BETA Technologies launches IPO of 25 million shares priced $27-$33

Introduction & Market Context

BorgWarner Inc (NYSE:BWA) presented its Q2 2025 investor presentation highlighting the company’s strategic positioning amid automotive industry transformation and challenging market conditions. The presentation comes after BorgWarner reported strong Q1 2025 results, with earnings per share of $1.11 exceeding analyst expectations of $0.98 and revenue reaching $3.52 billion against forecasted $3.41 billion.

The automotive supplier continues to navigate a complex landscape characterized by the industry’s shift toward electrification, while facing headwinds including tariff impacts estimated at over $200 million and a revised downward outlook for North American vehicle production by 7-12%.

Strategic Initiatives

BorgWarner’s presentation emphasized its balanced approach to the automotive industry’s transition, maintaining its vision of "a clean, energy-efficient world" while leveraging its diversified product portfolio across combustion, hybrid, and electric vehicle technologies.

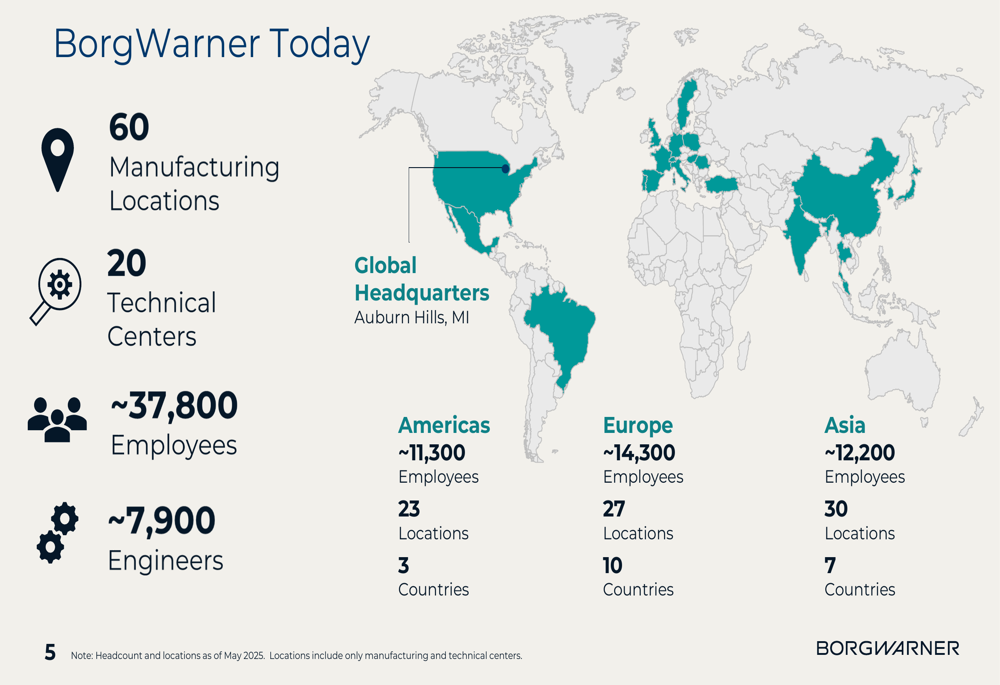

The company highlighted its global presence with 60 manufacturing locations and 20 technical centers employing approximately 37,800 people worldwide. This extensive footprint provides BorgWarner with significant operational flexibility and market access across key automotive regions.

As shown in the following regional breakdown of BorgWarner’s global operations:

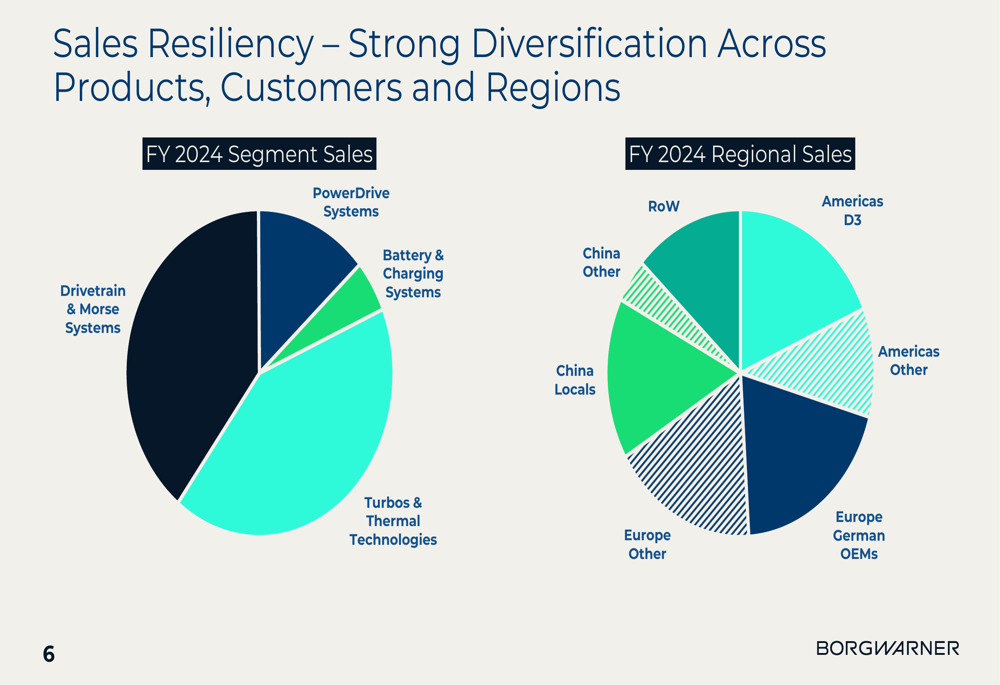

A key strategic focus for BorgWarner is its diversified sales across products, customers, and regions, providing resilience against market volatility. The FY 2024 data demonstrates how the company has balanced its revenue streams across different segments and geographic markets:

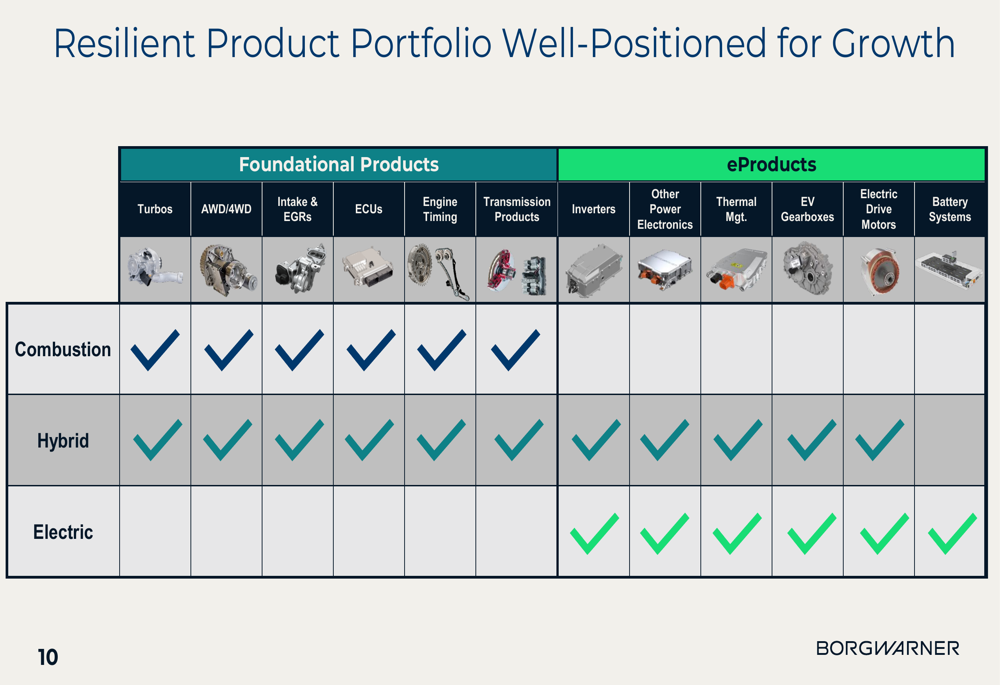

The company’s product strategy centers on maintaining leadership in foundational automotive components while aggressively expanding its electric vehicle offerings. BorgWarner claims #1 or #2 market share positions in its foundational products, with growing share in several electric products.

The presentation illustrated how BorgWarner’s portfolio is positioned across different powertrain technologies, demonstrating the company’s ability to serve traditional combustion, hybrid, and fully electric vehicles:

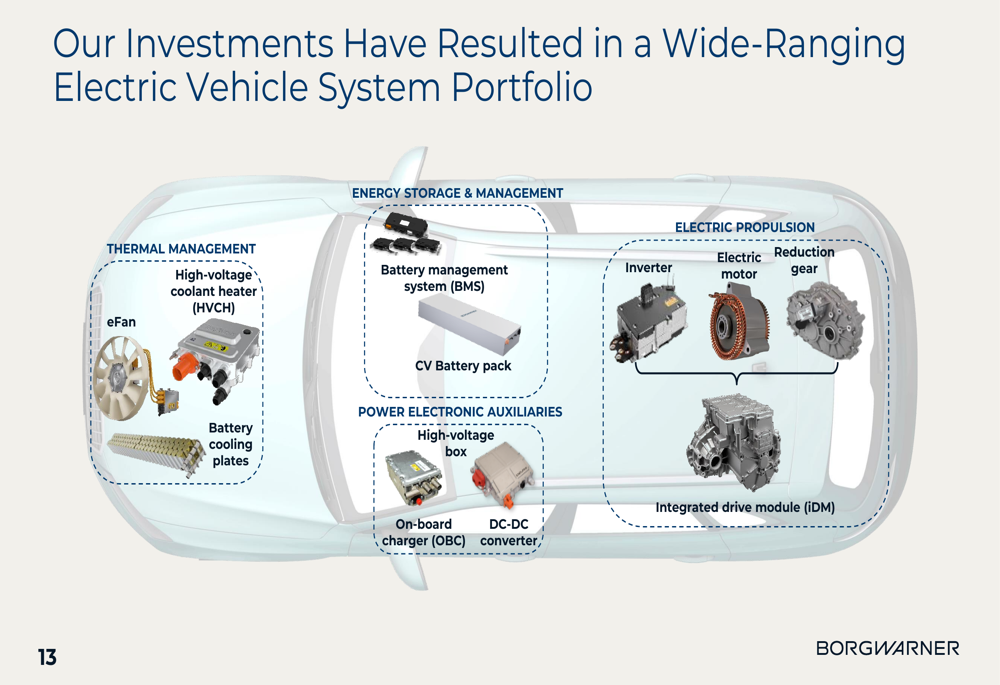

BorgWarner’s electric vehicle system portfolio encompasses a comprehensive range of components, positioning the company to capture significant value as the industry electrifies:

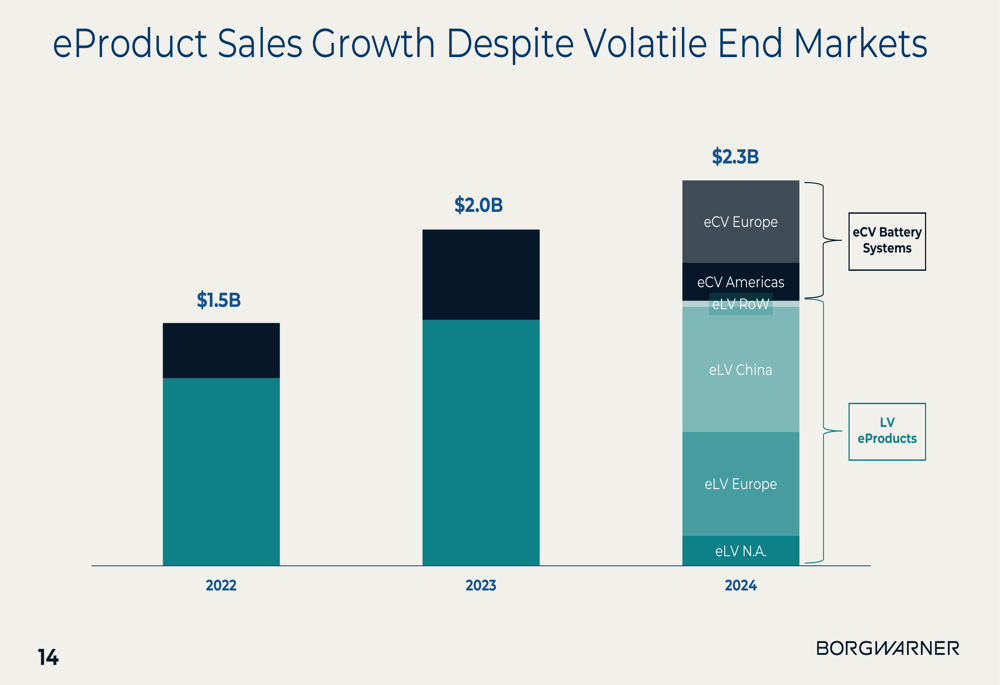

Despite market challenges, BorgWarner has achieved consistent growth in its electric product sales, reaching $2.3 billion in 2024, up from $2.0 billion in 2023 and $1.5 billion in 2022:

Operational Adjustments

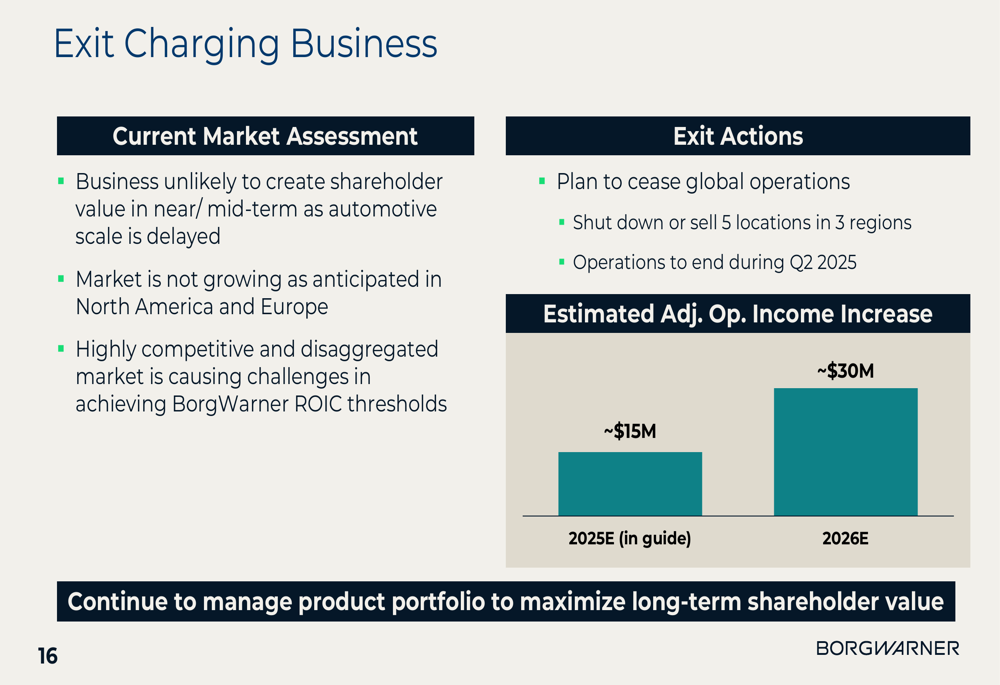

A significant announcement in the presentation was BorgWarner’s decision to exit the charging business, citing unfavorable market conditions. The company stated that the business was "unlikely to create shareholder value in the near/mid-term" due to slower-than-anticipated market growth and a highly competitive landscape. Operations are expected to end during Q2 2025, with the exit projected to increase adjusted operating income by approximately $15 million in 2025 and $30 million in 2026.

The strategic rationale and financial impact of exiting the charging business is detailed in the following slide:

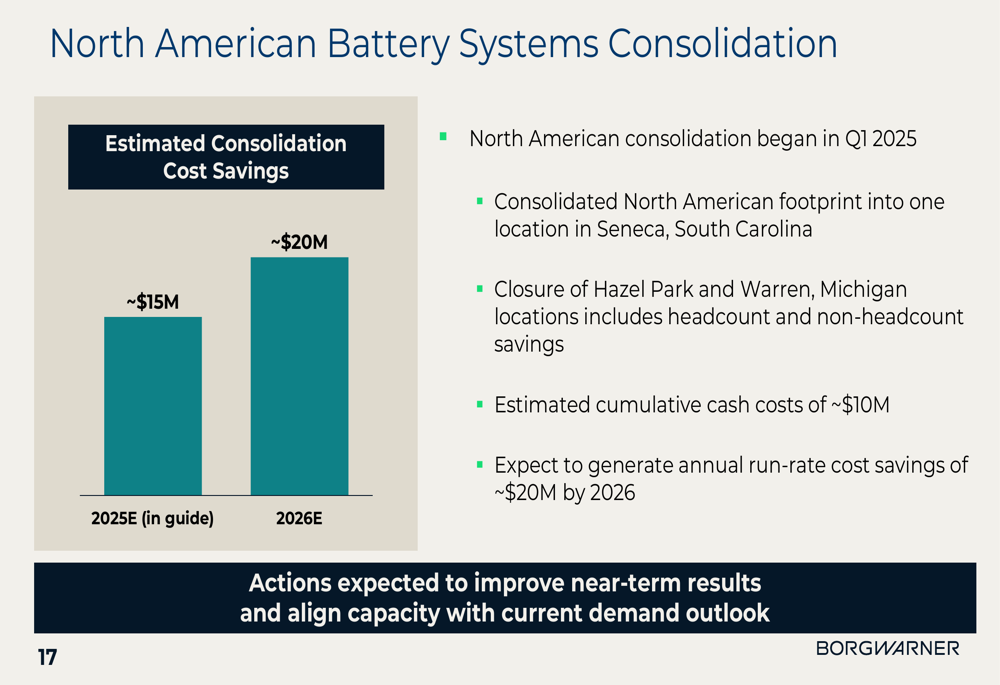

Additionally, BorgWarner is consolidating its North American battery systems operations into a single location in Seneca, South Carolina, closing facilities in Hazel Park and Warren, Michigan. This consolidation, which began in Q1 2025, is expected to generate annual run-rate cost savings of approximately $20 million by 2026:

Financial Performance & Outlook

BorgWarner’s Q1 2025 performance showed resilience with revenue of $3.52 billion and an adjusted operating margin of 10%. The company’s stock rose by 3.84% following the earnings announcement, reflecting positive investor sentiment.

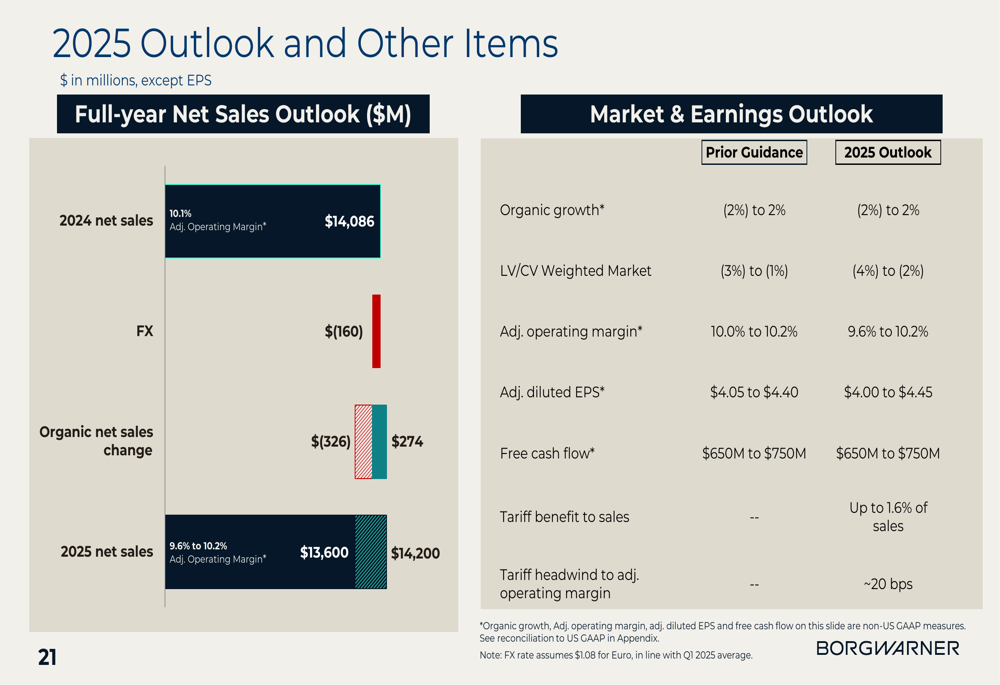

For the full year 2025, BorgWarner provided the following financial outlook:

This guidance reflects a cautious approach to market conditions, with projected net sales of $13.6 billion to $14.2 billion compared to $14.086 billion in 2024. The company expects organic growth between -2% and 2%, against a light vehicle and commercial vehicle weighted market decline of -4% to -2%.

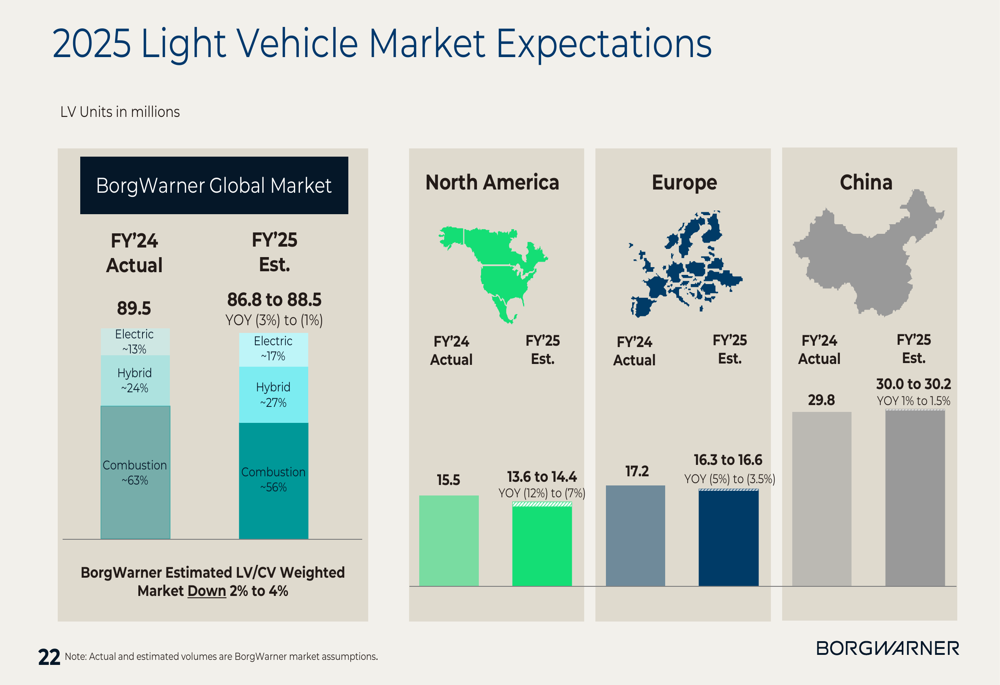

BorgWarner’s light vehicle market expectations for 2025 indicate a challenging environment, with global production projected to decline from 89.5 million units in 2024 to between 86.8 and 88.5 million units in 2025:

Growth Opportunities

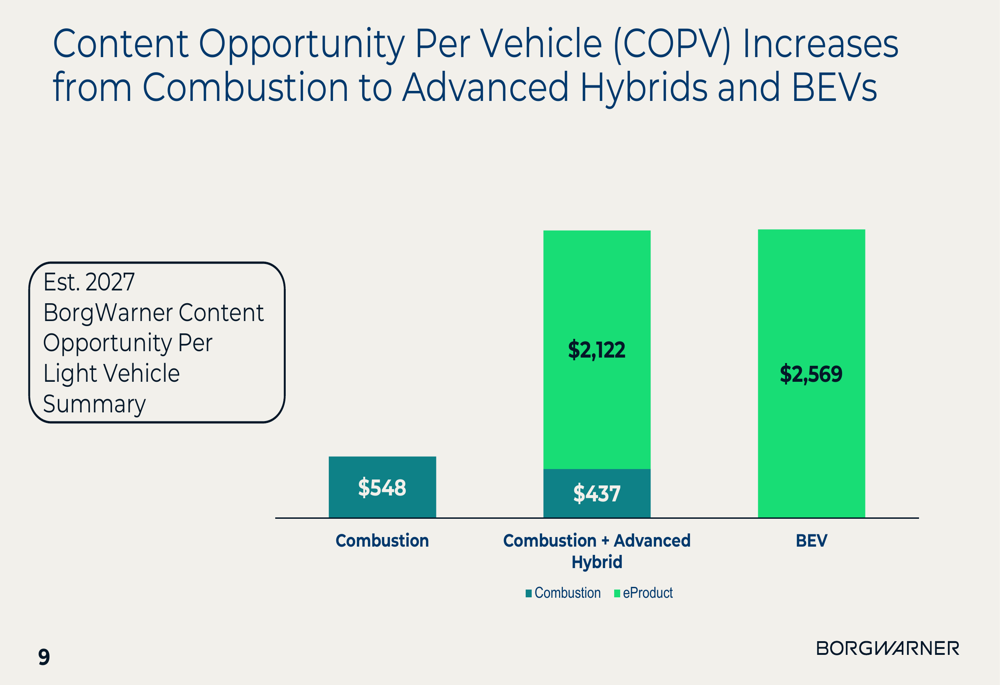

Despite market headwinds, BorgWarner highlighted significant growth opportunities, particularly in the electrification space. The company’s content opportunity per vehicle (COPV) increases substantially as vehicles transition from combustion engines to hybrids and battery electric vehicles:

The presentation showed that BorgWarner’s estimated COPV for 2027 increases from $548 for combustion vehicles to $2,122 for advanced hybrids and $2,569 for battery electric vehicles, representing a substantial revenue growth opportunity as the market electrifies.

The company also identified growth opportunities within its foundational product portfolio, particularly in regions with lower penetration rates for certain technologies. For example, North American turbocharger penetration stands at 51% compared to 93% in Europe and 70% in China, while China’s all-wheel drive penetration is just 9% compared to 54% in North America.

Forward-Looking Statements

BorgWarner’s presentation outlined three key focus areas for 2025 and beyond: outgrowing end markets by leveraging core competencies, building on the existing product portfolio through organic and inorganic investments, and driving enhanced financial performance through margin expansion and cash generation.

The company’s capital allocation strategy from 2020-2024 demonstrates a balanced approach, with 57% directed toward M&A, 21% to share buybacks, 14% to dividends, and 8% to non-controlling interest dividends, totaling $4.9 billion.

Looking ahead, BorgWarner faces several challenges, including potential tariff impacts, declining vehicle production, and ongoing industry electrification. However, the company’s diversified portfolio, global presence, and strategic operational adjustments position it to navigate these headwinds while capitalizing on the long-term electrification trend in the automotive industry.

During the Q1 2025 earnings call, CEO Joe expressed confidence in the company’s direction, stating, "We have the right portfolio, a decentralized operating model, and the financial strength to deliver our revised guidance and drive long-term profitable growth." This sentiment was echoed by CFO Craig, who noted, "Our sales outgrowth, margin, and free cash flow performance represents a strong start to the year."

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.