Gold prices steady ahead of Fed decision; weekly weakness noted

Introduction & Market Context

Bharat Petroleum Corporation Limited (NSE:BPCL), India’s second-largest oil marketing company, delivered a robust financial performance in Q4 FY25, driven by strong gross refining margins (GRMs) and operational efficiency. The company’s investor presentation, released in April 2025, outlines BPCL’s strategic roadmap focusing on both core business growth and future-oriented investments in petrochemicals and green energy.

With a market capitalization of $16.17 billion and a current stock price of INR 332.90 (as of July 28, 2025), BPCL continues to strengthen its position in India’s energy landscape. The company’s shares have shown positive momentum, up 0.63% in recent trading, reflecting investor confidence in its strategic direction.

Financial Performance Highlights

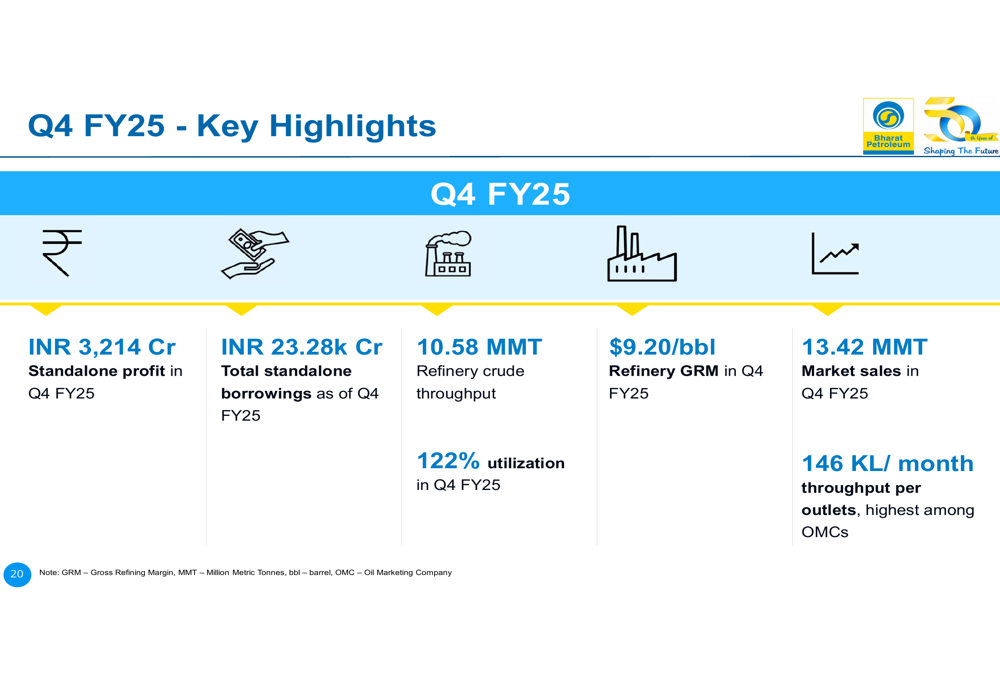

BPCL reported impressive financial results for both Q4 FY25 and the full fiscal year. The standalone profit for Q4 FY25 stood at INR 3,214 crore, significantly exceeding analyst expectations. This strong performance was largely driven by exceptional refining margins of $9.20/bbl for the quarter.

As shown in the following quarterly performance highlights:

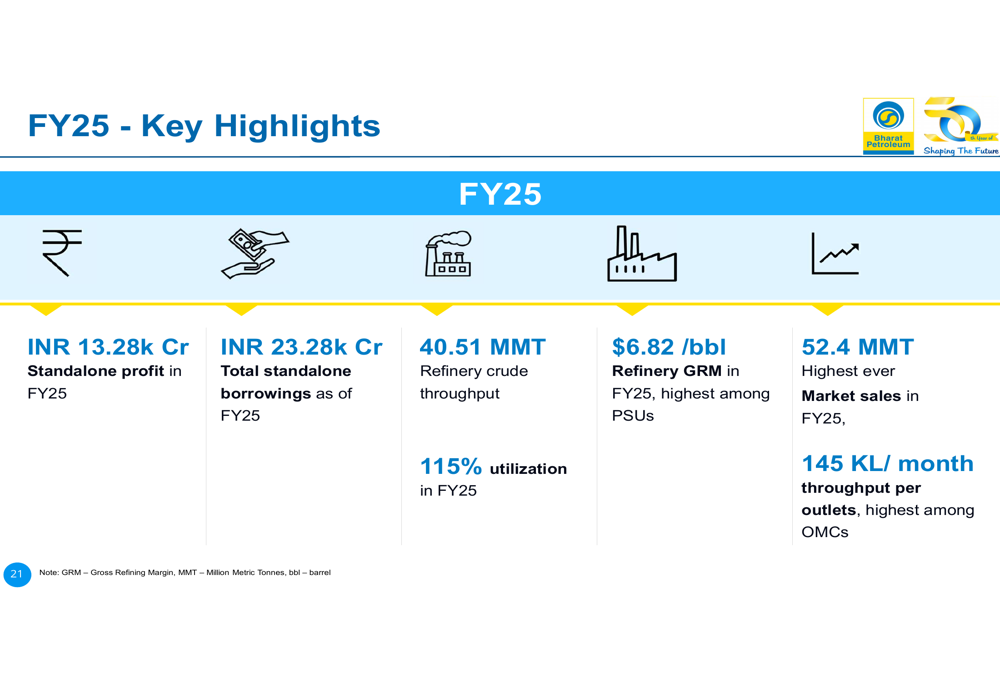

For the full fiscal year FY25, BPCL achieved a standalone profit of INR 13.28k crore, with total market sales reaching 52.4 MMT. The company maintained industry-leading refinery utilization rates of 115% with a crude throughput of 40.51 MMT, demonstrating operational excellence across its facilities.

The annual performance metrics showcase BPCL’s consistent delivery:

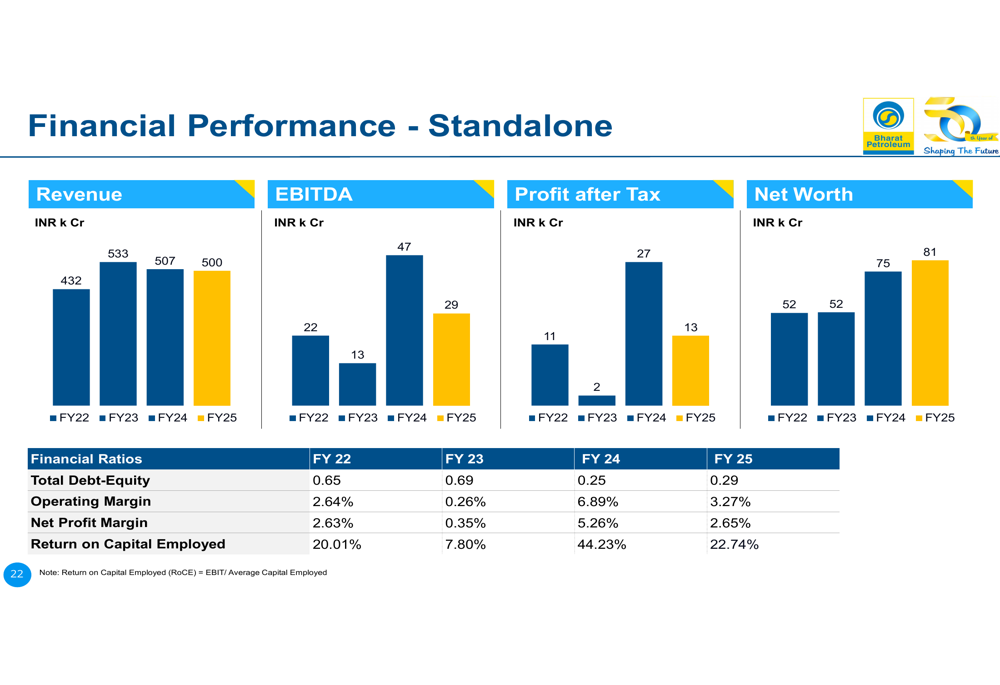

BPCL’s financial health remains robust, with a Return on Capital Employed (ROCE) of 22.74% on a standalone basis for FY25. The company’s operating margin and net profit margin have shown steady improvement over the past four years, as illustrated in the following financial performance chart:

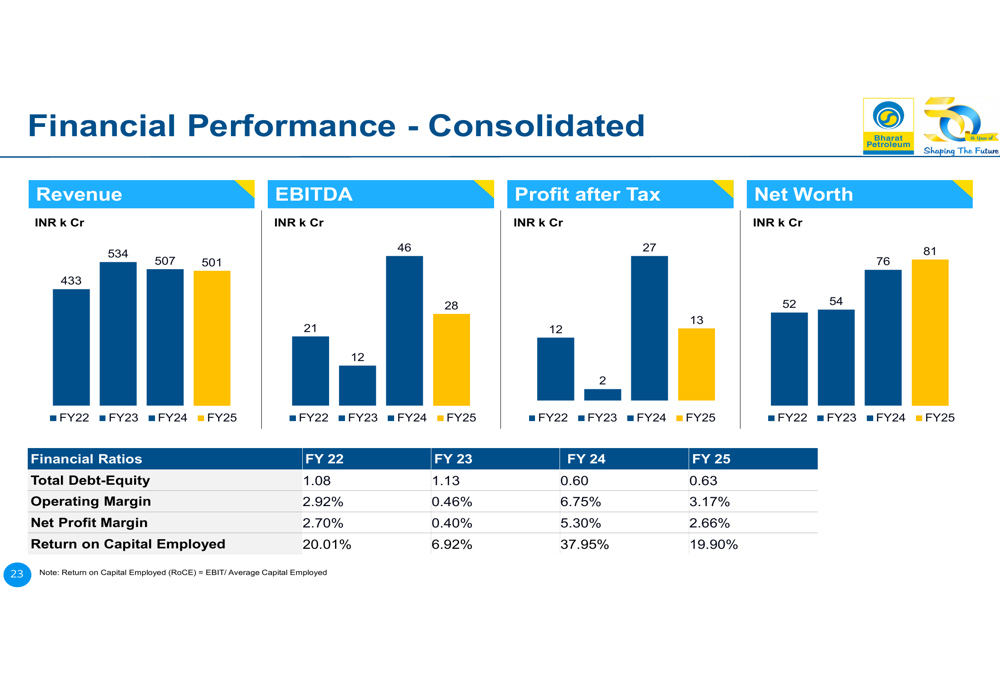

On a consolidated basis, BPCL reported revenue of INR 5,03,202 crore for FY25, with a profit after tax of INR 13,337 crore. This represents a compound annual growth rate (CAGR) of 8.5% for revenue and 21.44% for PAT over the past 15 years, underscoring the company’s consistent long-term performance.

Strategic Initiatives and Capex Plans

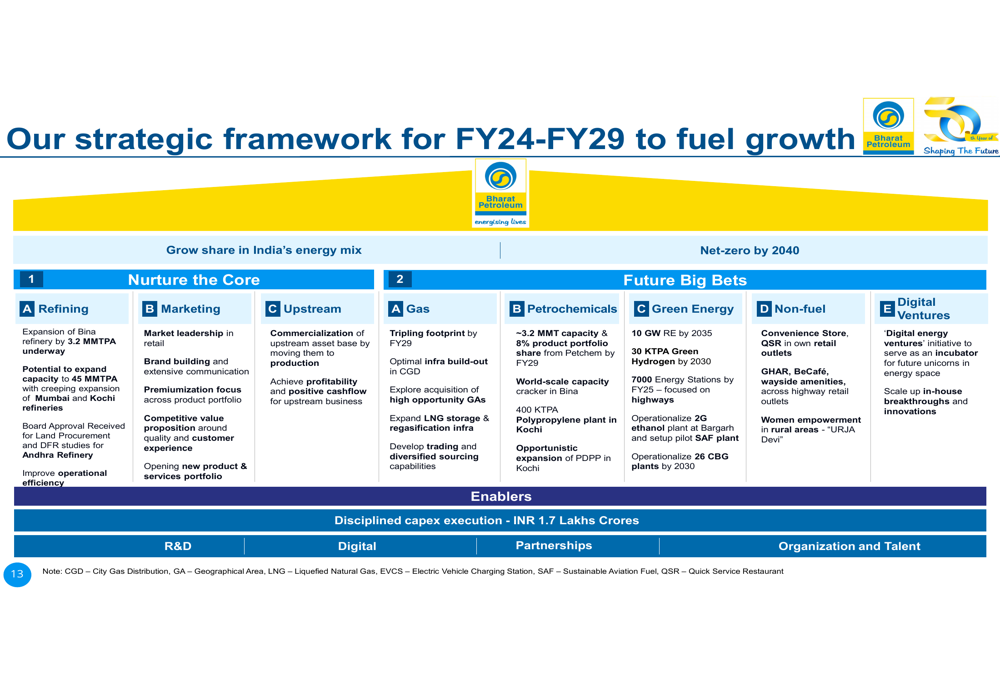

BPCL has outlined an ambitious strategic framework for FY24-FY29, focusing on growing its share in India’s energy mix while working toward achieving net-zero emissions by 2040. The strategy balances nurturing core businesses (Refining, Marketing, Upstream) with investments in future growth areas like Gas, Petrochemicals, Green Energy, and Digital Ventures.

The company’s strategic roadmap is clearly defined in the following framework:

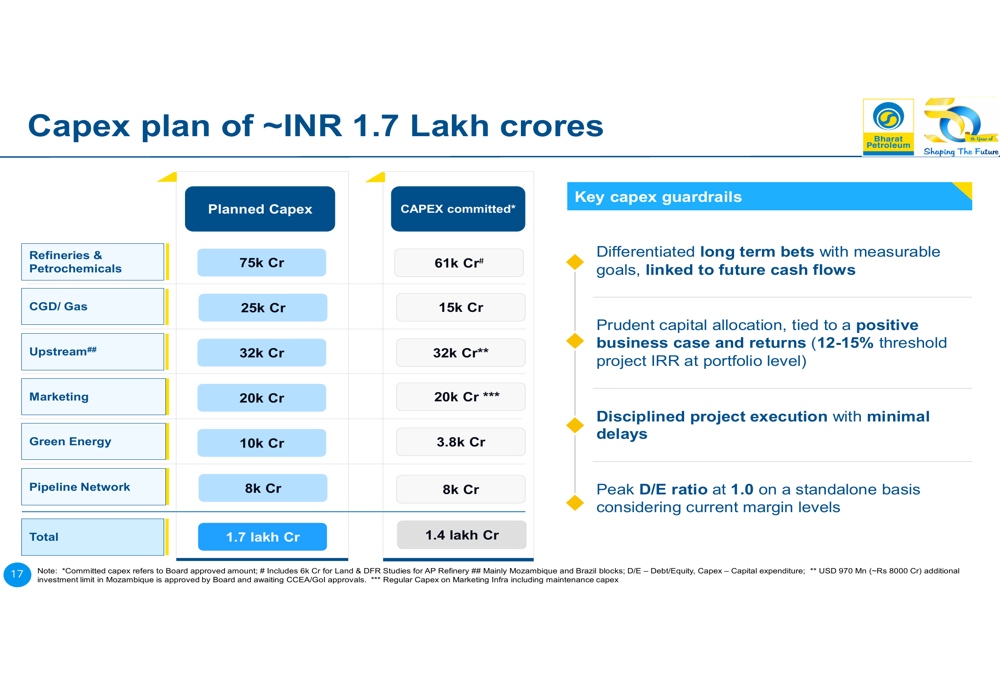

To execute this strategy, BPCL has announced a substantial capex plan of approximately INR 1.7 lakh crores. The largest allocation (INR 75,000 crores) is earmarked for Refineries & Petrochemicals, highlighting the company’s focus on value-added products. Other significant investments include INR 32,000 crores for Upstream, INR 25,000 crores for CGD/Gas, and INR 10,000 crores for Green Energy initiatives.

The detailed capex allocation demonstrates BPCL’s balanced approach to future growth:

This capex plan aligns with the guidance provided during BPCL’s recent earnings call, where management outlined a progressive increase in capital expenditure from INR 16,400 crore in FY 2025 to INR 30,000 crore in subsequent years.

Refining and Marketing Strengths

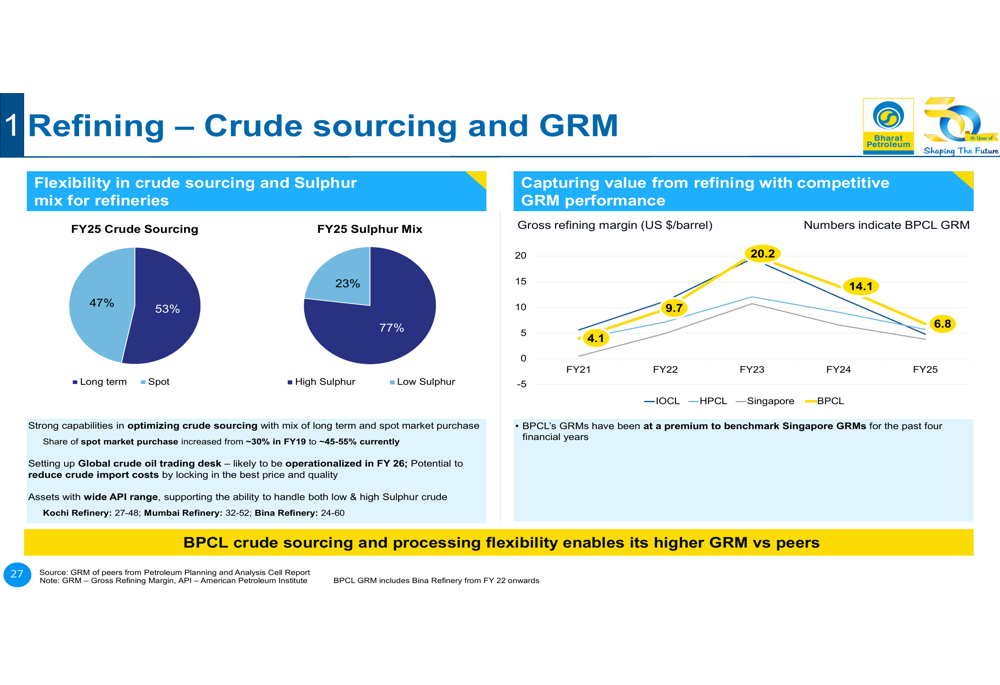

BPCL’s refining operations continue to be a key strength, with the company consistently outperforming competitors in terms of gross refining margins (GRMs). The company’s flexibility in crude sourcing and superior refining capabilities have enabled it to maintain GRMs above the Singapore benchmark for the past four financial years.

The following chart illustrates BPCL’s superior GRM performance compared to competitors:

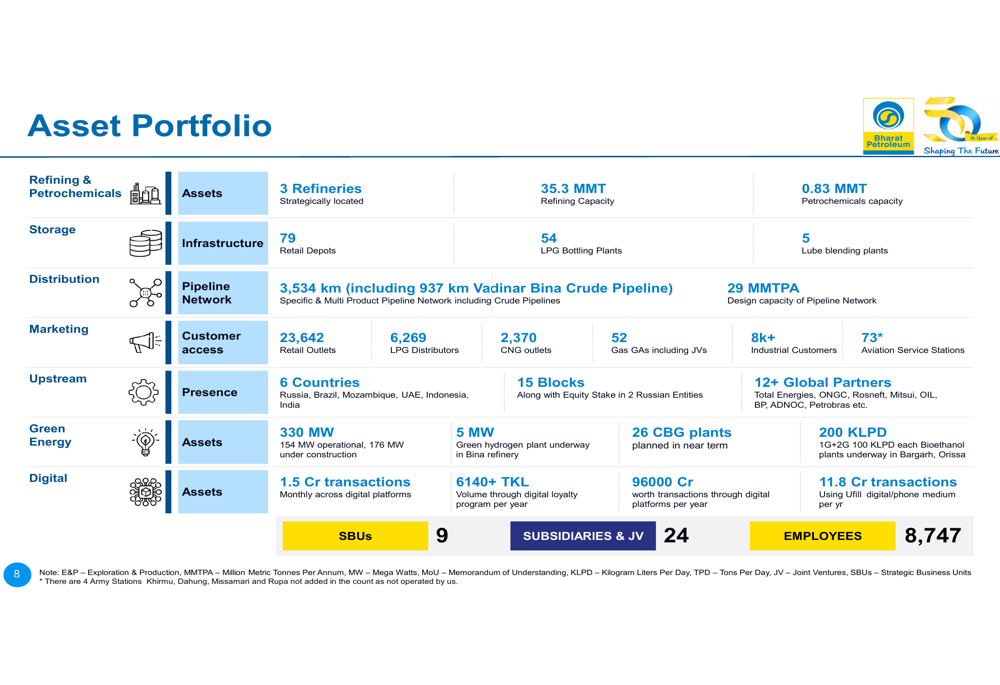

BPCL operates three refineries with a combined capacity of 35.3 MMTPA, achieving impressive utilization rates: Mumbai Refinery (130%), Kochi Refinery (111%), and Bina Refinery (99%). These high utilization rates reflect the operational efficiency and technical capabilities of BPCL’s refining assets.

In the marketing segment, BPCL has strengthened its position as the second-largest oil marketing company in India with a domestic market share of 27.44% in FY25. The company’s retail network achieved the highest throughput per outlet in the industry at 145 KL/month, demonstrating superior efficiency and customer reach.

Future Growth Areas: Petrochemicals and Green Energy

BPCL is strategically expanding its petrochemicals business to capture higher margins and reduce dependence on traditional fuel products. The company plans to increase its petrochemical capacity from the current 0.83 MMTPA to 3.2 MMTPA by FY29, representing approximately 8% of its product portfolio.

A major initiative in this direction is the Ethylene Cracker Project at Bina Refinery, with an investment of approximately INR 50,000 crores and a capacity of 2.2 MMTPA of bulk petrochemicals, expected to be commissioned by 2028.

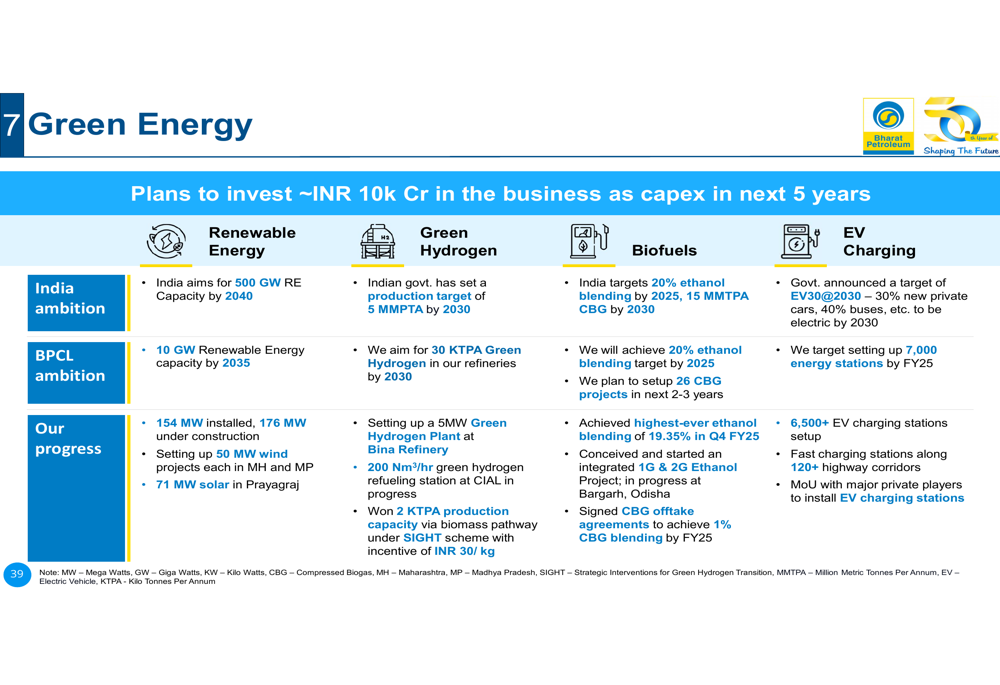

Simultaneously, BPCL is making significant strides in green energy, with a comprehensive roadmap to achieve net-zero emissions for Scope 1 and Scope 2 by 2040. The company plans to invest approximately INR 10,000 crores in green energy initiatives over the next five years.

The following slide outlines BPCL’s green energy strategy:

The company’s green energy initiatives span renewable energy, green hydrogen, biofuels, and EV charging infrastructure. BPCL has already achieved its highest-ever ethanol blending rate of 16.35% in FY25, demonstrating tangible progress in its sustainability goals.

Forward-Looking Statements

BPCL’s presentation outlines an optimistic outlook for the company, with a clear focus on balancing traditional energy business growth with future-oriented investments. The company’s asset portfolio, which includes 23,642 retail outlets, 6,269 LPG distributors, and 2,370 CNG outlets, provides a strong foundation for sustained growth.

Looking ahead, BPCL faces both opportunities and challenges. The company’s ambitious capex plans will require disciplined execution, particularly for major projects like the Ethylene Cracker at Bina Refinery. Additionally, the transition toward green energy will need to be carefully managed to ensure it complements rather than cannibalizes the core business.

During the recent earnings call, management expressed optimism about government mechanisms for LPG compensation and highlighted the increasing use of Russian crude, which constituted 24% of Q4 processing and is expected to rise to 30-32%, potentially supporting continued strong refining margins.

With its robust financial performance, clear strategic direction, and balanced approach to future growth, BPCL appears well-positioned to navigate the evolving energy landscape while delivering value to shareholders through both dividends and capital appreciation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.