Can anything shut down the Gold rally?

Introduction & Market Context

Campbell Soup Company (NYSE:CPB) released its third-quarter fiscal 2025 earnings presentation on June 2, 2025, revealing a mixed performance across its business segments. The company’s stock closed at $34.04 on May 30, 2025, down significantly from the $37.86 level seen after its Q2 earnings report, reflecting ongoing market concerns despite some operational improvements in Q3.

The presentation highlighted Campbell’s ability to deliver solid overall results despite facing headwinds in its Snacks business, with CEO Mick Beekhuizen emphasizing that Q3 earnings performance exceeded expectations due to strength in the Meals & Beverages segment.

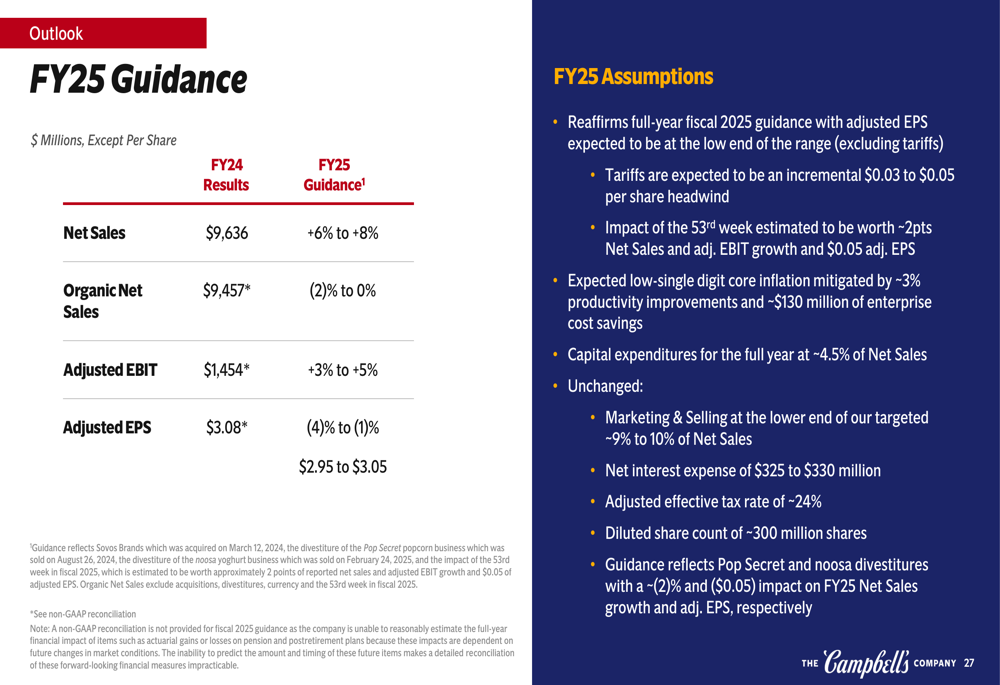

As shown in the following key messages slide, the company reaffirmed its fiscal 2025 guidance but cautioned that adjusted EPS is expected to be at the low end of the range due to incremental tariff impacts:

Quarterly Performance Highlights

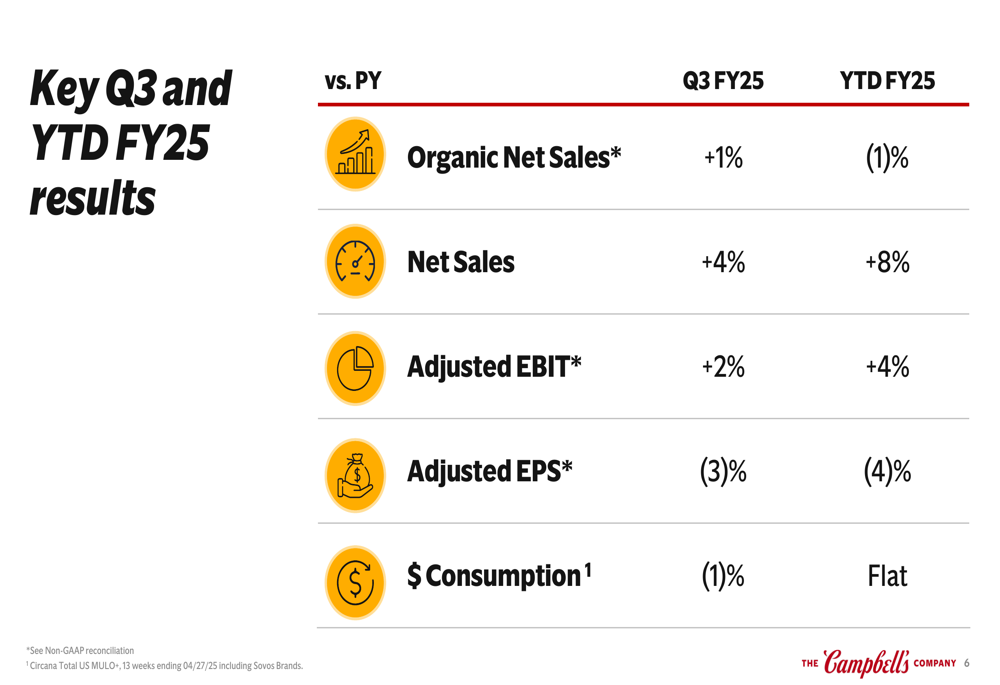

Campbell’s Q3 FY25 results showed improvement from the previous quarter, with organic net sales growing 1% compared to the 2% decline reported in Q2. Net sales increased 4% year-over-year to $2.475 billion, while adjusted EBIT rose 2% to $362 million. However, adjusted EPS declined 3% to $0.73, primarily due to higher interest expenses.

The following slide illustrates the key financial metrics for both Q3 and year-to-date performance:

The company’s performance continues to be a tale of two segments. The Meals & Beverages division showed remarkable strength with 6% organic net sales growth and 7% volume/mix growth in Q3, while the Snacks segment faced challenges with a 5% decline in both organic net sales and volume/mix.

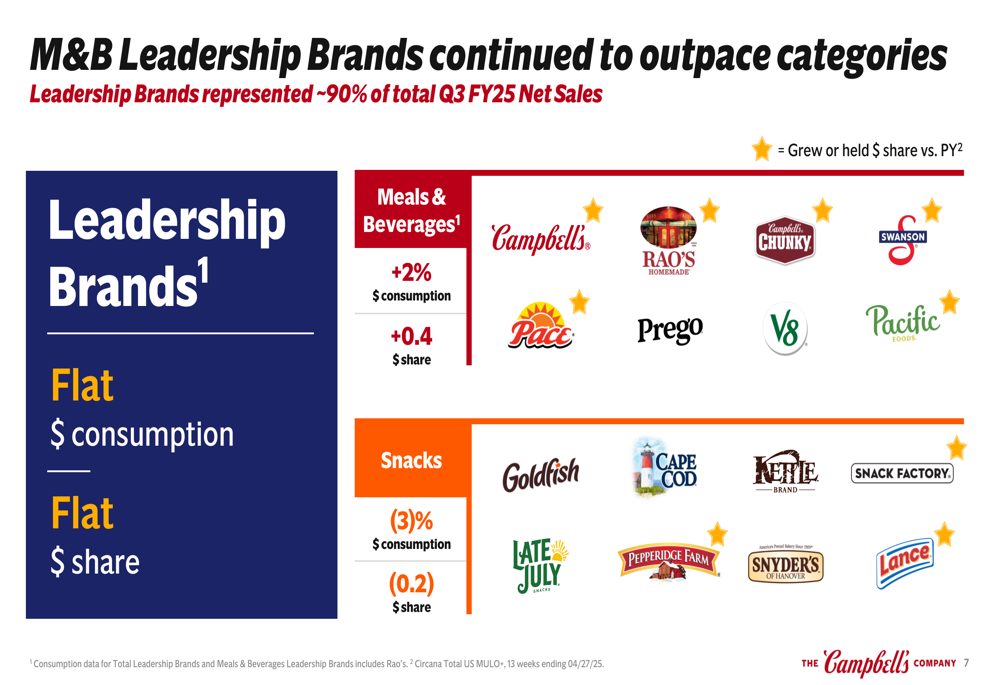

Campbell’s leadership brands, which represent approximately 90% of total Q3 FY25 net sales, showed stable overall share and consumption. Meals & Beverages brands grew dollar consumption by 2% and gained 0.4% in dollar share, while Snacks brands saw dollar consumption decline by 3% and lost 0.2% in dollar share.

Detailed Financial Analysis

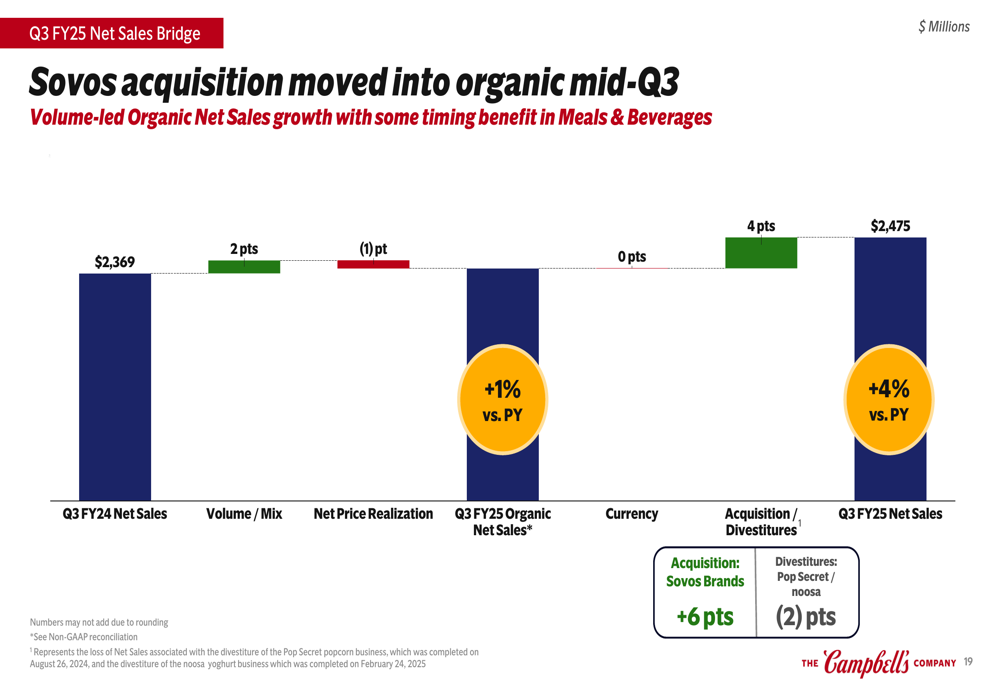

The company’s net sales bridge reveals that volume/mix contributed 2 percentage points to growth, while acquisition/divestitures added 4 percentage points, offset by a 1 percentage point decline from net price realization:

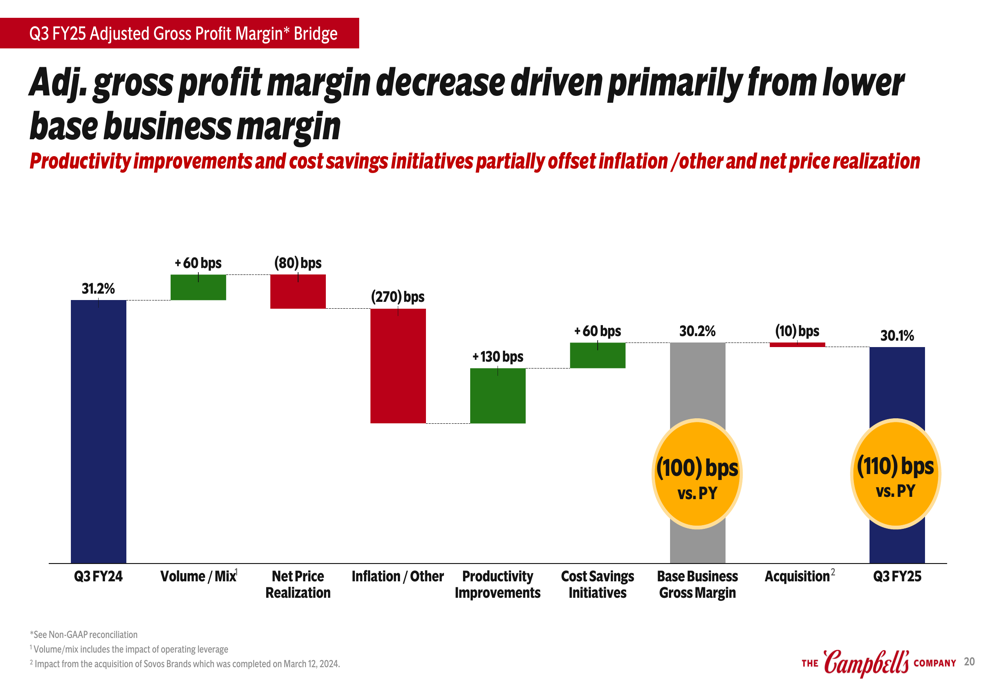

However, Campbell’s adjusted gross profit margin declined from 31.2% in Q3 FY24 to 30.1% in Q3 FY25. This 110 basis point decrease was primarily driven by inflation and other factors (-270 bps) and lower net price realization (-80 bps), partially offset by productivity improvements (+130 bps), volume/mix benefits (+60 bps), and cost savings initiatives (+60 bps):

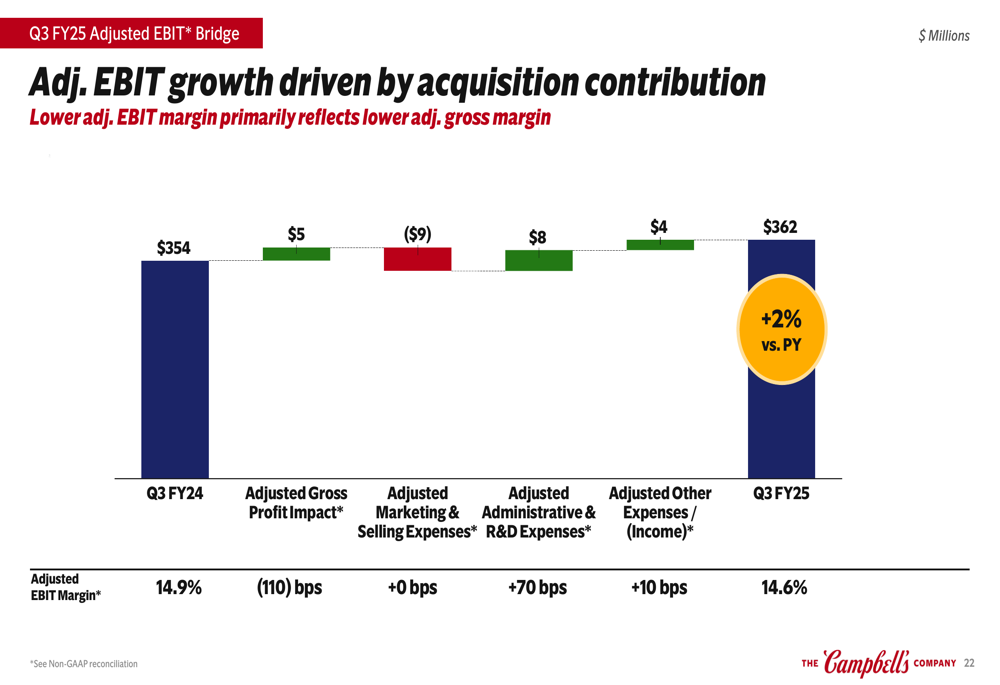

Despite the gross margin pressure, adjusted EBIT increased by $8 million or 2% year-over-year to $362 million, benefiting from higher adjusted gross profit, lower administrative and R&D expenses, and lower other expenses:

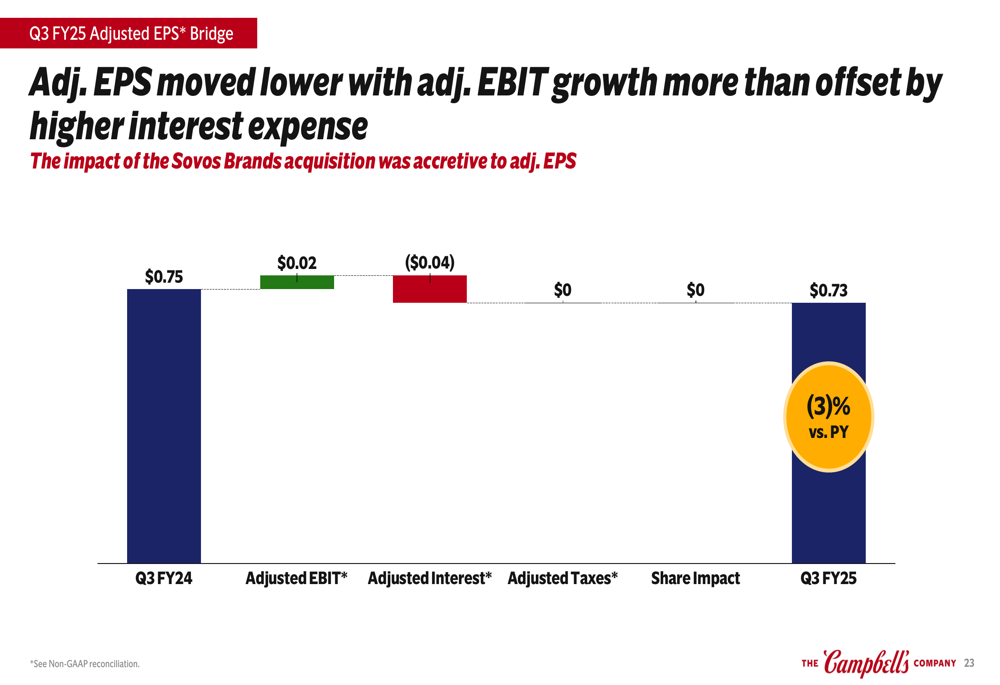

Adjusted EPS declined from $0.75 in Q3 FY24 to $0.73 in Q3 FY25, representing a 3% decrease. While adjusted EBIT contributed positively (+$0.02), this was more than offset by higher adjusted interest expenses (-$0.04):

Competitive Industry Position

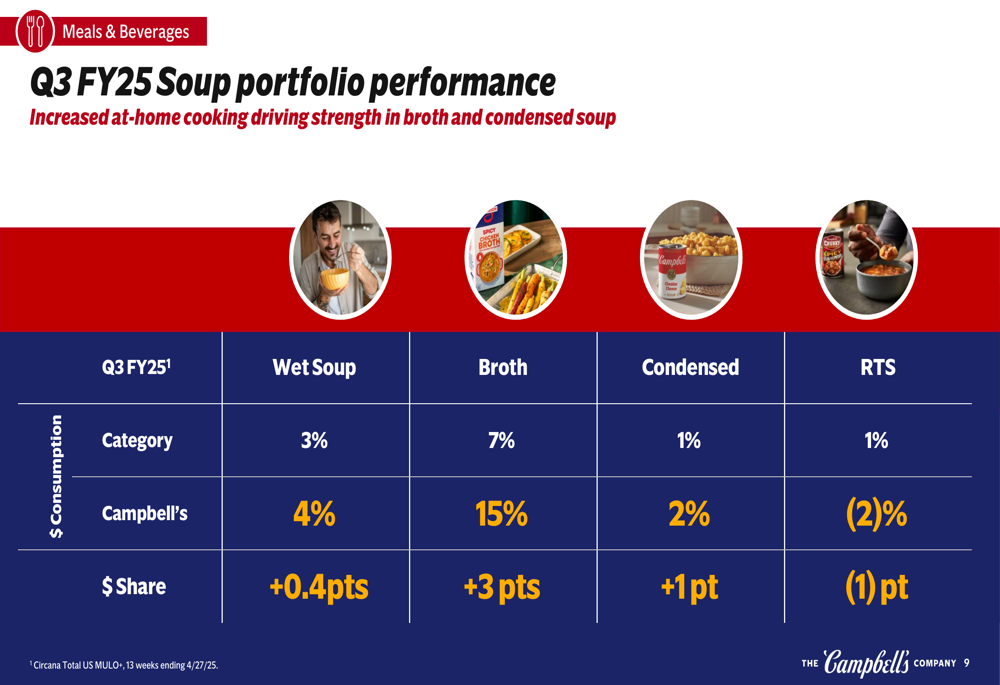

The Meals & Beverages segment demonstrated strong competitive performance in Q3, with particularly impressive results in the soup portfolio. Campbell’s wet soup consumption grew 4% against category growth of 3%, resulting in a 0.4 percentage point share gain. The company’s broth products significantly outperformed the category, with 15% consumption growth compared to 7% category growth, leading to a substantial 3 percentage point share gain:

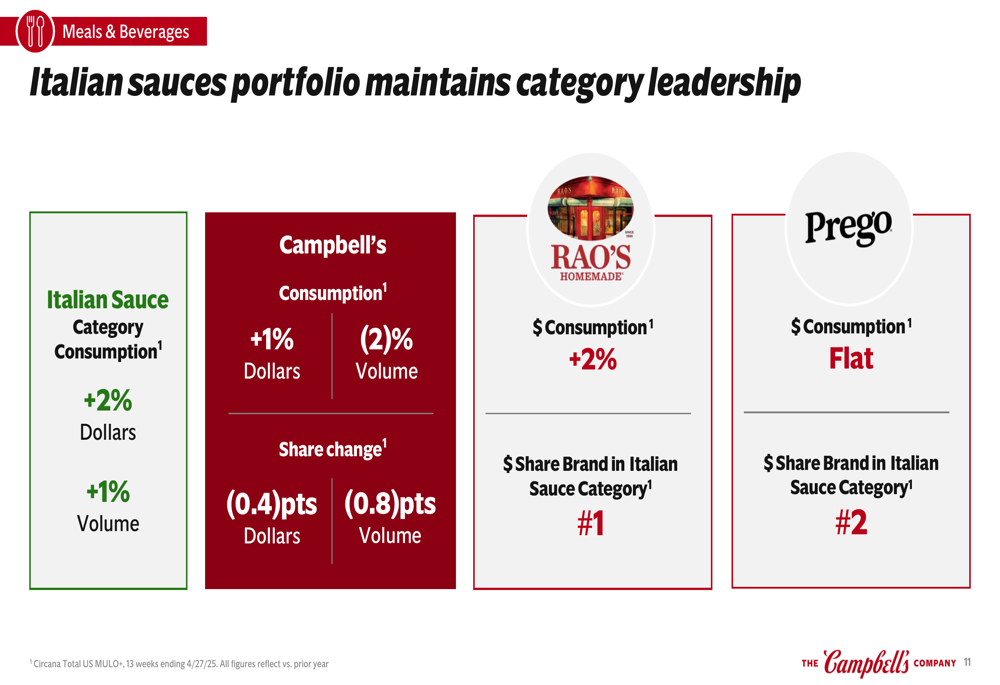

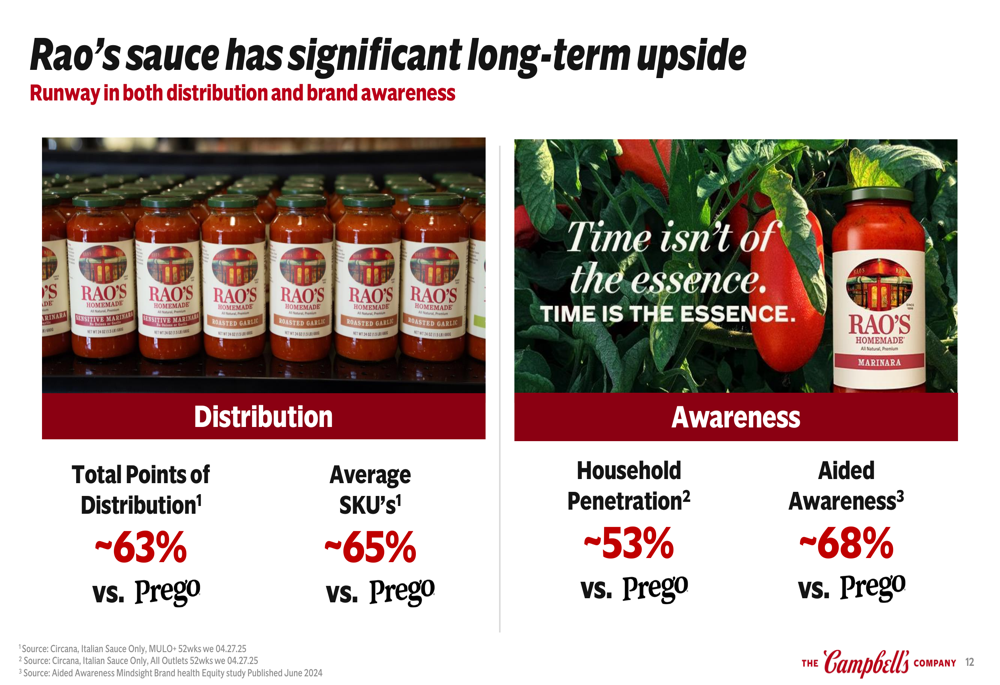

In the Italian sauces category, Campbell’s maintains leadership positions with both Rao’s (#1) and Prego (#2) brands. While the overall category grew 2% in dollar consumption, Campbell’s saw 1% growth in dollar consumption but lost 0.4 percentage points in dollar share:

The presentation highlighted significant growth potential for the Rao’s sauce brand, which currently has distribution at approximately 63% versus Prego and household penetration at about 53% versus Prego:

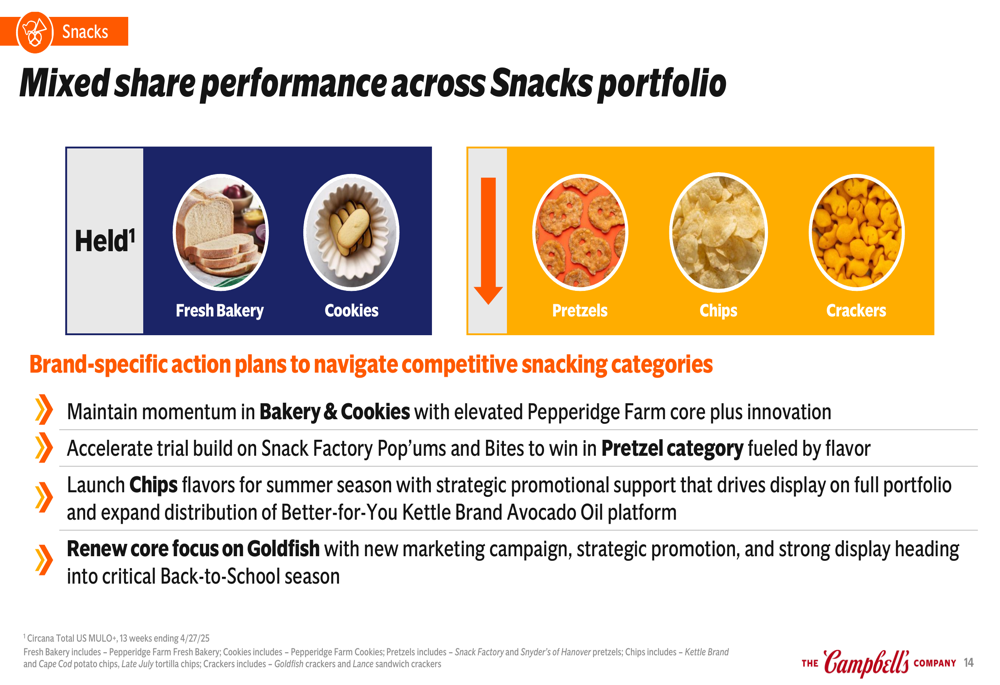

The Snacks segment continues to face competitive challenges, with dollar consumption declining 3% in Q3 and 2% year-to-date. The company outlined specific action plans to address these challenges, including maintaining momentum in Bakery & Cookies, accelerating trial for Snack Factory products, launching new Chips flavors, and renewing focus on the Goldfish brand:

Strategic Initiatives

Campbell’s is focusing on several strategic initiatives to drive growth and mitigate challenges. In the Meals & Beverages segment, the company highlighted success in growing its cooking condensed soup category, which achieved its highest Q3 volume growth and household penetration gain in four years. The brand gained one million new cooking buyers, 51% of whom were millennials:

For the Snacks segment, Campbell’s is implementing brand-specific actions to navigate competitive pressures. Despite overall segment challenges, the company noted growth in Pepperidge Farm Bakery, which achieved its highest volume and dollar growth in nine quarters, driven by the Farmhouse Brioche platform. Additionally, Pepperidge Farm Milano Cookies saw the strongest household penetration gains in nine quarters, fueled by the White Chocolate platform launch:

Forward-Looking Statements

Campbell’s reaffirmed its fiscal year 2025 guidance but noted that adjusted EPS is expected to be at the low end of the range due to incremental tariff impacts of $0.03 to $0.05 per share. The company projects net sales growth of 6% to 8%, organic net sales between -2% and 0%, and adjusted EBIT growth of 3% to 5%. Adjusted EPS is now expected to be in the range of $2.95 to $3.05:

The company emphasized its near-term focus on in-market execution while actively mitigating potential tariff impacts. Campbell’s is also building a stronger foundation by improving efficiency and effectiveness across the organization to facilitate growth across its brand portfolio.

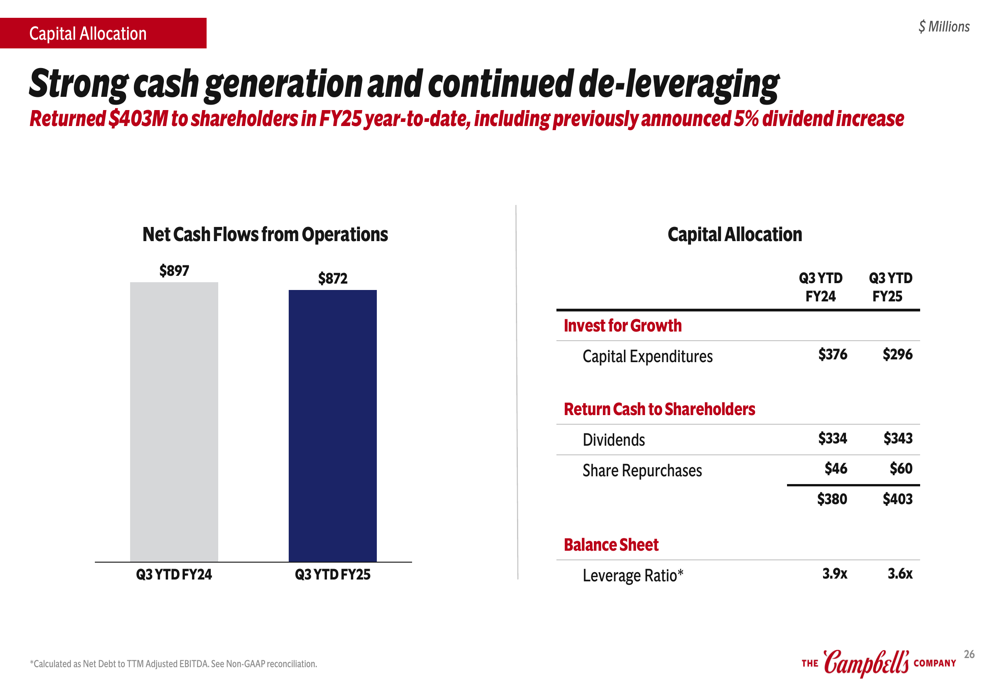

In terms of capital allocation, the company reported strong cash generation with $872 million in net cash flows from operations year-to-date. Campbell’s has returned $403 million to shareholders in FY25 year-to-date, including a previously announced 5% dividend increase:

While Campbell’s Q3 results showed improvement in organic sales compared to Q2, the company continues to face challenges from competitive pressures in the Snacks segment and the impact of tariffs on its outlook. The strength in Meals & Beverages provides a solid foundation, but investors will be watching closely to see if the company can successfully execute its strategic initiatives to address the ongoing challenges in its Snacks business and navigate the inflationary and tariff headwinds affecting its margins and earnings.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.