Street Calls of the Week

Introduction & Market Context

Brookline Bancorp Inc. (NASDAQ:BRKL) reported its second quarter 2025 financial results on July 24, showing improved profitability despite strategic loan portfolio contraction as the company prepares for its upcoming merger with Berkshire Hills (NYSE:BHLB) Bancorp. The bank’s shares have traded in a range between $9.24 and $13.15 over the past 52 weeks, with recent trading at $10.32, down 1.26% following the earnings release.

The company delivered earnings per share of $0.25, meeting market expectations, while revenue came in at $94.7 million, slightly below analysts’ forecasts of $94.9 million. The results demonstrate Brookline’s focus on margin improvement and deposit growth while strategically managing its commercial real estate exposure.

Quarterly Performance Highlights

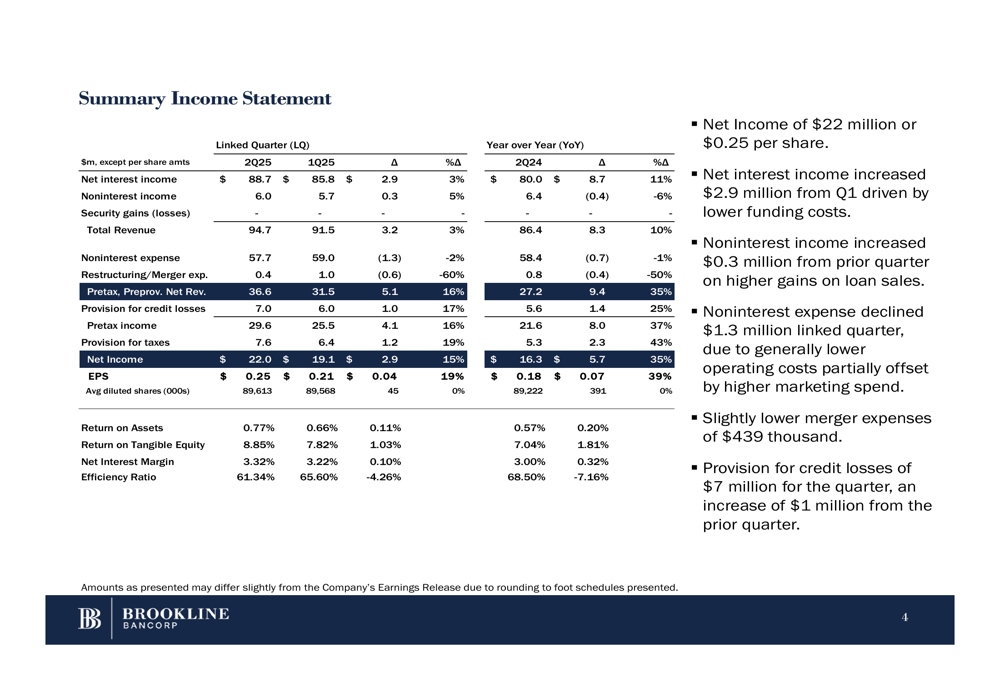

Brookline reported net income of $22.0 million for Q2 2025, representing a significant improvement from both the linked quarter ($19.1 million) and the same period last year ($16.3 million). On an operating basis, excluding $0.4 million in merger-related expenses, earnings reached $22.4 million.

The company’s profitability metrics showed notable improvement, with return on assets increasing to 0.77% from 0.66% in the previous quarter and 0.57% a year ago. Return on tangible equity rose to 8.85%, up from 7.82% in Q1 2025 and 7.04% in Q2 2024.

As shown in the following income statement summary, Brookline’s net interest income grew to $88.7 million, up from $85.8 million in the previous quarter and $80.0 million in the same period last year, while the efficiency ratio improved significantly to 61.34%:

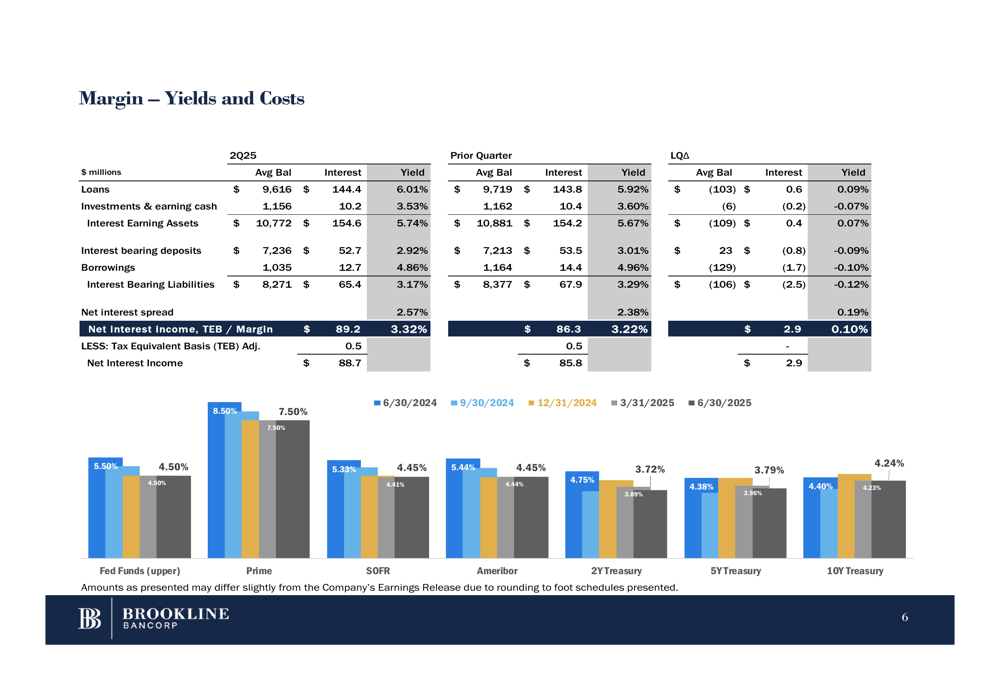

A key driver of improved performance was the expansion in net interest margin, which increased by 10 basis points to 3.32% compared to the previous quarter, continuing an upward trend from 3.00% a year ago. This margin improvement helped offset the impact of strategic loan portfolio contraction.

The following chart illustrates the company’s margin performance, showing the positive trend in yields and spreads:

Balance Sheet Management

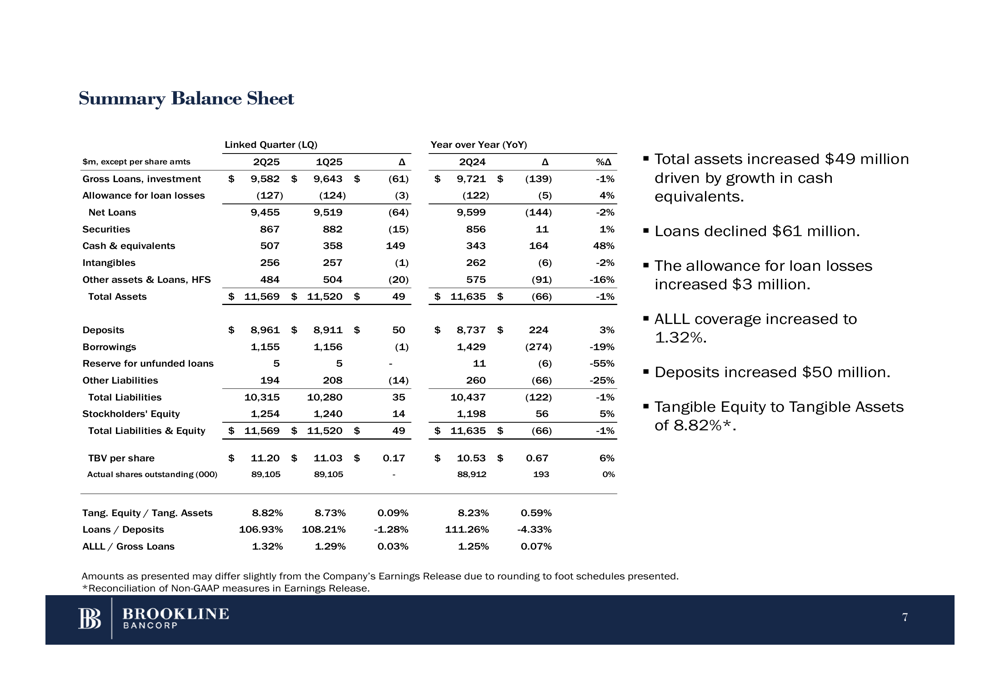

Brookline’s total assets increased by $49 million to $11.57 billion during the quarter, despite a strategic reduction in the loan portfolio. Gross loans declined by $61 million to $9.58 billion, primarily driven by a $95 million reduction in commercial real estate loans as part of the company’s risk management strategy.

The summary balance sheet highlights these changes while showing deposit growth of $50 million:

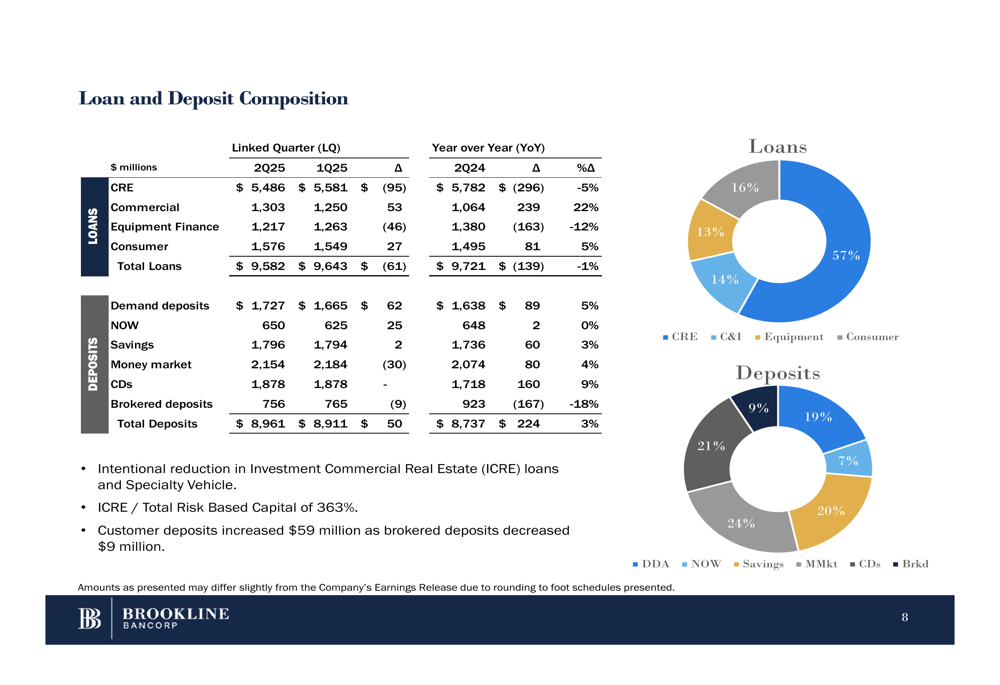

The company maintains a diversified loan portfolio, with commercial real estate representing 57% of total loans, followed by consumer loans at 16%, commercial loans at 14%, and equipment finance at 13%. On the funding side, deposits show healthy diversification across demand deposits (19%), savings accounts (20%), money market accounts (24%), and certificates of deposit (21%).

The following chart provides a detailed breakdown of the loan and deposit composition:

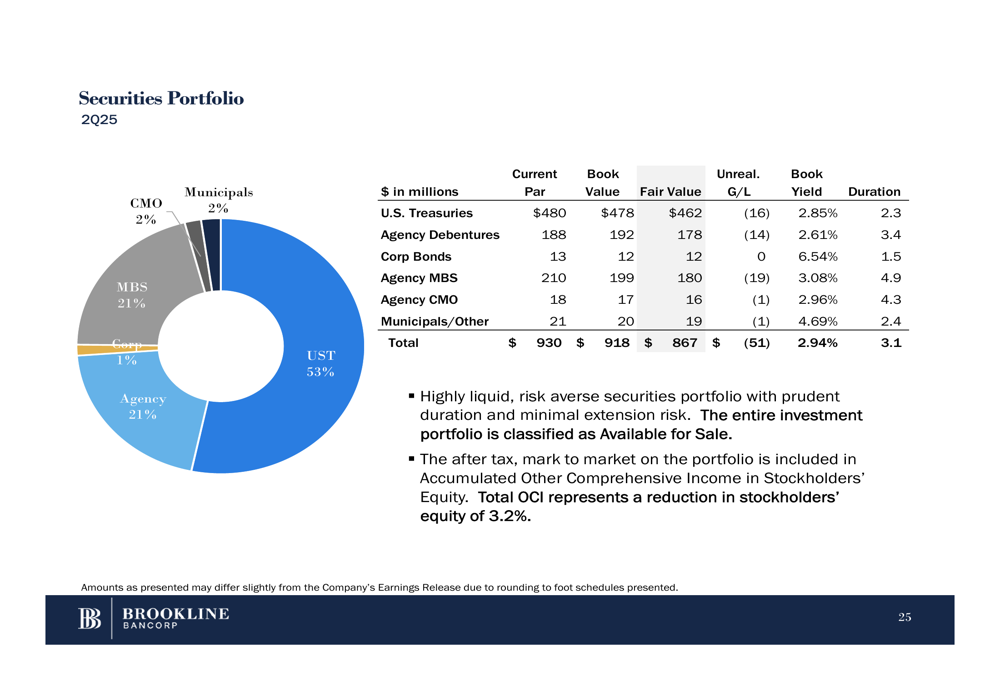

Brookline’s securities portfolio remains well-structured, with unrealized losses of $50.9 million as of Q2 2025. The portfolio is predominantly composed of U.S. Treasury securities (53%), with agency securities and mortgage-backed securities each representing 21%:

Capital Position & Credit Quality

Brookline maintains a strong capital position, with all regulatory ratios well above the "well-capitalized" thresholds. The company reported a total risk-based capital ratio of 13.0% and a tangible equity to tangible assets ratio of 8.8%.

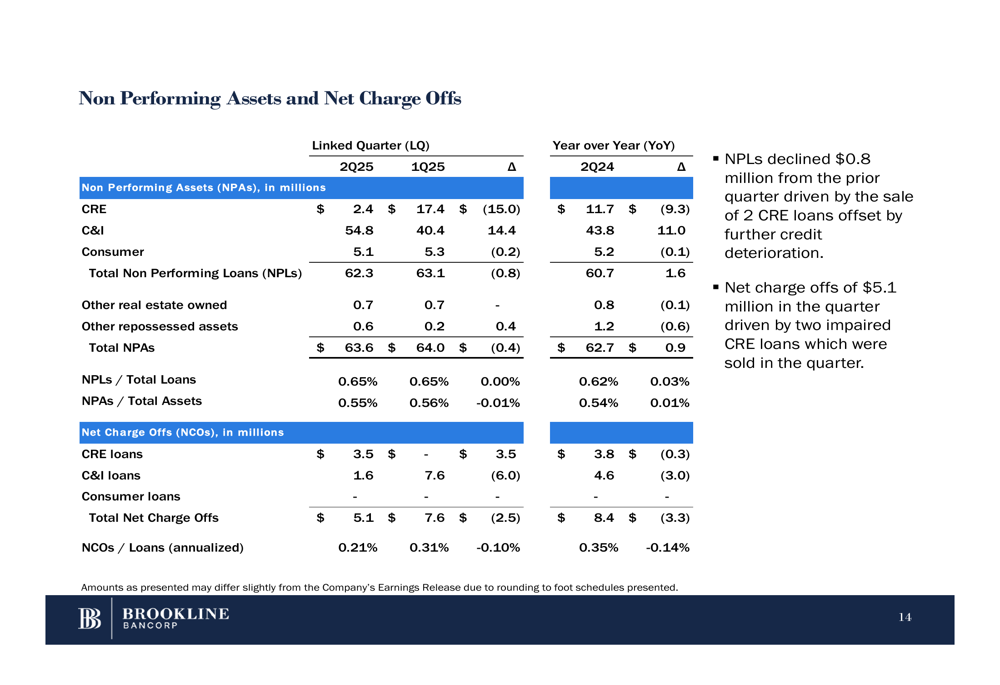

Credit quality metrics showed some pressure but remained manageable. Non-performing assets to total assets stood at 0.55%, while net charge-offs for the quarter were $5.1 million (0.21% annualized), primarily driven by two impaired commercial real estate loans that were sold during the quarter.

The following table details the company’s non-performing assets and charge-offs:

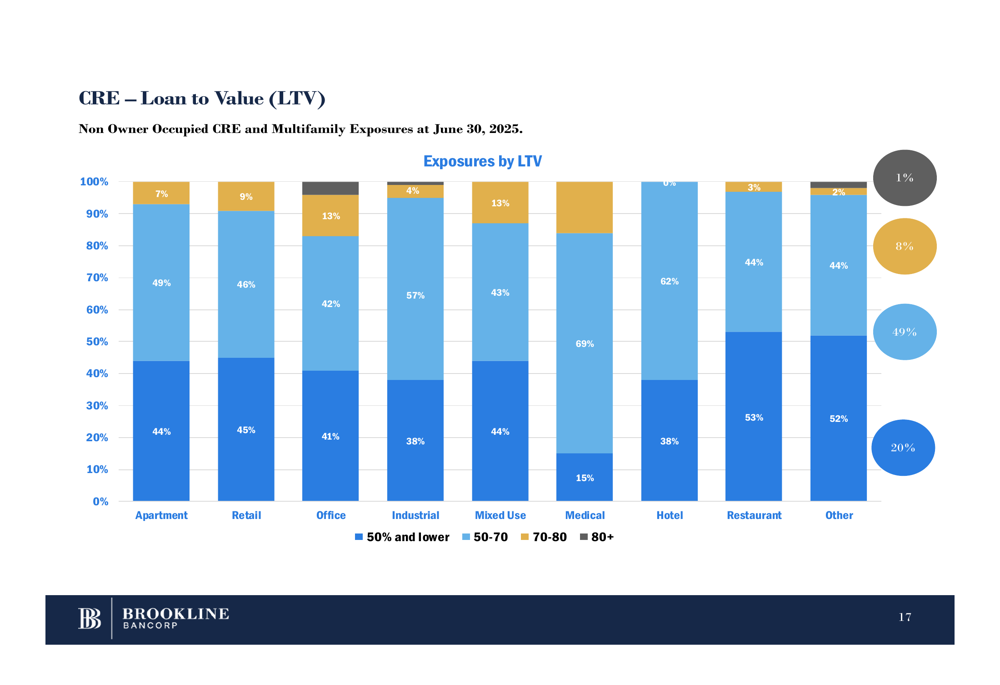

The company’s commercial real estate portfolio shows prudent risk management, with loan-to-value ratios concentrated in the lower risk bands. For apartments, which represent a significant portion of the CRE portfolio, 44% of loans have LTVs of 50% or lower, demonstrating conservative underwriting standards:

Berkshire Hills Bancorp Merger Update

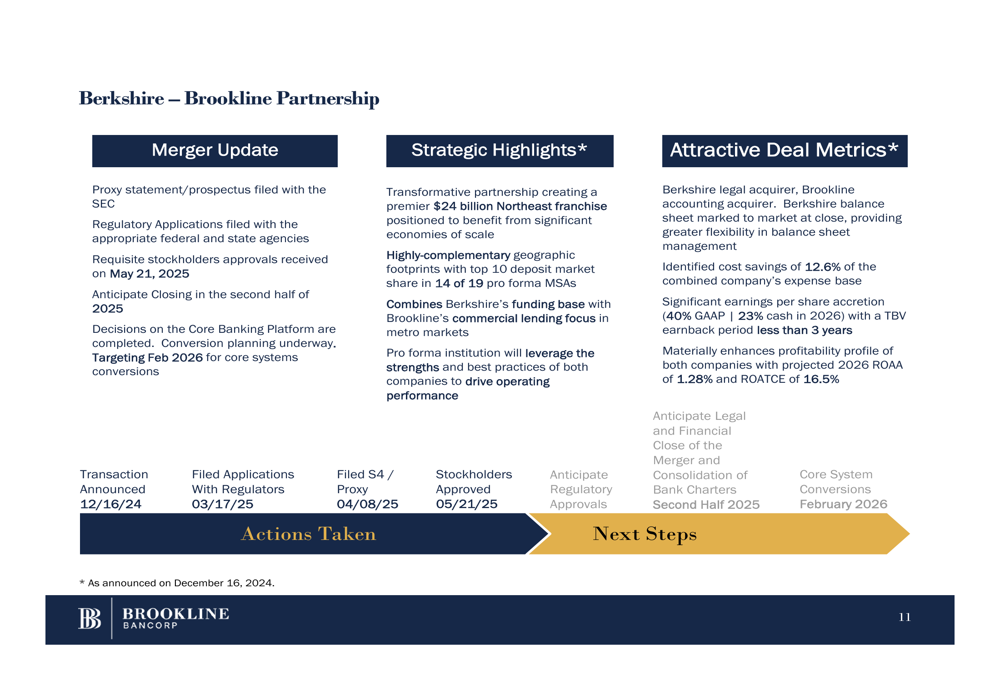

A significant strategic focus for Brookline is its pending merger with Berkshire Hills Bancorp, which received stockholder approval on May 21, 2025, and is expected to close in the second half of 2025. The merger will create a $24 billion Northeast franchise with complementary geographic footprints.

The company anticipates significant financial benefits from the merger, including cost savings of 12.6% of the combined company’s expense base and substantial earnings accretion (40% GAAP and 23% cash in 2026) with a tangible book value earnback period of less than three years.

The following slide outlines the merger progress and strategic benefits:

Forward Outlook

Looking ahead, Brookline anticipates modest improvements in its net interest margin, projecting an increase of 4-8 basis points in Q3. The company is strategically positioning its balance sheet ahead of the Berkshire Hills merger, focusing on maintaining strong capital levels and credit quality while managing its commercial real estate exposure.

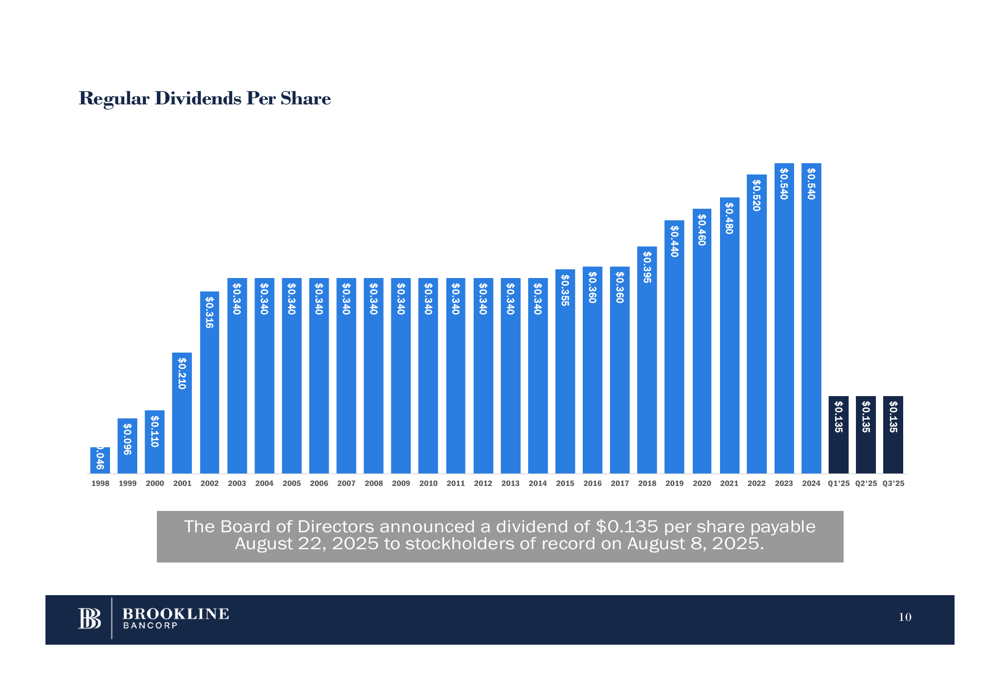

The bank continues to demonstrate its commitment to shareholder returns, maintaining a quarterly dividend of $0.135 per share, payable on August 22, 2025, to stockholders of record as of August 8, 2025. This continues the company’s long history of consistent dividend payments:

Management remains focused on the successful completion of the Berkshire Hills merger, with core systems conversion targeted for February 2026. The combined entity is expected to leverage the strengths and best practices of both institutions to drive improved operating performance and shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.