Street Calls of the Week

Introduction & Market Context

Braemar Hotels & Resorts (NYSE:BHR) released its second quarter 2025 earnings presentation showing modest RevPAR growth translating into stronger EBITDA performance, with luxury resorts continuing to be the primary driver of results. Despite operational improvements, the company’s stock has faced pressure, declining 5% following the earnings announcement despite beating analyst expectations.

The company reported a net loss attributable to common stockholders of $16.0 million or $0.24 per diluted share, which was better than the forecasted loss of $0.40 per share. Total (EPA:TTEF) hotel revenue reached $179.9 million, representing a 3.3% increase year-over-year and exceeding analyst expectations of $172.56 million.

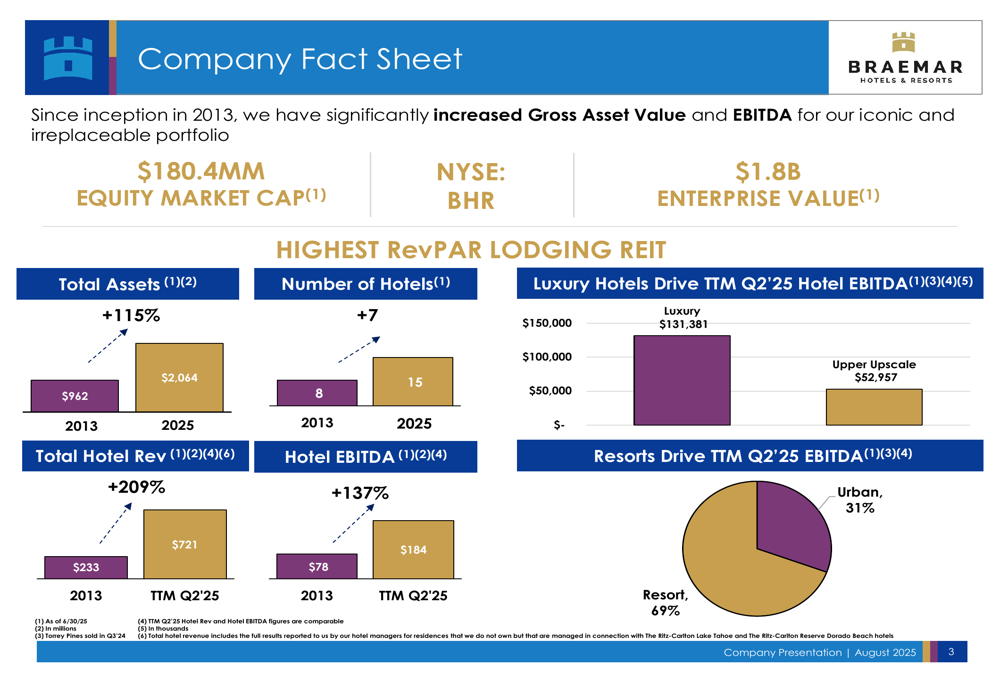

As shown in the following company fact sheet, Braemar has significantly grown its portfolio and financial metrics since its inception in 2013:

Quarterly Performance Highlights

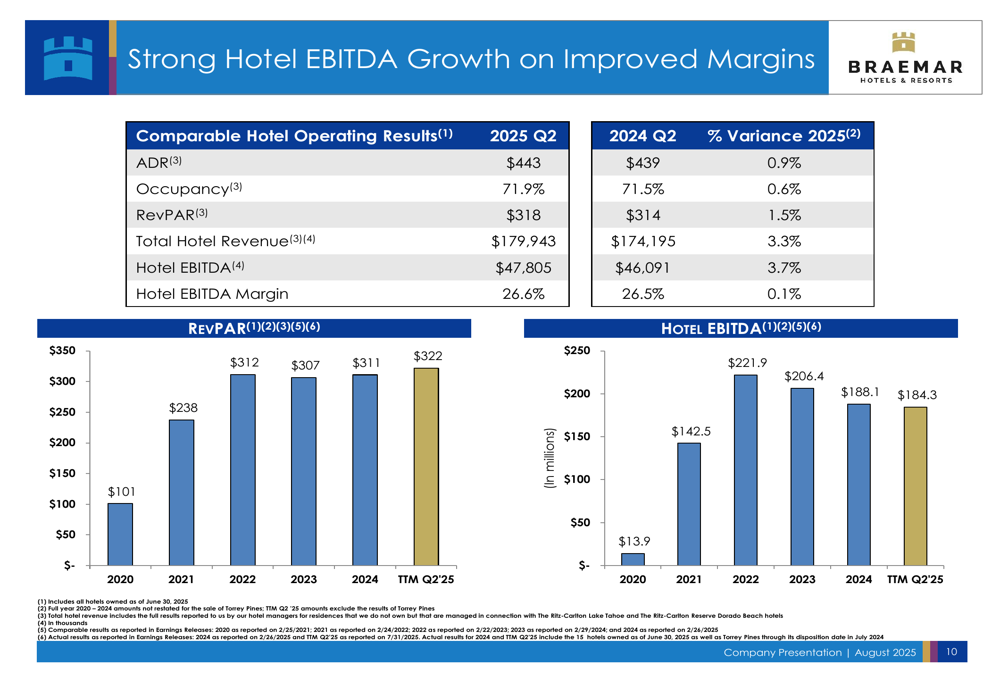

Braemar’s Q2 2025 results demonstrated the company’s ability to translate modest RevPAR growth into stronger EBITDA performance. Key operational metrics showed improvement across the board, with RevPAR increasing 1.5% to $318, ADR rising 0.9% to $443, and occupancy improving 0.6% to 71.9%. This translated to a 3.7% increase in Hotel EBITDA to $47.8 million and a slight improvement in Hotel EBITDA margin to 26.6%.

The following chart illustrates the company’s strong Hotel EBITDA growth on improved margins:

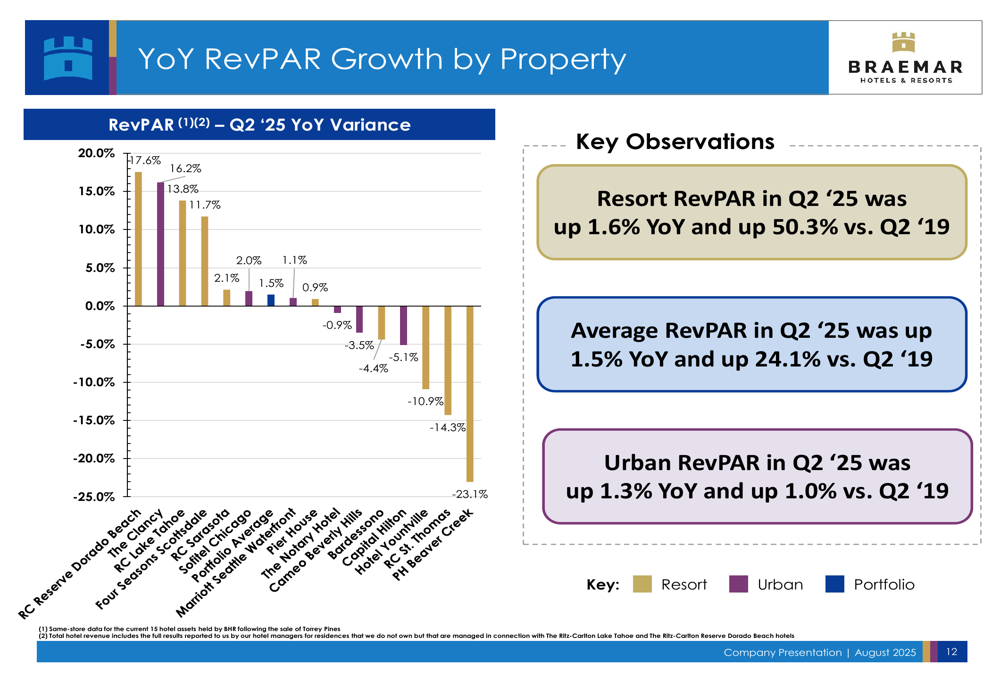

Performance varied significantly across the portfolio, with resorts posting strong year-over-year EBITDA growth of 6.9%, while urban properties were relatively flat with just 0.3% growth. The best performing properties were The Clancy, which benefited from a stronger conference calendar and improved market share, and Ritz-Carlton Lake Tahoe, which is rebounding from a renovation last year. Conversely, The Cameo struggled in the aftermath of LA wildfires, and Park Hyatt Beaver Creek was under renovation.

The property-by-property RevPAR performance is illustrated in the following chart:

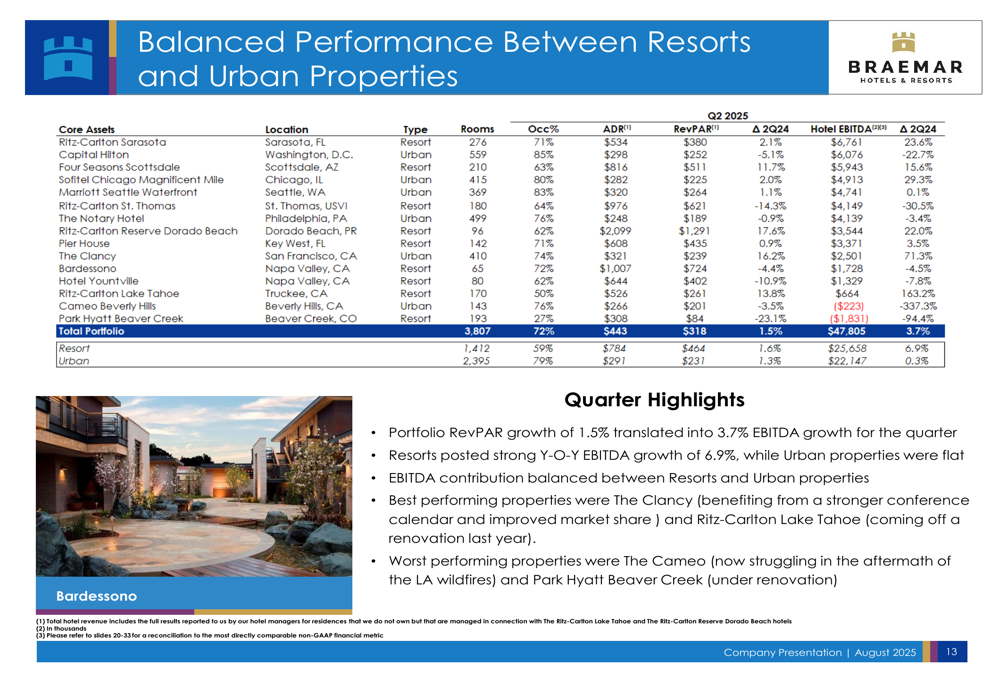

Braemar’s portfolio demonstrates a balanced performance between resort and urban properties, though resorts continue to drive higher ADR and RevPAR. The following slide provides a comprehensive overview of the portfolio’s performance:

Industry Positioning

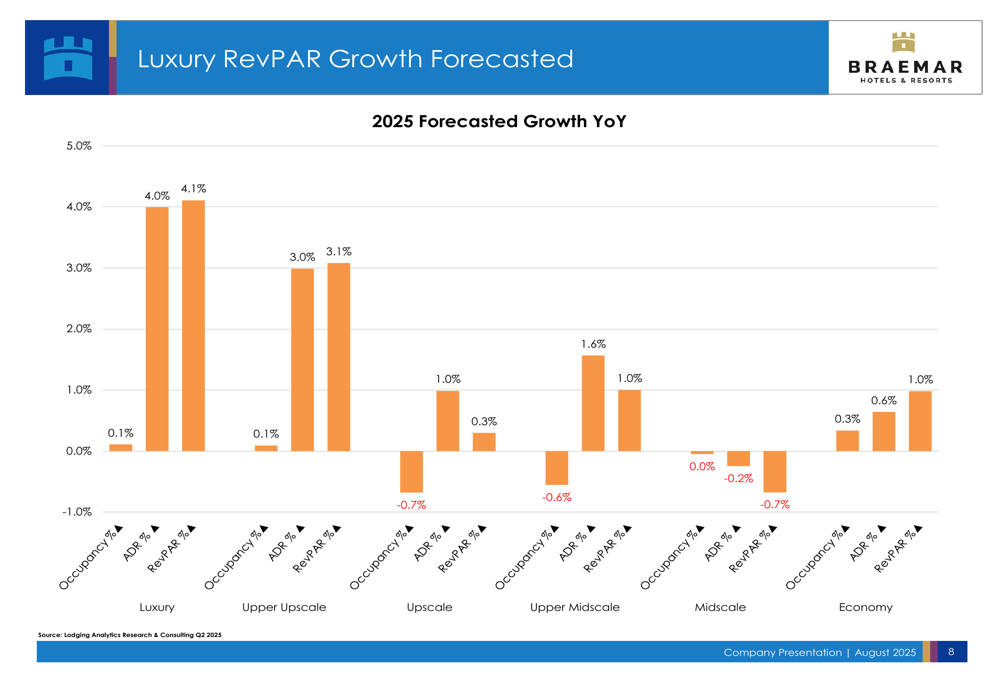

Braemar’s strategic focus on luxury hotels and resorts continues to position the company favorably within the industry. The luxury segment is forecasted to outperform other hotel categories in 2025, with projected RevPAR growth of 4.1%, significantly higher than other segments.

The following chart illustrates the forecasted RevPAR growth by hotel category:

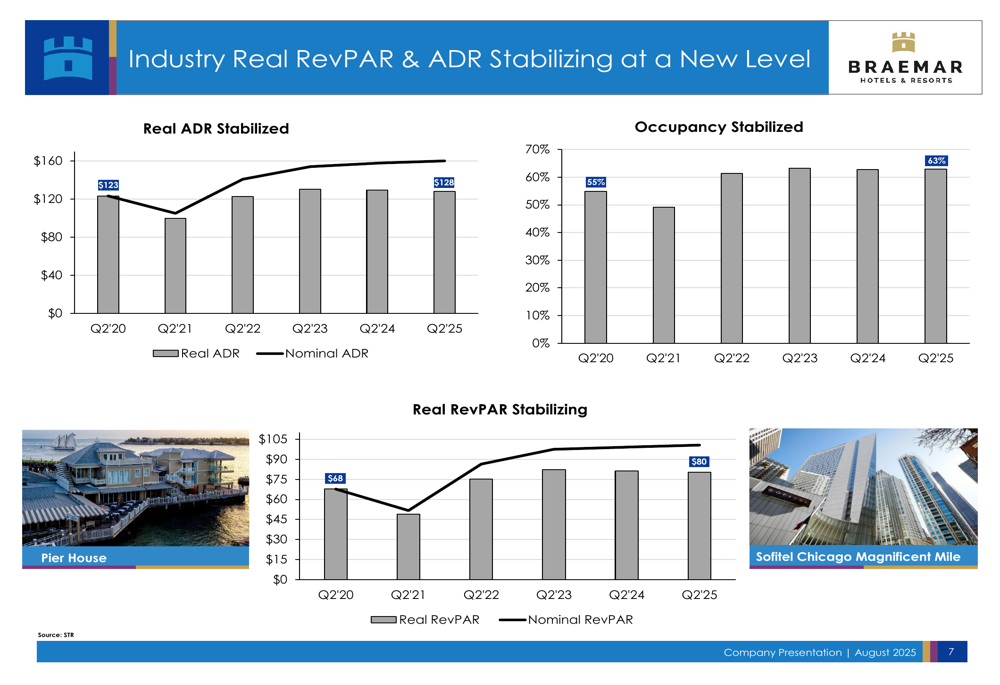

Industry RevPAR continues to exceed 2019 levels, with 2025 forecasted to be 17% above pre-pandemic performance. This is primarily driven by ADR strength, as occupancy remains slightly below 2019 levels.

As shown in the following chart, industry RevPAR and ADR are stabilizing at a new, higher level:

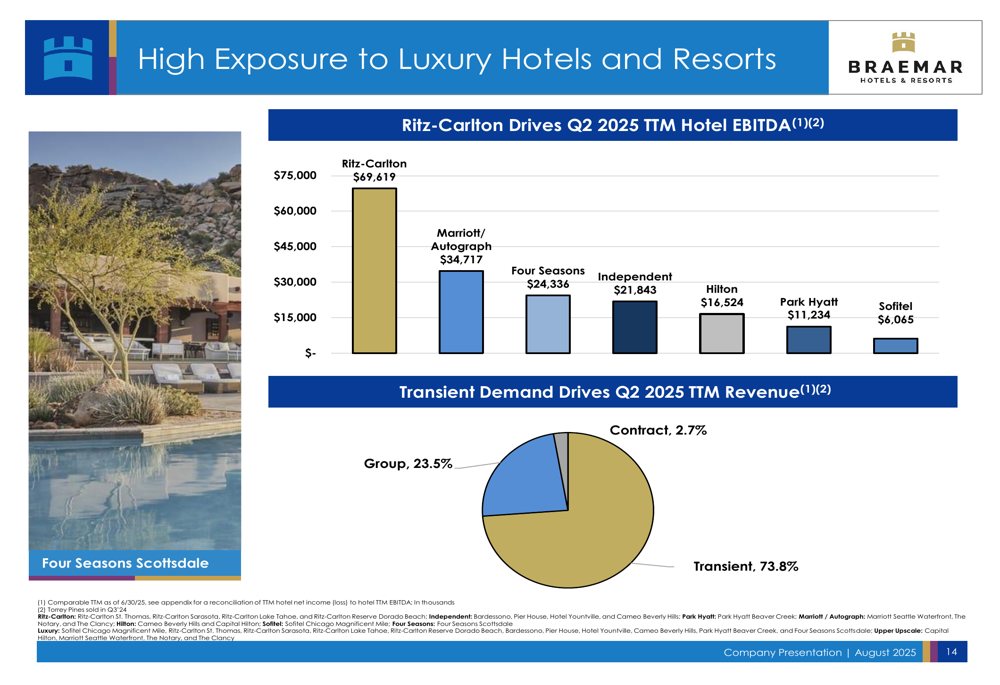

Braemar’s high exposure to luxury hotels and resorts, particularly the Ritz-Carlton brand, continues to be a key driver of the company’s performance. The following chart shows the breakdown of EBITDA contribution by brand:

Strategic Initiatives

Braemar is planning significant capital expenditures in 2025, with a range of $75-95 million allocated to various renovation projects. Key projects include guestroom renovations at Hotel Yountville and Park Hyatt Beaver Creek, a Café Blue renovation at Ritz-Carlton Lake Tahoe, and a Hilton LXR conversion at Cameo Beverly Hills.

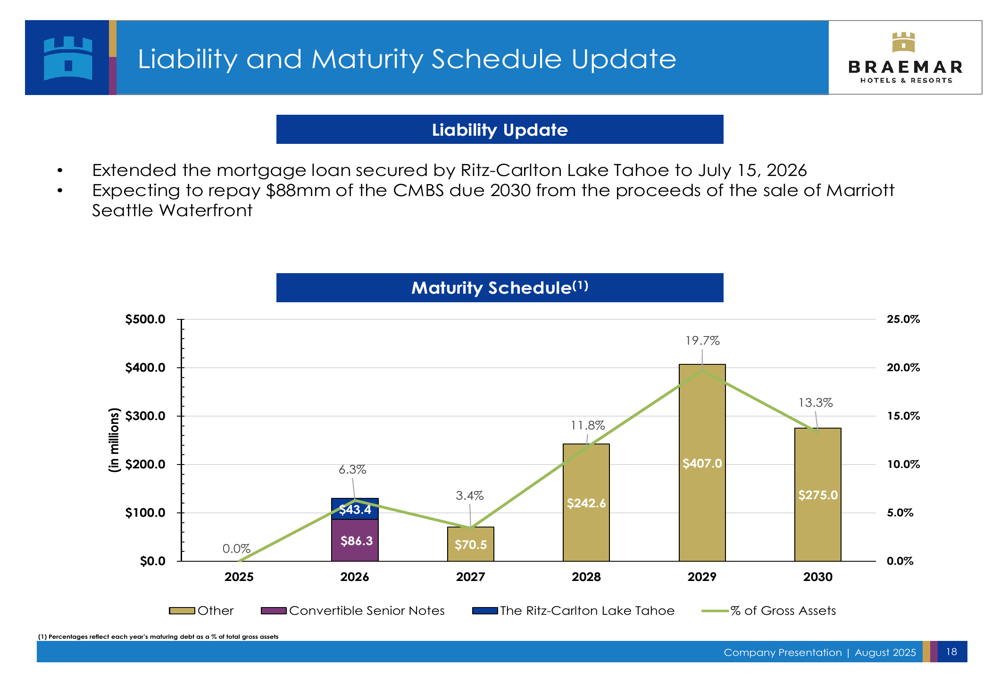

On the liability management front, Braemar has extended the mortgage loan secured by Ritz-Carlton Lake Tahoe to July 15, 2026, and is expecting to repay $88 million of CMBS due in 2030 from the proceeds of the sale of Marriott Seattle Waterfront. The company’s maturity schedule shows limited near-term maturities, with most debt coming due in 2028 and beyond.

The following chart provides an overview of the company’s liability and maturity schedule:

Forward-Looking Statements

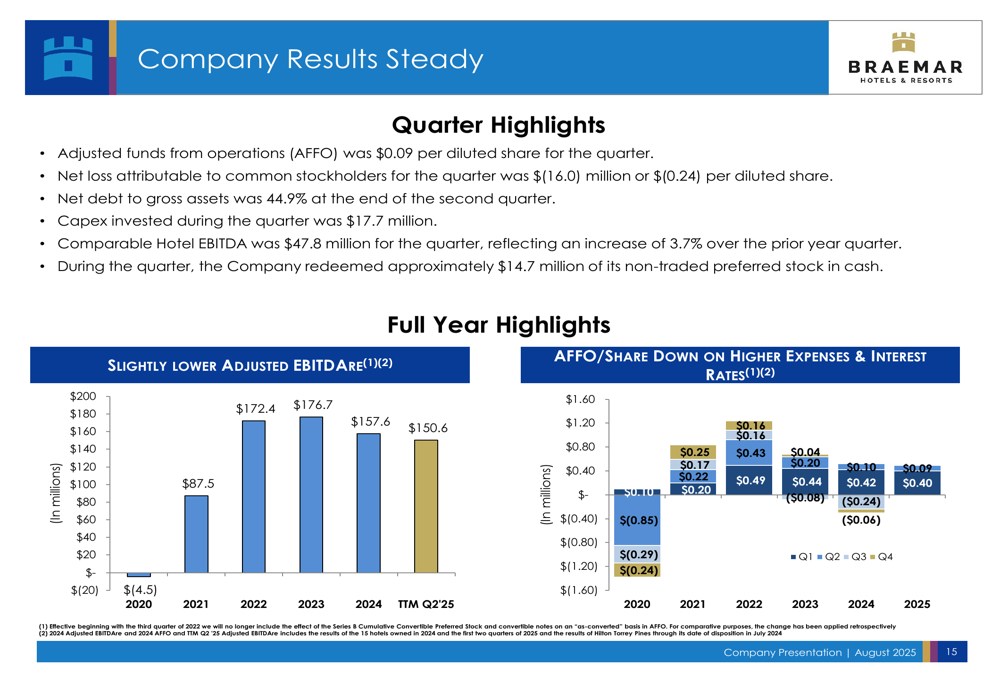

Despite operational improvements, Braemar continues to face challenges with its high debt levels, with net debt to gross assets at 44.9% at the end of the second quarter. The company redeemed approximately $14.7 million of its non-traded preferred stock in cash during the quarter, demonstrating a commitment to managing its capital structure.

The company’s adjusted funds from operations (AFFO) was $0.09 per diluted share for the quarter. However, as shown in the following chart, AFFO per share has been impacted by higher expenses and interest rates:

Looking ahead, Braemar is well-positioned to benefit from the continued strength in the luxury segment, particularly in resort destinations. The company’s balanced portfolio between resort and urban properties provides some diversification, though resorts continue to drive the majority of EBITDA.

Market reaction to Braemar’s results has been mixed, with the stock declining 5% following the earnings announcement despite beating analyst expectations. The stock is currently trading at $2.17, up 3.33% in the most recent session, but remains well below its 52-week high of $3.82, suggesting investors remain cautious about the company’s high leverage and broader market conditions affecting the hospitality sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.