S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Brunswick Corporation (NYSE:BC) reported its second quarter 2025 results on July 24, showing flat sales but declining margins as tariff impacts weighed on profitability. The marine industry leader highlighted record free cash flow generation as a bright spot amid earnings pressure.

Quarterly Performance Highlights

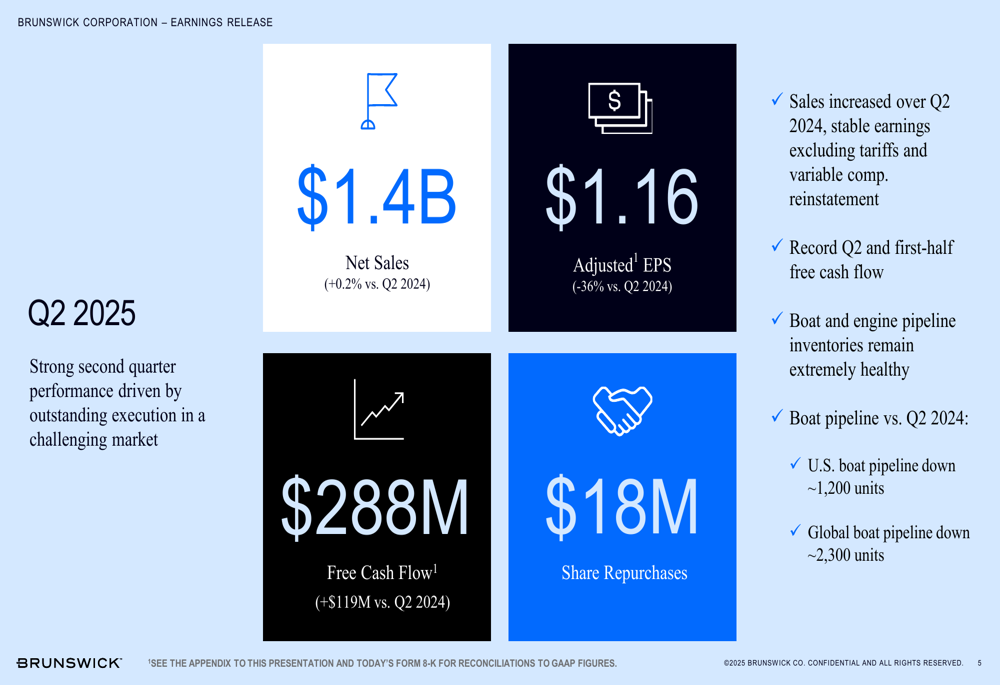

Brunswick reported Q2 2025 net sales of $1.4 billion, a slight increase of 0.2% compared to the same period last year. However, adjusted earnings per share (EPS) fell 36% year-over-year to $1.16, while adjusted operating margin declined to 8.7% from 12.5% in Q2 2024.

The company’s free cash flow performance stood out as a significant achievement, reaching $288 million in Q2 2025, a $119 million increase compared to Q2 2024 and a record for any second quarter in the company’s history.

As shown in the following chart of Brunswick’s Q2 2025 financial performance:

"Sales increased over Q2 2024, with stable earnings excluding tariffs and variable compensation reinstatement," noted the company in its presentation. Brunswick also highlighted that boat and engine inventories remain "extremely healthy," with the U.S. boat pipeline down approximately 1,200 units and global boat pipeline down approximately 2,300 units versus Q2 2024.

Segment Analysis

Brunswick’s Propulsion segment was a standout performer, with Q2 2025 net sales increasing 7% to $598.2 million, driven by strong outboard engine performance, particularly in higher horsepower categories. However, adjusted operating margin declined 420 basis points to 11.3%, and adjusted operating earnings fell 22% to $67.3 million compared to Q2 2024.

The Engine Parts & Accessories segment delivered a 1% sales increase to $337.8 million, while operating margin declined 130 basis points to 21.3%. The company noted steady performance despite unfavorable weather in the U.S. at the start of the boating season.

The following chart details Brunswick’s Propulsion segment performance:

The Navico Group segment experienced a 4% sales decline to $202.3 million, with adjusted operating margin falling 210 basis points to 5.3%. Brunswick cited "continued steady aftermarket sales and strong new product momentum, with OEM and Specialty channels improving."

The Boat segment saw a 7% sales decline to $405.6 million, with adjusted operating margin dropping 290 basis points to 3.3%. The company characterized this as "steady performance consistent with expectations" and maintained that pipeline inventory remains healthy.

Industry Context and Market Position

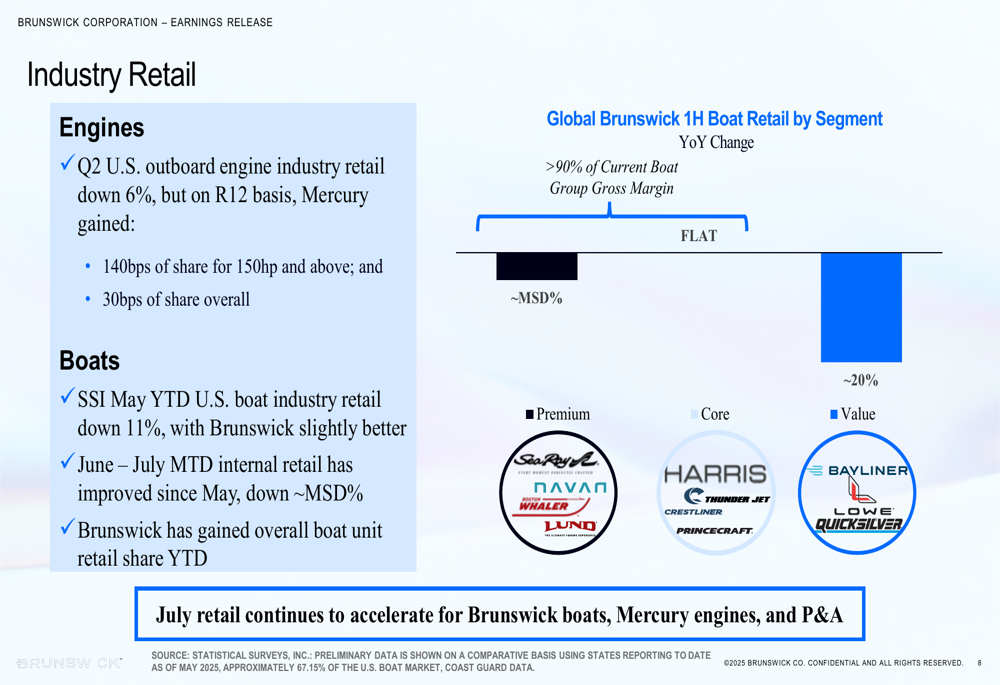

Brunswick is navigating a challenging industry environment, with May year-to-date U.S. boat industry retail down 11%, though the company noted its performance was "slightly better." The company has gained overall boat unit retail share year-to-date, with premium segments performing significantly better than value segments.

In the engine market, Q2 U.S. outboard engine industry retail was down 6%, but Mercury gained 140 basis points of share in the 150hp and above category and 30 basis points of share overall on a rolling 12-month basis.

The following chart illustrates Brunswick’s industry retail performance:

The company highlighted its Freedom Boat Club expansion to 433 global locations, including its first Middle East location in Dubai, as part of its business innovation strategy. Brunswick also emphasized that it’s on track to earn over 100 industry awards in 2025, with more than 50 already secured through Q2.

Tariff Impact and Cash Flow Strength

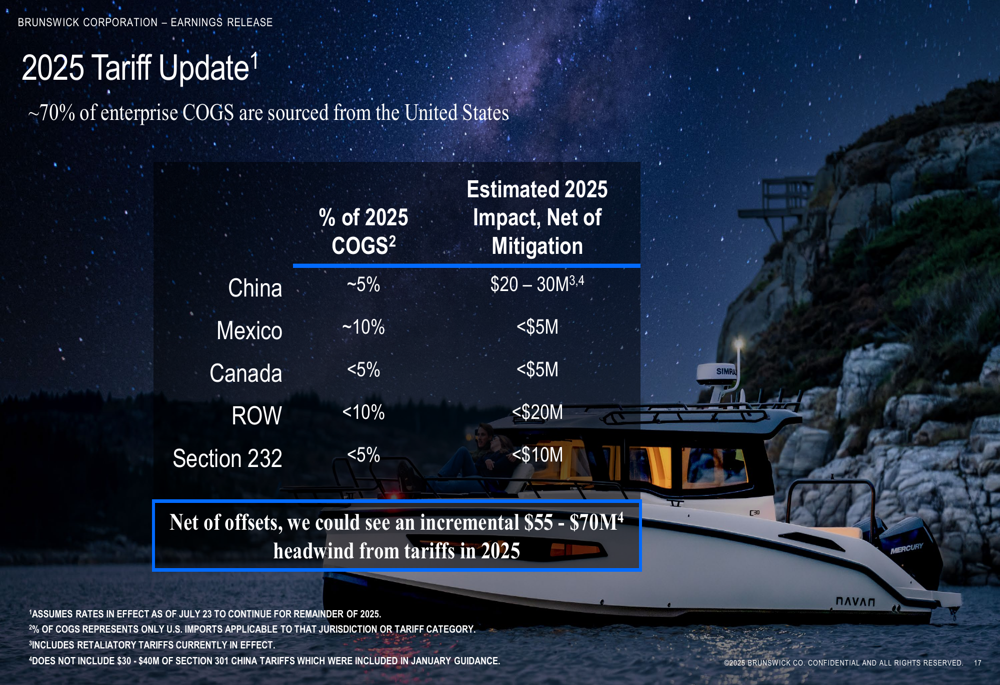

A significant focus of Brunswick’s presentation was the impact of tariffs on its business. The company projects an incremental enterprise tariff exposure of $55-70 million for fiscal year 2025, outpacing its tariff mitigation efforts.

The following chart details Brunswick’s projected tariff impact for 2025:

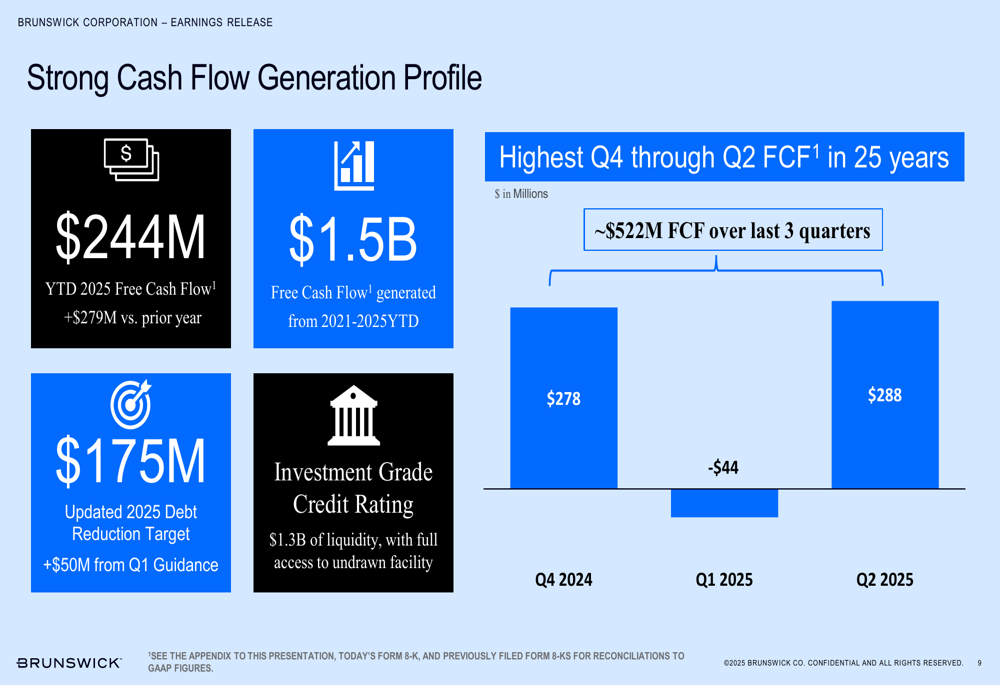

Despite these headwinds, Brunswick’s cash flow generation remains robust. Year-to-date 2025 free cash flow reached $244 million, up $279 million versus the prior year. The company has generated $1.5 billion in free cash flow from 2021 through the first half of 2025.

As illustrated in the following chart of Brunswick’s cash flow performance:

Brunswick has increased its 2025 debt reduction target to $175 million, up $50 million from its Q1 guidance. The company maintains an investment grade credit rating with $1.3 billion of liquidity and full access to an undrawn facility.

2025 Guidance and Outlook

Brunswick updated its full-year 2025 guidance, projecting revenue of approximately $5.2 billion, operating margin of around 7.0%, EPS of approximately $3.25, and free cash flow exceeding $400 million. For the third quarter, the company expects revenue between $1.1 billion and $1.3 billion and EPS between $0.75 and $0.90.

The following chart presents Brunswick’s updated 2025 guidance:

Market Reaction

Despite Brunswick’s emphasis on cash flow strength and market share gains, investors appeared to focus on the earnings decline and margin pressure. According to available data, Brunswick’s stock was down 8.69% in premarket trading following the earnings release, trading at $59.07.

This reaction contrasts with the company’s Q1 2025 performance, when Brunswick’s stock surged 5.7% after beating market expectations with an EPS of $0.56 against a forecast of $0.24.

The negative market response likely reflects concerns about continued margin compression due to tariff impacts and the challenging retail environment, particularly in the value boat segment, despite the company’s strong cash generation and healthy inventory position.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.