Street Calls of the Week

Introduction & Market Context

Brink’s Company (NYSE:BCO) released its second quarter 2025 investor presentation on August 6, highlighting the company’s strategic transformation and financial outlook. The presentation comes as Brink’s stock jumped 5.41% in premarket trading to $93.46, building on yesterday’s 1.33% gain during regular trading hours.

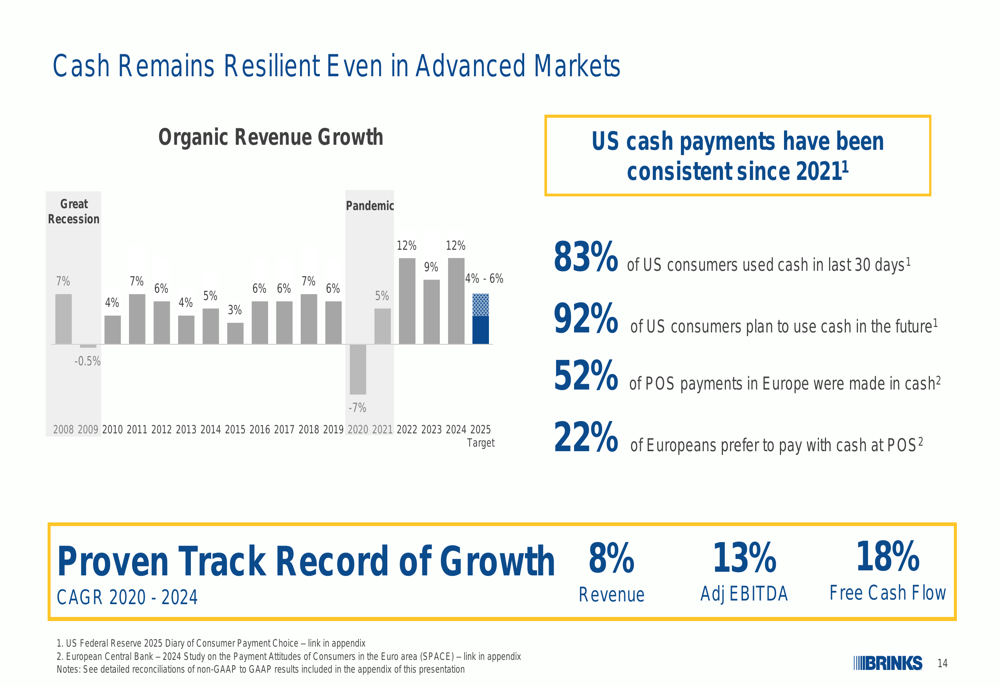

The cash management and secure logistics provider is emphasizing its evolution beyond traditional services, positioning itself as a partner in securing commerce across both physical and digital channels. This strategic shift comes amid persistent cash usage globally, with the company citing data showing 83% of U.S. consumers used cash in the last 30 days and 92% plan to continue using cash in the future.

Strategic Initiatives

Brink’s is aggressively expanding its ATM Managed Services ( AMS (VIE:AMS2)) and Digital Retail Solutions (DRS) businesses, which offer higher margins and stronger growth potential than traditional cash management services. These initiatives represent a significant strategic pivot for the 166-year-old company.

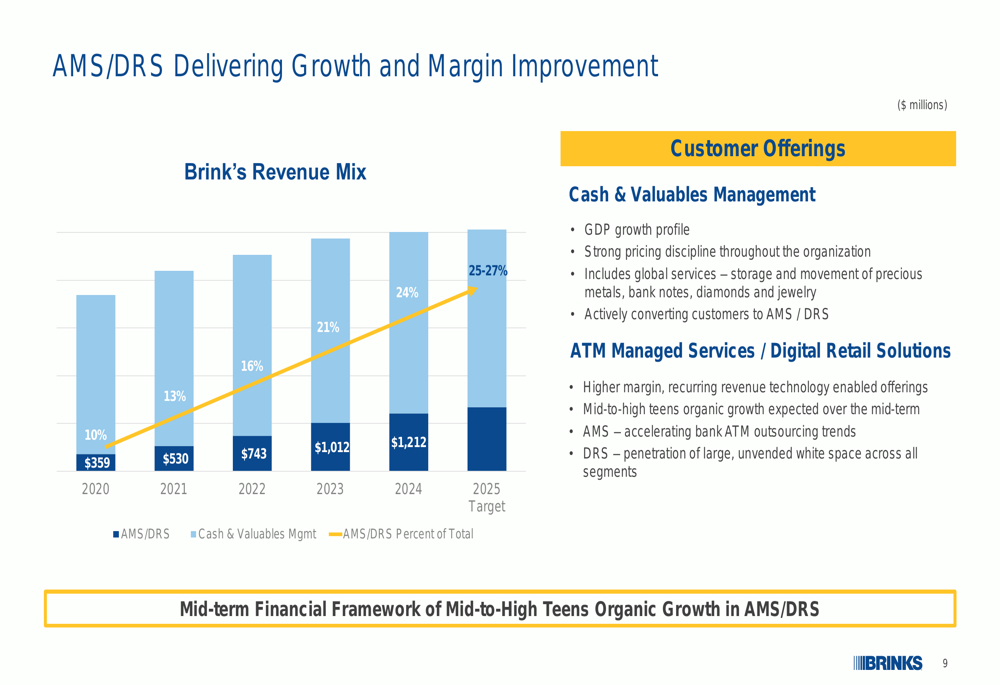

As shown in the following chart of Brink’s revenue mix evolution:

The company has already increased AMS/DRS from 10% of total revenue in 2020 to 24% in 2024, with a target to reach 25-27% by the end of 2025. This aligns with the company’s Q1 2025 earnings report, which noted these services now account for 25% of total business.

According to the presentation, this strategic shift substantially expands Brink’s addressable market:

The company estimates its addressable market has grown by 2-3 times through these new service offerings, targeting both financial institutions looking to outsource ATM management and retailers seeking integrated cash handling solutions.

Brink’s value creation strategy is built on four key pillars designed to drive growth and shareholder returns:

Detailed Financial Analysis

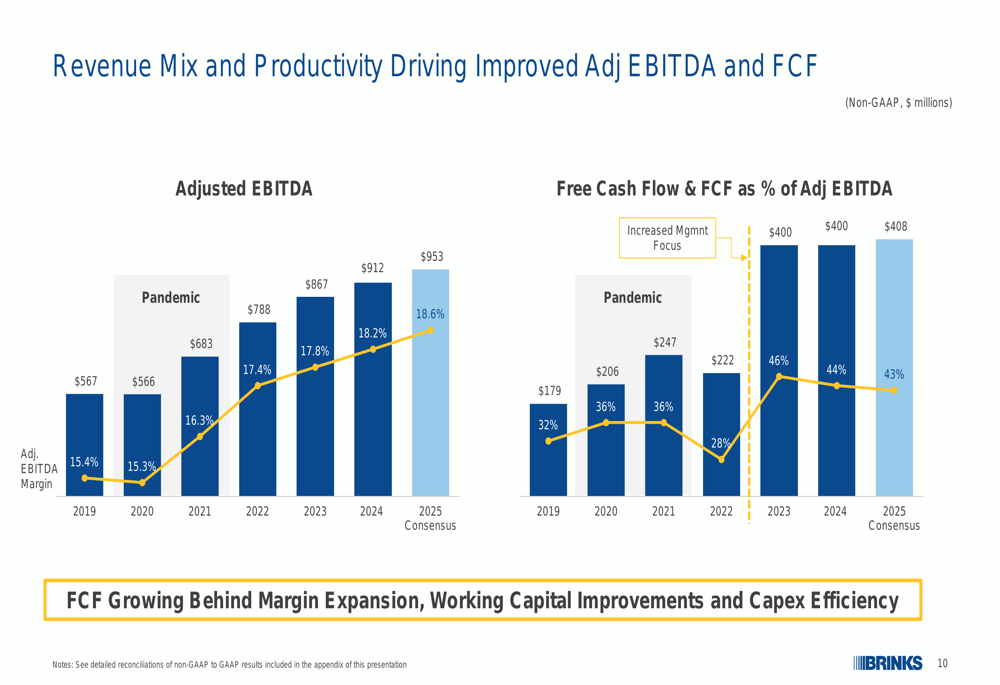

The company’s financial trajectory shows improving profitability and cash flow conversion as the business mix shifts toward higher-margin services. The presentation highlights significant growth in adjusted EBITDA and free cash flow:

Adjusted EBITDA is projected to reach $953 million in 2025 (consensus estimate), up from $567 million in 2019, representing a 68% increase over six years. More impressively, free cash flow is expected to reach $408 million in 2025, a 128% increase from $179 million in 2019.

The free cash flow conversion rate (FCF as a percentage of adjusted EBITDA) is projected to improve from 32% in 2019 to 43% in 2025, reflecting the company’s focus on operational efficiency and working capital management.

This financial improvement aligns with Brink’s Q1 2025 performance, which exceeded analyst expectations with earnings per share of $1.62 versus a forecast of $1.37, and revenue of $1.25 billion compared to an anticipated $1.21 billion.

Capital Allocation Strategy

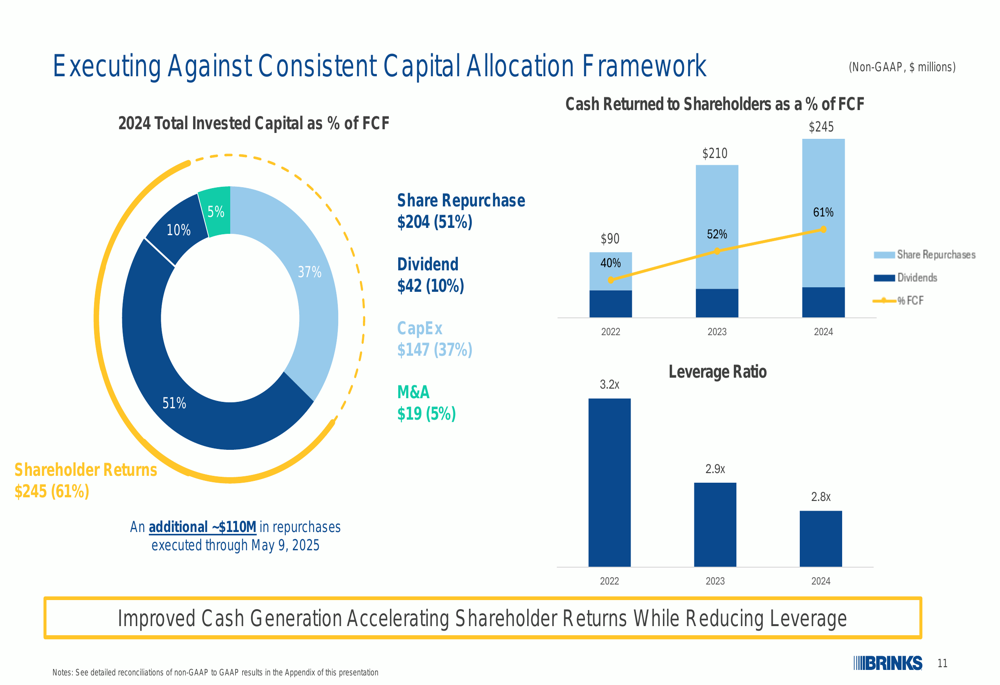

Brink’s is emphasizing shareholder returns through its capital allocation framework:

In 2024, the company allocated 51% of its free cash flow to share repurchases, 10% to dividends, 37% to capital expenditures, and 5% to acquisitions. Share repurchases increased from $210 million in 2022 to $245 million in 2024, demonstrating the company’s commitment to returning capital to shareholders.

This focus on shareholder returns is consistent with the company’s earnings call commentary, where management highlighted its aggressive share buyback program and consistent dividend increases over the past four years. According to the recent earnings report, Brink’s has maintained dividend payments for 37 consecutive years.

Forward-Looking Statements

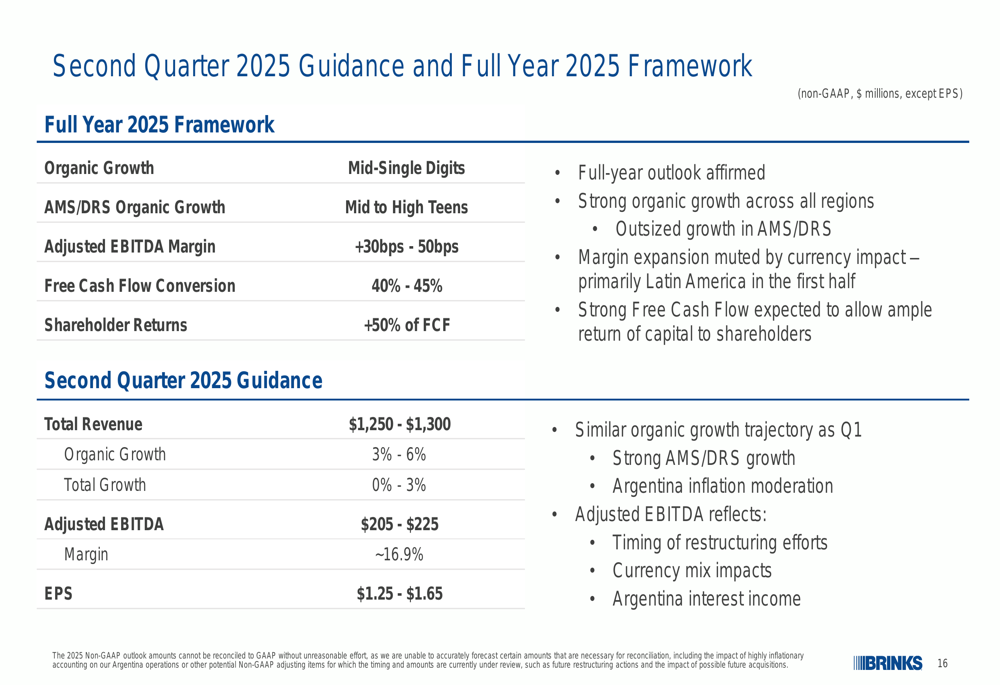

For Q2 2025, Brink’s has provided the following guidance:

The company expects Q2 2025 revenue between $1.25 billion and $1.30 billion, consistent with its Q1 2025 performance of $1.25 billion. For the full year 2025, Brink’s is targeting mid-single-digit organic growth overall, with mid-to-high teens growth in the AMS/DRS segment.

The company’s mid-term financial framework emphasizes:

- Mid-single-digit total organic growth driven by mid-to-high teens AMS/DRS growth

- 30-50 basis points of annual margin expansion

- 40-45% free cash flow conversion

- At least 50% of free cash flow allocated to shareholder returns

Competitive Industry Position

Despite the global shift toward digital payments, Brink’s presentation emphasizes the resilience of cash in the global economy:

The company cites independent studies showing that 52% of point-of-sale payments in Europe are still made in cash, and 22% of Europeans prefer to pay with cash. This data supports Brink’s long-term business model while the company simultaneously expands into digital solutions.

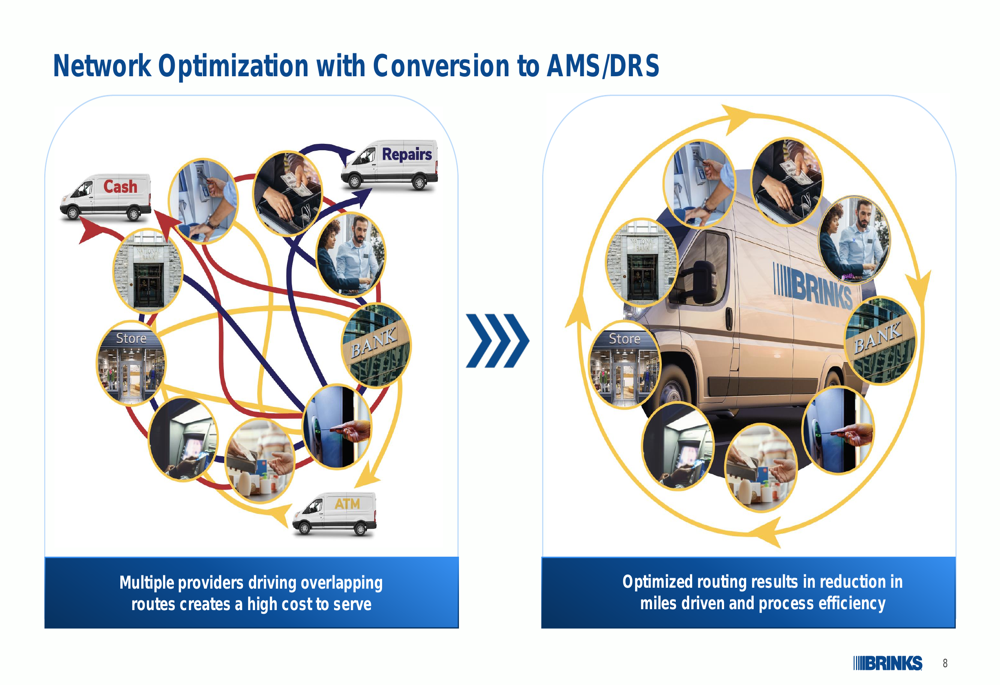

Brink’s describes itself as holding the #1 or #2 market position in most geographies where it operates, with a presence in over 100 countries. The company’s extensive network allows it to optimize routes and reduce costs when converting customers to its AMS/DRS offerings:

This network optimization creates a competitive advantage by reducing miles driven and improving process efficiency, which translates to approximately 10-20% total cost of ownership savings for customers while improving Brink’s own margins.

As cash-intensive businesses continue to seek ways to reduce costs and improve efficiency, Brink’s positioning at the intersection of physical and digital commerce appears well-aligned with market trends, despite ongoing shifts in payment preferences.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.