Nvidia’s results, Tesla’s European sales, Japan trade - what’s moving markets

Introduction & Market Context

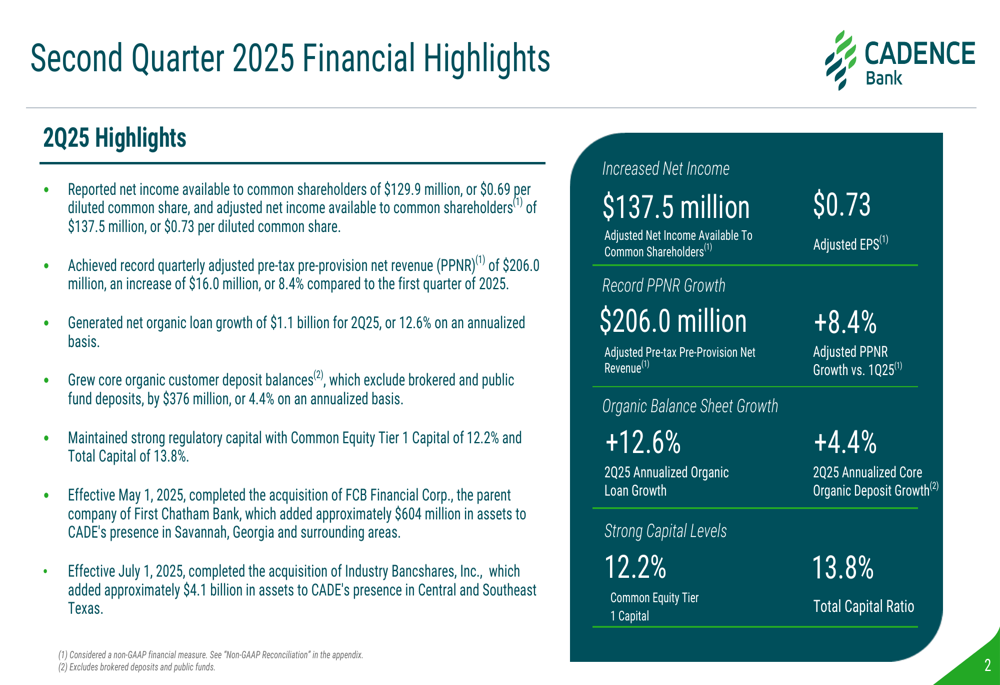

Cadence Bank (NASDAQ:CADE) released its second quarter 2025 earnings presentation on July 23, highlighting record pre-tax pre-provision net revenue (PPNR) and the completion of two strategic acquisitions. The bank reported net income available to common shareholders of $129.9 million, or $0.69 per diluted share, with adjusted earnings of $0.73 per share. Following the announcement, Cadence shares closed at $35.47, up 1.27% for the day.

The bank’s performance comes amid a period of strategic expansion in the southern United States, particularly strengthening its footprint in Georgia and Texas through acquisitions. These results follow a strong first quarter where the bank exceeded analyst expectations with EPS of $0.71.

Quarterly Performance Highlights

Cadence Bank achieved record quarterly adjusted pre-tax pre-provision net revenue of $206.0 million in Q2 2025, representing an 8.4% increase from the previous quarter’s $190 million. The bank also reported robust organic growth metrics, with net organic loan growth of $1.1 billion (12.6% annualized) and core organic customer deposit growth of $376 million (4.4% annualized).

As shown in the following comprehensive overview of the quarter’s financial highlights:

Despite the strong PPNR performance, the bank’s net interest margin declined by 6 basis points to 3.40%, compared to 3.46% in Q1 2025. This slight compression reflects ongoing challenges in the interest rate environment, though the bank has maintained strong overall profitability.

Strategic Acquisitions

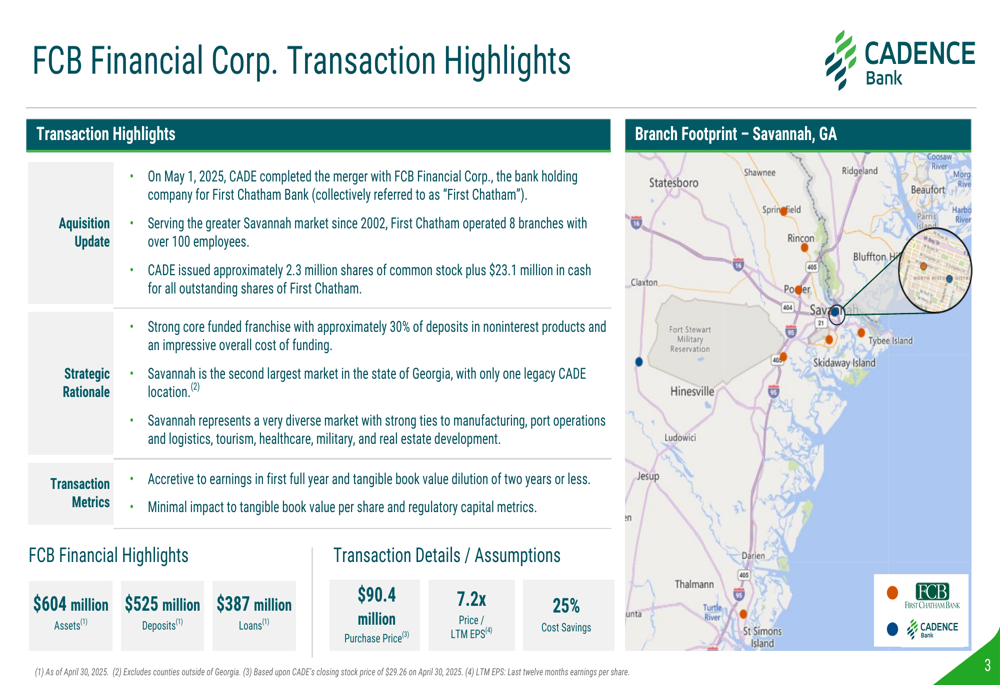

A key highlight of the quarter was the completion of two strategic acquisitions that significantly expanded Cadence Bank’s footprint. On May 1, 2025, the bank completed its merger with FCB Financial Corp., adding approximately $604 million in assets and enhancing its presence in the Savannah, Georgia market.

The FCB Financial acquisition details are illustrated in this transaction summary:

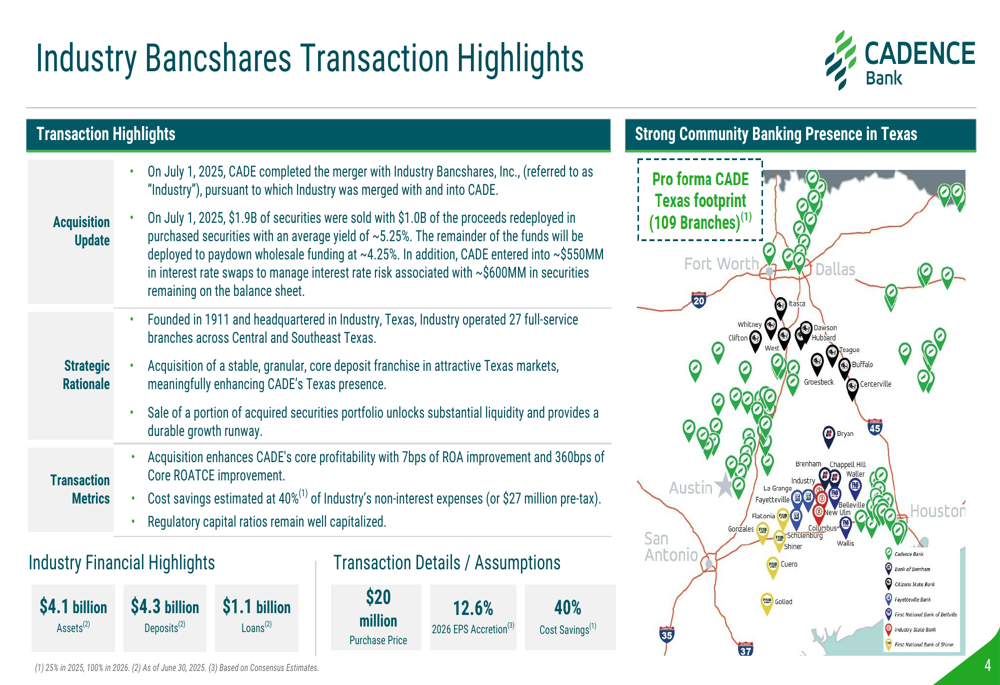

Following closely, on July 1, 2025, Cadence completed its acquisition of Industry Bancshares, adding approximately $4.1 billion in assets and substantially strengthening its Texas presence with 27 additional full-service branches across Central and Southeast Texas.

The strategic rationale and financial impact of the Industry Bancshares acquisition are detailed in this overview:

These acquisitions align with Cadence’s stated strategy of expanding in high-growth markets while maintaining strong capital ratios. The bank reported that both transactions are expected to be accretive to earnings, with the Industry Bancshares acquisition projected to provide 12.6% EPS accretion in 2026.

Balance Sheet Strength

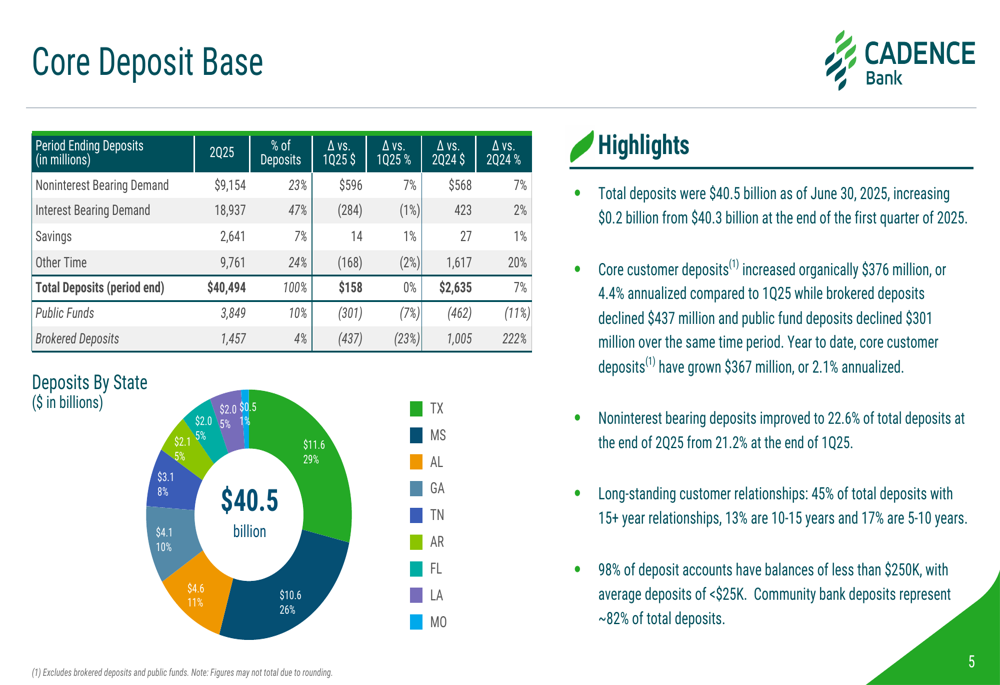

Cadence Bank maintained a strong balance sheet with total deposits of $40.5 billion and total loans and leases of $35.5 billion as of June 30, 2025. The deposit base remains well-diversified across the bank’s footprint, with Texas representing the largest share at 29% of total deposits.

The following chart provides a detailed breakdown of the bank’s core deposit base:

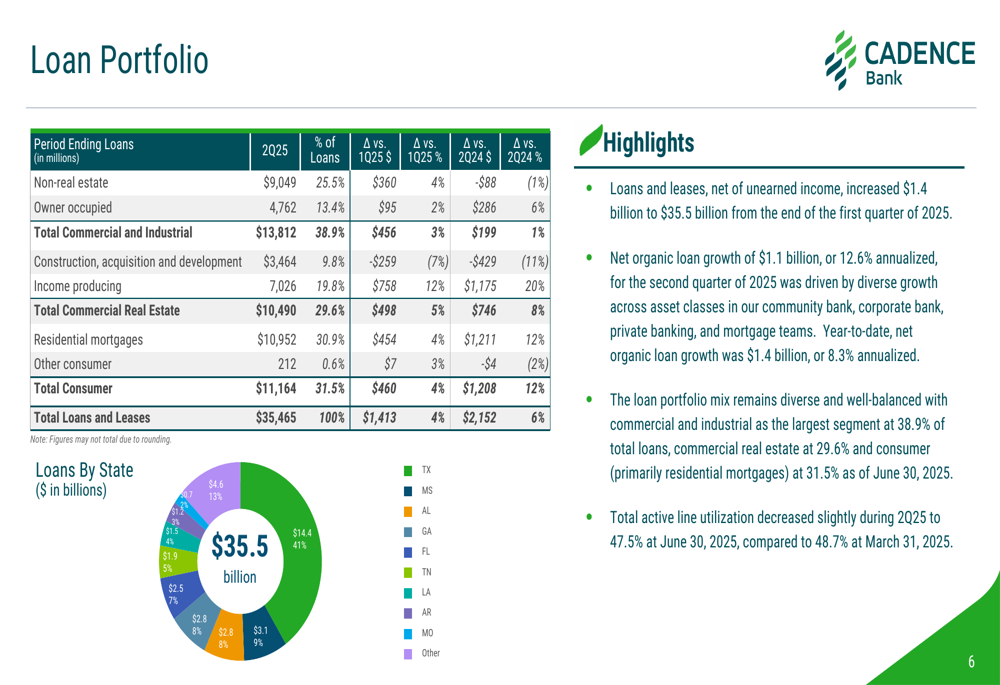

The loan portfolio similarly shows strong diversification across geographies and sectors, with Texas representing 41% of total loans. Commercial and Industrial (C&I) loans constitute the largest segment at 38.9% of the portfolio, followed by Consumer loans at 31.5% and Commercial Real Estate at 29.6%.

As illustrated in this comprehensive loan portfolio breakdown:

Credit Quality

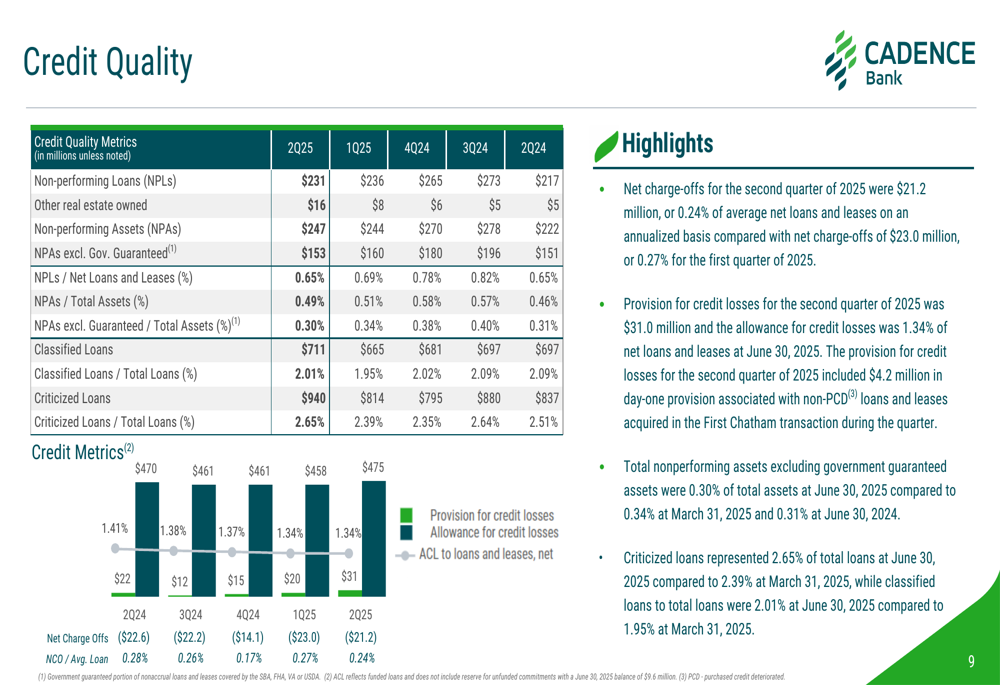

Credit quality metrics remained stable during the quarter, with non-performing loans (NPLs) totaling $231 million and non-performing assets (NPAs) at $247 million. Net charge-offs for the second quarter were $21.2 million.

The following chart details the bank’s credit quality metrics:

The bank’s allowance for credit losses and provision trends indicate a prudent approach to risk management amid economic uncertainties. Cadence maintained strong regulatory capital levels, with Common Equity Tier 1 Capital of 12.2% and Total (EPA:TTEF) Capital of 13.8%, well above regulatory requirements.

Net Interest Income Dynamics

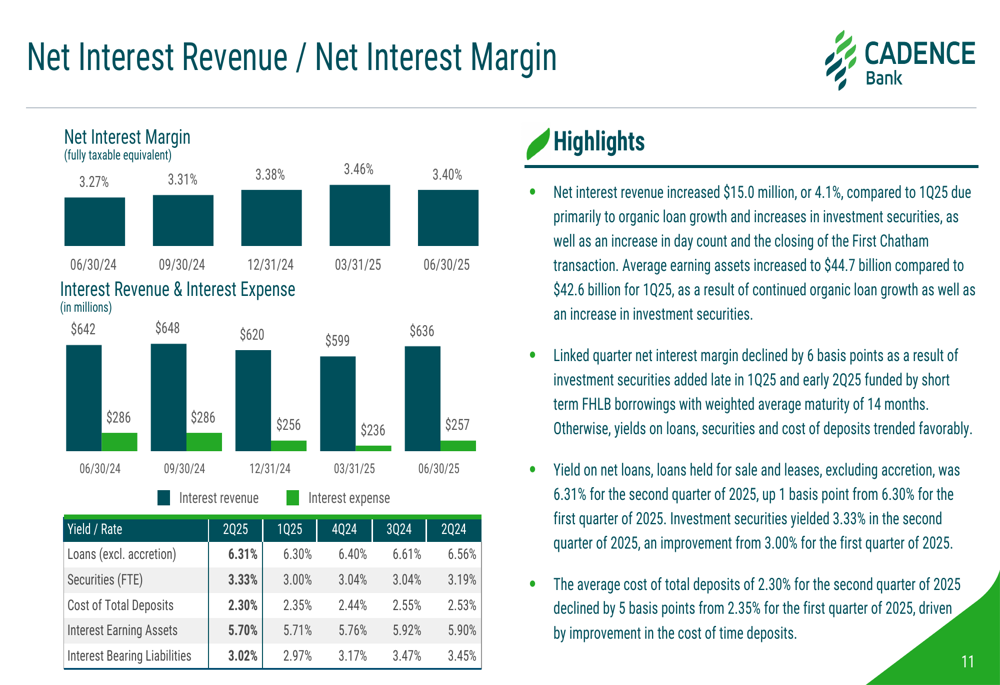

While Cadence reported strong overall performance, net interest margin declined by 6 basis points quarter-over-quarter to 3.40%. This compression occurred despite the yield on interest-earning assets increasing to 5.70%, as the cost of interest-bearing liabilities rose to 3.02%.

The following chart illustrates the bank’s net interest revenue and margin trends:

The average cost of total deposits increased to 2.30%, reflecting the competitive deposit environment. However, the bank’s net interest revenue still increased by $15.0 million compared to the previous quarter, demonstrating effective balance sheet management despite margin pressure.

Forward-Looking Statements

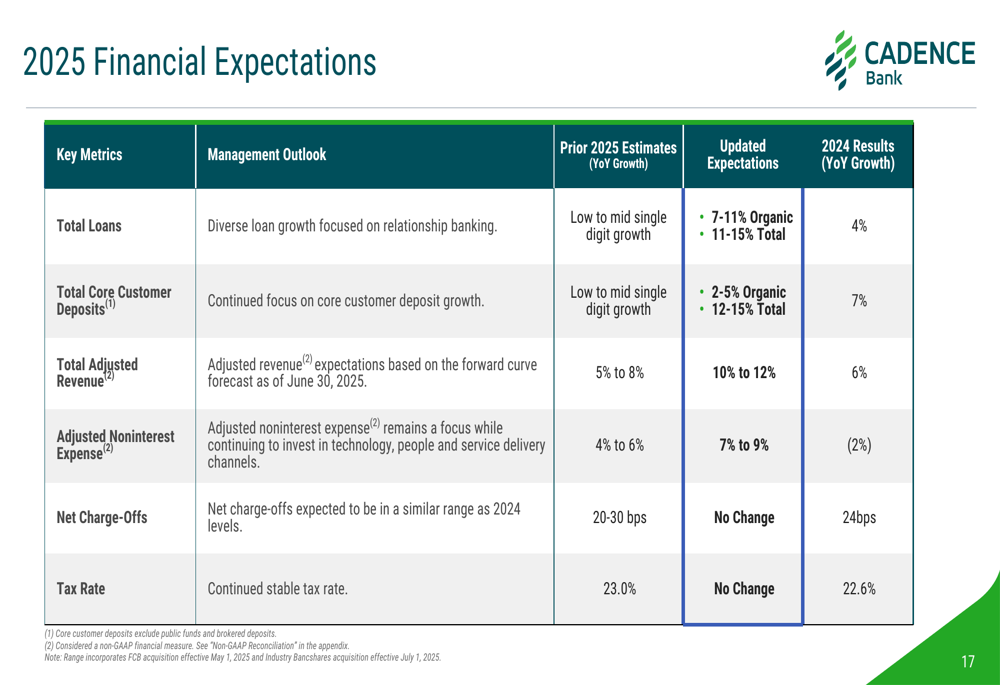

Looking ahead, Cadence Bank provided financial expectations for 2025, projecting continued growth in loans, deposits, and revenue. The bank expects to maintain its strong capital position while continuing to pursue strategic opportunities.

The following slide outlines the bank’s financial expectations for 2025:

Management expects the recently completed acquisitions to contribute meaningfully to earnings in the coming quarters, with the Industry Bancshares transaction projected to provide 12.6% EPS accretion in 2026. The bank also anticipates continued organic growth in its core markets.

Conclusion

Cadence Bank’s Q2 2025 results demonstrate a balanced approach to growth through both strategic acquisitions and organic expansion. While facing some margin pressure, the bank achieved record PPNR and maintained strong credit quality metrics. The successful completion of two acquisitions positions Cadence for continued growth in its key southern markets, particularly in Texas and Georgia.

With a well-diversified loan and deposit base, strong capital position, and clear strategic direction, Cadence appears well-positioned to navigate the current banking environment. Investors will likely focus on how effectively the bank integrates its recent acquisitions and manages net interest margin pressures in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.