Stock market today: S&P 500 hits fresh record close on stronger economic growth

Introduction & Market Context

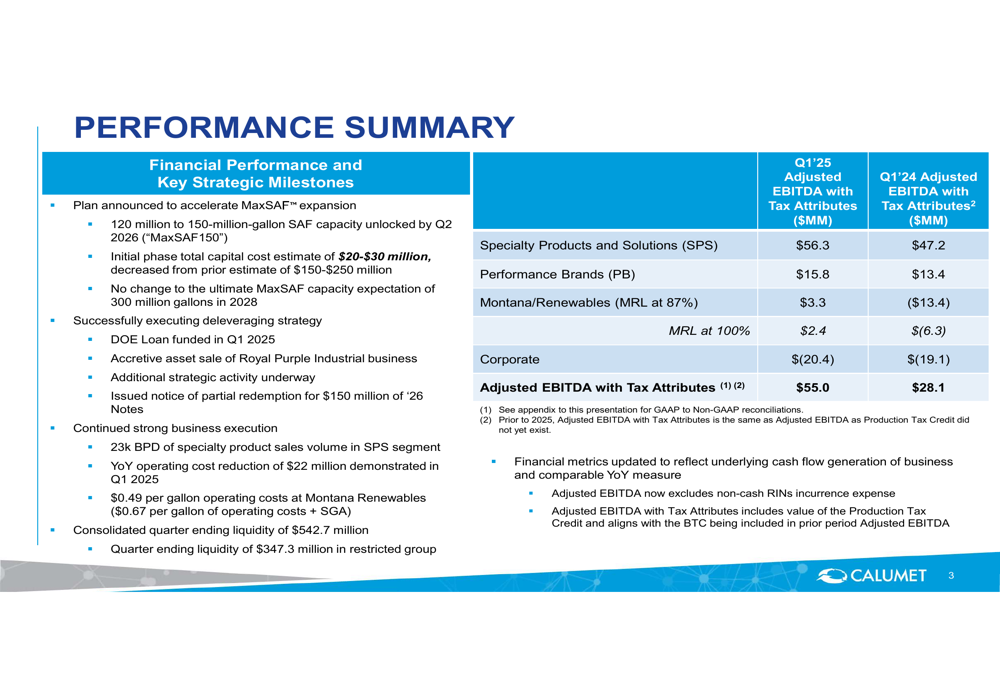

Calumet Inc. (NASDAQ:CLMT) presented its first quarter 2025 financial results on May 9, 2025, highlighting strategic shifts in its renewable fuels business and improved performance across segments. The specialty products and solutions provider reported consolidated Adjusted EBITDA with Tax Attributes of $55.0 million, showing resilience in its core business despite ongoing market challenges in the renewable fuels sector.

The presentation comes as Calumet’s stock closed at $11.87 on May 8, with premarket trading on May 9 showing a 5.05% decline to $11.27, suggesting investor caution about the company’s performance and strategic direction. This follows a challenging fourth quarter where the company missed earnings expectations with an EPS of -$0.47 against a forecast of -$0.21.

Quarterly Performance Highlights

Calumet reported improved year-over-year results across its business segments. The Specialty Products and Solutions (SPS) segment delivered Adjusted EBITDA of $56.3 million, up from $47.2 million in Q1 2024, demonstrating the resilience of the company’s core business. The Performance Brands segment showed an 18% year-over-year improvement with Adjusted EBITDA of $15.8 million compared to $13.4 million in the prior year.

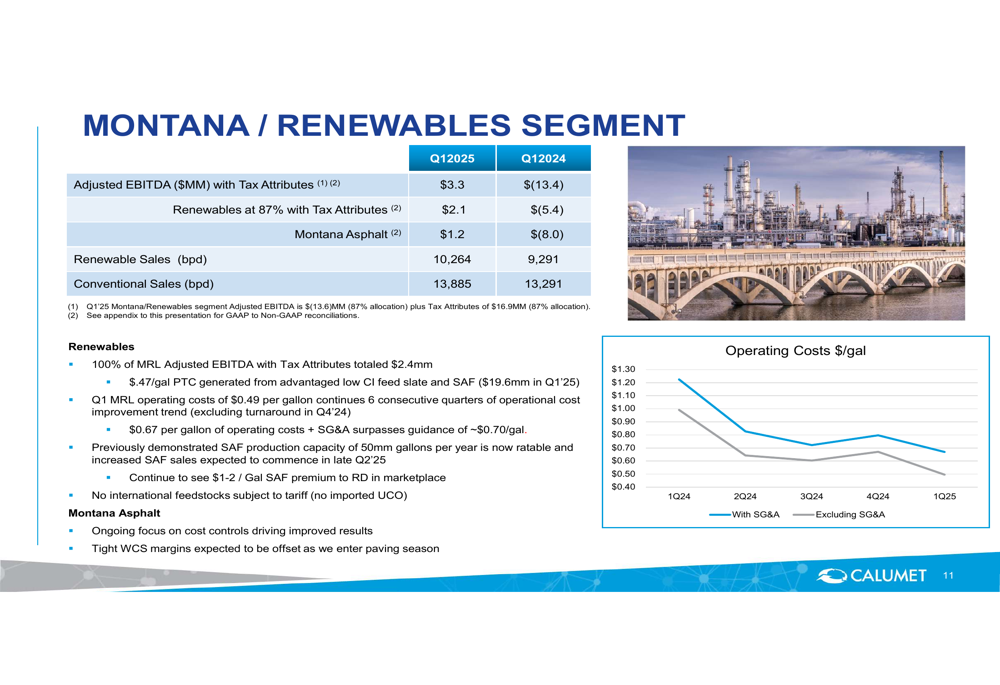

As shown in the following performance summary slide, the Montana/Renewables segment showed significant improvement, posting Adjusted EBITDA with Tax Attributes of $3.3 million compared to a loss of $13.4 million in Q1 2024:

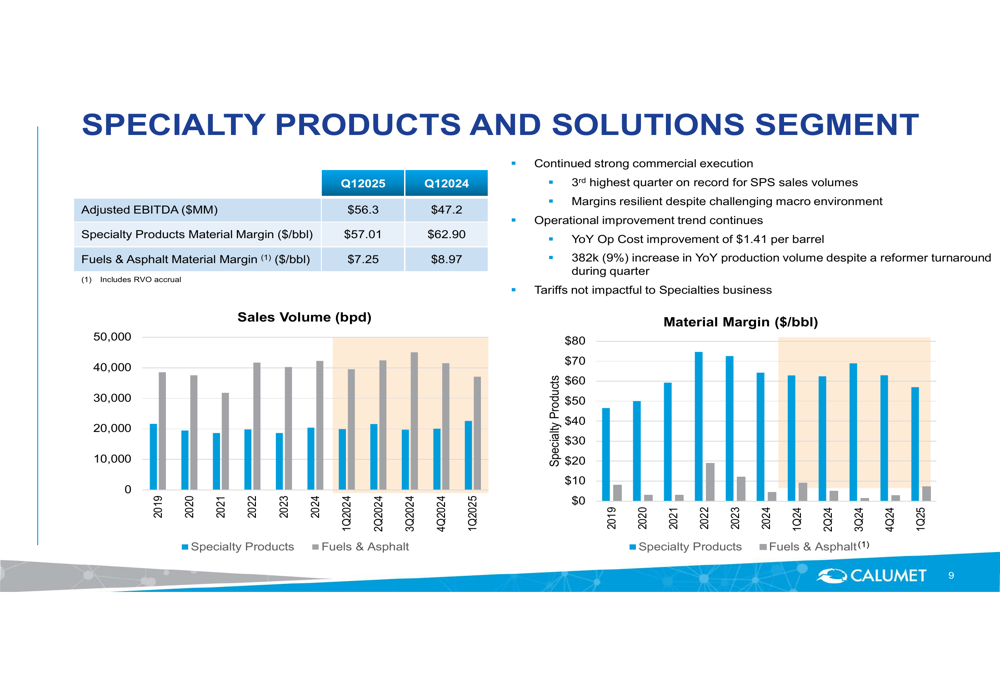

The company’s specialty products business continues to be a stable performer with 23,000 barrels per day of sales volume in the quarter. While specialty products material margin decreased to $57.01 per barrel from $62.90 in the prior year, the company emphasized that operational improvements contributed $1.41 per barrel year-over-year, helping to offset some of the margin pressure.

The following slide illustrates the consistent performance of the Specialty Products and Solutions segment over time:

Strategic Initiatives

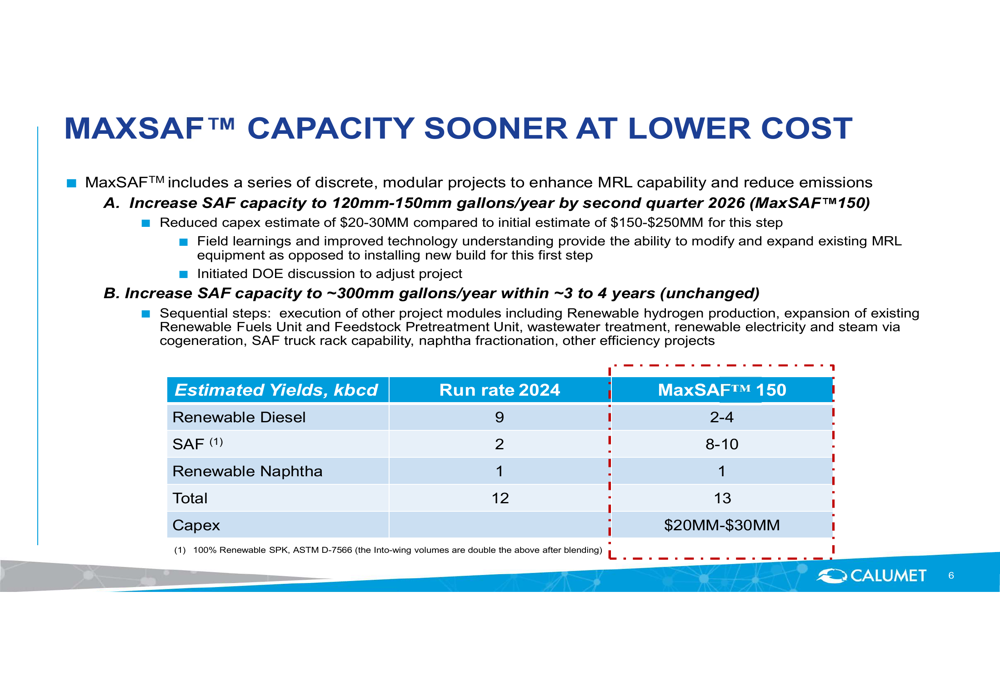

The most significant strategic announcement was Calumet’s decision to accelerate its MaxSAF™ expansion, aiming to unlock 120-150 million gallons of Sustainable Aviation Fuel (SAF) capacity by Q2 2026. Notably, the company has reduced its capital cost estimate for this expansion to $20-$30 million, while maintaining its ultimate goal of 300 million gallons of capacity by 2028.

This strategic pivot is detailed in the following slide, which outlines the revised capacity and cost projections:

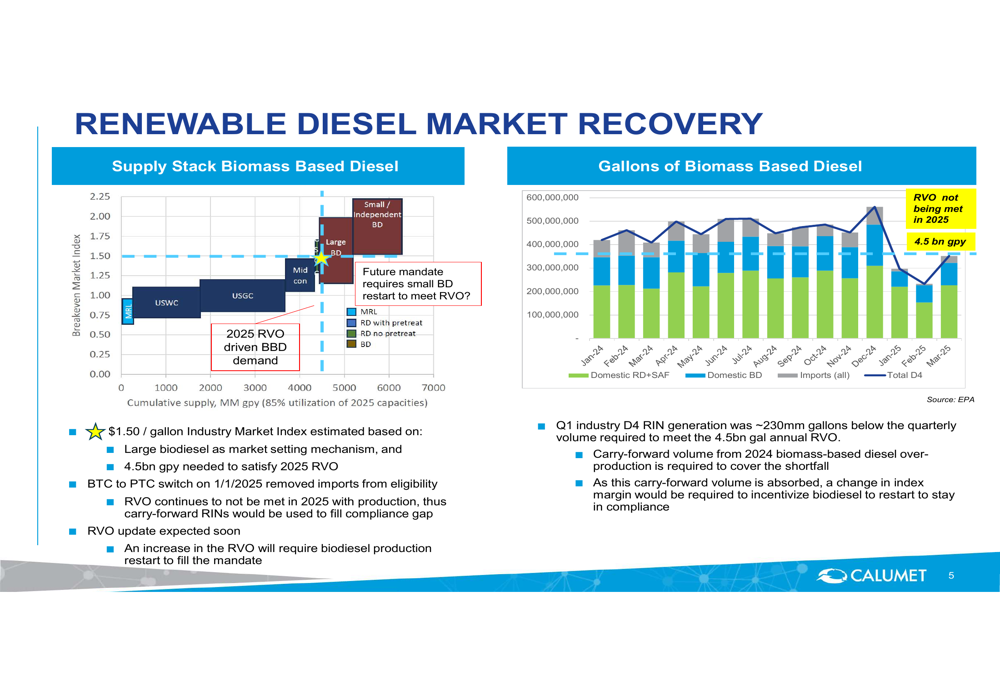

The accelerated SAF strategy comes amid signs of recovery in the renewable diesel market. Calumet noted that the Renewable Volume Obligation (RVO) is not being met in 2025, with 4.5 billion gallons per year needed to satisfy the 2025 RVO. This market dynamic is creating opportunities for producers like Calumet, as illustrated in the market analysis slide:

The company also highlighted its competitive advantage through dynamic optimization, noting that approximately 60% of Montana Renewables’ shipments were recently shifted to Washington and Oregon markets, demonstrating the flexibility of its operations to respond to market conditions.

Detailed Financial Analysis

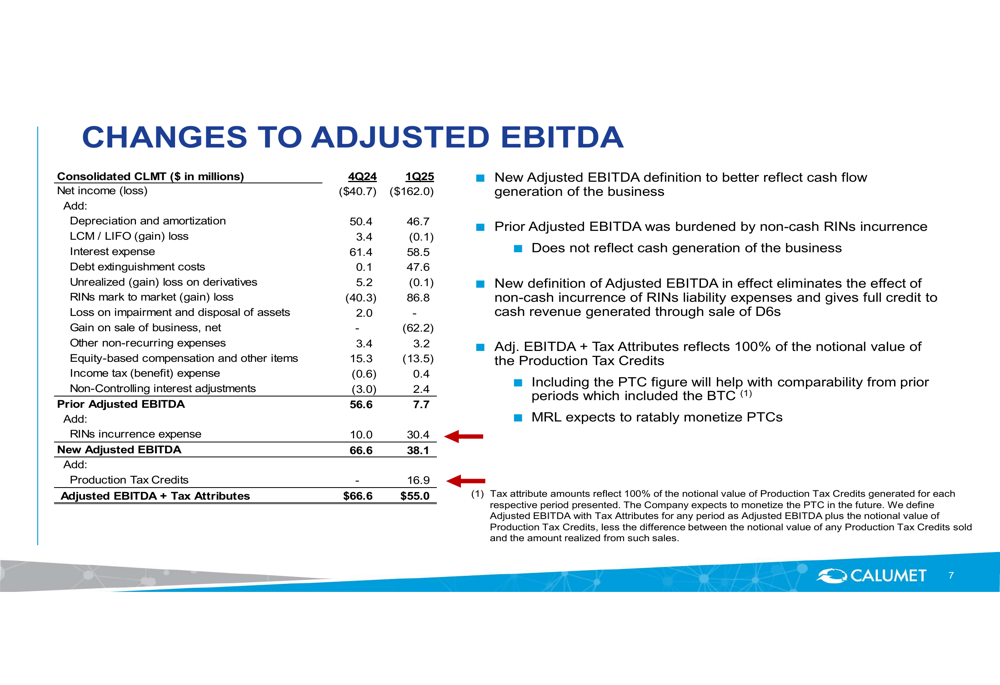

Calumet has implemented changes to its financial reporting, now including Tax Attributes with Adjusted EBITDA to better reflect the economic reality of its business. This change is particularly relevant for the Montana Renewables segment, which benefits from production tax credits.

The following slide details these changes to the company’s financial reporting methodology:

The Montana/Renewables segment showed marked improvement, with operating costs at $0.49 per gallon (including $0.67 SG&A). The company noted that its demonstrated SAF production capacity is now ratable, with increased SAF sales expected to commence in late Q2 2025. Management highlighted a potential $1-2 per gallon SAF premium to renewable diesel in the marketplace, which could significantly improve the segment’s profitability.

The segment’s performance metrics are illustrated in this slide:

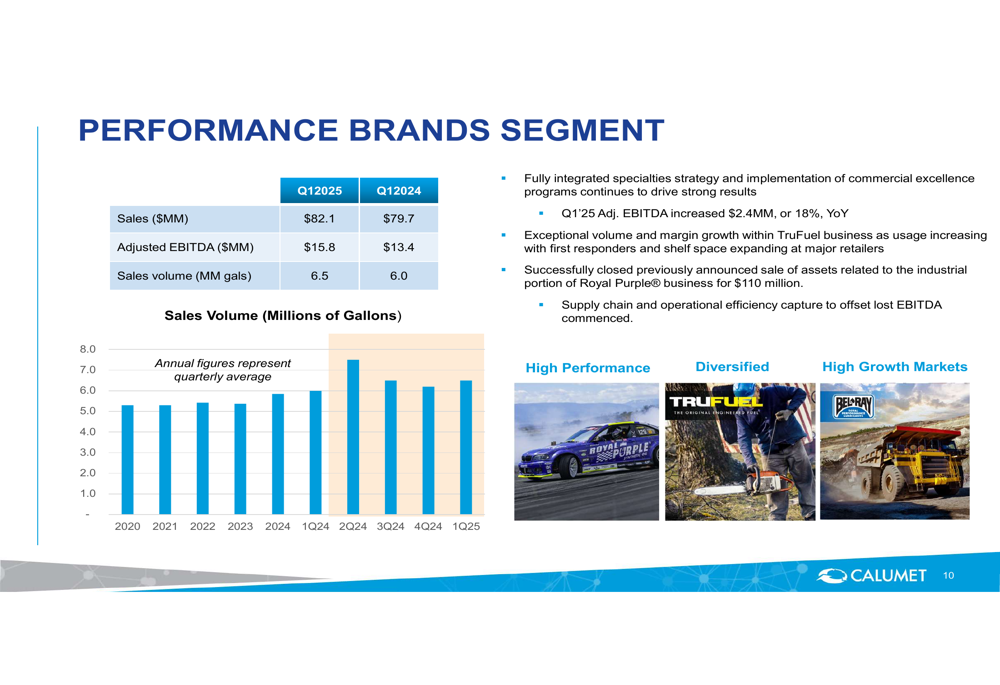

The Performance Brands segment also delivered strong results, with a focus on commercial excellence driving an 18% year-over-year increase in Adjusted EBITDA. The company successfully closed the sale of assets related to the industrial portion of the Royal Purple business, which aligns with its portfolio optimization strategy.

Forward-Looking Statements

Calumet emphasized its focus on deleveraging and value creation, highlighting several achievements including the successful funding of a Department of Energy loan, execution of the Royal Purple business sale, and partial redemption of $150 million of 2026 Notes. These efforts aim to strengthen the company’s balance sheet while positioning Montana Renewables for potential monetization.

The company’s deleveraging strategy is summarized in the following slide:

Looking ahead, Calumet appears to be positioning itself to capitalize on the evolving renewable fuels market, particularly in sustainable aviation fuel, while maintaining the strength of its specialty products business. The accelerated MaxSAF expansion represents a strategic pivot that could potentially deliver returns with significantly lower capital investment than previously anticipated.

However, investors should note that the company continues to face challenges, including a substantial debt burden and the need to demonstrate consistent profitability in its renewables segment. The premarket stock decline suggests that the market may be taking a cautious approach to the company’s strategic initiatives and financial performance, despite the positive framing in the presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.