S&P 500 cuts losses as Nvidia climbs ahead of results

Introduction & Market Context

Broadwind Energy Inc. (NASDAQ:BWEN) released its second quarter 2025 financial results on August 12, 2025, showing revenue growth amid profitability pressures. The precision manufacturer, which serves wind energy, power generation, and industrial markets, reported 7.6% year-over-year revenue growth while experiencing margin compression across its business segments.

The company’s stock fell 18.47% in pre-market trading to $2.03, suggesting investors were disappointed with the results despite the revenue growth. This reaction follows a 4.62% gain the previous day, when the stock closed at $2.49.

Broadwind continues to position its domestic manufacturing capabilities as a competitive advantage, particularly as trade tariffs and import restrictions benefit U.S.-based wind tower manufacturers. However, manufacturing inefficiencies and lower capacity utilization in key segments weighed on profitability during the quarter.

Quarterly Performance Highlights

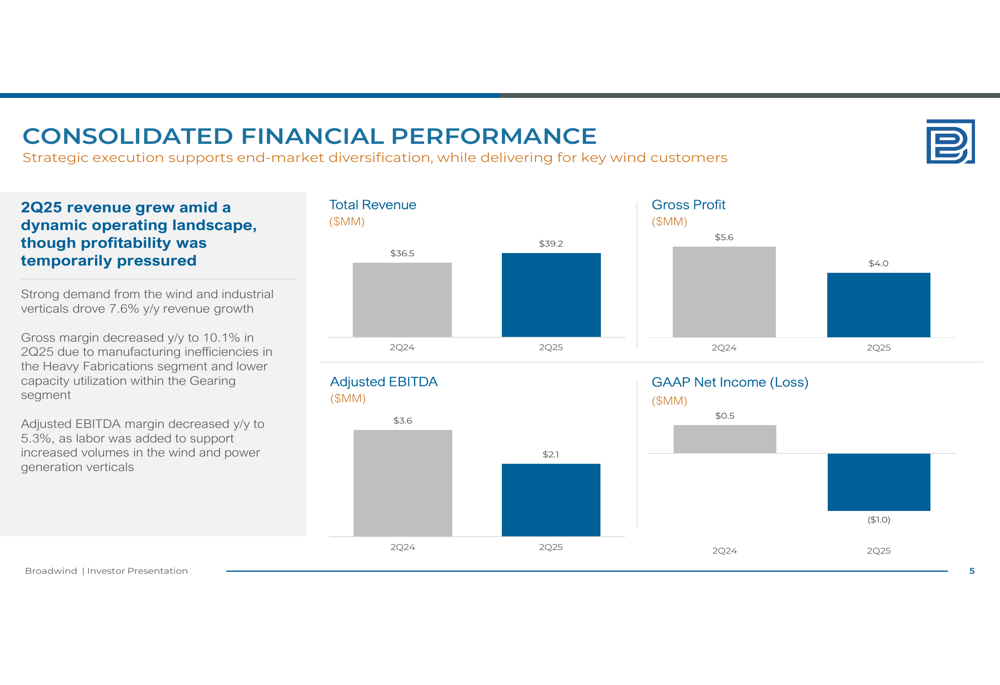

Broadwind reported second quarter 2025 revenue of $39.2 million, up 7.6% from $36.5 million in the same period last year. Despite this growth, the company swung to a net loss of $1.0 million, compared to net income of $0.5 million in Q2 2024. Gross margin decreased to 10.1%, while Adjusted EBITDA margin fell to 5.3%.

As shown in the following chart of quarterly financial performance:

The company attributed the profitability decline to manufacturing inefficiencies in the Heavy Fabrications segment and lower capacity utilization within the Gearing segment. Additionally, Broadwind noted that labor was added to support increased volumes in the wind and power generation verticals, further pressuring margins.

This performance represents a reversal from Q1 2025, when the company reported better-than-expected results with an EPS of -$0.02 that beat forecasts of -$0.04.

Segment-Level Analysis

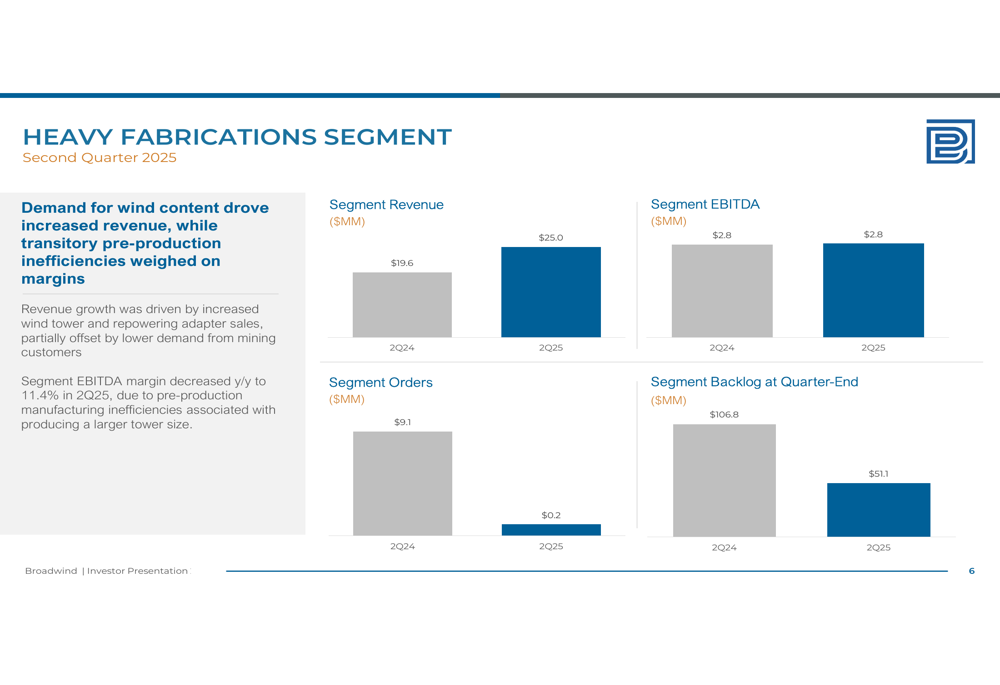

Broadwind’s Heavy Fabrications segment, which includes wind towers and industrial components, saw revenue increase to $25.0 million in Q2 2025, up from $19.6 million in Q2 2024. However, segment EBITDA margin decreased to 11.4% due to pre-production manufacturing inefficiencies associated with producing larger tower sizes. Notably, segment orders fell dramatically to just $0.2 million from $9.1 million a year earlier, while backlog declined to $51.1 million.

The segment’s performance is illustrated in the following chart:

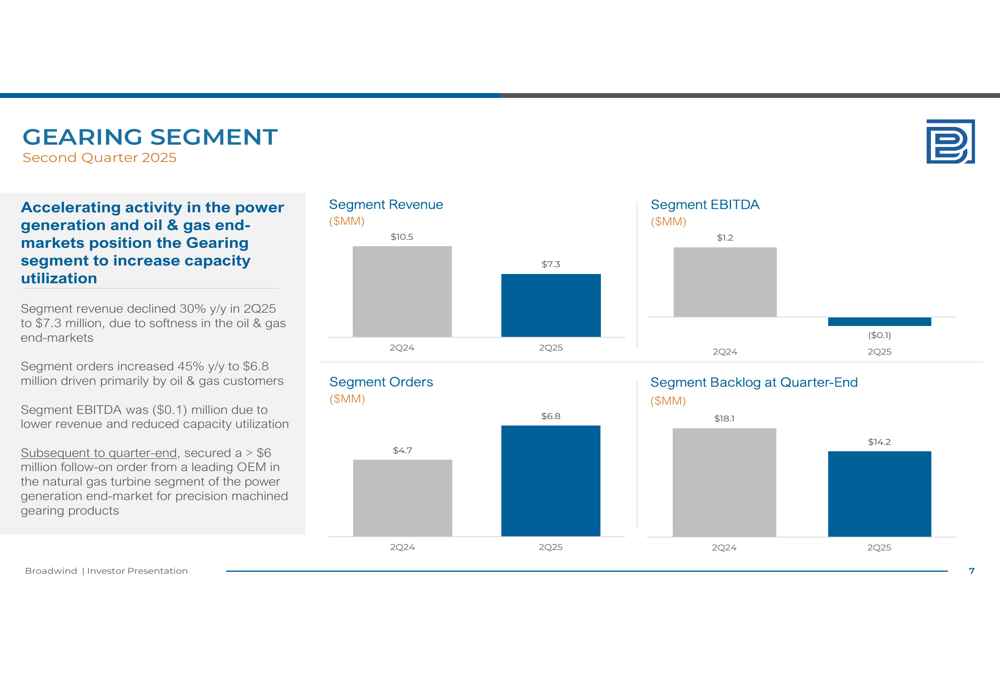

The Gearing segment, which provides custom gearing and gearboxes primarily for oil and gas and mining markets, experienced a 30% year-over-year revenue decline to $7.3 million. This resulted in a segment EBITDA loss of $0.1 million, compared to positive EBITDA of $1.2 million in Q2 2024. However, orders increased 45% year-over-year to $6.8 million, driven primarily by oil and gas customers, potentially signaling a future recovery.

The following chart details the Gearing segment’s performance:

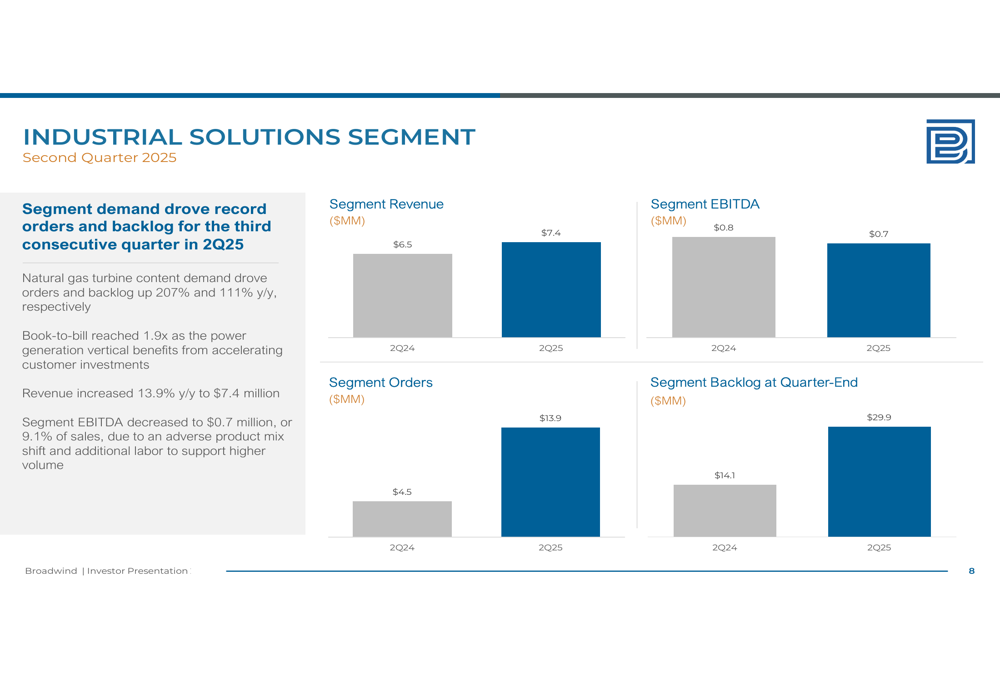

The Industrial Solutions segment was a bright spot, with revenue increasing 13.9% to $7.4 million and record orders for the third consecutive quarter. Orders surged 207% year-over-year to $13.9 million, driven by natural gas turbine content demand, while backlog more than doubled to $29.9 million. The segment’s book-to-bill ratio reached an impressive 1.9x. Despite the strong top-line performance, segment EBITDA decreased slightly to $0.7 million due to an adverse product mix shift and additional labor costs.

The Industrial Solutions segment’s performance is shown below:

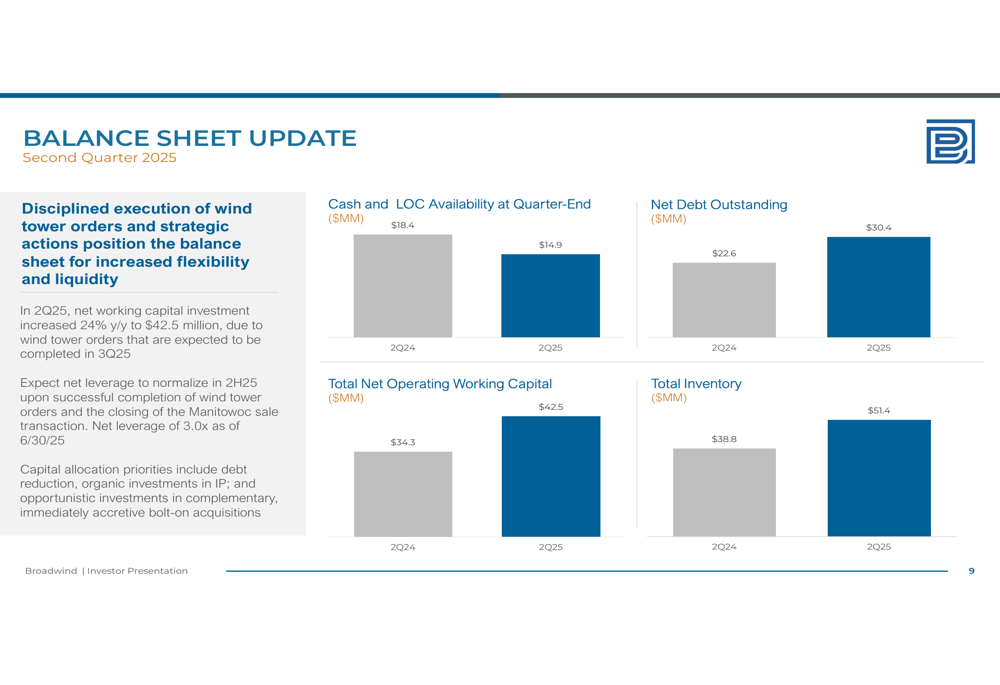

Balance Sheet and Financial Position

Broadwind’s balance sheet showed increased leverage in Q2 2025, with net debt rising to $30.4 million from $22.6 million a year earlier. Net leverage stood at 3.0x as of June 30, 2025. The company’s cash and line of credit availability decreased to $14.9 million from $18.4 million in Q2 2024.

Working capital investment increased 24% year-over-year to $42.5 million, which the company attributed to wind tower orders expected to be completed in Q3 2025. Total (EPA:TTEF) inventory rose to $51.4 million from $38.8 million a year earlier.

The following chart illustrates these balance sheet metrics:

Management expects net leverage to normalize in the second half of 2025 upon successful completion of wind tower orders and the closing of the Manitowoc sale transaction. The company’s capital allocation priorities include debt reduction, organic investments in intellectual property, and opportunistic investments in complementary, immediately accretive bolt-on acquisitions.

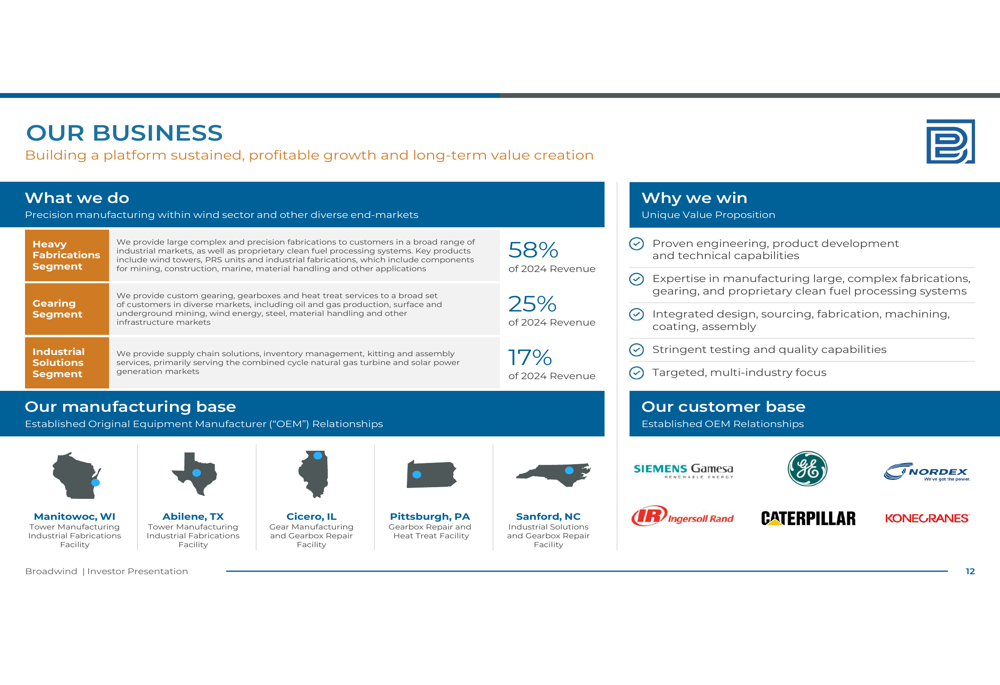

Strategic Initiatives and Outlook

Broadwind is pursuing several strategic initiatives to improve its competitive position and financial performance. The company is reallocating production capacity toward stable revenue streams across diverse markets and optimizing its asset base through the pending sale of its industrial fabrication operations in Manitowoc, Wisconsin.

Management believes this divestiture will increase revenue diversification, optimize assets, and improve the balance sheet. The company plans to provide updated full-year 2025 financial guidance upon closing of the Manitowoc transaction.

As shown in the following business overview, Broadwind’s strategy leverages its engineering capabilities and manufacturing expertise across multiple industries:

The company also highlighted a recent business development, securing over $6 million in follow-on orders for precision machined gearing products, announced on July 25. This order from a leading OEM in the natural gas turbine segment came after the quarter ended and is not reflected in the Q2 results.

Broadwind continues to emphasize its 100% domestic precision manufacturing as a competitive advantage, particularly as trade tariffs and import restrictions benefit U.S. wind tower manufacturers. However, the company faces challenges in improving operational efficiency and restoring profitability while managing its increased debt load and working capital requirements.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.