UBS Points to Two Top European Luxury Stocks Ahead of 2026 Upswing

Introduction & Market Context

Brink's Company (NYSE:BCO) released its third-quarter 2025 earnings presentation on November 5, 2025, highlighting strong performance across key metrics despite an earnings per share miss. The company's stock responded positively, rising 7.67% to close at $105.88, as investors focused on revenue growth, margin expansion, and the company's strategic shift toward higher-margin digital services.

The security and cash management solutions provider reported $1.335 billion in revenue for Q3 2025, representing a 6% year-over-year increase and exceeding analyst expectations of $1.3 billion. While the company's presentation emphasized non-GAAP EPS of $2.08 (a 28% increase), reported GAAP earnings came in at $1.65 per share, missing analyst forecasts of $2.01.

Quarterly Performance Highlights

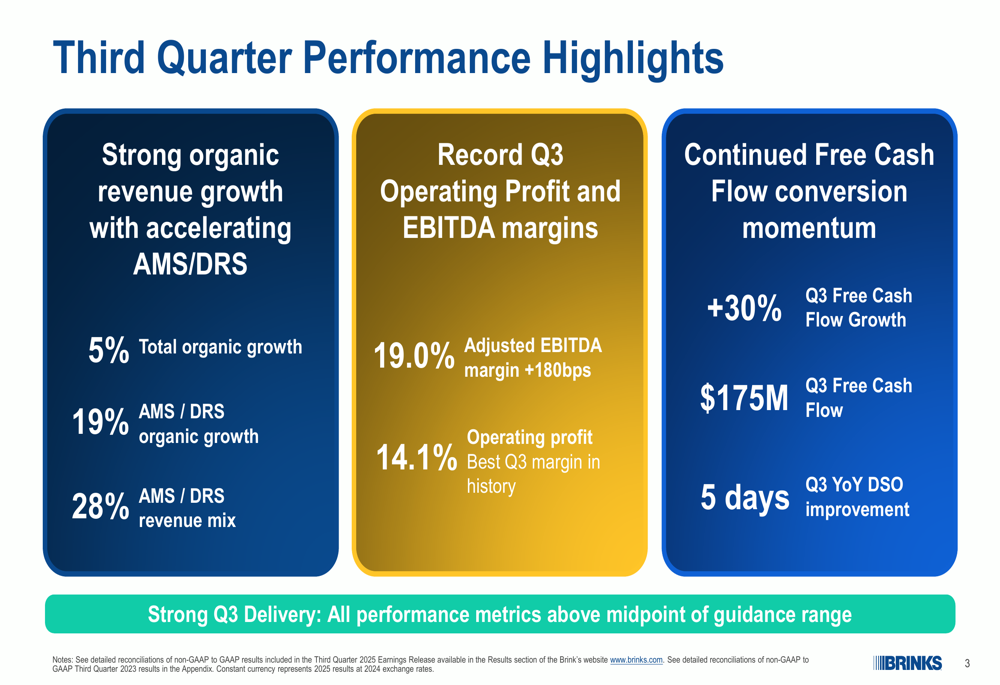

Brink's third quarter was characterized by strong organic growth and record profit margins. The company achieved 5% total organic growth, with its ATM Managed Services and Digital Retail Solutions (AMS/DRS) segment delivering an impressive 19% organic growth rate.

As shown in the following chart detailing Q3 performance highlights, Brink's achieved an adjusted EBITDA margin of 19.0%, representing a 180 basis point increase year-over-year, while operating profit reached 14.1%, which the company described as the best Q3 margin in its history:

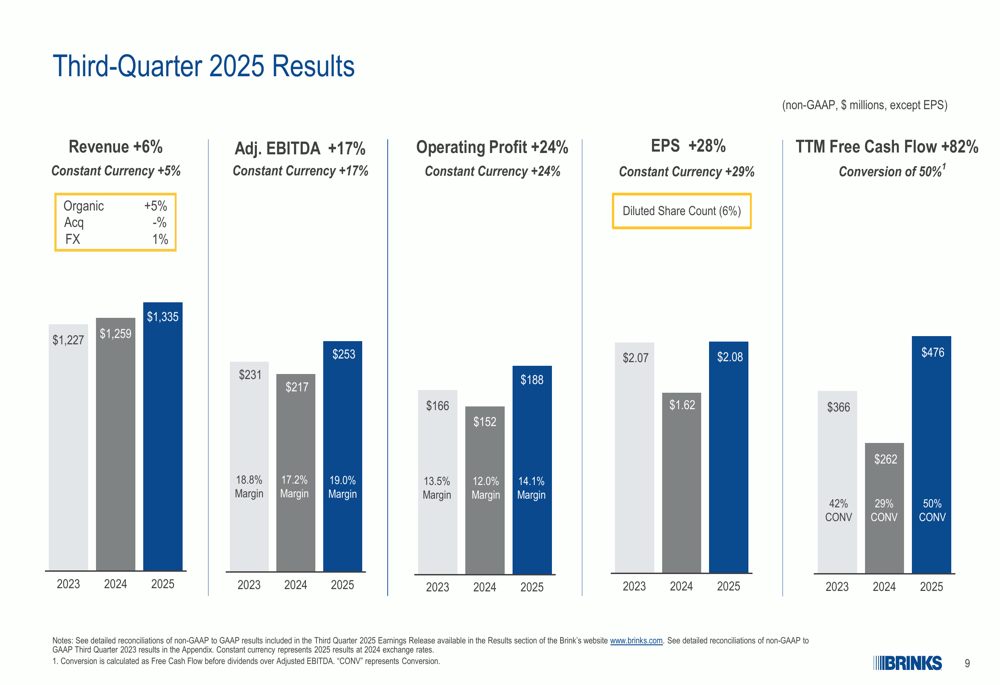

The company's financial results showed significant improvement across all key metrics compared to both 2023 and 2024. Revenue increased to $1,335 million, while adjusted EBITDA grew 17% to $253 million and operating profit jumped 24% to $188 million. Free cash flow also demonstrated strong momentum, growing 30% to $175 million with a 5-day year-over-year improvement in Days Sales Outstanding.

The following chart illustrates Brink's third-quarter 2025 results compared to the previous two years:

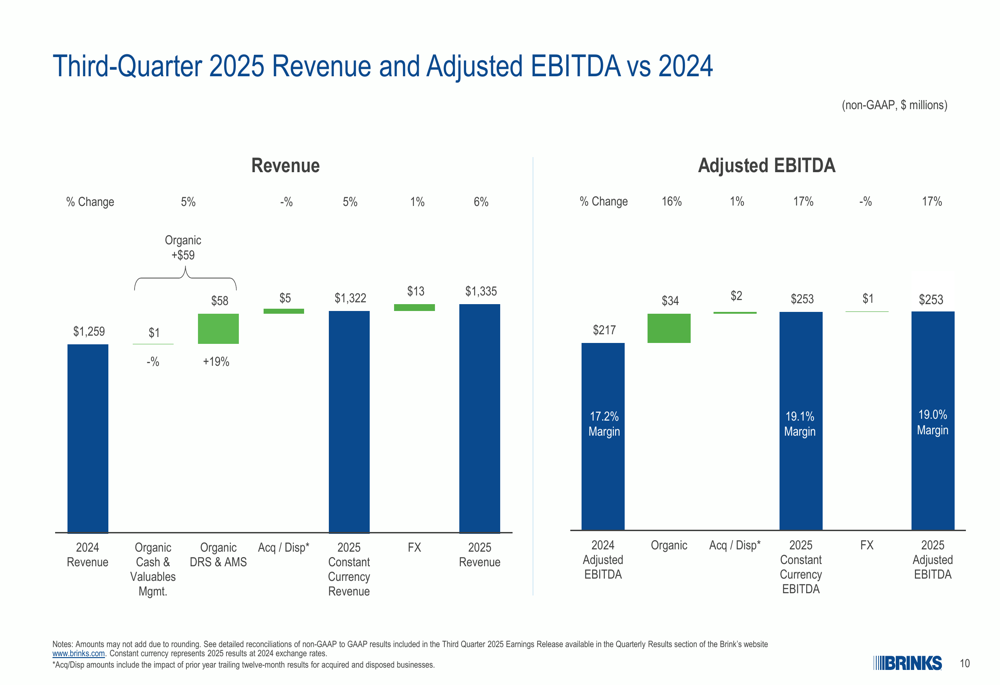

A more detailed breakdown of the revenue and adjusted EBITDA changes between Q3 2024 and Q3 2025 reveals that organic growth contributed $59 million to revenue and $34 million to adjusted EBITDA:

Strategic Initiatives

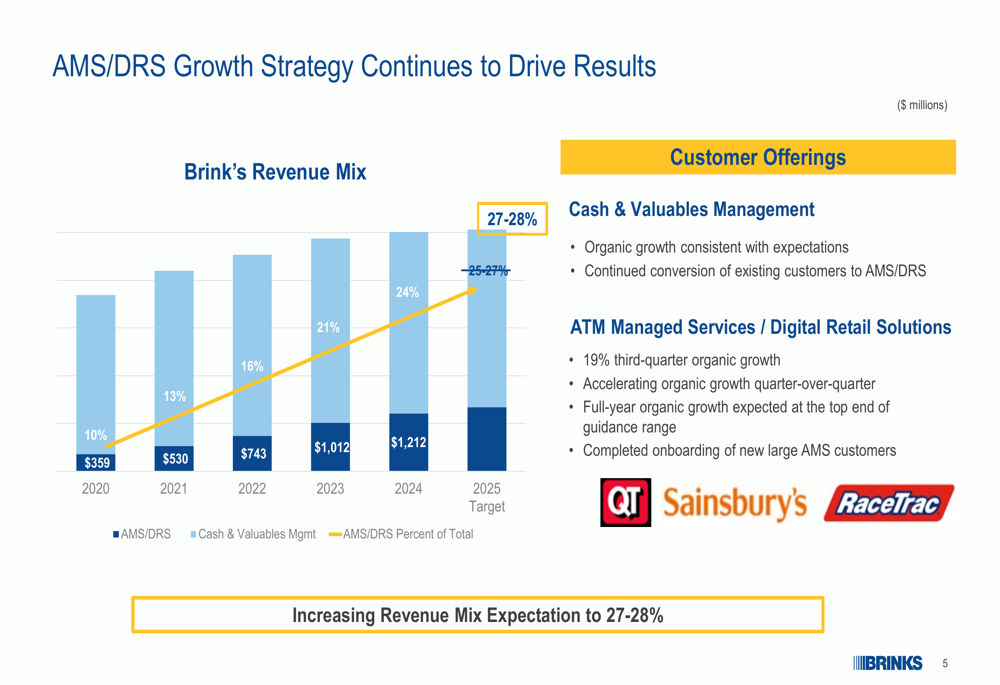

Brink's continues to execute on its strategic shift toward higher-margin ATM Managed Services and Digital Retail Solutions (AMS/DRS). This segment now represents 28% of the company's revenue mix, up from just 10% in 2020, and is on track to reach the company's 2025 target of 27-28%.

The following chart demonstrates the steady progression of AMS/DRS as a percentage of Brink's total revenue since 2020:

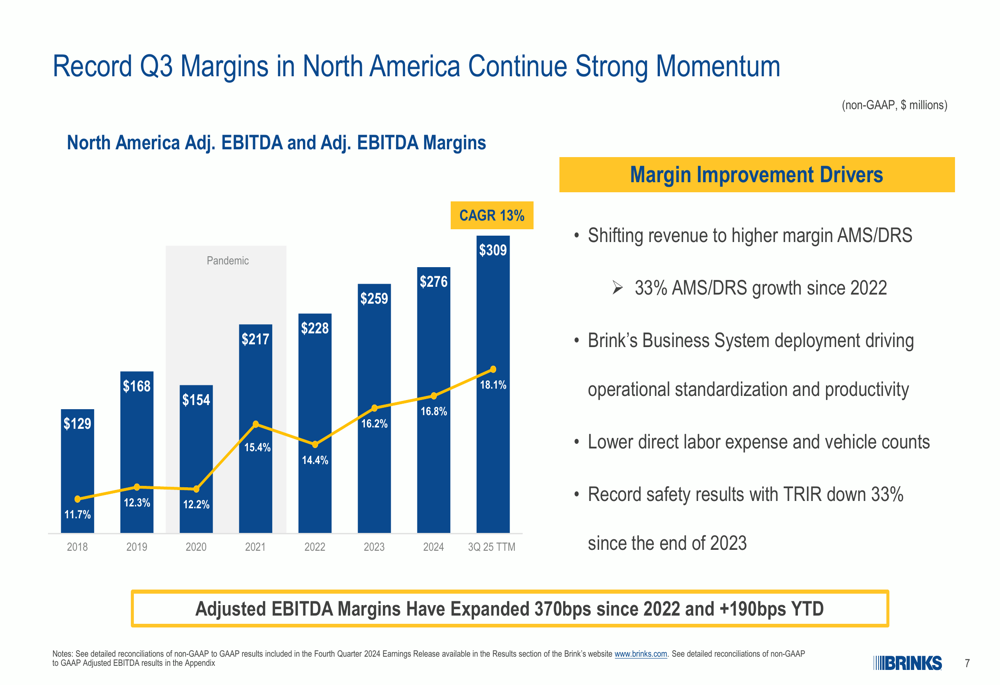

North America has been a particular bright spot for margin expansion, with adjusted EBITDA margins reaching 18.1% in Q3 2025 (trailing twelve months), representing a 370 basis point improvement since 2022. The company attributes this success to shifting revenue to higher-margin AMS/DRS services, operational standardization through the Brink's Business System, lower direct labor expenses, and improved safety results.

As illustrated in the following chart, North America's adjusted EBITDA has grown from $129 million in 2018 to $309 million in Q3 2025 TTM, with margins expanding from 11.7% to 18.1% over the same period:

Detailed Financial Analysis

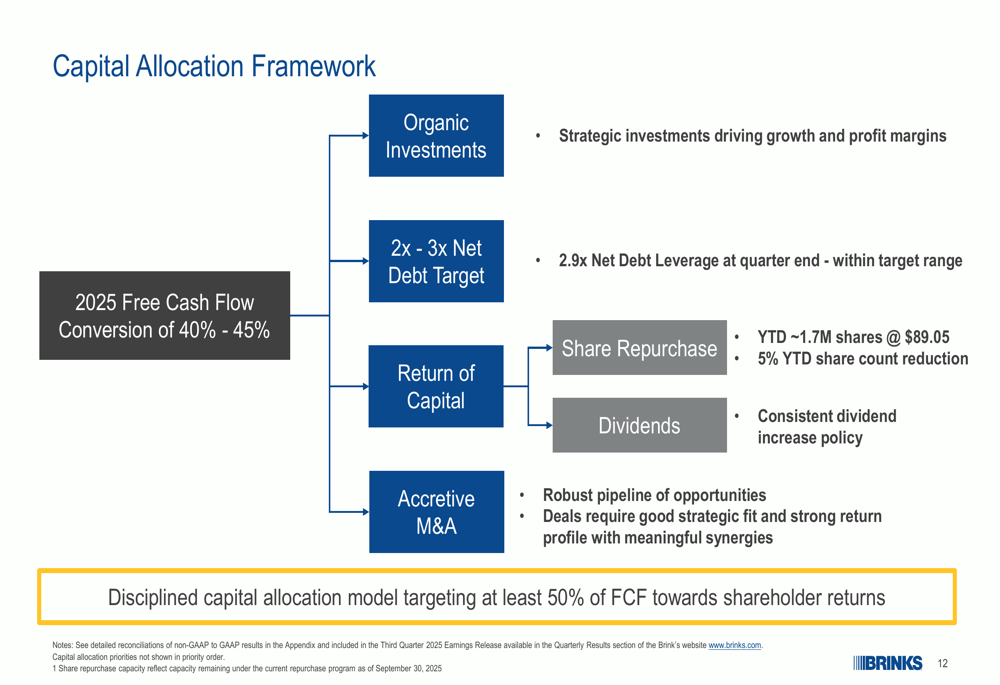

Brink's capital allocation strategy emphasizes a balanced approach between organic investments, maintaining a healthy balance sheet, returning capital to shareholders, and pursuing accretive acquisitions. The company reported a net debt leverage ratio of 2.9x at quarter-end, within its target range of 2-3x.

The company's capital allocation framework prioritizes shareholder returns, with a target of returning at least 50% of free cash flow to shareholders through dividends and share repurchases. Year-to-date, Brink's has repurchased approximately 1.7 million shares at an average price of $89.05, reducing its share count by 5%.

The following chart outlines Brink's capital allocation framework:

Forward-Looking Statements

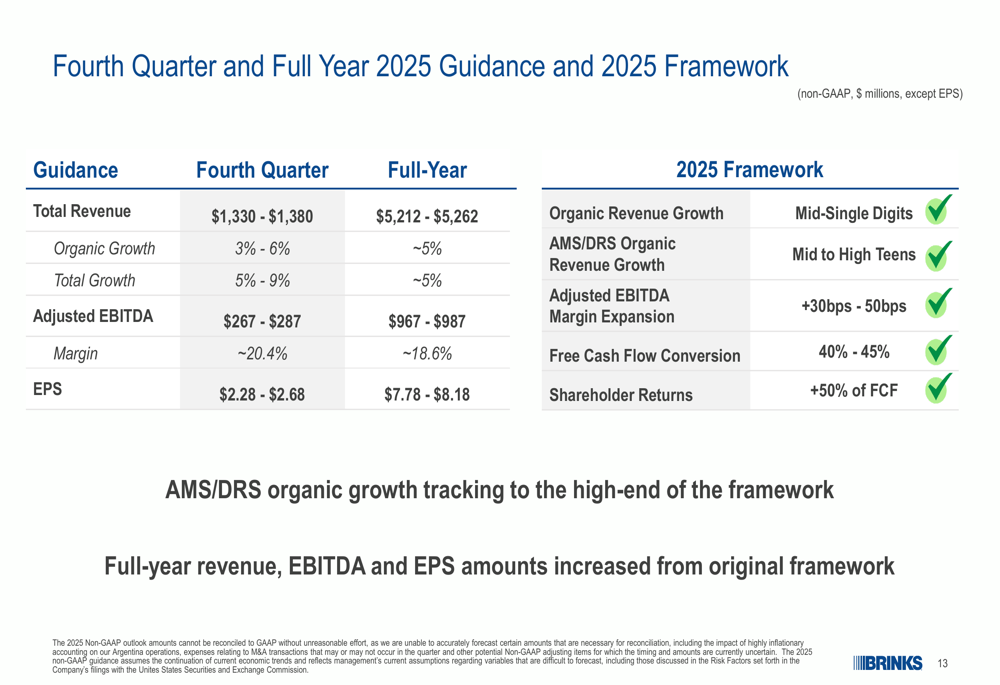

For the fourth quarter of 2025, Brink's provided guidance for total revenue between $1,330 million and $1,380 million, with organic growth of 3-6% and total growth of 5-9%. The company expects adjusted EBITDA between $267 million and $287 million, with a margin of approximately 20.4%, and EPS between $2.28 and $2.68.

For the full year 2025, Brink's anticipates total revenue between $5,212 million and $5,262 million, with organic growth of approximately 5%. The company projects adjusted EBITDA between $967 million and $987 million, with a margin of approximately 18.6%, and EPS between $7.78 and $8.18.

Looking ahead to the remainder of 2025, Brink's provided the following guidance and framework:

CEO Mark Eubanks emphasized the company's market penetration potential during the earnings call, stating, "We are still in the early stages of penetrating this large and growing total addressable market." This sentiment is reflected in the presentation's characterization of ATM outsourcing as being in its early stages with "2-3x addressable market expansion potential."

Despite the EPS miss, Brink's strong performance across other key metrics and clear strategic direction appear to have resonated with investors, as evidenced by the stock's positive movement following the earnings announcement. The company's continued shift toward higher-margin digital services and focus on operational efficiency position it well for sustained growth and profitability in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.