Bitcoin price today: dips to $92k as Fed cut doubts spark risk-off mood

Introduction & Market Context

Booz Allen Hamilton (NYSE:BAH) presented its second quarter fiscal 2026 results on October 24, 2025, revealing significant revenue declines and a substantial downward revision to its full-year guidance. The company’s stock plummeted 9.4% in pre-market trading to $89.75, approaching its 52-week low of $88.12, as investors reacted to performance that fell short of expectations.

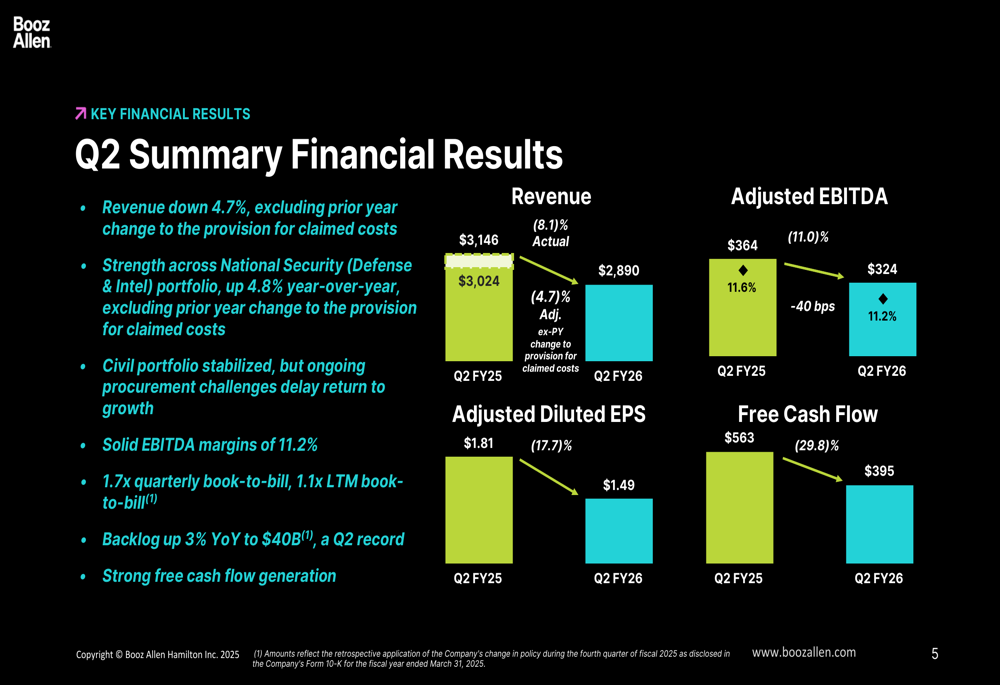

The global consulting firm reported quarterly revenue of $2.9 billion, representing an 8.1% year-over-year decline, while adjusted earnings per share came in at $1.49, missing analyst expectations of $1.53. The company’s performance reflects what CEO Horacio Rozanski described as "the most bifurcated environment" he has witnessed, with stark differences between the company’s national security and civil portfolios.

Quarterly Performance Highlights

Booz Allen’s Q2 FY26 results painted a mixed picture across its business segments. The National Security portfolio, encompassing Defense and Intelligence operations, demonstrated resilience with 4.8% year-over-year growth when excluding prior year changes to the provision for claimed costs. However, this strength was insufficient to offset broader challenges.

As shown in the following financial summary:

The company’s civil portfolio, while stabilized, continues to face procurement challenges that have delayed its return to growth. Despite these headwinds, Booz Allen maintained solid EBITDA margins of 11.2%, though this represents a 40 basis point decline from the previous year. The company also reported strong bookings with a quarterly book-to-bill ratio of 1.7x and a last-twelve-months ratio of 1.1x, contributing to a record Q2 backlog of $40 billion, up 3% year-over-year.

Net income saw a dramatic 55.1% decline to $175 million, reflecting the significant challenges the company faced during the quarter.

Detailed Financial Analysis

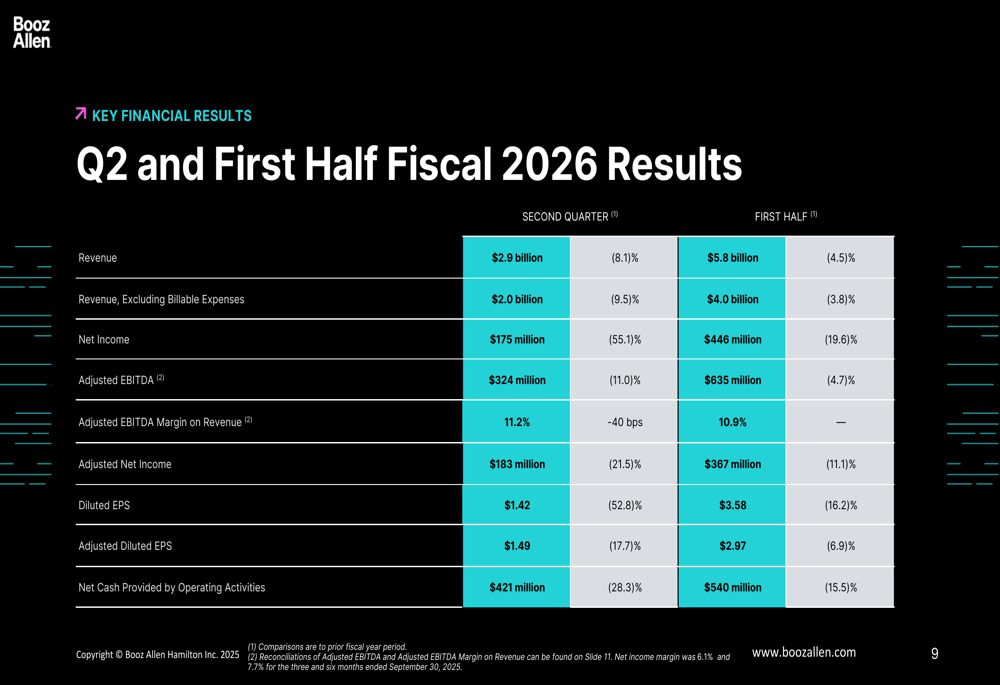

The company’s financial performance for both the second quarter and first half of fiscal 2026 shows consistent pressure across most metrics. Revenue excluding billable expenses declined 9.5% in Q2 to $2.0 billion, while adjusted EBITDA fell 11.0% to $324 million.

Free cash flow generation remained a relative bright spot, though still declining by 29.8% to $395 million. This cash flow performance has enabled the company to maintain its capital deployment strategy despite operational challenges.

The following detailed breakdown of Q2 and first half results provides additional context:

Despite the challenging environment, Booz Allen has maintained an active capital allocation approach, balancing shareholder returns with strategic investments. The company’s board approved a quarterly dividend of $0.55 per share, continuing its track record of dividend growth since 2013. Additionally, Booz Allen executed $208 million in share repurchases during the second quarter and increased its repurchase authorization by $500 million.

As illustrated in the capital deployment strategy:

The company also continued strategic investments in its technology ecosystem, including a $3 million deployment in SHIFT5 through Booz Allen Ventures. These investments align with the firm’s focus on maintaining technological leadership despite current market challenges. The company’s 2.5x net leverage ratio provides financial flexibility to pursue its strategic objectives.

Strategic Initiatives

Amid revenue challenges, Booz Allen emphasized its commitment to key growth vectors, particularly in national security-related technologies. The company is "doubling down" on proven growth areas including cyber, artificial intelligence, and warfighting technologies.

CEO Horacio Rozanski underscored this strategic focus, stating: "I am deeply committed to ensuring Booz Allen is an essential player in driving America’s technological superiority. I remain very optimistic about the future of our company."

The key takeaways from the presentation highlight these strategic priorities:

The company is taking "significant actions to reaccelerate growth and profitability," though specific details about these initiatives were limited in the presentation. Management acknowledged operating in a "bifurcated market" where funding levels have not normalized, particularly affecting the civil segment of the business.

Forward-Looking Statements

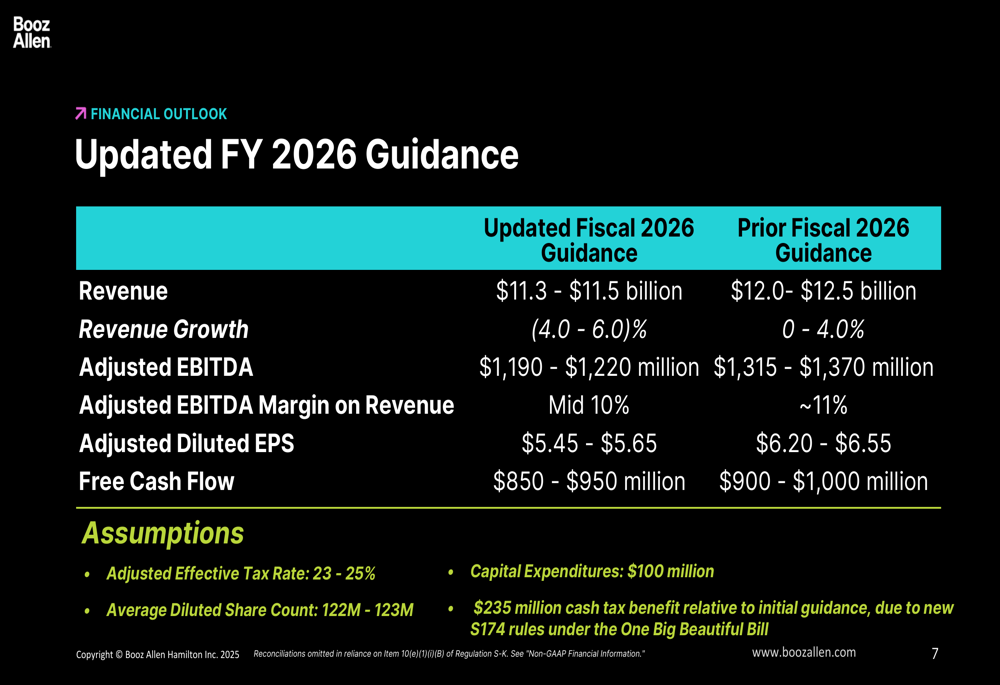

Perhaps most significantly, Booz Allen substantially revised its full-year guidance downward across all key metrics. The updated outlook reflects continued challenges, particularly in the civil portfolio.

The following revised guidance illustrates the magnitude of these adjustments:

Revenue expectations were slashed from $12.0-12.5 billion to $11.3-11.5 billion, representing a projected decline of 4-6% compared to the previous guidance of 0-4% growth. Adjusted EBITDA guidance was reduced from $1,315-1,370 million to $1,190-1,220 million, with margins expected in the mid-10% range versus the previous ~11% target.

Adjusted diluted EPS projections were cut from $6.20-6.55 to $5.45-5.65, reflecting the significant operational challenges the company faces. Free cash flow guidance was modestly reduced to $850-950 million from $900-1,000 million.

The company noted a $235 million cash tax benefit relative to initial guidance due to new S174 rules under recent legislation, which partially offsets some of the operational headwinds.

According to the earnings call, the civil business is expected to decline by low 20% for the year, while the national security portfolio is anticipated to grow mid-single digits, reinforcing the bifurcated nature of the company’s current market environment.

Despite these challenges, management expressed confidence in the company’s long-term positioning, particularly in high-demand areas like artificial intelligence and cybersecurity within the national security sector. The company’s record backlog provides some visibility into future revenue, though procurement delays and funding uncertainties continue to present significant challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.