BETA Technologies launches IPO of 25 million shares priced $27-$33

Introduction & Market Context

Swedish book retailer Bokusgruppen AB (BOKUS) reported strong first-quarter results for 2025, continuing its positive momentum with significant growth in both sales and profitability. The company, which operates the Akademibokhandeln stores, Bokus online bookstore, and Bokus Play audiobook service, has shown consistent improvement in its financial performance despite operating in what management describes as an "uncertain and turbulent external environment."

The stock closed at 51.0 SEK on April 25, 2025, up 0.4 SEK (0.79%) following the release of the quarterly results. The share price has traded between 42.5 SEK and 55.0 SEK over the past 52 weeks.

Quarterly Performance Highlights

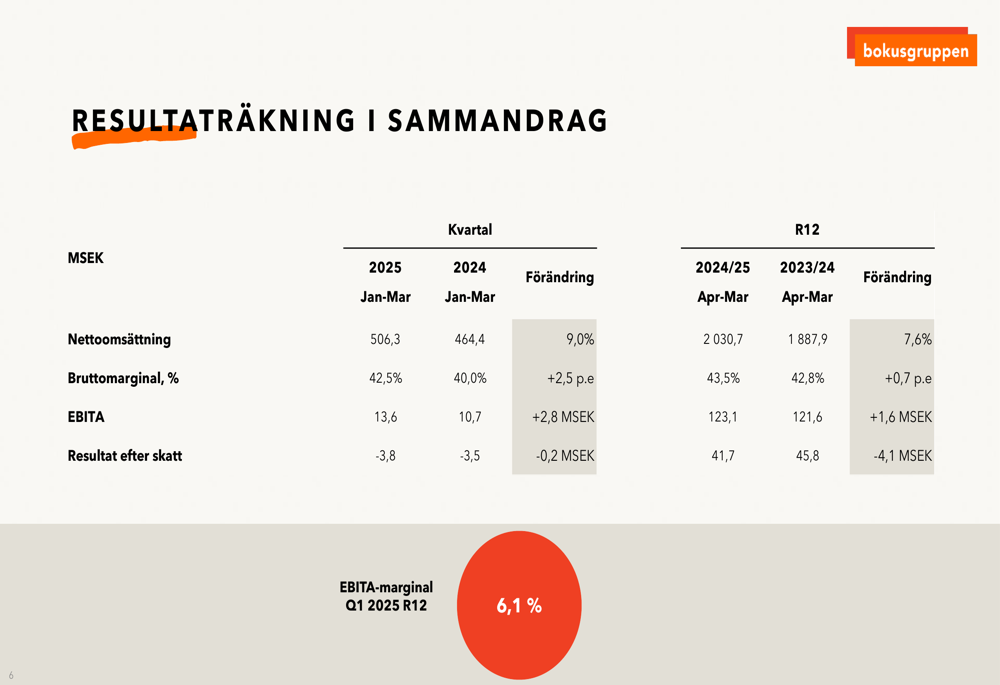

Bokusgruppen delivered impressive growth across key financial metrics in Q1 2025. Net sales increased by 9.0% compared to the same period last year, while gross profit grew by 15.8%. The company’s EBITA (earnings before interest, taxes, and amortization) showed even stronger improvement, increasing by 26.3% year-over-year.

As shown in the following chart of Bokusgruppen’s Q1 2025 performance metrics:

The company’s gross margin expanded significantly to 42.5% in Q1 2025, up 2.5 percentage points from 40.0% in Q1 2024. This margin improvement, combined with the sales growth, drove the substantial increase in EBITA.

Management attributed the strong performance to both organic growth and contributions from recent acquisitions, though specific details about these acquisitions were not provided in the presentation.

Detailed Financial Analysis

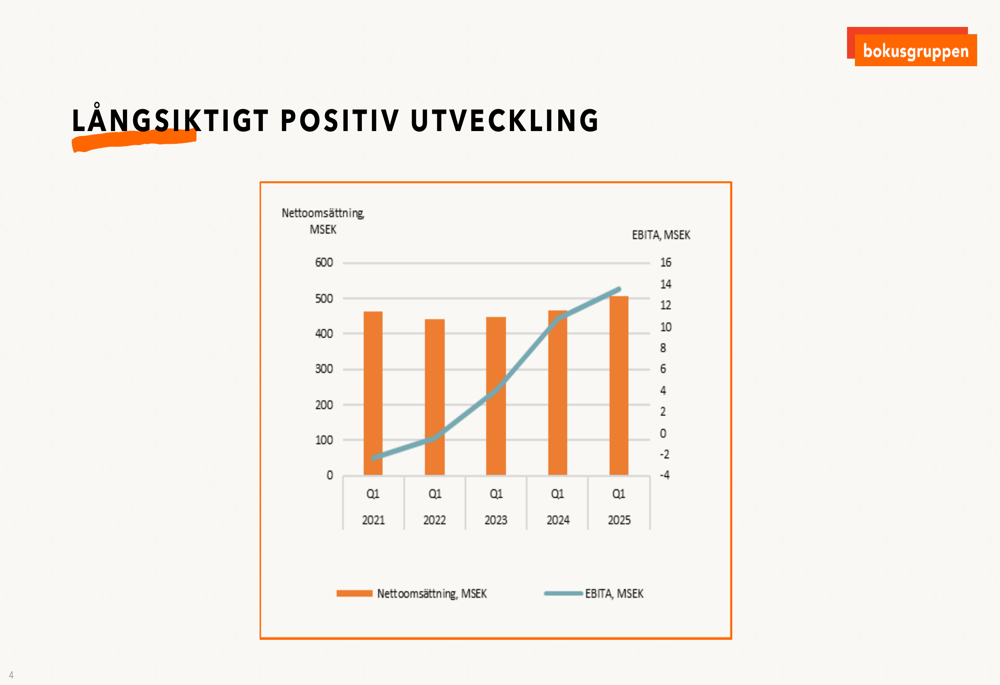

Bokusgruppen has demonstrated consistent improvement in its financial performance over the past several years. The following chart illustrates the company’s long-term positive development in both net sales and EBITA from Q1 2021 through Q1 2025:

The detailed financial results for Q1 2025 compared to Q1 2024, as well as rolling 12-month figures, show solid growth across most metrics:

While the company posted a loss after taxes of 3.8 MSEK for Q1 2025 (slightly worse than the 3.5 MSEK loss in Q1 2024), this appears to be in line with the company’s seasonal business pattern. The rolling 12-month profit after taxes stands at 41.7 MSEK, though this represents a decline from the 45.8 MSEK reported for the previous 12-month period.

Bokusgruppen maintains a strong financial position with a net debt to adjusted EBITA ratio of 0.6x and an equity ratio of 41% as of March 31, 2025. Based on the strong performance, the board has proposed increasing the dividend from 3.30 to 3.60 SEK per share.

Segment Performance

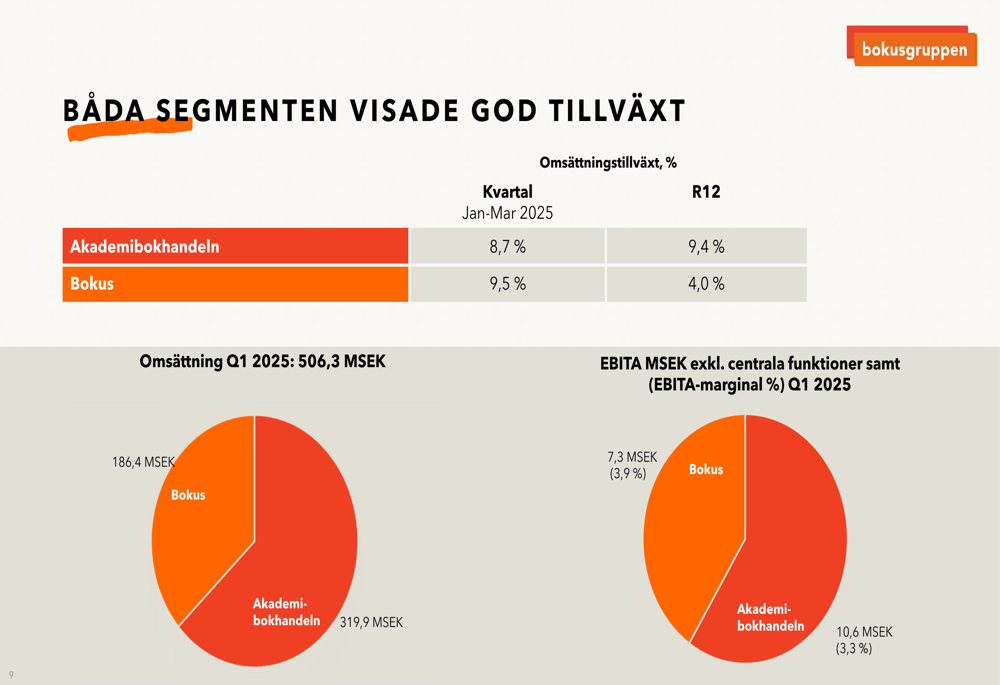

Both of Bokusgruppen’s main business segments contributed to the company’s growth in Q1 2025. The following chart breaks down the performance by segment:

Akademibokhandeln, the company’s physical and online bookstore chain, achieved 8.7% growth in Q1 2025 and 9.4% growth on a rolling 12-month basis. The segment’s physical store sales increased by 7.9% in Q1 2025, compared to 5.5% growth in Q1 2024. Online sales now represent 10.5% of Akademibokhandeln’s total sales, up from 9.8% in Q1 2024.

The number of active Akademibokhandeln customers has shown steady growth, reaching 1.533 million in Q1 2025, up from 1.472 million in Q1 2024.

Bokus, the company’s online bookstore and digital book service, grew by 9.5% in Q1 2025 and 4.0% on a rolling 12-month basis. Digital books were a particular bright spot, with 13.0% growth in Q1 2025. The segment maintained a strong Net Promoter Score (NPS) of 66 on a rolling 12-month basis.

The company noted that acquisitions were a significant driver of growth for the Bokus segment, though specific details about these acquisitions were not provided in the presentation.

Strategic Initiatives & Outlook

Bokusgruppen highlighted several strategic initiatives and provided an optimistic outlook for the remainder of 2025. The company reached a milestone in its e-commerce rollout with the completion of its first delivery (PIM), which appears to be part of a broader digital transformation strategy.

The company is making progress toward its financial goals, though with mixed results:

- Net sales growth: 7.6% on a rolling 12-month basis, exceeding the 4% target

- EBITA margin: 6.1% on a rolling 12-month basis, below the 8% target

- Return on Capital Employed (ROCE): 28.3% on a rolling 12-month basis, below the 35% target

Management expressed confidence about the company’s momentum heading into the rest of 2025, while acknowledging the uncertain and turbulent external environment. The company also mentioned a sustainability initiative called "Vässa pennan. Novelltävling for unga" (Sharpen the pencil. Short story competition for young people), though details were limited.

With continued growth in both physical and digital channels, along with the ongoing rollout of new e-commerce systems, Bokusgruppen appears well-positioned to continue its positive trajectory despite external challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.