Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Brookdale Senior Living Inc. (NYSE:BKD) showcased strong first-quarter 2025 performance in its May 6 investor presentation, highlighting significant year-over-year improvements in key financial metrics and raising its full-year guidance. The senior living operator continues to benefit from occupancy gains, operational efficiencies, and favorable demographic trends.

Executive Summary

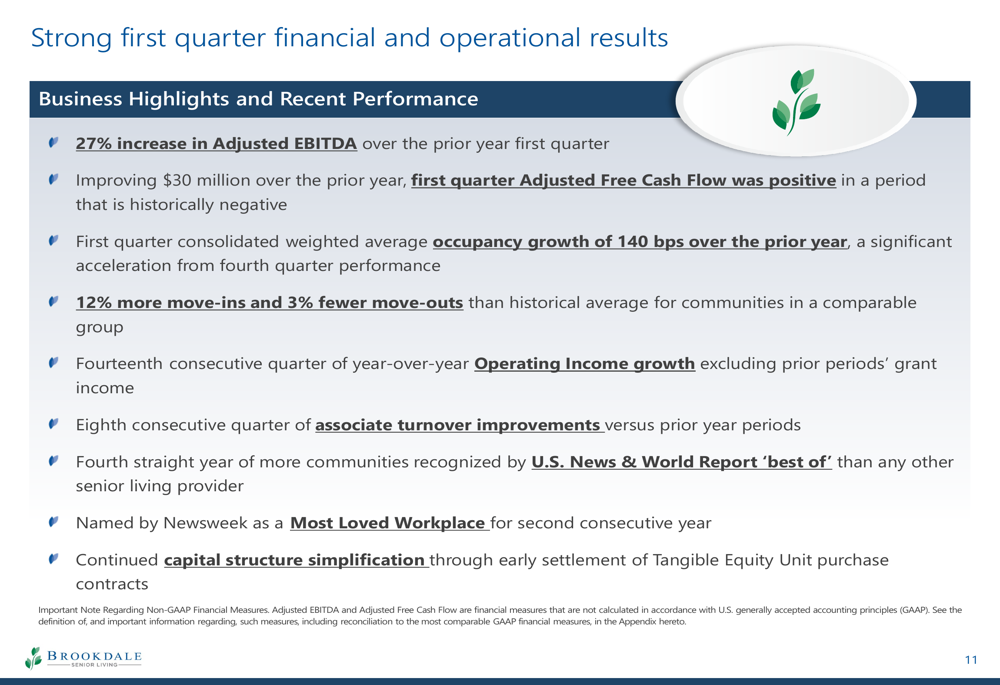

Brookdale reported a 27% increase in Adjusted EBITDA over the prior year for Q1 2025, marking its fourteenth consecutive quarter of year-over-year Operating Income growth. The company achieved positive Adjusted Free Cash Flow in the first quarter, improving $30 million compared to Q1 2024.

As shown in the following comprehensive performance highlights, Brookdale has maintained strong momentum across multiple operational metrics:

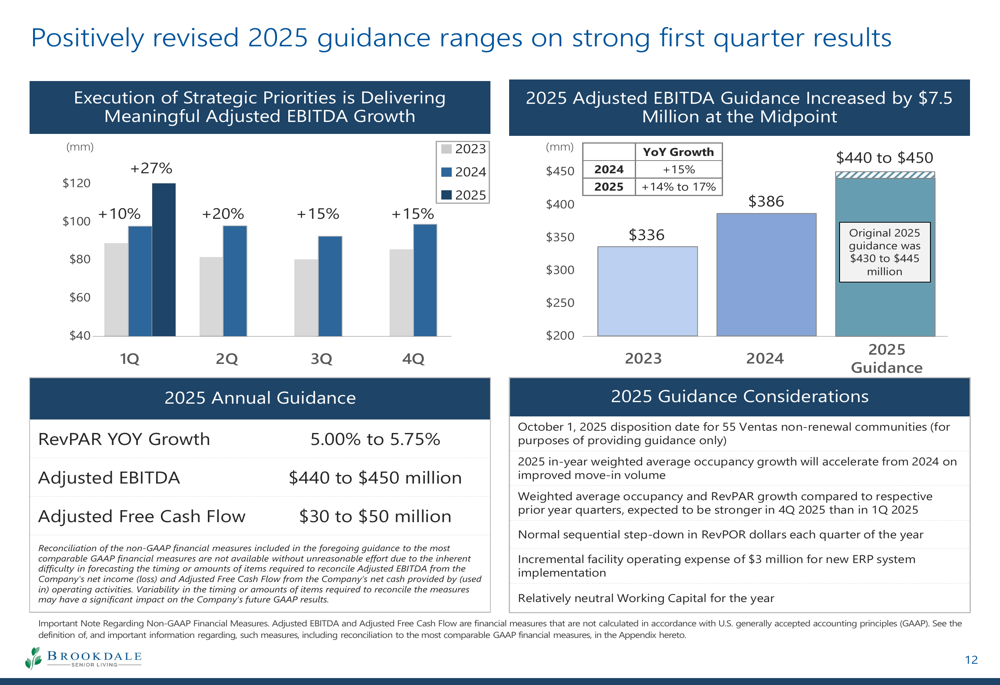

Based on this strong performance, Brookdale raised its full-year 2025 guidance, now projecting Adjusted EBITDA of $440-450 million (up from the original $430-445 million) and Adjusted Free Cash Flow of $30-50 million. The company expects RevPAR year-over-year growth of 5.00% to 5.75%.

Quarterly Performance Highlights

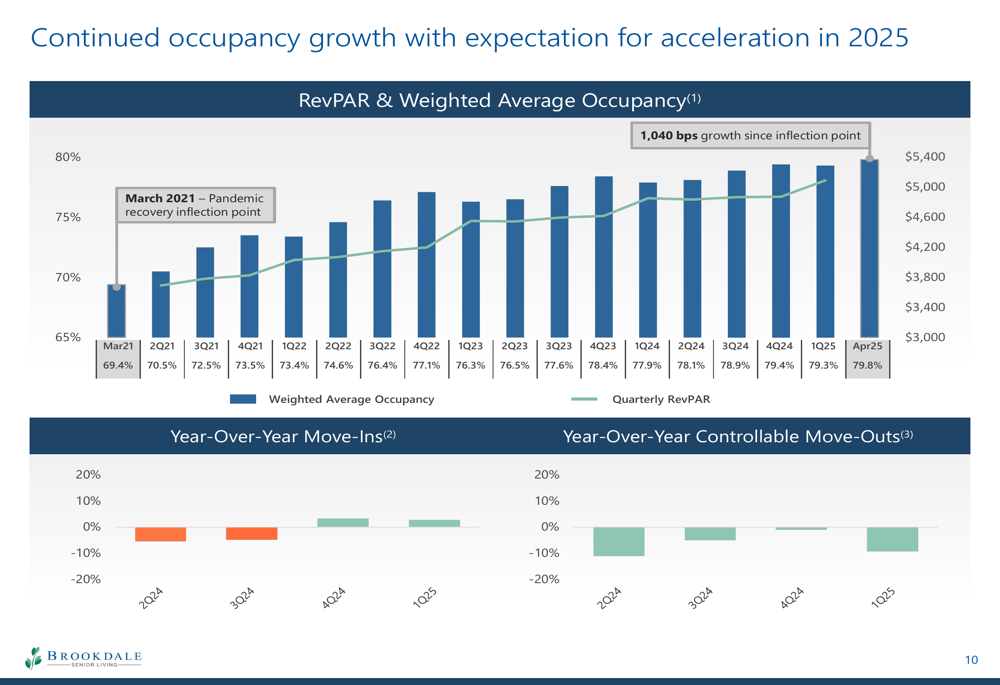

Brookdale’s occupancy continues to recover from pandemic lows, with weighted average occupancy reaching 79.8% in April 2025, representing 1,040 basis points of growth since the post-pandemic inflection point. This occupancy improvement, combined with rate increases, has driven steady RevPAR growth to $386 in April 2025.

The following chart illustrates this consistent occupancy and RevPAR improvement:

The company’s Q1 2025 performance builds on momentum from previous quarters. According to the earnings article from Q2 2024, Brookdale had already demonstrated significant improvement with a 20% increase in adjusted EBITDA and a 26% improvement in adjusted free cash flow compared to the previous year.

Strategic Initiatives

Brookdale’s 2025 strategic priorities focus on three key areas: maximizing unit occupancy at profitable rates, attracting and retaining quality associates, and earning resident and family trust through high-quality care and personalized service.

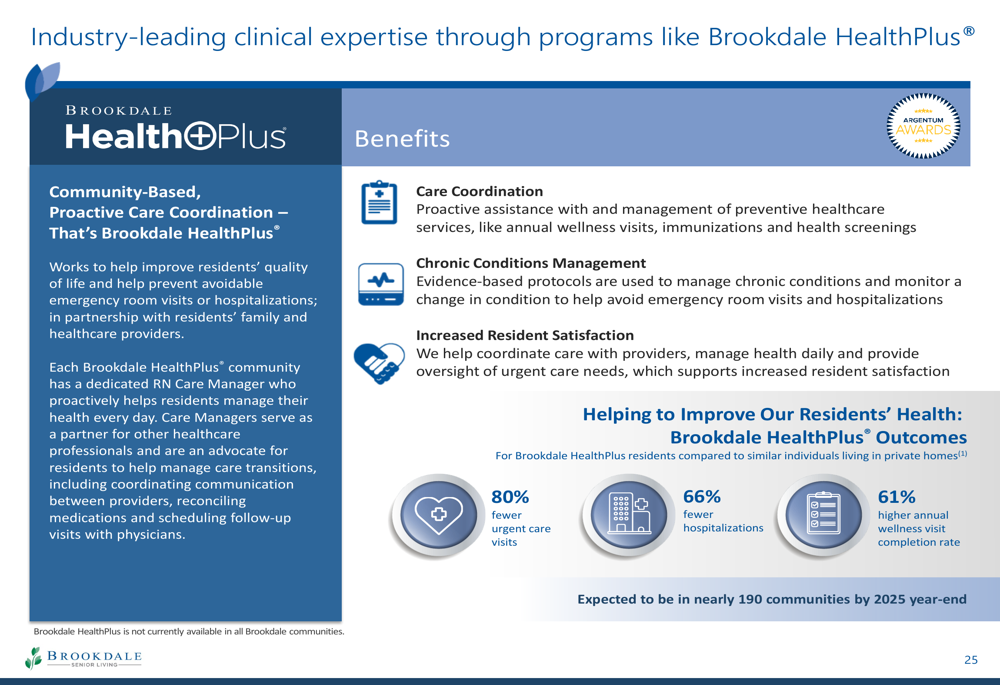

A significant component of Brookdale’s differentiation strategy is its HealthPlus program, a community-based, proactive care coordination initiative that has demonstrated impressive results in reducing hospitalizations and urgent care visits while improving wellness visit completion rates:

The company plans to expand this program to nearly 190 communities by the end of 2025, up from 49 communities mentioned in the Q2 2024 earnings report, which had targeted 130 communities by the end of 2024.

Market Position & Industry Outlook

As the largest senior living operator in the United States, Brookdale maintains a significant competitive advantage in a highly fragmented industry. The company operates 647 communities across 41 states, serving approximately 58,000 residents with 36,000 associates.

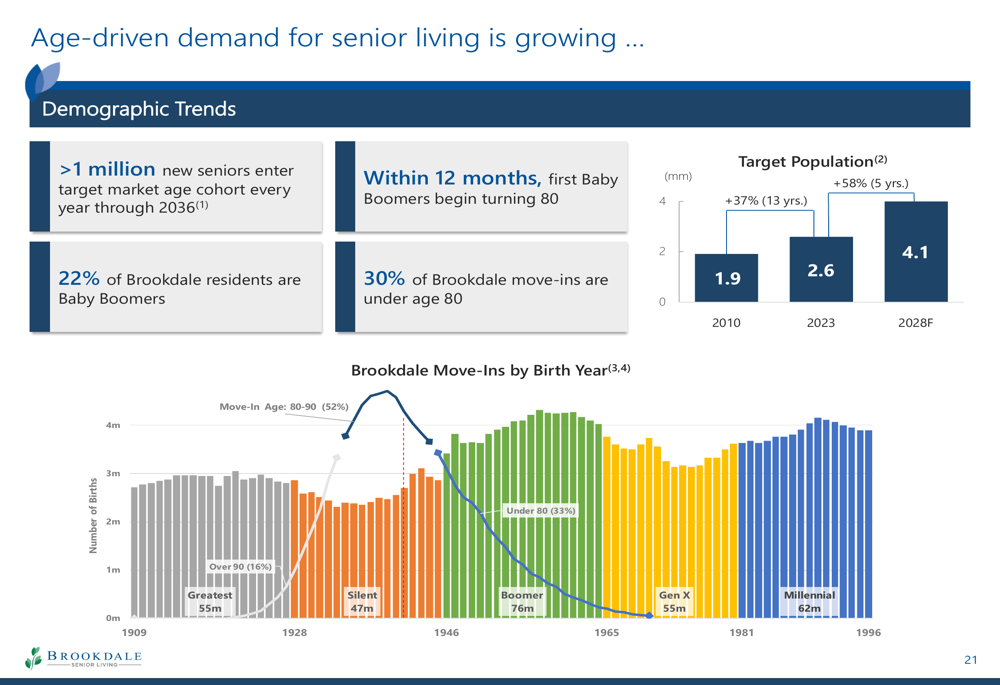

Brookdale is positioned to benefit from strong demographic tailwinds, with more than one million new seniors entering the target market age cohort annually through 2036. Notably, the first Baby Boomers will begin turning 80 within the next 12 months, representing a significant inflection point for the industry.

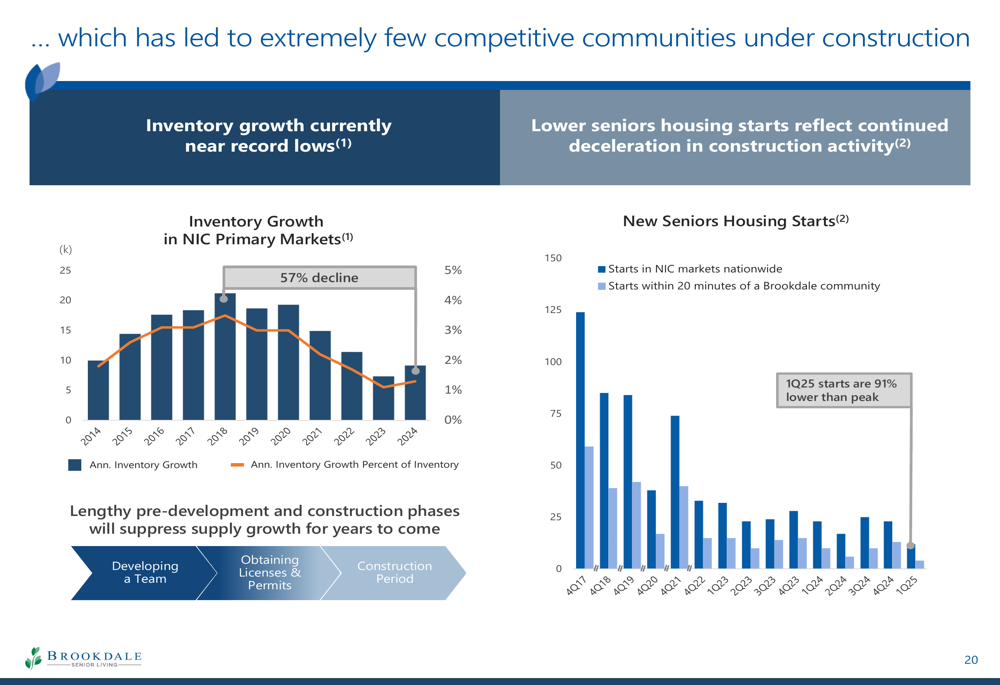

The company also stands to benefit from limited new supply in the senior housing market. Construction costs have increased 35% since 2020, while labor shortages and elevated interest rates have significantly reduced new development activity:

Financial Structure & Long-term Growth Potential

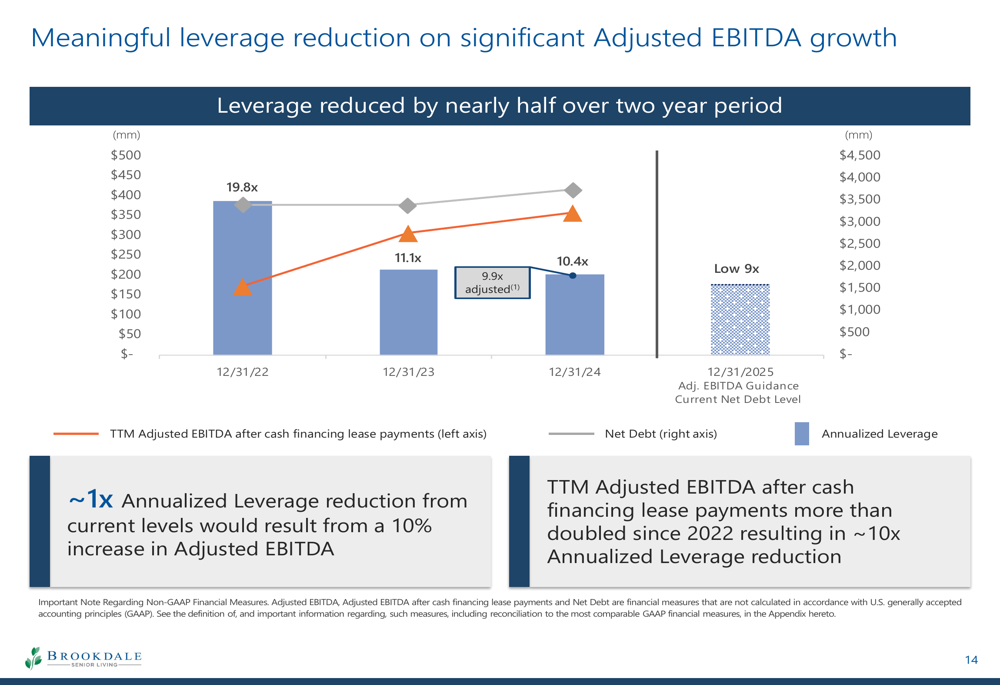

Brookdale has made significant progress in reducing its leverage, with annualized leverage decreasing from 19.8x in December 2022 to a projected 9x by December 2025. This improvement has been driven by both debt reduction and EBITDA growth.

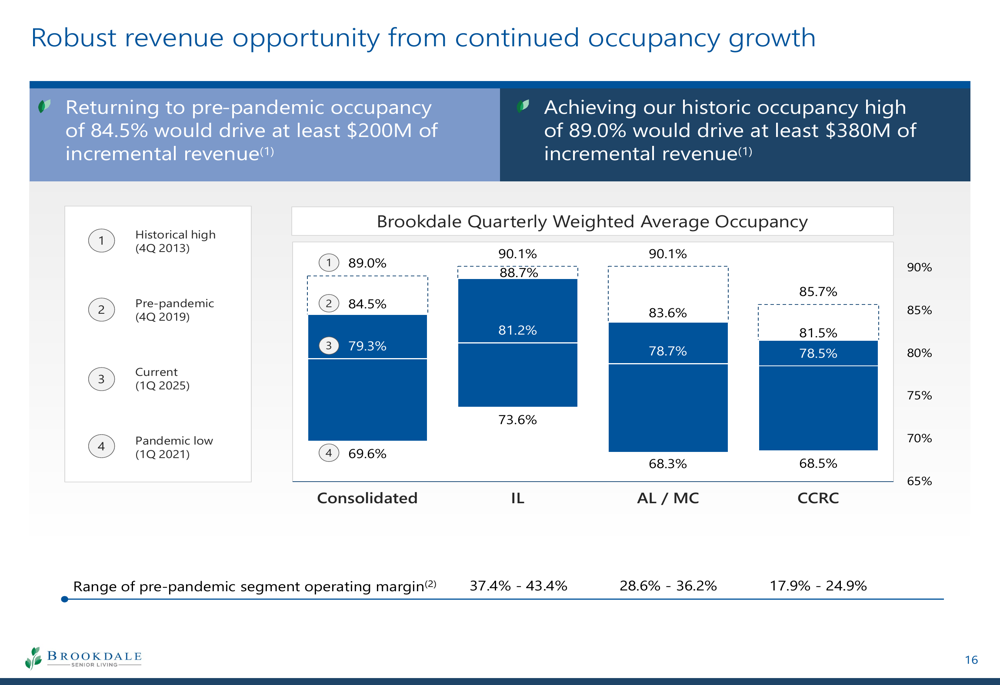

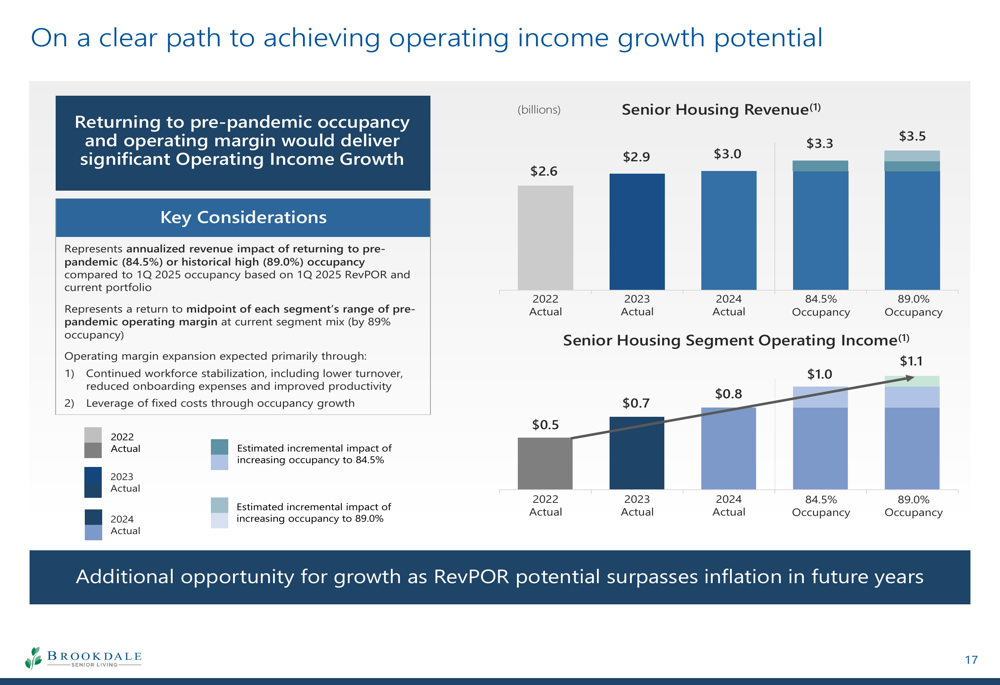

The company has quantified its revenue opportunity from continued occupancy growth, noting that returning to pre-pandemic occupancy of 84.5% would generate at least $200 million in incremental revenue, while achieving its historic high of 89.0% would drive at least $380 million in incremental revenue.

This revenue growth potential translates to significant operating income upside, as illustrated in the following projection:

Forward-Looking Statements

Brookdale’s revised 2025 guidance reflects management’s confidence in continued operational improvements and financial growth. The company expects RevPAR growth of 5.00% to 5.75%, Adjusted EBITDA of $440-450 million, and Adjusted Free Cash Flow of $30-50 million for the full year.

Long-term, Brookdale is positioned as a compelling investment opportunity due to its strong brand and leadership position, accelerating demographic growth, positive supply trends, needs-based business model, clinical expertise, and significant real estate value. The company has substantial growth potential from continued occupancy increases and improved fixed-cost leverage.

While the presentation highlights Brookdale’s strengths and opportunities, investors should note that the Q2 2024 earnings report mentioned some challenges, including softer move-ins due to a decline in paid third-party referrals and increased facility operating expenses. The company’s ability to navigate these challenges while executing on its growth strategy will be key to achieving its projected financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.