FTSE 100 today: Index flat at open, European markets mixed; pound weakens

Introduction & Market Context

Campbell Soup Company (NYSE:CPB) released its fourth quarter fiscal 2025 earnings presentation on September 3, 2025, reporting results slightly ahead of expectations despite a challenging operating environment. The stock responded positively in premarket trading, rising 1.24% to $31.85 after closing the previous session at $31.46, as investors welcomed the company’s expanded cost savings initiatives and strategic focus on premium brands.

CEO Mick Beekhuizen emphasized the company’s focus on "day-to-day execution" while building foundations for future growth, a strategy that appears to be maintaining stability in a difficult consumer environment. The presentation follows Campbell’s strong Q3 performance, where the company exceeded analyst expectations with an EPS of $0.73 against a forecast of $0.65.

Quarterly Performance Highlights

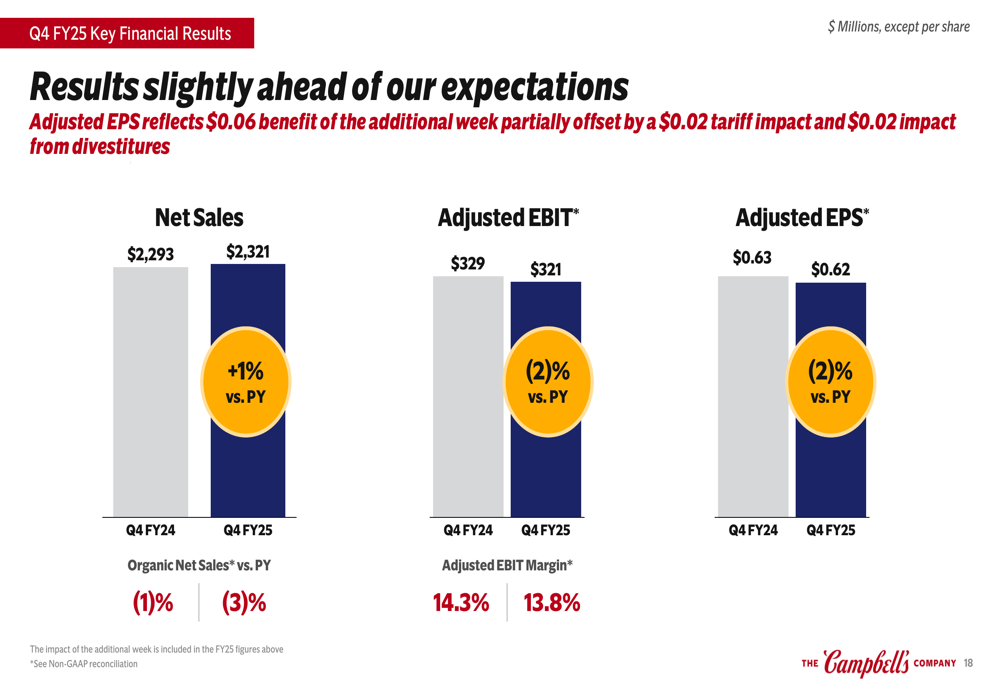

Campbell’s reported Q4 net sales of $2.32 billion, representing a 1% increase compared to the prior year, while organic net sales declined 3%. Adjusted EBIT fell 2% to $321 million with a margin of 13.8%, and adjusted EPS decreased 2% to $0.62. The company noted that Q4 volume/mix was negatively impacted by the reversal of Q3 shipment timing benefits.

As shown in the following financial results summary:

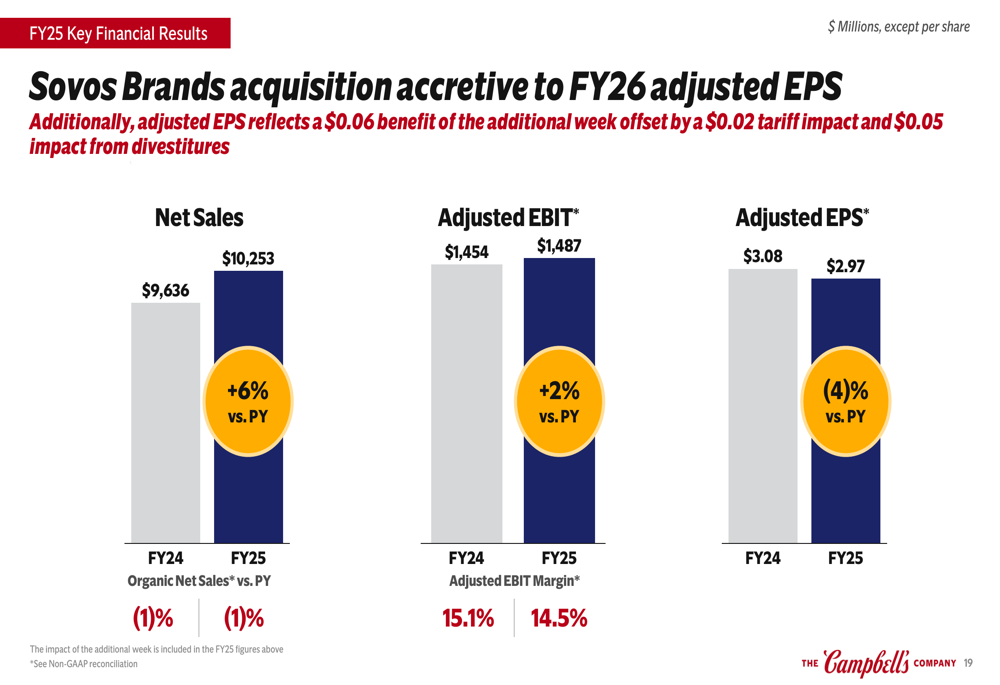

For the full fiscal year 2025, Campbell’s reported net sales of $10.25 billion, a 6% increase versus the prior year, though organic net sales declined 1%. Adjusted EBIT grew 2% to $1.49 billion, while adjusted EPS decreased 4% to $2.97.

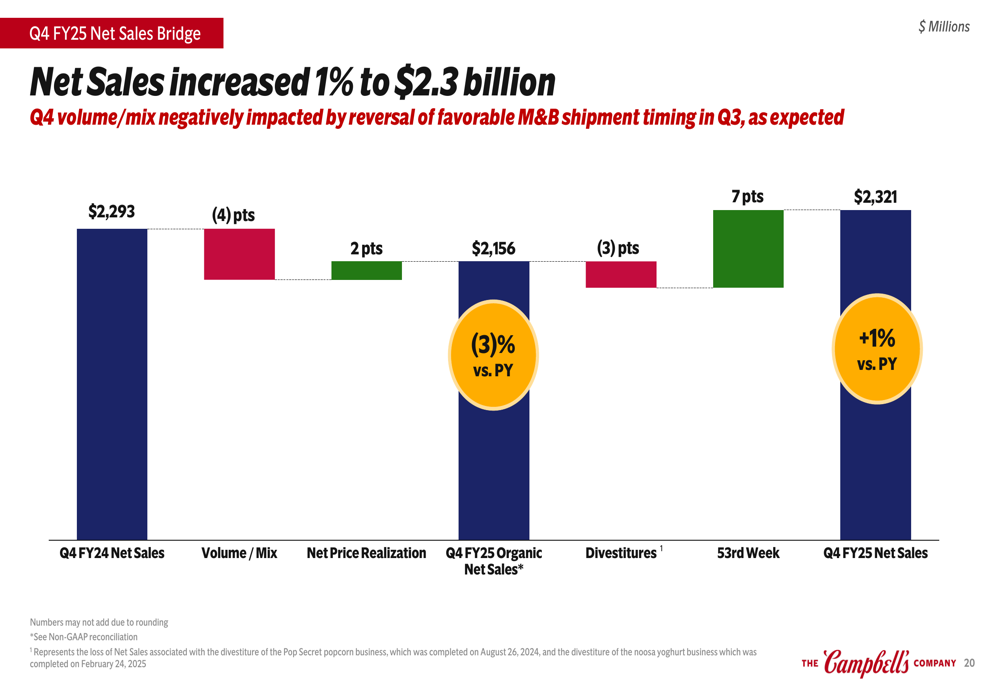

The Q4 net sales bridge reveals how a 7-point contribution from the 53rd week and 2 points from net price realization helped offset a 4-point decline in volume/mix and a 3-point impact from divestitures:

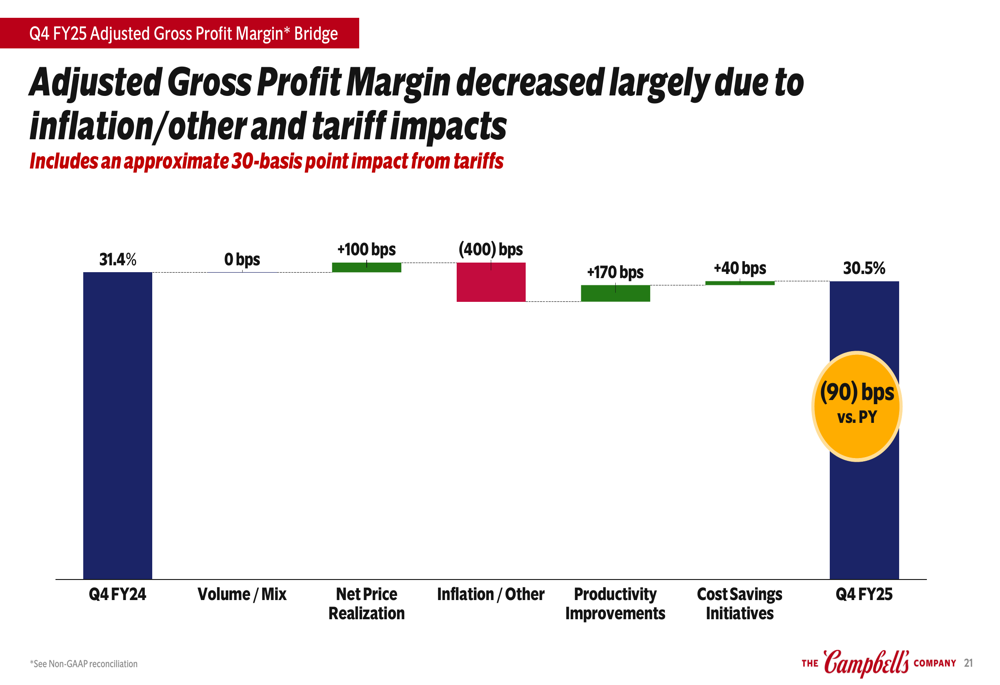

Gross profit margin decreased by 90 basis points to 30.5% in Q4, primarily due to inflation and tariff impacts, though this was partially mitigated by productivity improvements and cost-saving initiatives:

Segment Analysis

Meals & Beverages

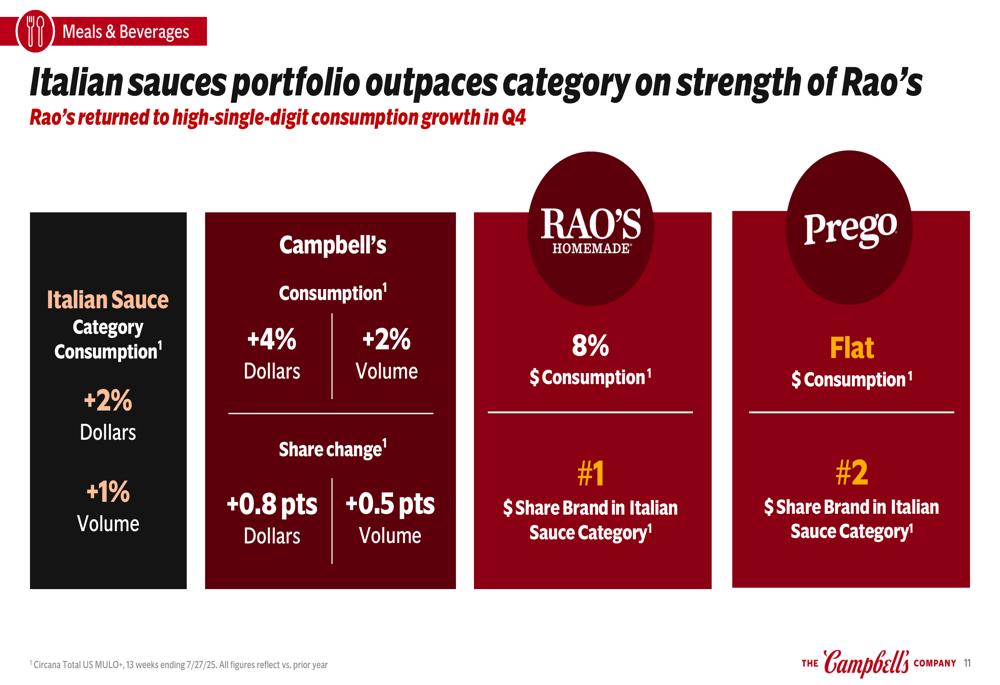

The Meals & Beverages segment demonstrated resilience with 1% dollar consumption growth and a 0.2 point share gain in Q4, outpacing category performance. While organic net sales declined 3%, this reflected the expected reversal of Q3 shipment timing benefits rather than fundamental weakness.

Campbell’s soup portfolio showed mixed results with flat performance in wet soup and condensed categories, while ready-to-serve declined 6%. The company’s Italian sauces portfolio was a particular bright spot, outpacing category growth with Rao’s returning to high-single-digit consumption growth (8%) and maintaining its position as the #1 share brand in the category:

The broth category also demonstrated sustained growth, with Campbell’s broth/stock achieving volume share growth in seven of eight quarters and outperforming category growth in both buy rate and trips per buyer:

Snacks

The Snacks segment showed sequential improvement despite a 2% decline in dollar consumption, with organic net sales down 2% and volume/mix down 5%. The company highlighted that half of its Snacks Leadership Brands had sequential consumption and share improvement.

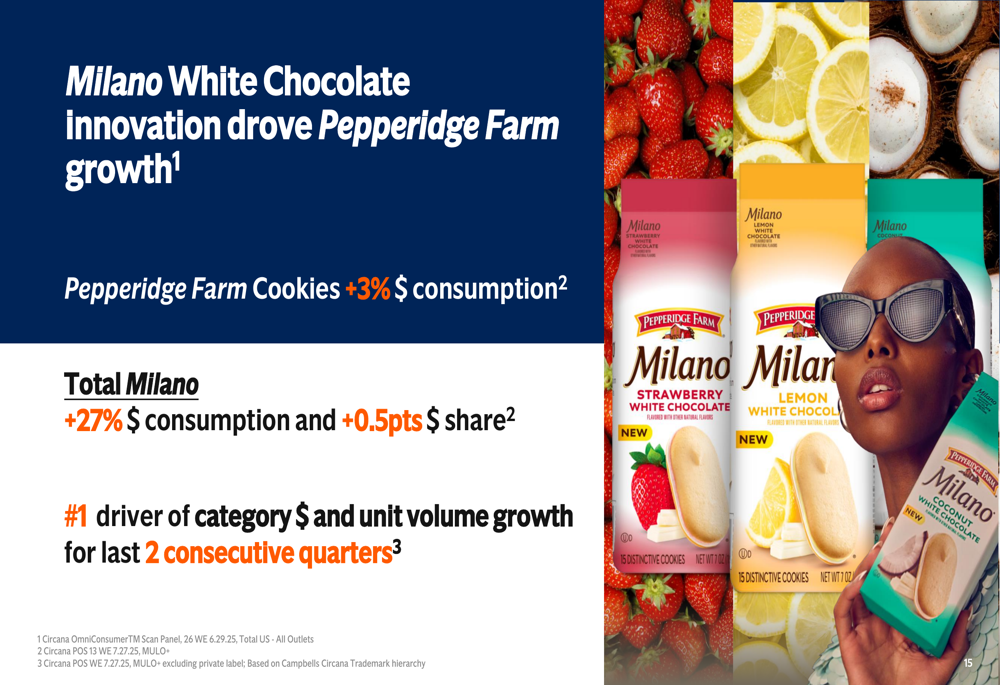

A standout performer was Milano cookies, particularly the White Chocolate innovation, which drove Pepperidge Farm cookies to 3% dollar consumption growth. Total Milano sales increased 27% with a 0.5 point share gain, making it the #1 driver of category dollar and unit volume growth for two consecutive quarters:

Strategic Initiatives and Cost Savings

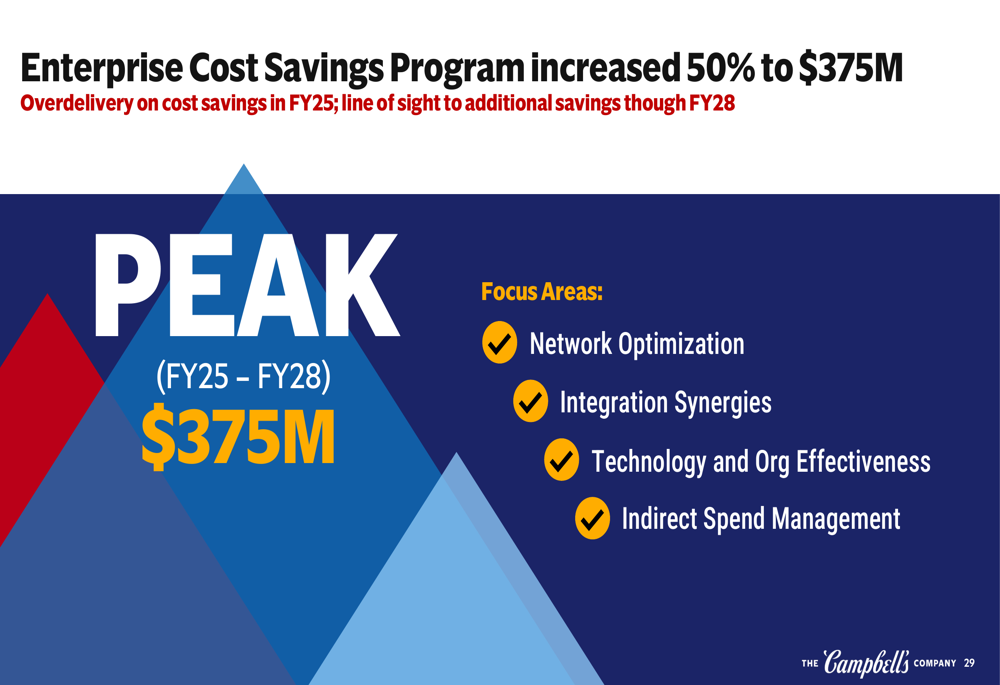

Campbell’s announced a significant expansion of its Enterprise Cost Savings Program, increasing the target by 50% to $375 million through fiscal 2028. The program encompasses network optimization, integration synergies, technology and organizational effectiveness improvements, and indirect spend management.

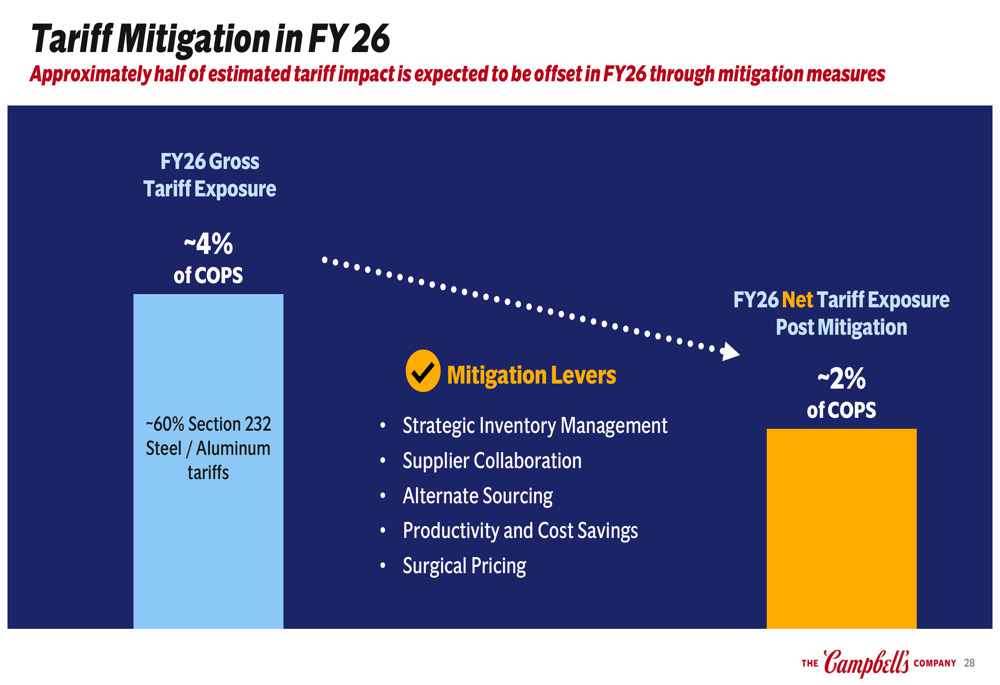

The company is also implementing a comprehensive tariff mitigation strategy for fiscal 2026, designed to offset approximately half of the estimated tariff impact through strategic inventory management and other measures. The net tariff exposure is expected to be around 2% of cost of products sold, with approximately 60% coming from Section 232 steel and aluminum tariffs:

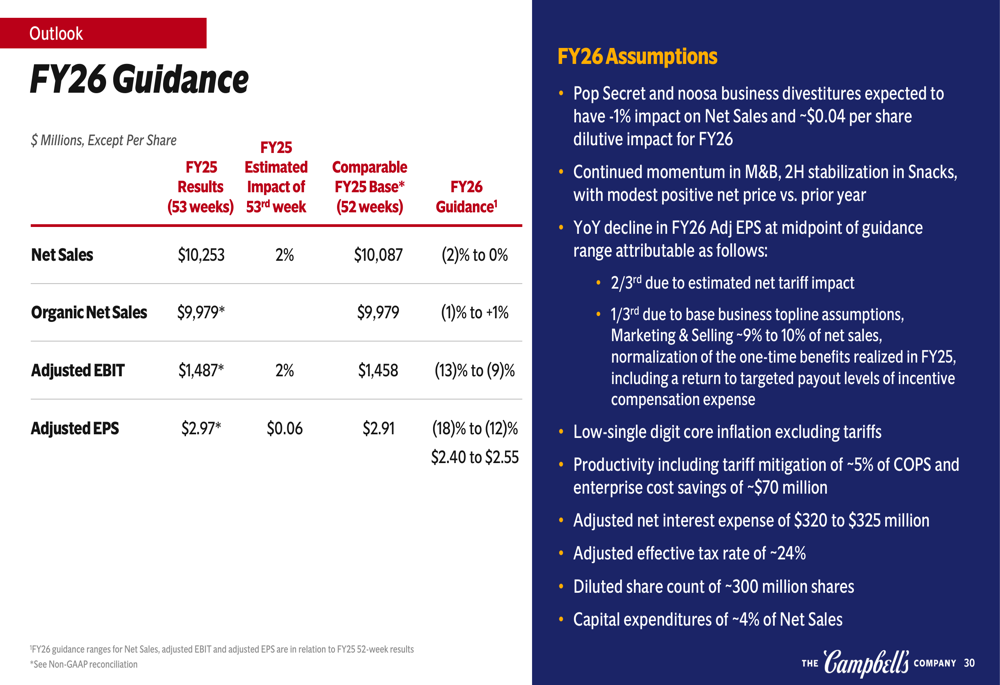

FY26 Outlook & Guidance

Looking ahead to fiscal 2026, Campbell’s provided guidance that reflects its focus on sustainable growth while managing near-term cost pressures. The company expects net sales growth of -1% to +1%, adjusted EBIT of approximately $1.46 billion, and adjusted EPS of around $2.91.

The guidance incorporates an approximately 1% negative impact from the divestiture of Pop Secret and Noosa businesses. Management emphasized a two-pronged approach of "delivering today" through day-to-day execution and capitalizing on cooking momentum, while "building for tomorrow" through the newly launched growth office and selective investments in digital transformation.

Campbell’s is maintaining a strong cash position with $1.13 billion in operating cash flow for fiscal 2025 and a leverage ratio of 3.6x. The company returned $521 million to shareholders during the fiscal year, underscoring its commitment to shareholder value despite challenging market conditions.

As Campbell’s navigates fiscal 2026, investors will be watching closely to see if the company’s expanded cost savings initiatives and premium brand strategy can successfully offset inflationary pressures and drive sustainable growth in an increasingly competitive consumer packaged goods landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.