Kraft Heinz confirms plans to split into two public companies by second half 2026

Introduction & Market Context

Bright Horizons Family Solutions Inc (NYSE:BFAM), a leading provider of early education, childcare, and workplace solutions, delivered solid results in Q4 2024, capping off a year of consistent growth. The company’s investor presentation highlights its resilient business model built on employer partnerships, diversified service offerings, and global presence.

The company operates in a large addressable market with favorable demographic trends, including 46% of households having both parents working and 60% of families seeking center-based childcare. With 1,019 centers globally and serving over 1,450 clients, Bright Horizons has established itself as a market leader in employer-sponsored childcare and complementary services.

Executive Summary

Bright Horizons reported Q4 2024 revenue of $674 million, representing 10% year-over-year growth. Adjusted EBITDA reached $111 million, up 12% from Q4 2023, with margins improving to 16.4%. The company’s adjusted EPS grew 18% to $0.98.

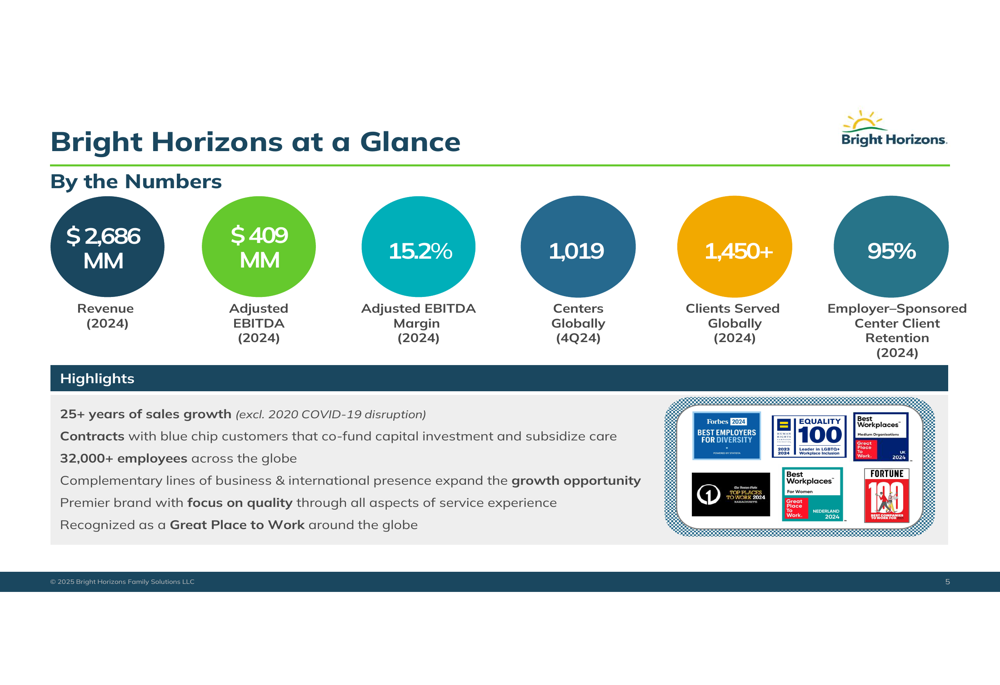

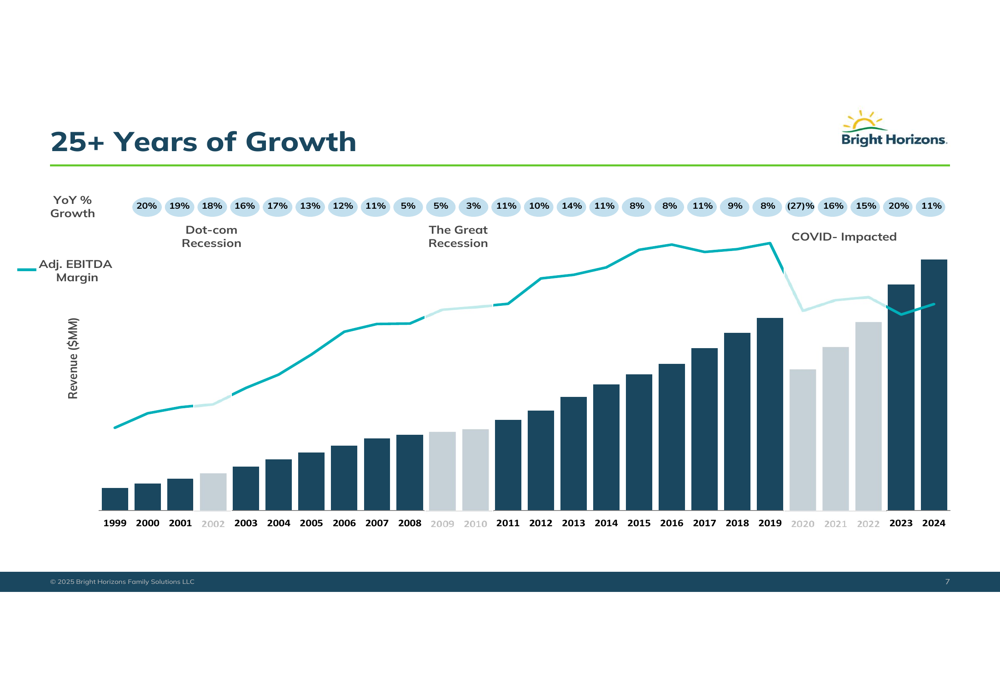

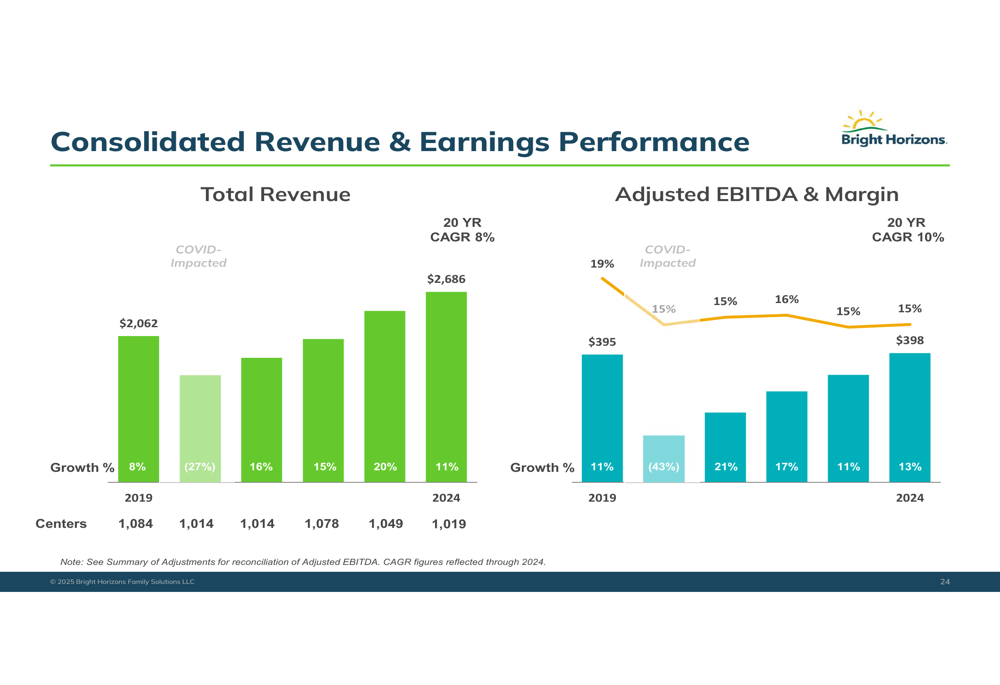

For the full year 2024, Bright Horizons generated $2.686 billion in revenue with an adjusted EBITDA of $409 million, representing a 15.2% margin. The company has demonstrated remarkable consistency with 25+ years of sales growth (excluding 2020 due to COVID-19).

As shown in the following key metrics overview, Bright Horizons maintains high client retention rates and a strong reputation in the industry:

Business Model & Competitive Advantages

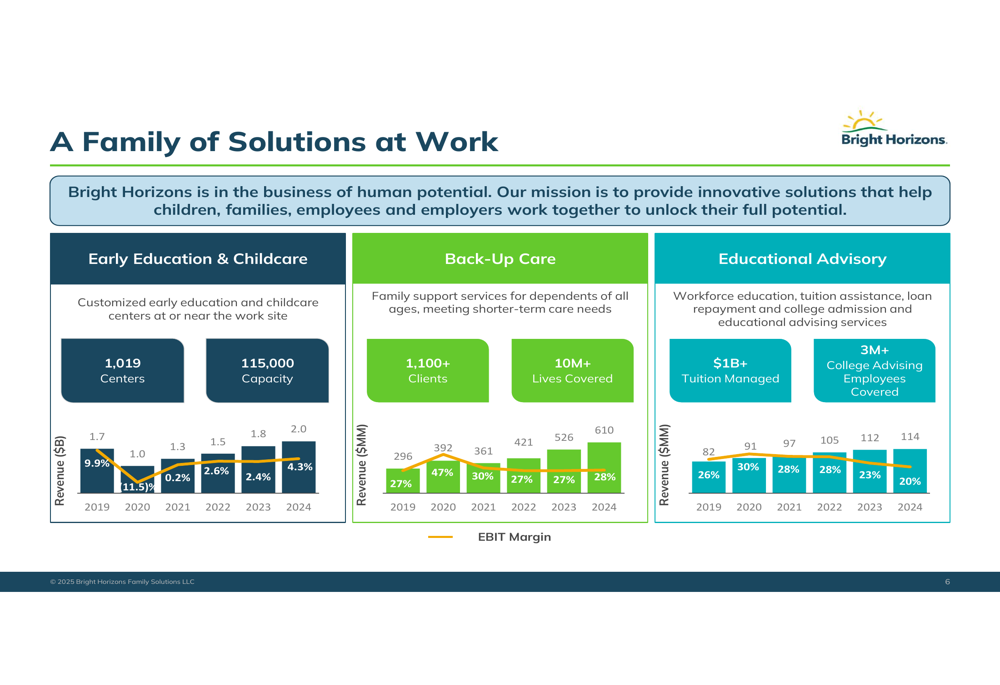

Bright Horizons operates through three main business segments: Early Education & Childcare, Back-Up Care, and Educational Advisory. Each segment serves different needs across various life and career stages, creating multiple revenue streams and cross-selling opportunities.

The company’s presentation illustrates how these segments have performed historically:

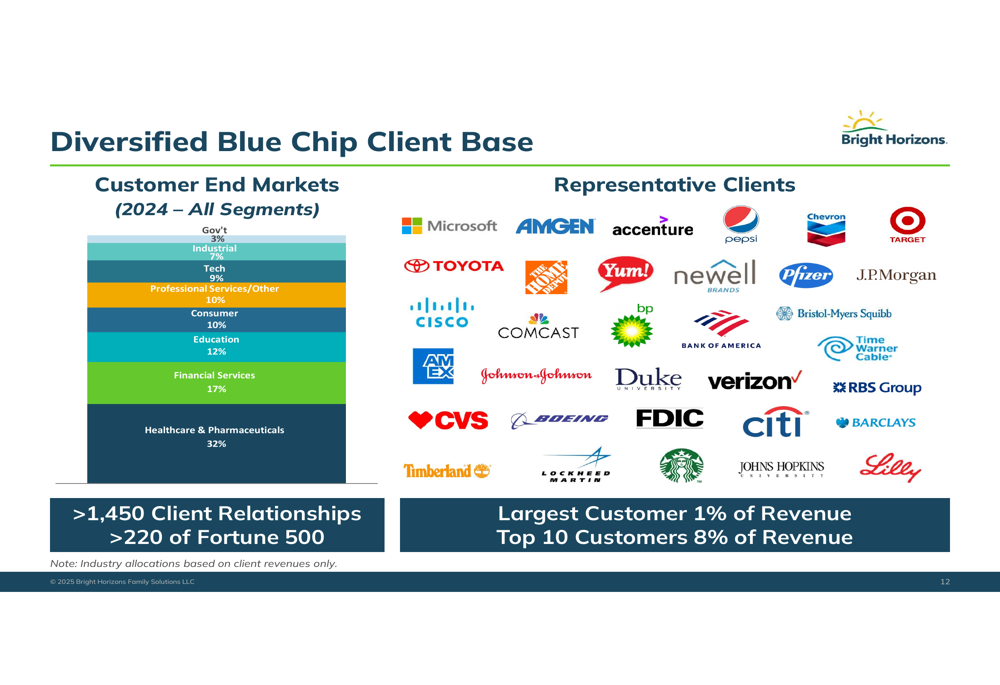

A key strength of Bright Horizons is its diversified blue-chip client base across multiple industries. Healthcare & Pharmaceuticals represent the largest sector at 32% of revenue, followed by Financial Services (17%) and Education (12%). Importantly, no single customer accounts for more than 1% of revenue, and the top 10 customers collectively represent just 8% of total revenue.

The following chart demonstrates this diversification across industries and showcases some of the company’s prestigious clients:

Bright Horizons’ competitive advantages include its employer-centric model with 95% renewal rates, capital-light structure with client-funded investments, and diversification across customers, offerings, and geographies. The company’s mission-critical services provide employers with tangible ROI through improved employee retention, recruitment, and productivity.

Quarterly Performance Highlights

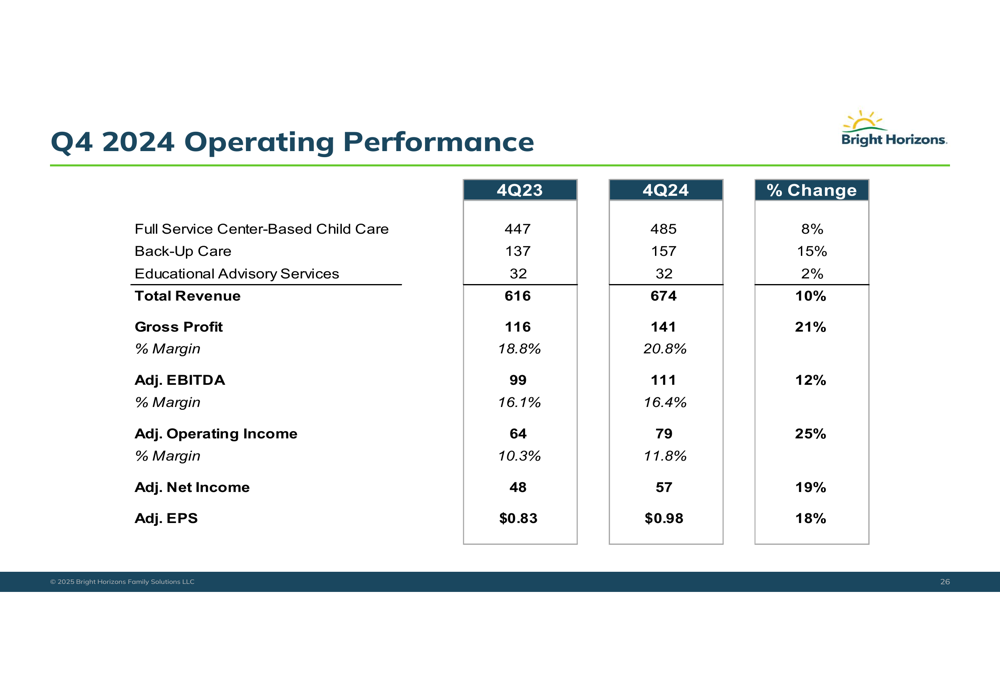

Q4 2024 results showed strong performance across all business segments. Full Service Center-Based Child Care revenue grew 8% year-over-year, while Back-Up Care revenue increased by 15%. Educational Advisory Services revenue grew 2% compared to Q4 2023.

The company’s gross profit margin improved significantly from 18.8% in Q4 2023 to 20.8% in Q4 2024, demonstrating improved operational efficiency. Adjusted operating income increased 25% year-over-year to $79 million.

The following table provides a detailed breakdown of Q4 2024 performance metrics:

This strong quarterly performance aligns with the company’s continued momentum into 2025. According to the recent earnings report, Bright Horizons exceeded expectations in Q1 2025 with revenue of $666 million (7% YoY growth) and adjusted EPS of $0.77 (51% YoY growth), leading to a modest stock price increase of 0.38% in aftermarket trading.

Financial Analysis

Bright Horizons has demonstrated impressive long-term financial performance with a 20-year CAGR of 8% for revenue and 10% for adjusted EBITDA. The company successfully navigated the COVID-19 disruption and has returned to growth.

The following chart illustrates this long-term growth trajectory:

The Back-Up Care segment has been particularly strong, growing from $296 million in 2019 to $610 million in 2024, representing a 16% CAGR. This segment maintains healthy EBIT margins of 28% in 2024, consistent with its historical performance.

The company’s consolidated revenue and earnings performance shows the resilience of its business model:

Growth Strategy

Bright Horizons has identified multiple growth channels to sustain its expansion. These include developing new client relationships, cross-selling additional services to existing clients, entering new communities and markets, and strategic acquisitions.

The company has a proven track record in acquisitions, averaging 30 centers acquired annually over the last 15 years. These acquisitions have expanded both the company’s geographic footprint and service offerings.

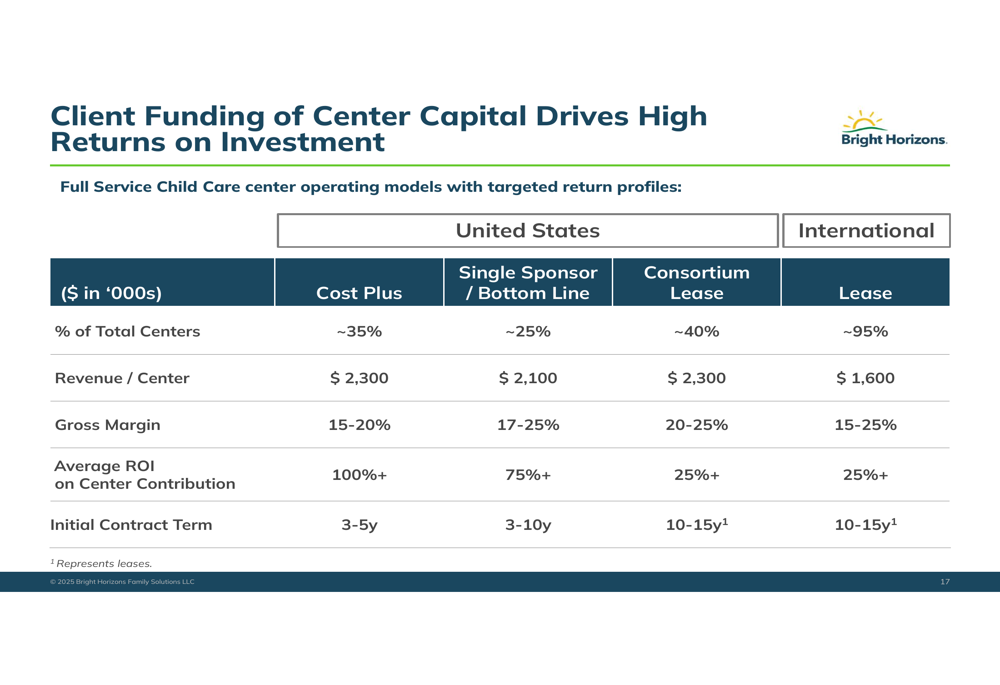

Bright Horizons operates with diverse business models that provide flexibility and different financial returns. The following slide details the various operating models and their financial characteristics:

Looking ahead, Bright Horizons expects steady-state long-term revenue growth of 8-10%, driven by new centers (1-2%), tuition increases (3-4%), enrollment growth (1-3%), Back-Up and Educational Advisory services (1-2%), and acquisitions (1-2%), offset by center closings (-1-2%).

Forward-Looking Statements

Based on its Q1 2025 performance, Bright Horizons has raised its revenue growth guidance to 6.5%-8.5% for the year while maintaining its adjusted EPS guidance of $3.95-$4.15. The company expects Q2 2025 revenue to be between $720 million and $730 million.

The company plans to continue its balanced approach to center openings and closings, with approximately 25 new centers and 25 closures expected in 2025, leading to a neutral net change. This strategic portfolio management helps maintain quality and profitability across locations.

Bright Horizons faces some challenges, including macroeconomic uncertainties affecting enrollment rates, potential slower decision-making processes for new enrollments, and navigating labor market fluctuations. However, the company’s diversified model and high client retention rates position it well to manage these challenges.

Conclusion

Bright Horizons’ Q4 2024 investor presentation showcases a company with a resilient business model, strong client relationships, and consistent financial performance. The diversification across business segments, client industries, and geographies provides stability and multiple growth avenues.

The company’s 25+ year track record of growth, excluding the COVID-19 disruption in 2020, demonstrates its ability to navigate various economic cycles. With a high client retention rate of 95% and a blue-chip customer base, Bright Horizons is well-positioned to continue its growth trajectory.

Recent Q1 2025 results confirm this positive momentum, with the company exceeding analyst expectations and raising its revenue growth guidance for the year. As Bright Horizons continues to expand its service offerings and global footprint, it remains a leader in the employer-sponsored childcare and workplace solutions market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.