CME glitch; U.S. dollar on pace for weekly fall; Tokyo CPI - what’s moving markets

California Water Service Group (NYSE:CWT) reported mixed results for the third quarter of 2025, with revenue growth of 3.9% year-over-year but falling short of analyst expectations. The company's stock declined 4.99% following the October 30 earnings release, closing at $47.45.

Quarterly Performance Highlights

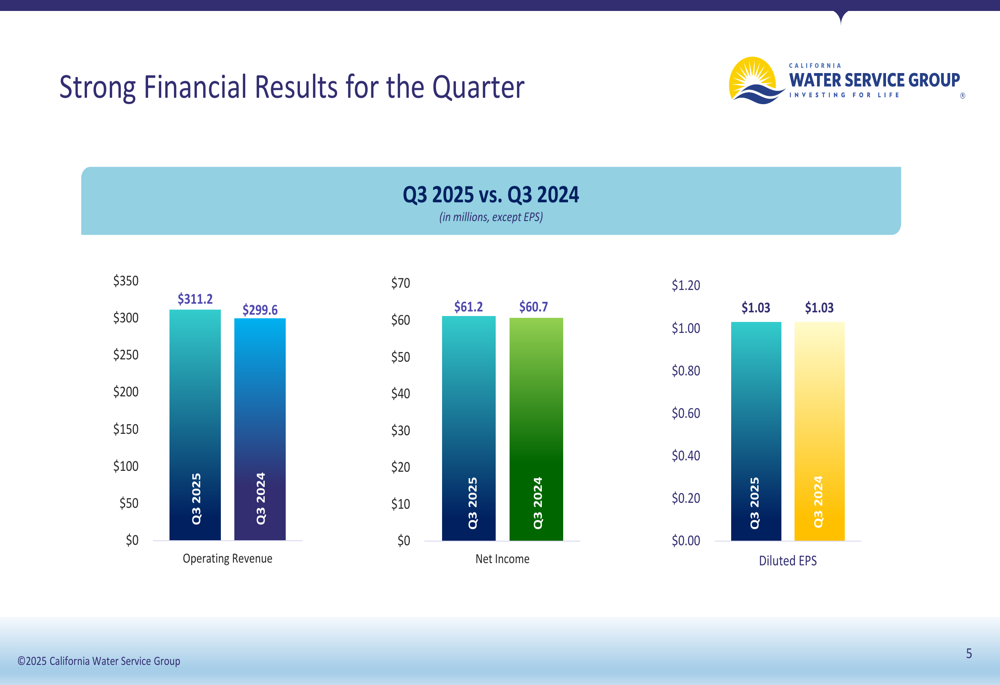

California Water Service reported Q3 2025 operating revenue of $311.2 million, up from $299.6 million in Q3 2024. Net income slightly increased to $61.2 million from $60.7 million, while diluted earnings per share remained flat at $1.03. Despite the revenue growth, these results missed analyst expectations of $1.17 EPS and $321.35 million in revenue.

As shown in the following chart comparing quarterly financial results:

The company's EPS performance was influenced by several offsetting factors. Rate increases and regulatory account changes contributed positively ($0.23 per share), along with income tax rate changes ($0.07). However, these gains were offset by decreased consumption and unbilled revenue changes (-$0.08), water production rate increases (-$0.11), higher depreciation (-$0.04), increased interest expenses (-$0.05), and other items (-$0.02).

This bridge analysis illustrates the factors affecting EPS performance:

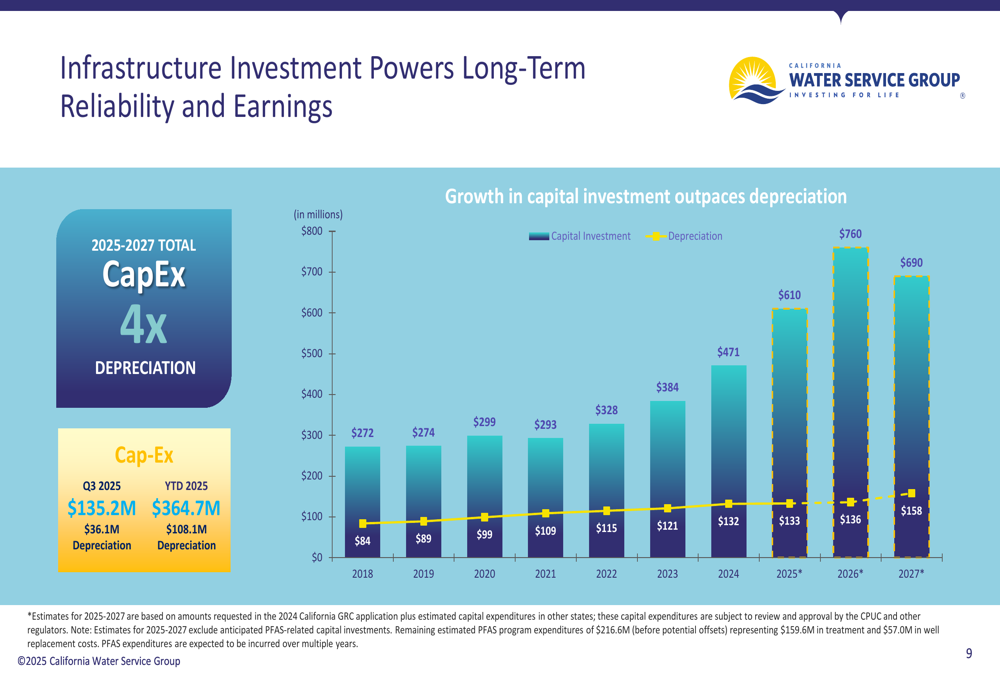

Strategic Infrastructure Investments

California Water Service continues to emphasize its long-term infrastructure investment strategy as a key driver of future growth. The company invested $135.2 million in Q3 2025 and $364.7 million year-to-date in water system infrastructure.

The company's capital expenditure forecast shows investments at approximately four times the depreciation rate, highlighting its commitment to infrastructure renewal and expansion:

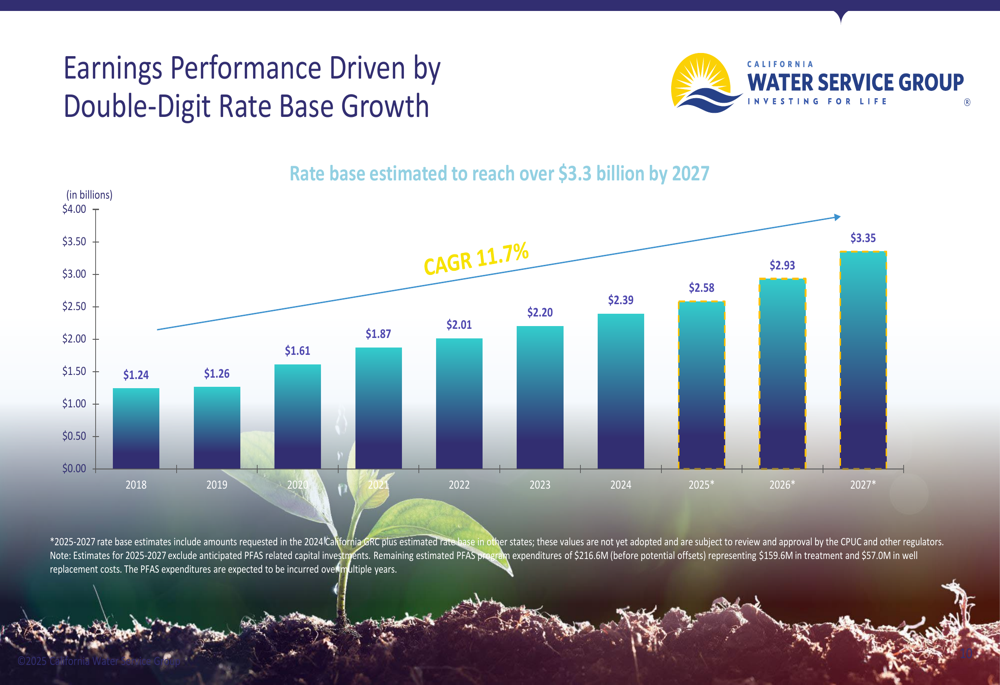

These investments are expected to drive significant rate base growth, with projections showing an 11.7% compound annual growth rate (CAGR) that would increase the rate base from $2.58 billion in 2025 to over $3.3 billion by 2027:

Financial Position and Dividend Strategy

The company maintains a strong liquidity profile to support its growth strategy, with $255 million in unrestricted cash, $45.6 million in restricted cash, and $76 million in available credit. CWT issued Notes and Bonds with an aggregate principal amount of $370 million on October 1, 2025, and maintains an A+/stable credit rating from S&P Global.

The following chart illustrates the company's liquidity position:

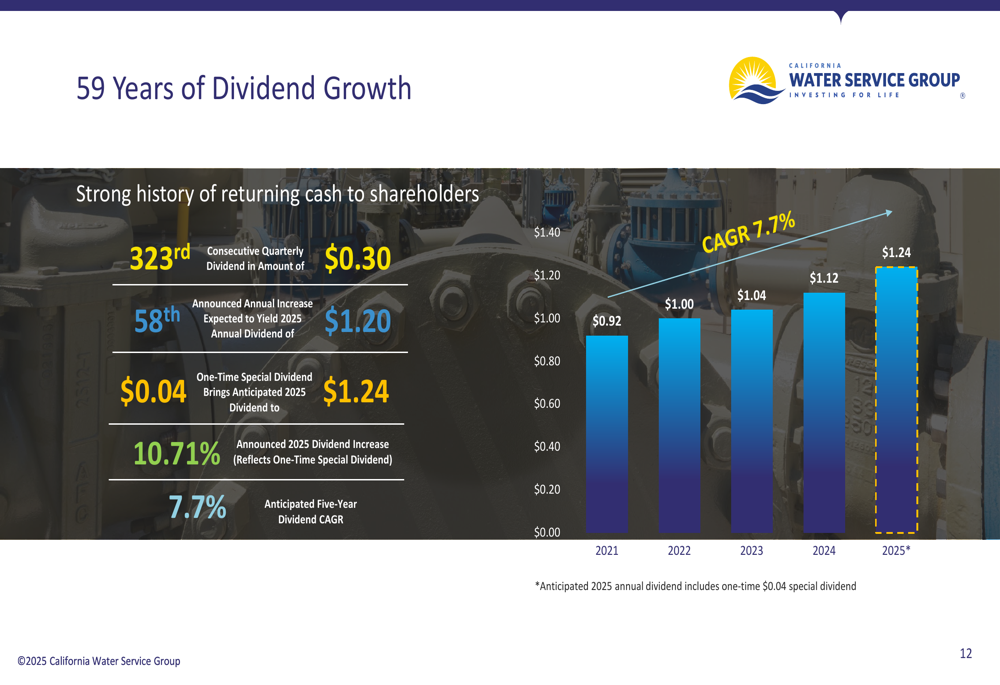

California Water Service continues its impressive dividend history, celebrating its 323rd consecutive quarterly dividend ($0.30). The company announced its 58th annual increase with an expected annual dividend of $1.20 in 2025, plus a one-time special dividend of $0.04, bringing the anticipated 2025 dividend to $1.24 – a 10.71% increase from the previous year.

As shown in the dividend growth chart:

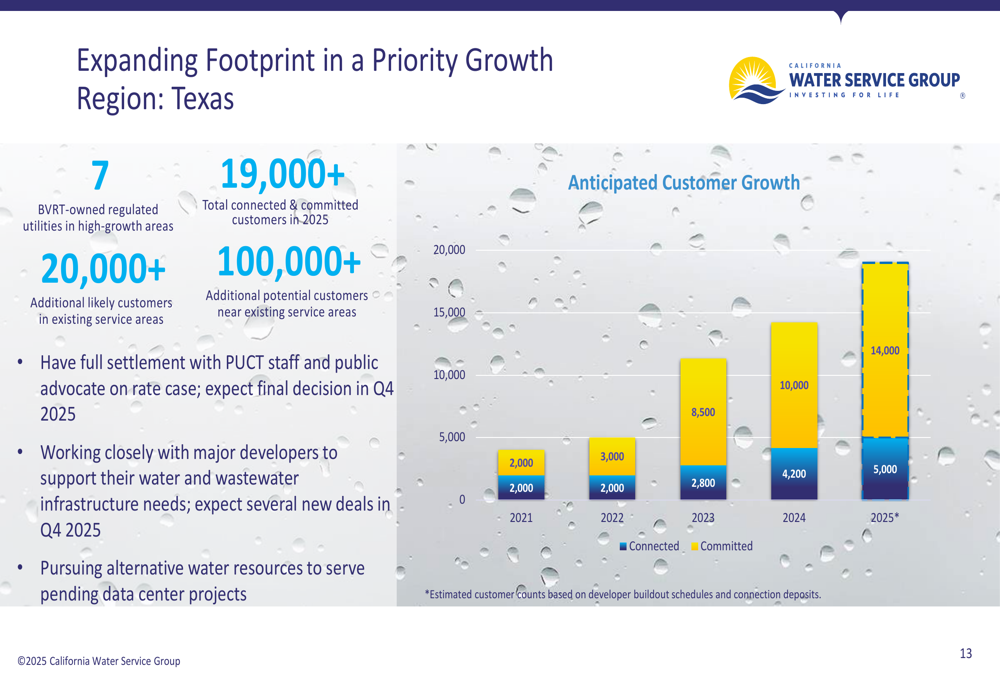

Regional Expansion and Regulatory Developments

California Water Service is expanding its footprint in Texas, which it identifies as a priority growth region. The company now has seven BVRT-owned regulated utilities in high-growth areas with over 19,000 total connected and committed customers in 2025, with potential for significant additional growth.

The company's Texas expansion strategy is illustrated here:

On the regulatory front, CWT has filed a $1.6 billion investment proposal for California from 2025-2027 as part of its 2024 California General Rate Case. The company is requesting rate adjustments to generate revenue increases of $140.6 million (17.1%) in 2026, $72.4 million (7.7%) in 2027, and $83.6 million (8.1%) in 2028.

Additional regulatory developments include the Hawaii Public Utilities Commission approving a $4.7 million revenue increase for Hawaii Water's five Waikoloa systems, effective October 9, 2025, and Washington Water filing a rate case with the Washington Utilities and Transportation Commission for a $4.9 million revenue increase.

PFAS Strategy and Settlements

The company continues to address per- and polyfluoroalkyl substances (PFAS) challenges through investments and legal settlements. CWT received $24.2 million net in PFAS settlement payments in Q3, bringing the year-to-date total to $34.8 million net.

While the company remains committed to PFAS treatment investments across California, Washington, and New Mexico, it noted that some well replacements will shift a portion of planned $226 million in PFAS investments from 2025-2027 to later years:

Despite the earnings miss in Q3 2025, California Water Service Group continues to emphasize its long-term strategy of infrastructure investment, regional expansion, and regulatory engagement to drive future growth and shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.