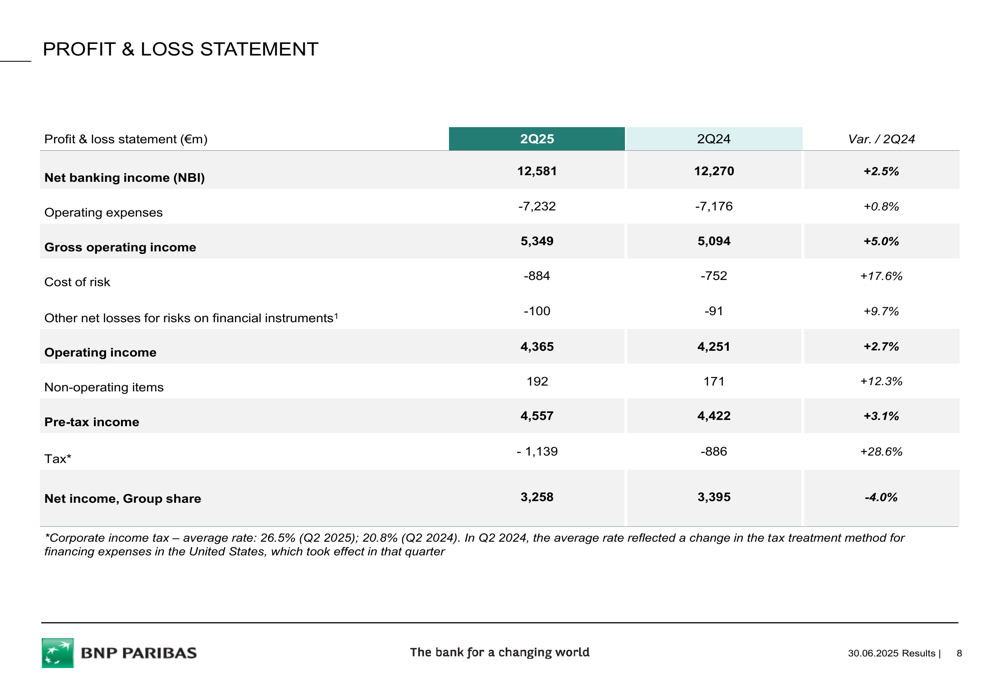

BNP Paribas reported revenues of €12,581 million in Q2 2025, representing a 2.5% increase compared to Q2 2024. Operating expenses rose slightly by 0.8% to €7,232 million, resulting in a gross operating income of €5,349 million, up 5.0% year-on-year. Pre-tax income increased by 3.1% to €4,557 million, while net income decreased by 4.0% to €3,258 million.

As shown in the following comprehensive profit and loss statement, the bank maintained solid performance across key metrics:

The decline in net income was primarily due to a higher corporate income tax rate, which averaged 26.5% in Q2 2025 compared to 20.8% in Q2 2024. The bank noted that the Q2 2024 rate reflected a change in the tax treatment method for financing expenses in the United States, which took effect in that quarter.

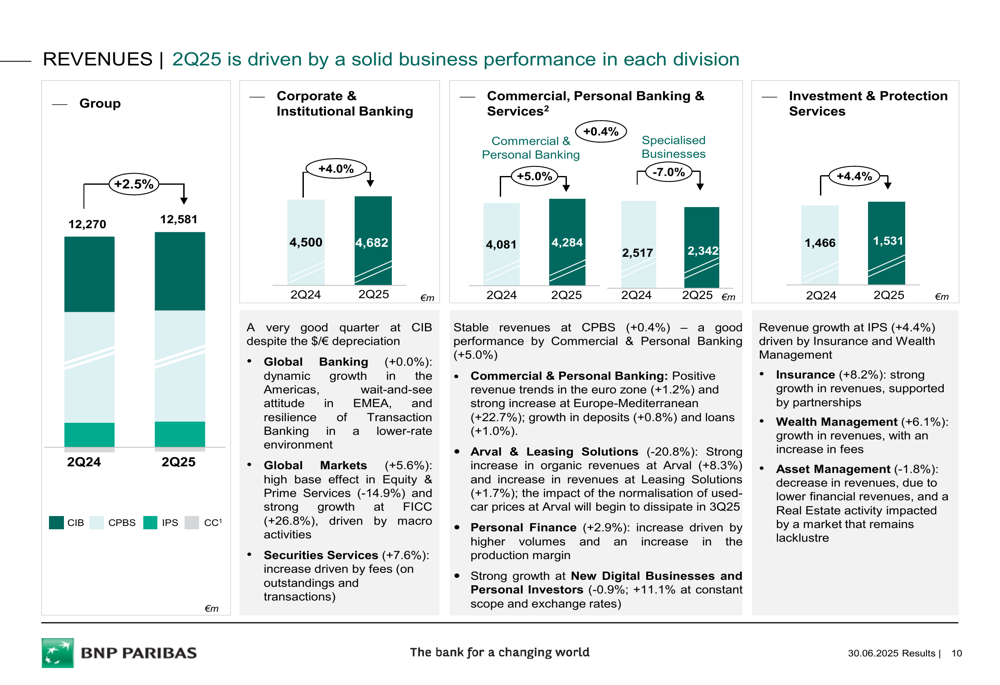

Revenue growth was driven by solid performance across all operating divisions. The Corporate & Institutional Banking (CIB) division led with a 4.0% increase, while Commercial, Personal Banking & Services (CPBS) and Investment & Protection Services (IPS) grew by 0.4% and 4.4%, respectively.

The following chart illustrates the revenue breakdown by division, highlighting the balanced contribution from each business segment:

Divisional Performance

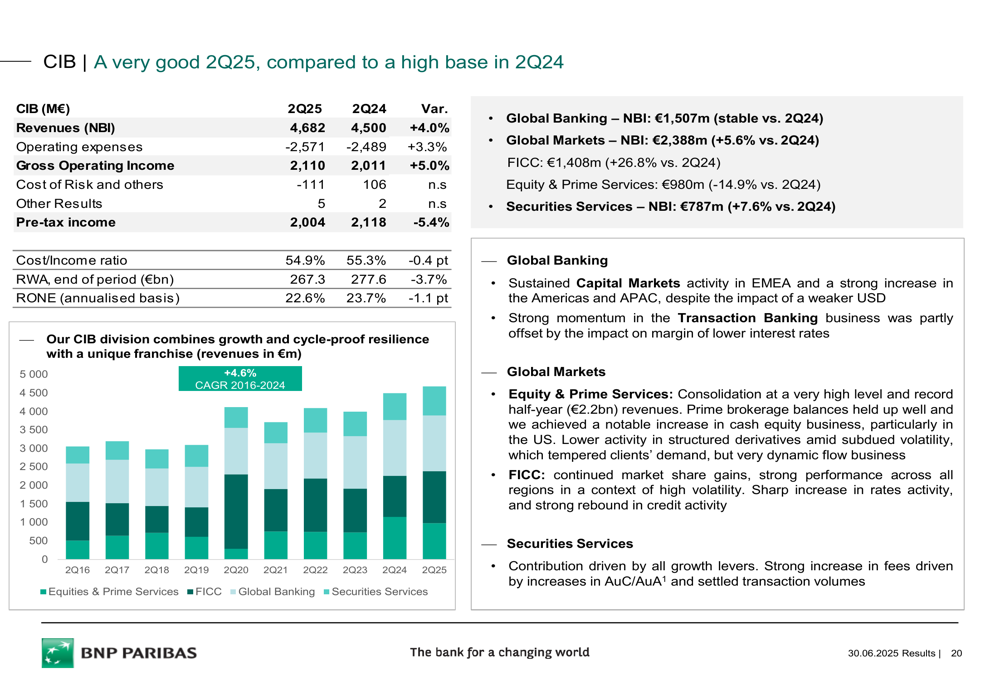

The Corporate & Institutional Banking division delivered strong results with revenues of €4,682 million, up 4.0% compared to Q2 2024. This growth was driven by Global Markets (+5.6%) and Securities Services (+7.6%), while Global Banking remained stable. Pre-tax income decreased by 5.4% to €2,004 million, but the division maintained a solid cost/income ratio of 54.9% and an annualized RONE of 22.6%.

As shown in the detailed CIB performance overview:

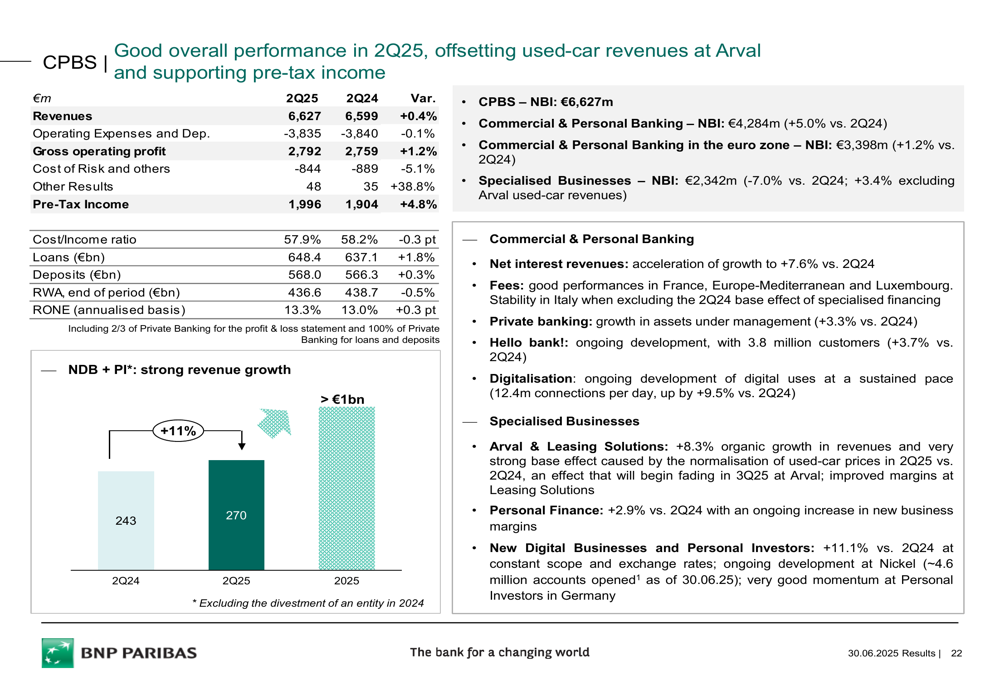

The Commercial, Personal Banking & Services division reported stable revenues of €6,627 million, a slight increase of 0.4% compared to Q2 2024. Pre-tax income grew by 4.8% to €1,996 million, reflecting improved operational efficiency. The division benefited from accelerating net interest income and very strong revenue growth in New Digital Businesses and Personal Investors (+11%).

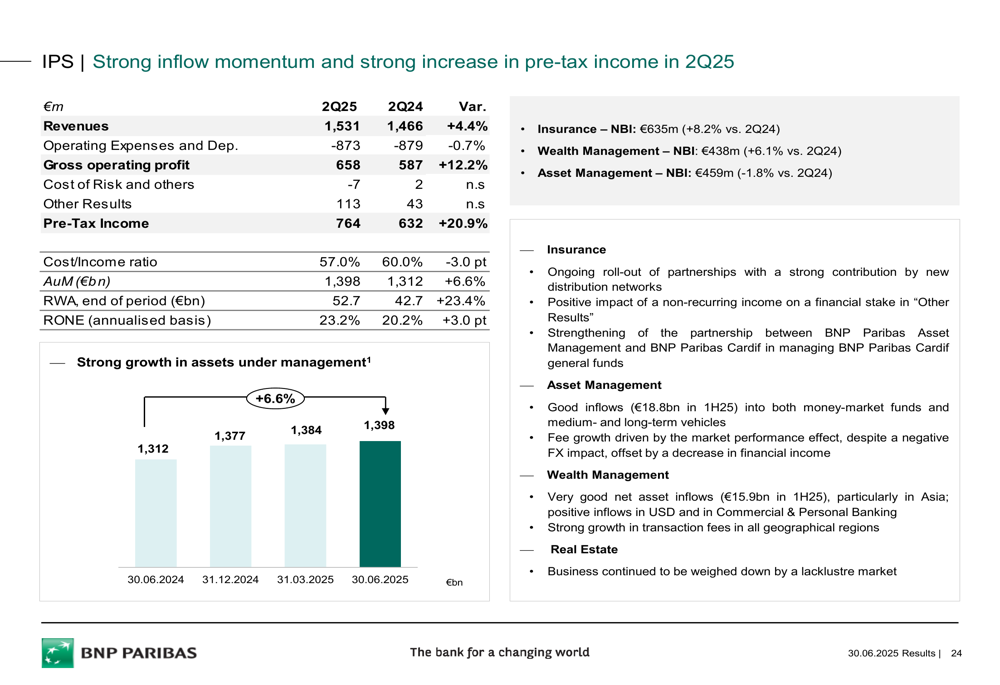

The Investment & Protection Services division showed strong momentum with revenues of €1,531 million, up 4.4% year-on-year. Pre-tax income increased significantly by 20.9% to €764 million. Assets under management grew by 6.6% to €1,398 billion, supported by solid net inflows and positive market effects.

Operational Efficiency & Cost Control

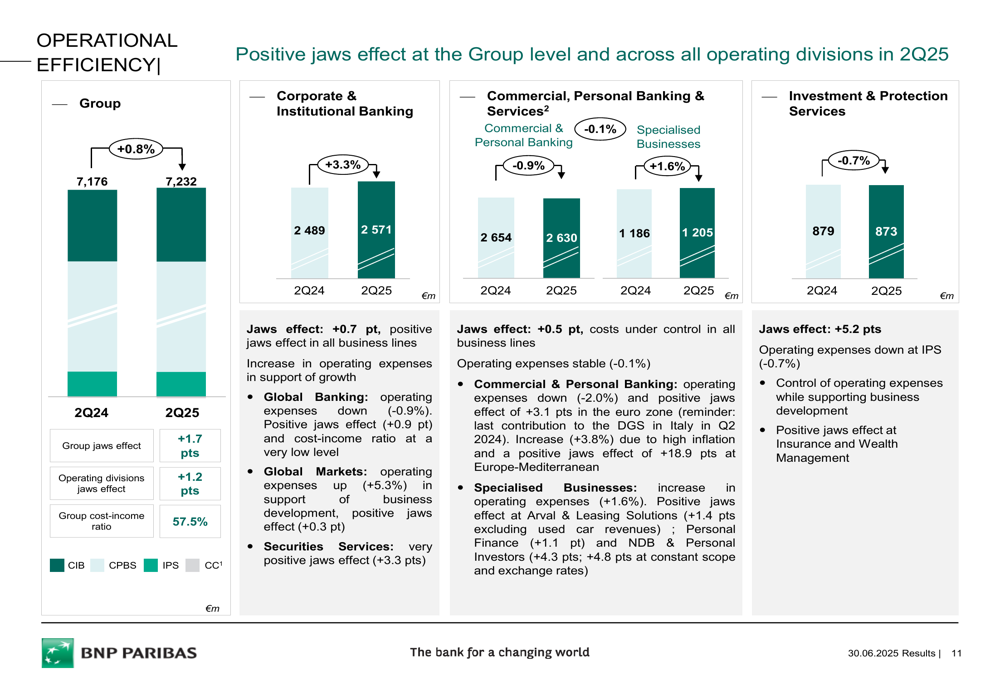

A key highlight of BNP Paribas’ Q2 2025 results was the positive jaws effect (revenue growth exceeding cost growth) across all operating divisions. At the Group level, the jaws effect was +1.7 percentage points, demonstrating the bank’s commitment to operational efficiency.

The following chart illustrates the positive jaws effect across divisions:

The bank reported that approximately €380 million of the total €600 million in additional cost measures planned for 2025 have already been achieved in the first half of the year. These operational efficiency measures have helped absorb the impacts of inflation while supporting continued business development.

Risk Management & Capital Position

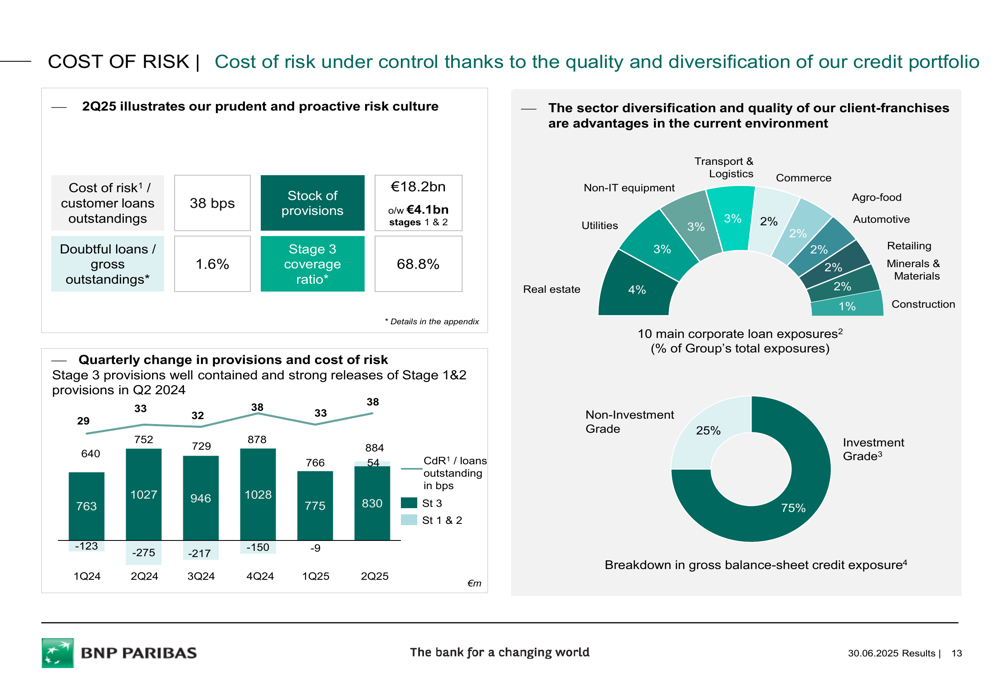

BNP Paribas maintained a prudent approach to risk management, with cost of risk at 38 basis points of customer loans outstanding. The bank’s credit portfolio quality remains high, with doubtful loans representing just 1.6% of gross outstandings and a stage 3 coverage ratio of 68.8%.

The following chart demonstrates the bank’s risk profile and sector diversification:

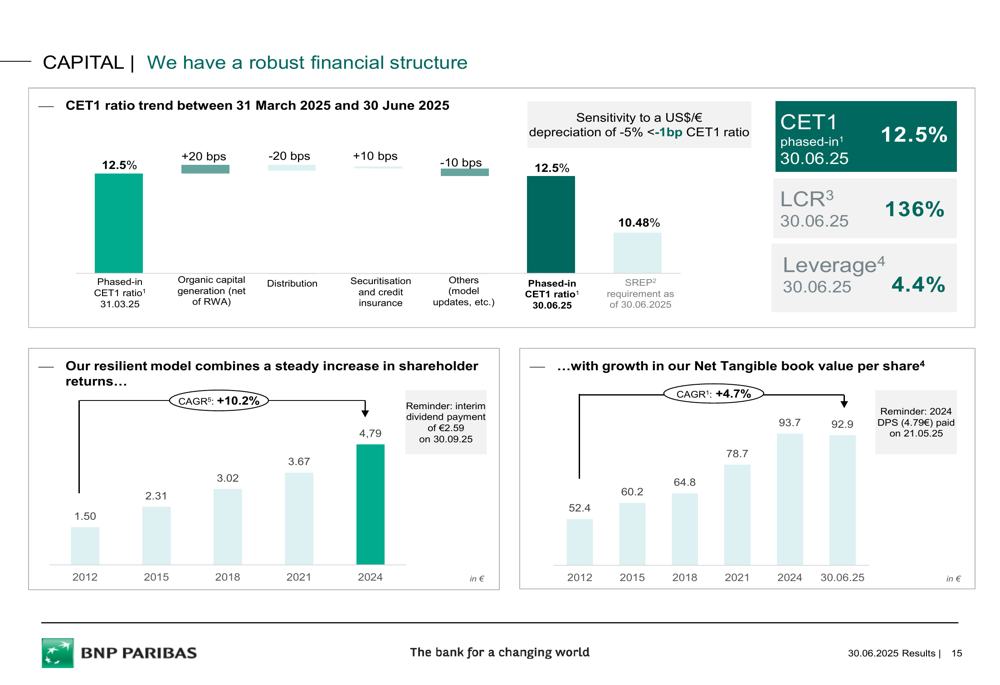

The bank’s financial structure remains robust, with a CET1 ratio of 12.5% as of June 30, 2025. The net tangible book value per share reached €92.9, representing a compound annual growth rate of 4.7% since 2012.

BNP Paribas completed a share buyback program of €1.08 billion on June 9, 2025, further enhancing shareholder returns. The bank’s dividend distribution policy remains strong, with a steady increase in shareholder returns at a CAGR of 10.2% since 2012.

Strategic Initiatives & Outlook

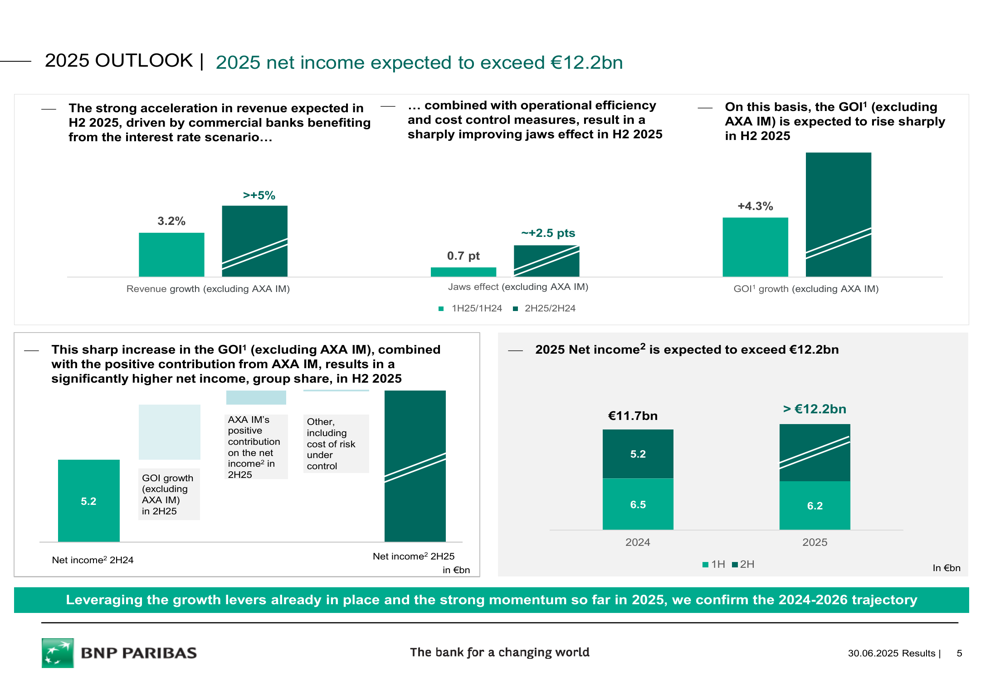

BNP Paribas is optimistic about its performance for the remainder of 2025, expecting a strong acceleration in net income in the second half of the year. The bank projects that its full-year net income will exceed €12.2 billion, compared to €11.7 billion in 2024.

The following chart outlines the 2025 outlook, highlighting the expected revenue growth and operational efficiency:

Looking further ahead, the bank confirmed its 2024-2026 trajectory, targeting revenue growth of more than 5% CAGR and net income growth exceeding 7% CAGR during this period. Earnings per share are expected to grow at more than 8% CAGR between 2024 and 2026.

The bank also highlighted its acquisition of AXA Investment Managers (AXA IM), which will strengthen its position as a European leader in long-term savings management. The acquisition is expected to have a CET1 impact of -35 basis points but will create significant synergies through an expanded client franchise and product offering.

Sustainable Development

BNP Paribas continues to focus on sustainable development, with new Corporate Social Responsibility targets aligned with its financial calendar. The bank aims to increase the share of women in senior management positions to 40% in 2025 and 42% in 2026, expand the number of beneficiaries of products and services supporting financial inclusion, and increase support for clients transitioning to a low-carbon economy.

The bank maintains strong extra-financial ratings, including a 17.2 score from Sustainalytics and 72/100 from Ecovadis, reflecting its commitment to environmental, social, and governance (ESG) principles.

Conclusion

BNP Paribas’ Q2 2025 results demonstrate solid operating performance across all divisions, with effective cost control measures offsetting inflationary pressures. Despite a slight decline in net income, the bank’s overall financial position remains strong, with robust capital ratios and continued shareholder returns through dividends and share buybacks.

The bank’s optimistic outlook for the second half of 2025 and confirmation of its 2024-2026 trajectory suggest confidence in its strategic direction and ability to navigate the evolving financial landscape. The acquisition of AXA IM further strengthens its position in the asset management sector, supporting long-term growth ambitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.