Joby Aviation closes $591 million stock offering with full underwriter option

BrightView Holdings , Inc. (NYSE:BV), the leading commercial landscaping services company in the United States, presented its second quarter fiscal year 2025 results on May 8, 2025, highlighting record EBITDA performance and raising its full-year guidance despite modest revenue challenges.

Executive Summary

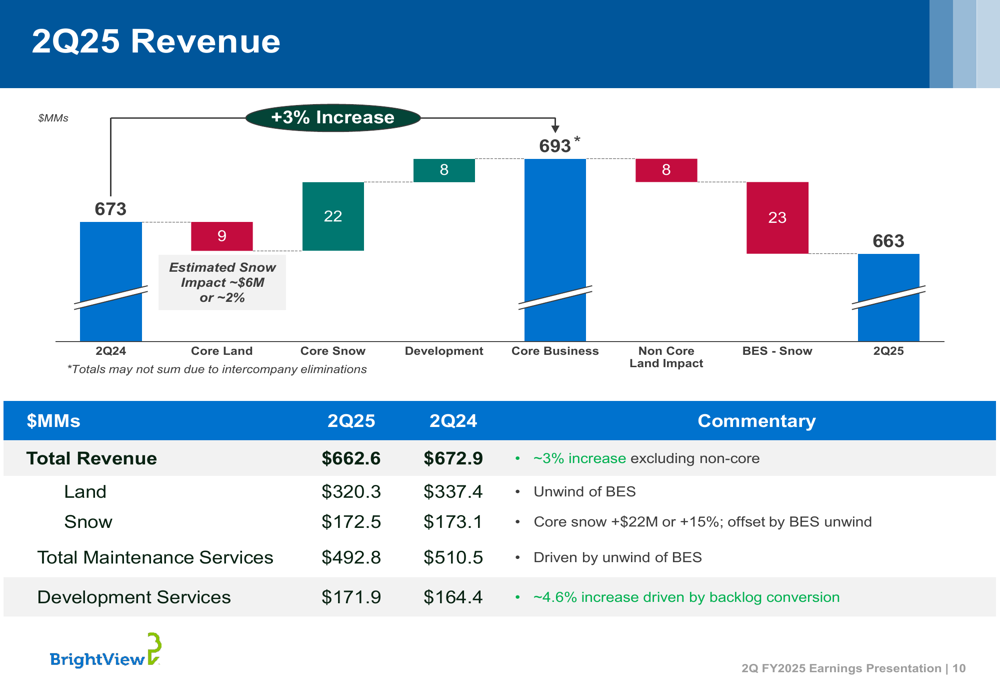

BrightView reported second-quarter revenue of $662.6 million, representing a 1.5% decrease from $672.9 million in the same period last year. However, the company achieved significant profitability improvements with Adjusted EBITDA reaching $73.5 million, a 13% increase year-over-year, and margin expansion of 150 basis points.

President and CEO Dale Asplund emphasized the company’s resilient business model and progress on strategic initiatives: "Our One BrightView transformation is progressing well, positioning us to drive profitable growth regardless of end-market conditions."

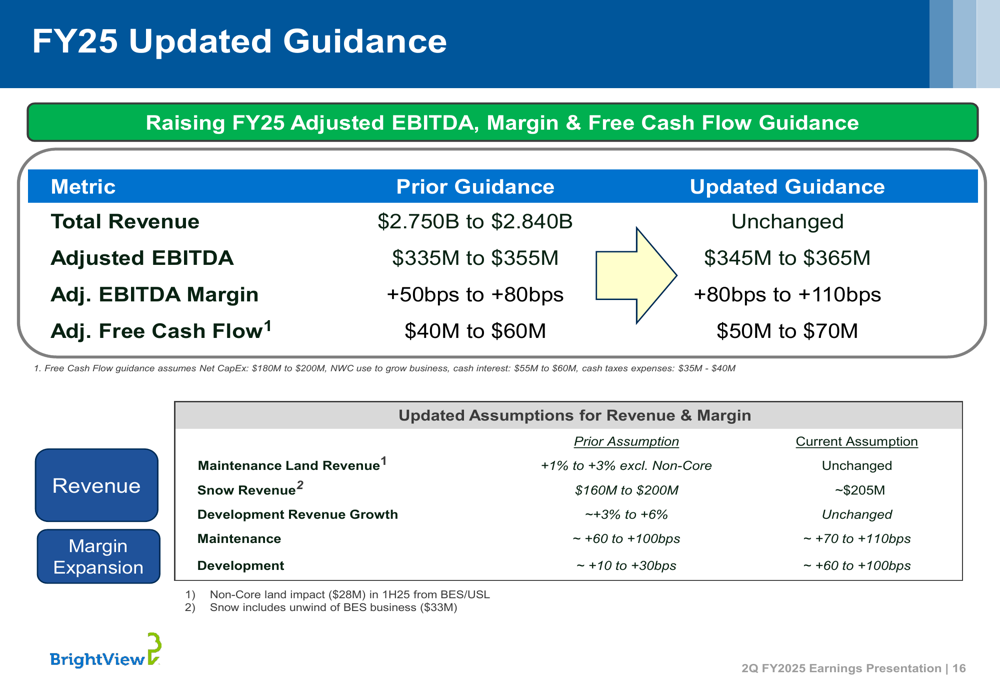

The company raised its full-year 2025 guidance for Adjusted EBITDA, margin, and free cash flow, reflecting confidence in its operational improvements and strategic direction.

Quarterly Performance Highlights

BrightView’s Q2 revenue performance showed mixed results across segments. While core snow services revenue increased by $22 million or 15% and development services grew by 4.6%, these gains were offset by the unwinding of BrightView Enterprise Services (BES).

As shown in the following revenue breakdown:

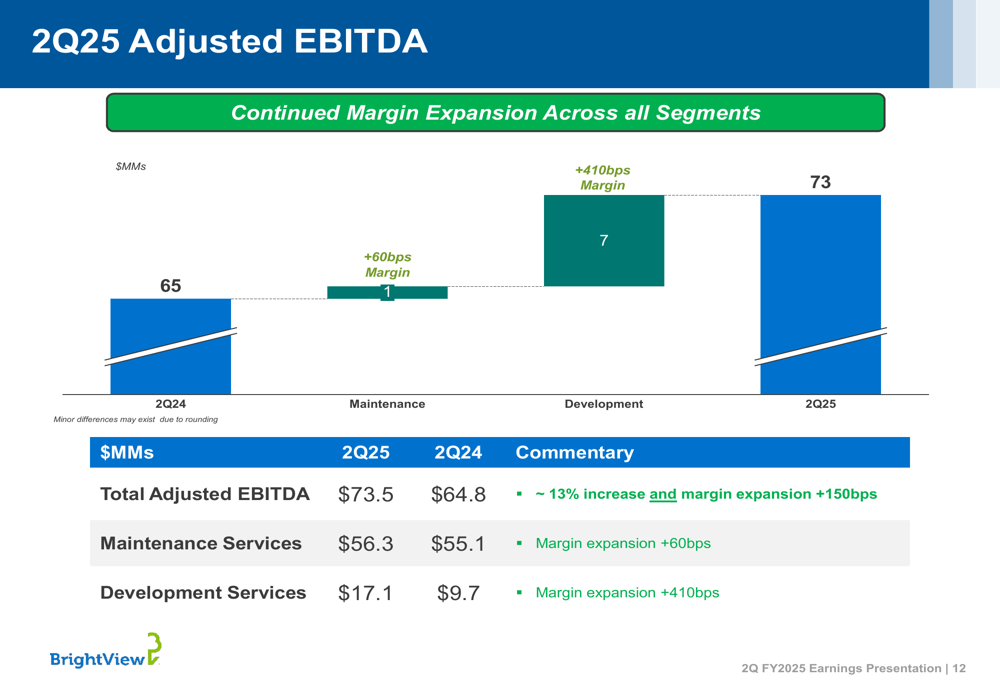

Adjusted EBITDA performance was particularly strong, with the company achieving a 13% increase to $73.5 million compared to $64.8 million in Q2 FY2024. This improvement was driven by margin expansion across both maintenance and development segments, with maintenance services margins improving by 60 basis points and development services margins expanding by an impressive 410 basis points.

The following chart illustrates the EBITDA performance:

CFO Brett Urban highlighted that the first half of fiscal 2025 delivered record EBITDA and margin performance: "We achieved a 13% increase in EBITDA to $126 million in the first half, with 140 basis points of margin improvement, while continuing to make strategic investments in our people and customers."

Strategic Initiatives

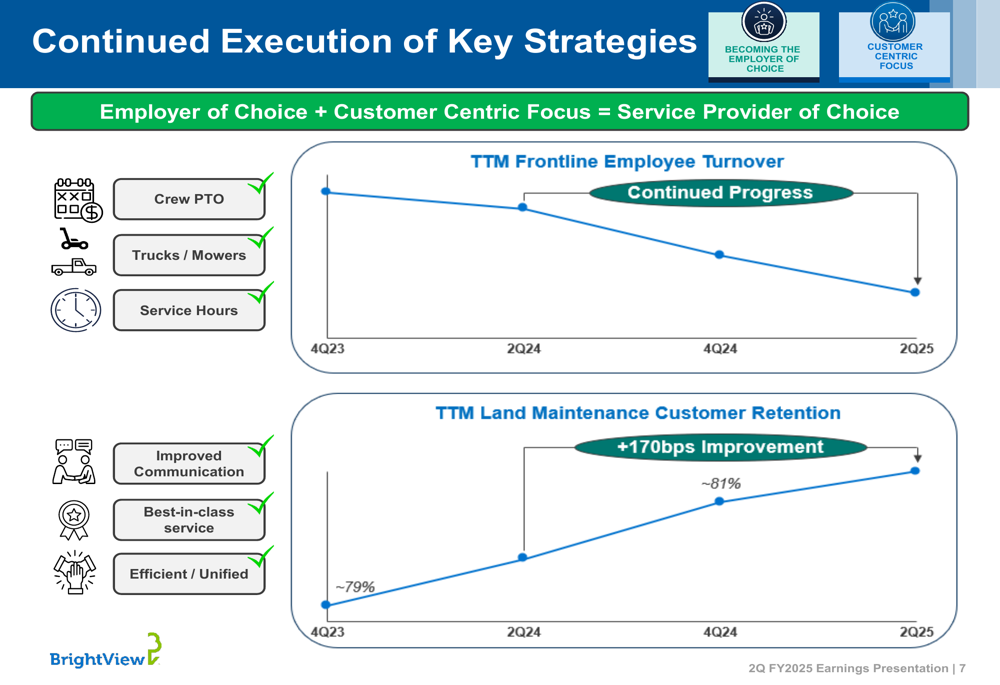

BrightView continues to execute on key strategic priorities centered around becoming the employer of choice, maintaining customer-centric focus, unlocking scale advantages, and strategic capital allocation.

The company has made notable progress in reducing employee turnover and improving customer retention, as illustrated in the following chart:

This improvement in employee retention and customer satisfaction is creating a virtuous cycle that management refers to as their "winning formula," where lower employee turnover leads to better customer retention, which in turn supports growing and more profitable branches.

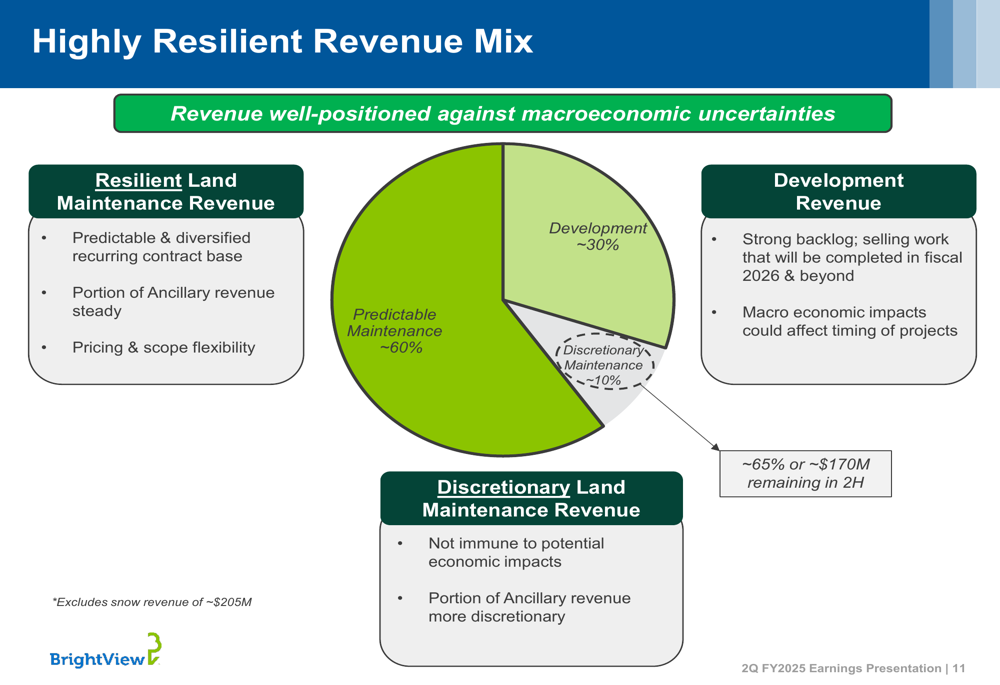

BrightView’s revenue mix demonstrates the resilience of its business model, with approximately 60% coming from predictable maintenance contracts, 30% from development services with strong backlog, and only 10% from more discretionary maintenance services.

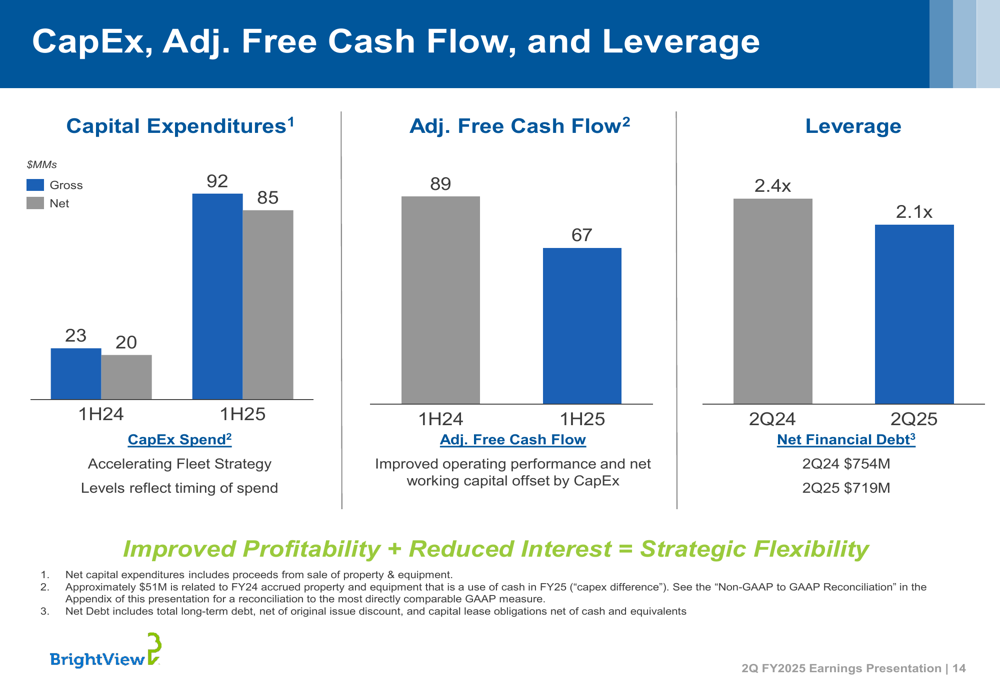

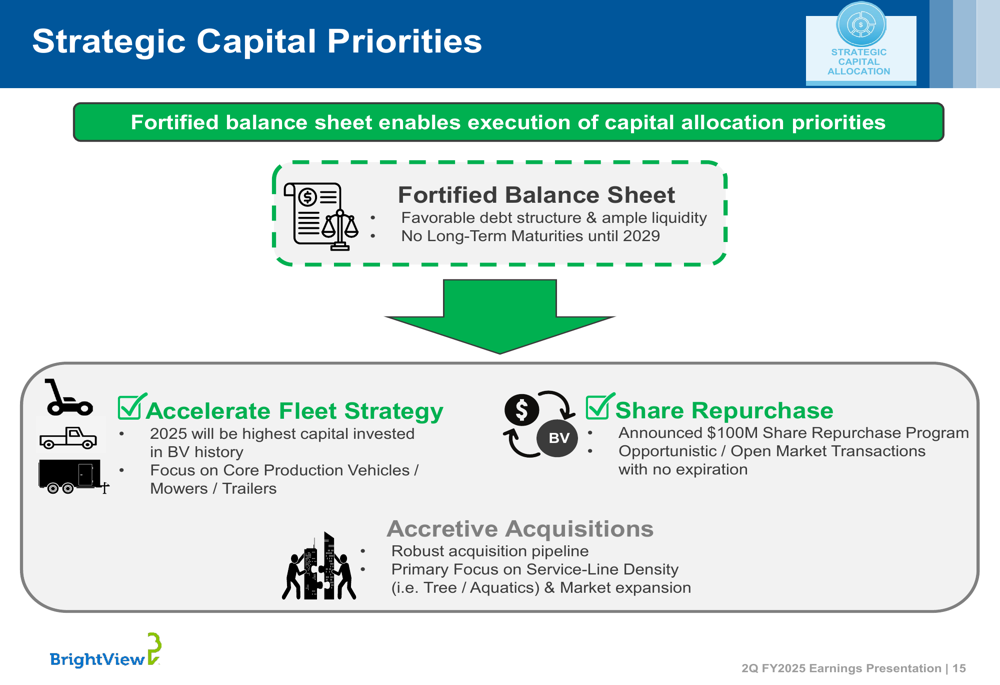

Financial Position and Capital Allocation

BrightView has strengthened its balance sheet, reducing its leverage ratio from 2.4x in Q2 FY2024 to 2.1x in Q2 FY2025. Net financial debt decreased from $754 million to $719 million during the same period.

The company’s improved financial position is illustrated in the following chart:

With this fortified balance sheet, BrightView announced a $100 million share repurchase program with no expiration date. During Q2, the company repurchased 136,352 shares at an average price of $13.11 per share.

The company outlined its strategic capital priorities, which include accelerating its fleet strategy, executing the share repurchase program, and pursuing accretive acquisitions focused on service-line density and market expansion.

Updated Guidance

Based on strong first-half performance, BrightView raised its fiscal year 2025 guidance:

Key updates to the guidance include:

- Adjusted EBITDA increased from a range of $335-$355 million to $345-$365 million

- Adjusted EBITDA margin improvement increased from 50-80 basis points to 80-110 basis points

- Adjusted free cash flow guidance raised from $40-$60 million to $50-$70 million

The company maintained its total revenue guidance, reflecting continued caution about macroeconomic conditions while expressing confidence in its ability to drive profitability improvements.

Long-Term Strategy

BrightView’s management emphasized that its "One BrightView" approach is driving long-term profitable growth by leveraging the company’s position as a market leader with scale advantages.

"We’re positioned to drive sustainable profitable growth and deliver meaningful shareholder value," said Asplund. "By focusing on our employees, customers, and operational efficiency, we’re building a stronger foundation for future growth."

The company’s stock closed at $14.36 on May 7, 2025, up 1.25% for the day, and has shown resilience in a challenging macroeconomic environment. In extended trading following the presentation, BrightView shares edged up slightly by 0.14% to $14.54.

As BrightView continues its transformation journey, investors will be watching closely to see if the company can maintain its margin expansion momentum while returning to revenue growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.