Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

Caesars Entertainment (NASDAQ:CZR) presented its Q2 2025 investor slides on July 29, showcasing mixed performance across its business segments. The casino and entertainment giant, which operates over 50 properties across North America, has seen its stock decline more than 51% over the past year, with shares trading at $22.03 at market close on October 14, 2025.

The company’s presentation highlighted its extensive portfolio spanning owned, leased, and managed properties, with a particular emphasis on digital growth offsetting challenges in traditional segments. This comes as the broader gaming industry navigates shifting consumer preferences and economic headwinds.

Quarterly Performance Highlights

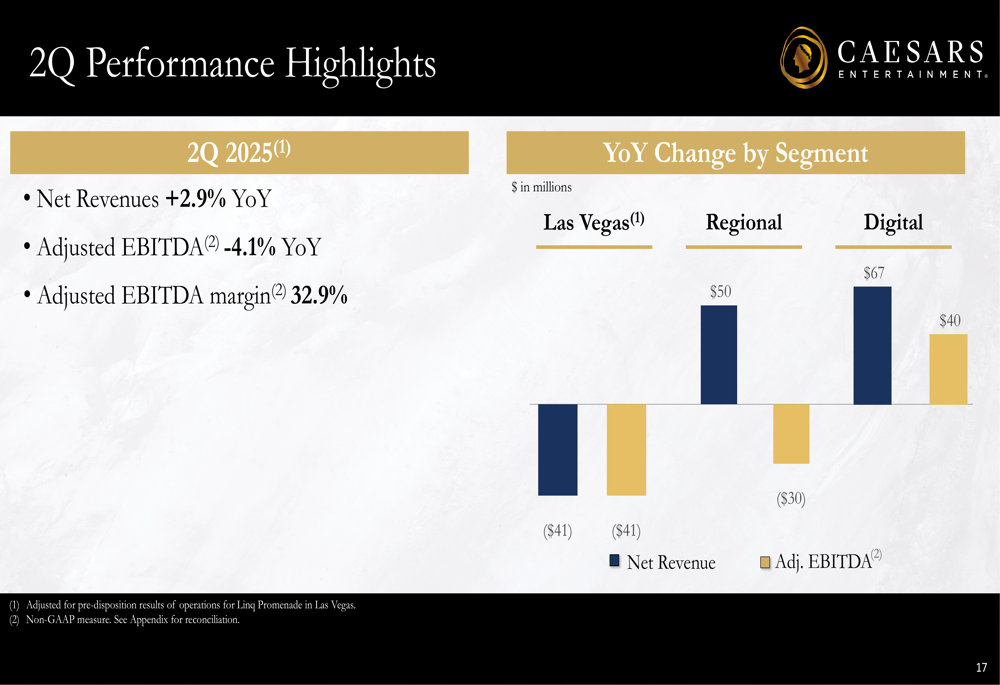

Caesars reported consolidated net revenues of $2.91 billion for Q2 2025, representing a 2.9% increase year-over-year. However, Adjusted EBITDA declined 4.1% to $955 million, with an Adjusted EBITDA margin of 32.9%.

The performance varied significantly across segments, with Digital showing strong growth while Las Vegas faced headwinds. The following chart illustrates the year-over-year changes by segment:

Regional properties delivered $1.44 billion in net revenue, while Las Vegas properties generated $1.05 billion. The company’s digital segment contributed $343 million, showing substantial growth compared to the previous year.

Digital Segment Success

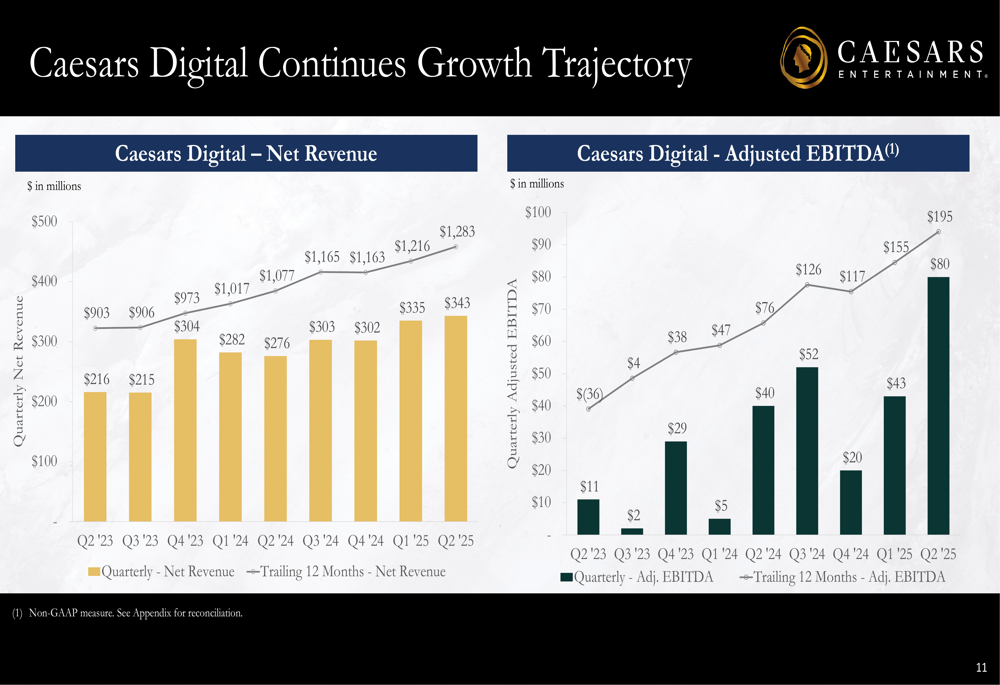

Caesars Digital emerged as the standout performer, posting its best quarter ever with $80 million in Adjusted EBITDA, a 100% increase from Q2 2024. Net revenues for the segment grew 24% year-over-year, with iGaming handle increasing 33% and sports net gaming revenue rising 28%.

The following chart demonstrates the impressive growth trajectory of Caesars Digital over recent quarters:

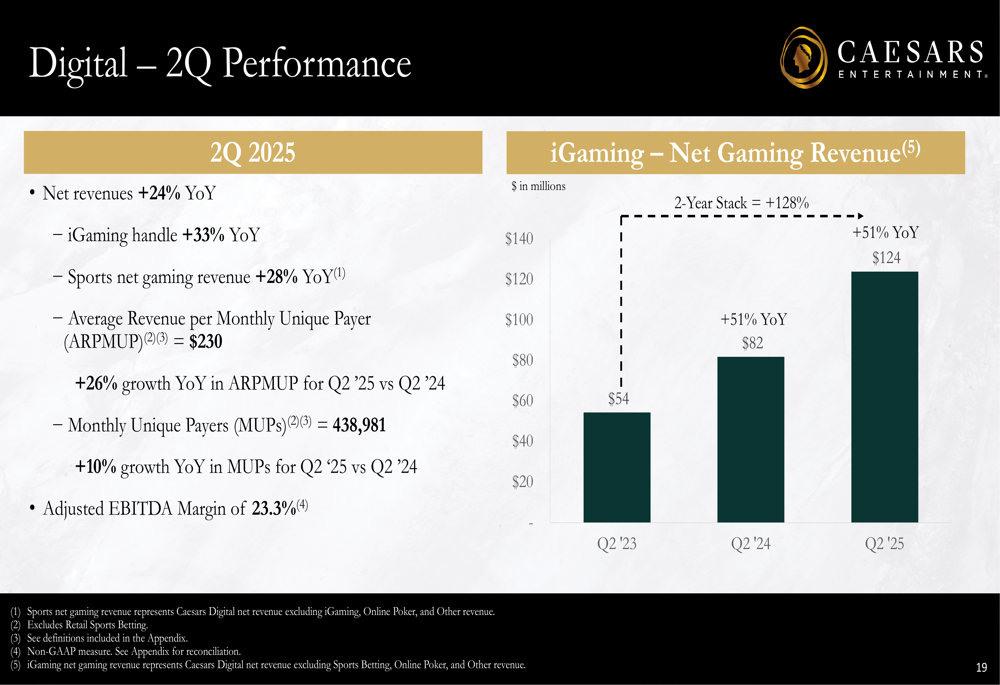

Key performance indicators for the digital segment showed robust improvement, with Average Revenue per Monthly Unique Payer (ARPMUP) reaching $230, a 26% increase year-over-year. Monthly Unique Payers grew 10% compared to Q2 2024, reaching nearly 439,000 users. The segment achieved an Adjusted EBITDA margin of 23.3%.

The company’s iGaming revenue has shown particularly strong momentum, as illustrated in this chart:

CEO Tom Reeg emphasized the digital segment’s performance during the earnings call, describing it as "fantastic" and noting its "extraordinary" momentum. The company expects its digital segment to generate over $500 million in EBITDA by 2026.

Regional and Las Vegas Performance

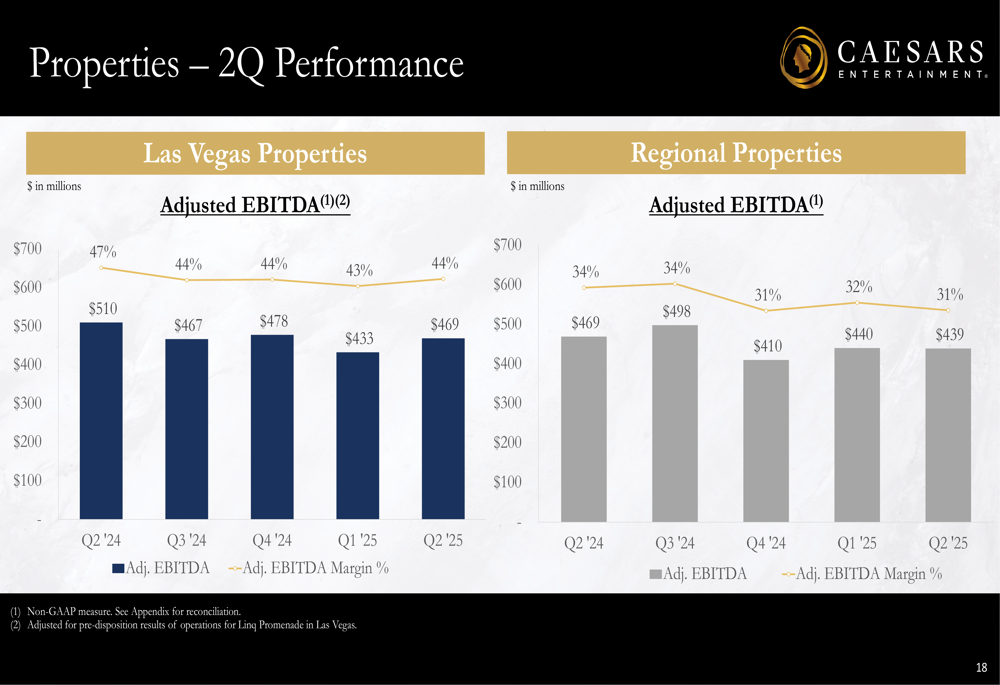

While the digital segment thrived, Caesars’ traditional brick-and-mortar operations showed mixed results. The Las Vegas segment experienced softness, with Adjusted EBITDA declining to $469 million in Q2 2025 from $510 million in Q2 2024.

The following chart shows the quarterly performance of Las Vegas and Regional properties:

The company’s Las Vegas Center Strip portfolio, which includes eight major casino resorts, has generated over $1 billion in trailing twelve-month Adjusted EBITDA. Caesars recently divested the Linq Promenade for $275 million at a 14x EBITDA multiple, demonstrating its strategic approach to portfolio management.

Regional properties delivered $439 million in Adjusted EBITDA for Q2 2025, slightly down from $469 million in the prior year. The company highlighted that it has completed a major investment cycle in its regional properties, having deployed approximately $2.9 billion since July 2020.

Strategic Initiatives

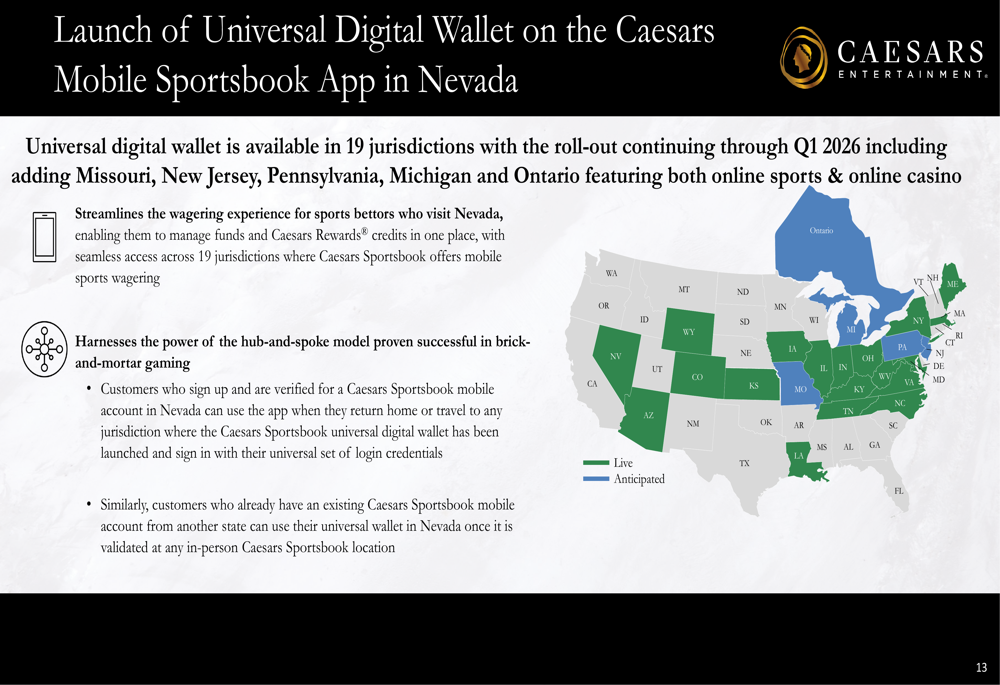

A key strategic focus for Caesars is the integration of its digital and physical gaming experiences through the Caesars Rewards loyalty program. The company recently launched its Universal Digital Wallet on the Caesars Mobile Sportsbook App in Nevada, with plans to expand to 19 jurisdictions by Q1 2026.

As shown in the following map, the Universal Digital Wallet will connect customers across multiple states:

This initiative aims to streamline the wagering experience for sports bettors who visit Nevada, enabling them to manage funds and Caesars Rewards credits in one place, with seamless access across jurisdictions where Caesars Sportsbook offers mobile sports wagering.

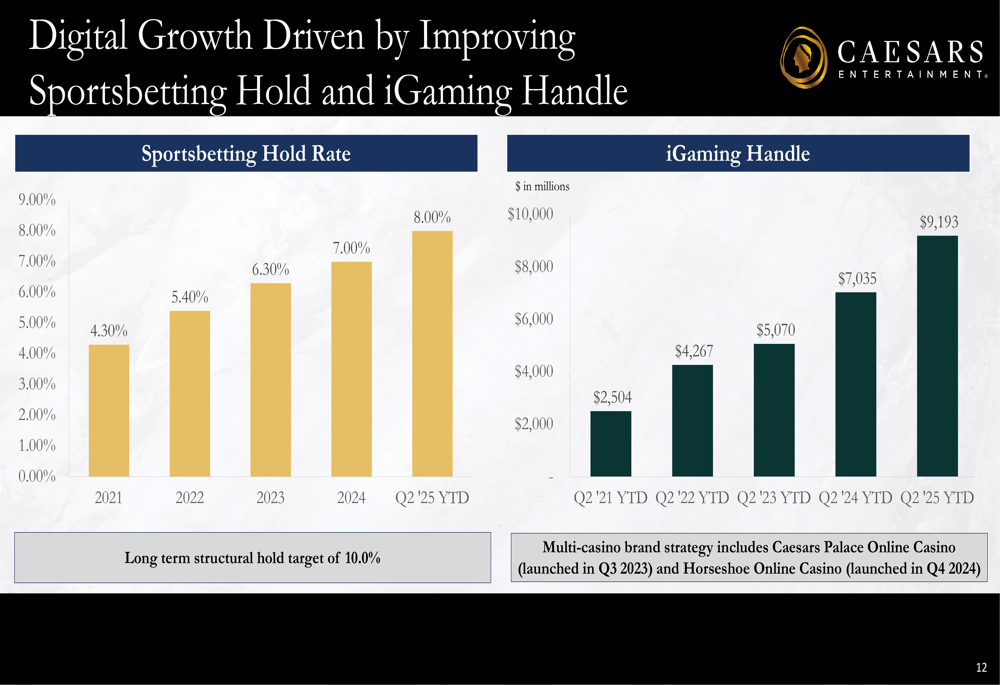

The company has also identified key drivers behind its digital growth, including improvements in sportsbetting hold rate and significant increases in iGaming handle:

The sportsbetting hold rate has improved from 4.30% in 2021 to 8.00% in Q2 2025 YTD, with a long-term structural hold target of 10.0%. Meanwhile, iGaming handle has grown from $2.5 billion in Q2 2021 YTD to $9.2 billion in Q2 2025 YTD.

Forward-Looking Statements

Caesars provided its financial outlook for 2025, projecting Master Lease Rent of $1.35 billion, Interest Expense of $775 million, and Capital Expenditures of $650 million (excluding the Caesars Virginia joint venture). The company expects cash income taxes to be approximately 3-4% of Adjusted EBITDA.

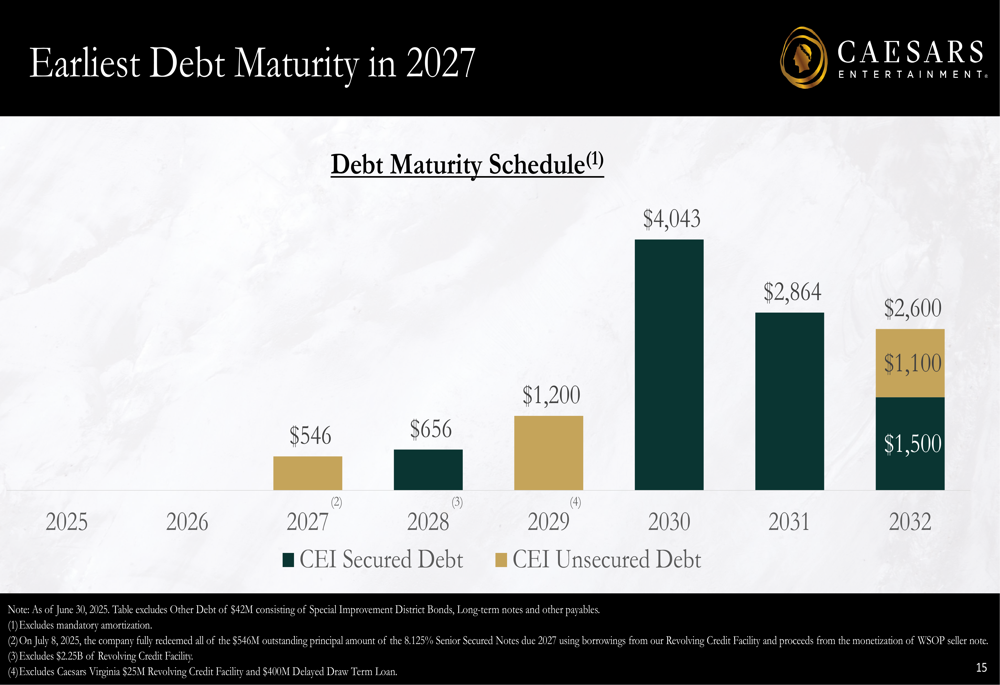

Management emphasized that growing free cash flow will enable debt repayment and/or share repurchases. The company’s debt maturity schedule shows significant maturities in 2030 and 2031:

Looking ahead, Caesars anticipates strong group bookings in Q4 2025 and into 2026. The company is also considering a potential separation of its digital business in 2026, though executives noted that international expansion is unlikely in the near term.

Analysts remain generally bullish on Caesars despite recent stock price weakness, with price targets ranging from $27 to $61, suggesting significant potential upside from current levels. The company’s focus on marketing efficiency and profitable customer acquisition, particularly in the digital segment, will be crucial for future performance as it navigates ongoing challenges in the Las Vegas leisure market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.