Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Calian Technologies Ltd (TSX:CGY) reported mixed third-quarter results for the period ending June 30, 2025, with continued challenges in its Information Technology and Cyber Solutions (ITCS) segment offset by strong performance in its Defence business. The company’s stock has shown resilience, trading at $50.68 as of August 12, 2025, up 0.34% and well above its 52-week low of $37.70, suggesting investor confidence in the company’s long-term strategy despite recent challenges.

The Q3 results come after a difficult second quarter when Calian’s stock dropped 17.27% following disappointing earnings and the withdrawal of full-year guidance. The latest presentation indicates some stabilization, with consolidated growth of 4% and a substantial increase in backlog providing improved revenue visibility.

Quarterly Performance Highlights

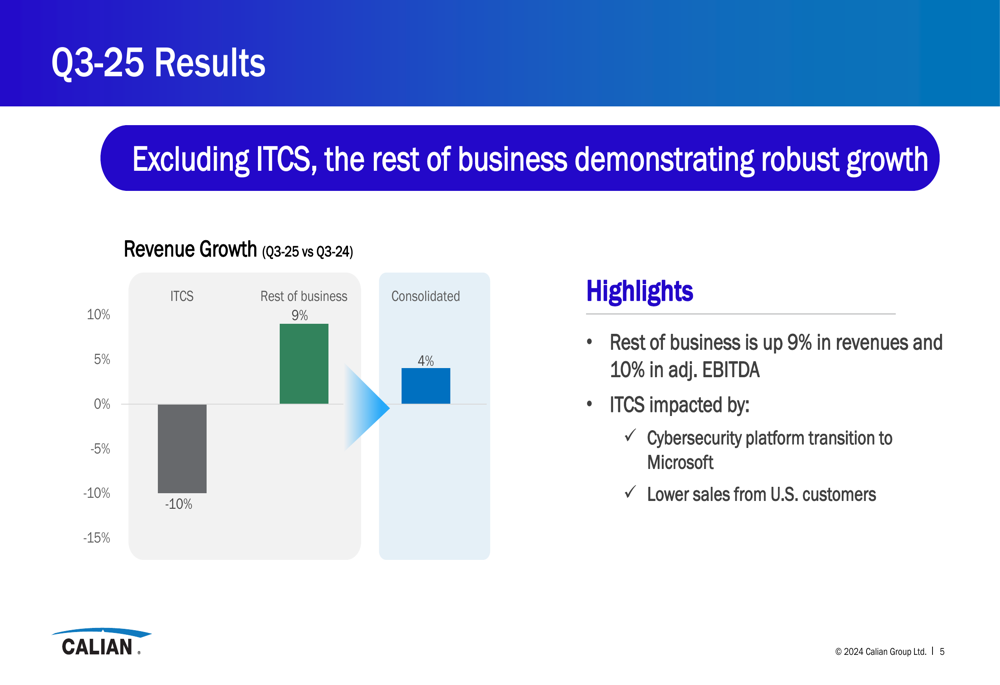

Calian’s Q3-25 results showed consolidated growth of 4% compared to Q3-24, with a clear divergence between segments. While the ITCS segment continued to face headwinds with a 10% decline, the rest of the business demonstrated robust growth of 9%.

As shown in the following revenue growth breakdown:

The company noted that ITCS performance was impacted by the ongoing cybersecurity platform transition to Microsoft and lower sales from U.S. customers. This represents an improvement from the 25% ITCS decline reported in Q2-25, suggesting the segment’s challenges may be gradually stabilizing.

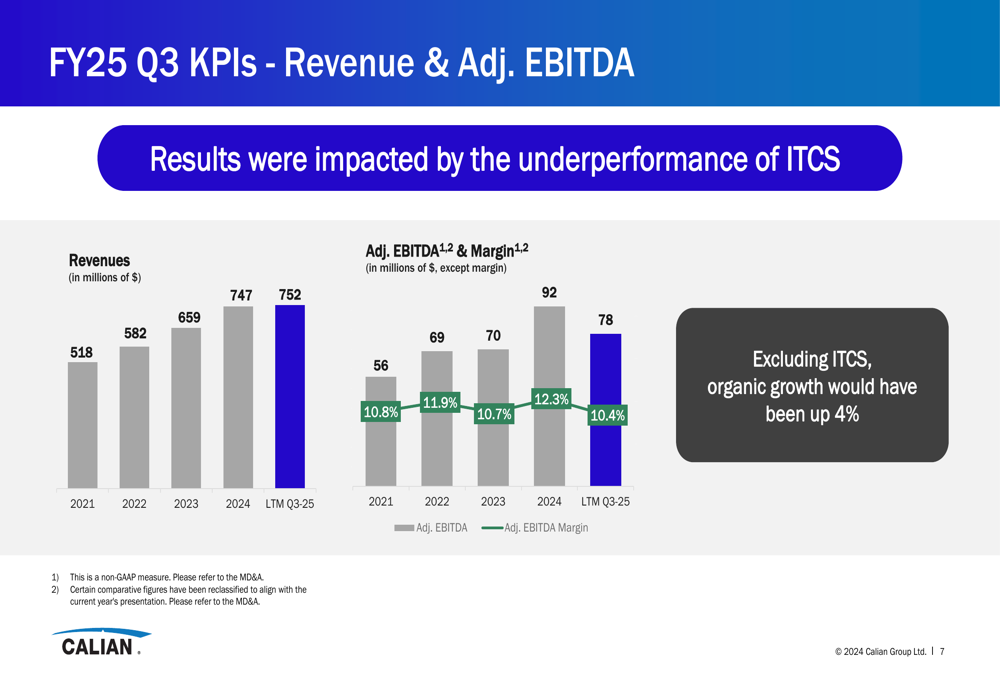

For the trailing twelve months ended June 30, 2025, Calian reported revenue of $752 million, slightly higher than the $747 million reported for fiscal year 2024. However, adjusted EBITDA declined to $78 million (10.4% margin) from $92 million (12.3% margin) in 2024.

The company’s operating free cash flow conversion also decreased to 69% for the LTM Q3-25 period, compared to 78% in fiscal 2024, reflecting the impact of lower profitability on cash generation.

Defence & Space Growth

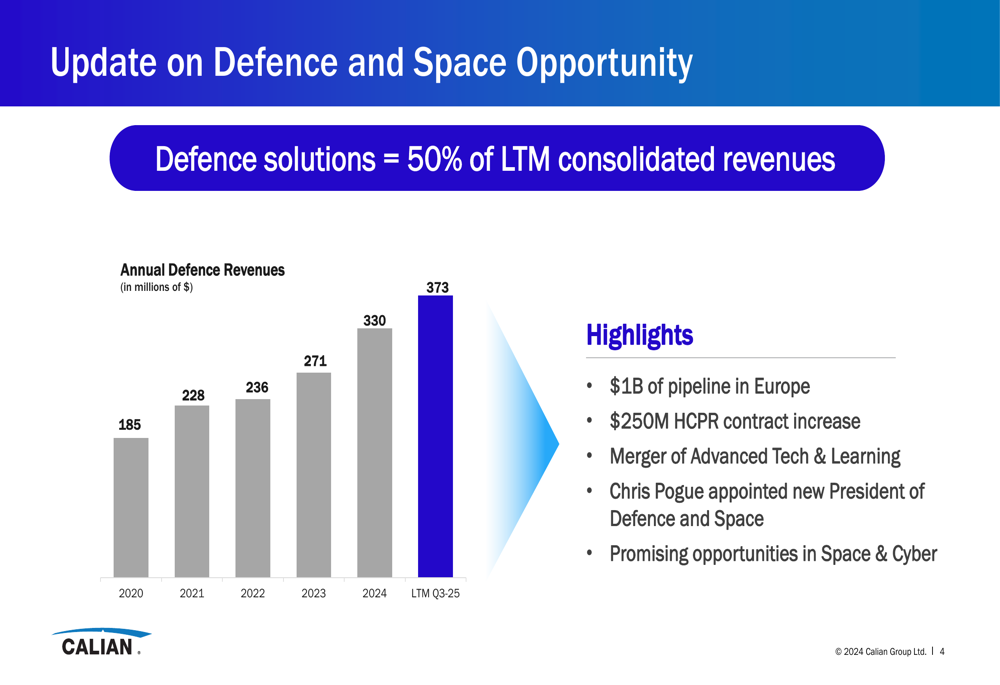

The standout performer in Calian’s portfolio continues to be its Defence and Space segment, which now represents 50% of the company’s trailing twelve-month consolidated revenues. The segment has shown impressive growth trajectory over the past several years, with revenues increasing from $185 million in 2020 to $373 million in the LTM Q3-25 period.

The following chart illustrates this consistent growth pattern:

Management highlighted several positive developments in the Defence and Space segment, including a $1 billion pipeline in Europe, a $250 million HCPR contract increase, and the appointment of Chris Pogue as the new President of Defence and Space. The company also noted promising opportunities in Space & Cyber subsectors.

This strategic focus on Defence appears well-timed given global geopolitical tensions and increased defense spending across NATO countries, providing Calian with a strong growth vector despite challenges in other segments.

Backlog and Financial Position

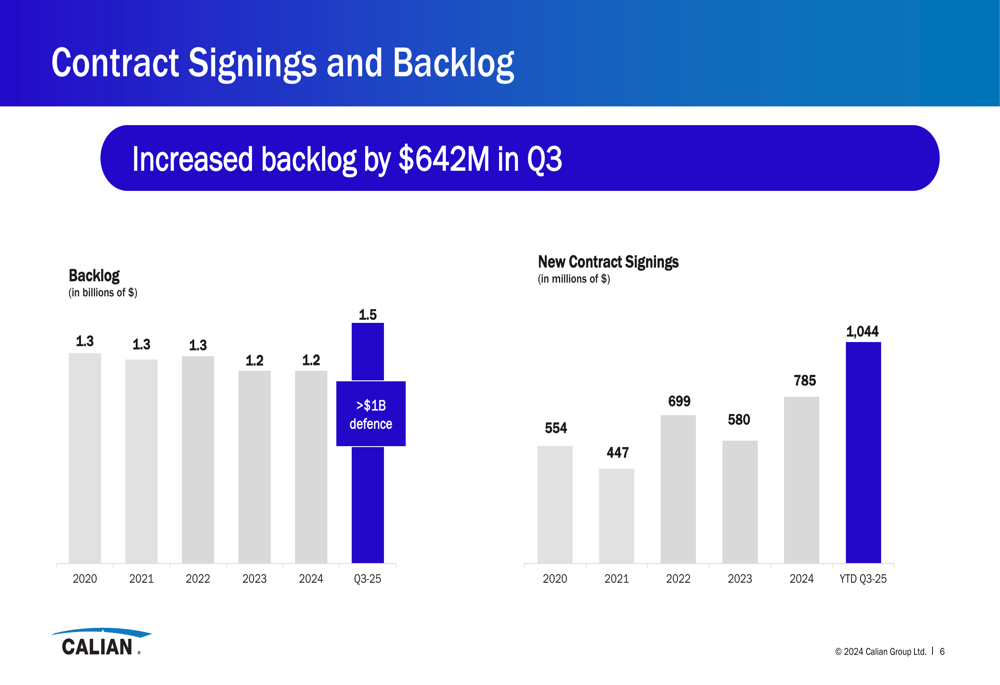

One of the most significant positive developments in Q3-25 was the substantial increase in Calian’s backlog, which grew by $642 million during the quarter to reach $1.5 billion. This represents a meaningful increase from the $1.2 billion reported at the end of fiscal 2024 and provides enhanced revenue visibility for future periods.

The following chart shows the company’s backlog and new contract signings trends:

New contract signings for the first nine months of fiscal 2025 reached $1,044 million, already surpassing the $785 million recorded for the entire 2024 fiscal year. This strong booking performance suggests potential for accelerated growth in future quarters as these contracts convert to revenue.

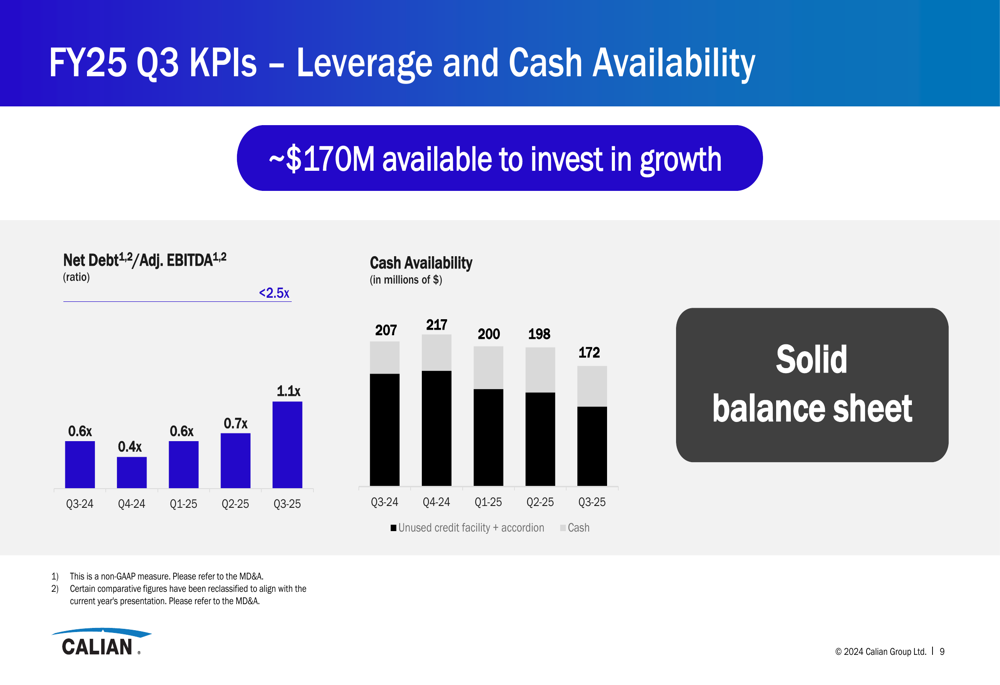

From a balance sheet perspective, Calian maintains a solid financial position with $172 million in cash availability as of Q3-25, though this represents a decrease from $217 million at the end of fiscal 2024. The company’s leverage ratio (Net Debt/Adj. EBITDA) increased to 1.1x in Q3-25 from 0.4x in Q4-24 but remains well below the company’s target of less than 2.5x.

Strategic Outlook

Looking ahead, Calian’s management expressed optimism about future prospects while acknowledging current challenges. The company outlined four key priorities: capitalizing on the Defence & Space portfolio, revitalizing the ITCS segment toward growth, expediting portfolio review, and using its strong balance sheet to pursue acquisitions.

Management reiterated its objective to grow double-digits through a combination of organic growth and acquisitions. The company also plans to repurchase up to 6% of its shares in fiscal 2025, reflecting confidence in its long-term value proposition.

CEO Kevin Ford had previously acknowledged in the Q2 earnings call that results fell short of expectations but emphasized that challenges were "essentially isolated to headwinds in the ITCS segment." The Q3 presentation suggests this assessment remains accurate, with the rest of the business showing healthy growth.

With a solid backlog, strong Defence segment performance, and available capital for strategic acquisitions, Calian appears positioned to weather its current challenges while building for future growth. Investors will be watching closely to see if the company can successfully revitalize its ITCS segment while continuing to capitalize on its Defence & Space opportunities in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.