Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

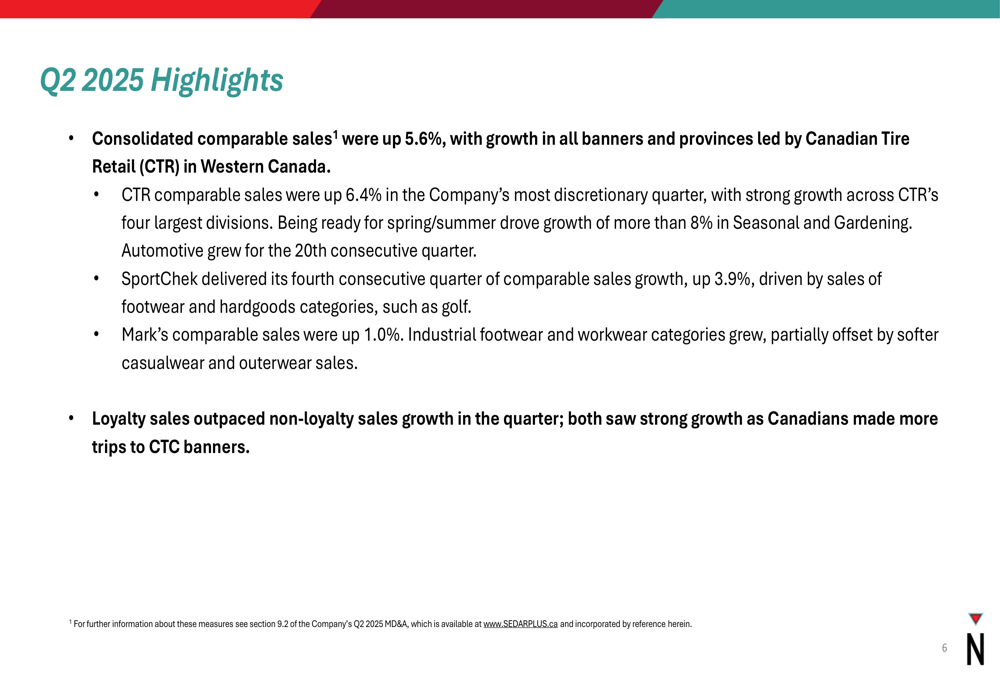

Canadian Tire Corporation (TSX:CTC) presented its Q2 2025 financial results on August 7, 2025, highlighting strong sales performance across all retail banners despite ongoing costs related to its True North transformation strategy. The company reported consolidated comparable sales growth of 5.6%, with increases across all banners and provinces, suggesting resilient consumer spending in the Canadian retail market.

The results come as Canadian Tire continues to implement its transformative growth strategy launched in Q1 2025, which includes significant investments in store enhancements, digital capabilities, and operational restructuring. While these initiatives are creating short-term costs, the company’s underlying performance metrics show positive momentum.

Quarterly Performance Highlights

Canadian Tire reported strong comparable sales growth across all its retail banners in Q2 2025. Canadian Tire Retail (CTR) led with a 6.4% increase, followed by SportChek at 3.9% and Mark’s at 1.0%. The company noted that Western Canada was particularly strong for CTR, and loyalty sales outpaced non-loyalty sales growth across the business.

As shown in the following slide detailing sales performance:

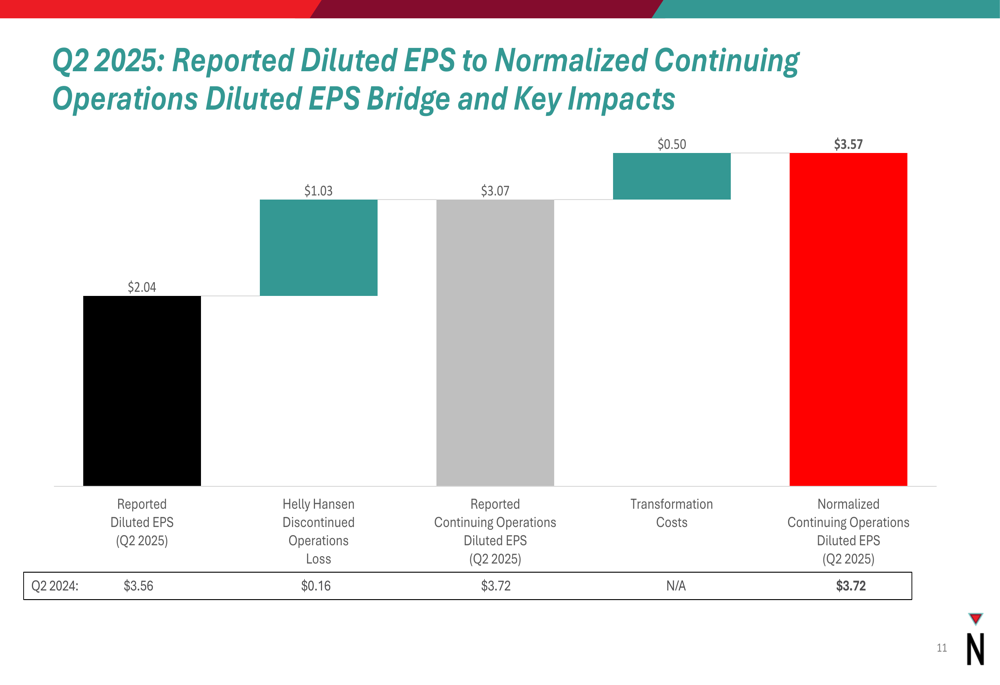

Retail revenue increased by 5.3% (or 9.0% excluding Petroleum), reflecting the strong sales performance. However, reported diluted earnings per share (EPS) was $2.04, down $1.52 from the previous year, primarily due to the Helly Hansen sale and True North transformation expenses.

When normalizing for these one-time factors, the company’s continuing operations generated $3.57 in diluted EPS, down only $0.15 from the previous year, demonstrating relatively stable underlying performance despite the transformation costs.

The following EPS bridge illustrates the impact of various factors on the company’s earnings:

Notably, the company’s Retail Return on Invested Capital (ROIC) improved to 10.3%, compared to 9.0% in Q2 2024, suggesting better capital efficiency despite the ongoing investments.

Strategic Initiatives

Canadian Tire’s True North transformation strategy, launched in Q1 2025, represents a significant strategic shift for the company. By the end of June 2025, the company had completed 21 of the 54 store enhancement projects planned for the year, representing approximately $116 million of operating capital expenditure in the first half.

These completed projects include:

- 14 Canadian Tire Retail store refreshes

- 5 Mark’s store refreshes

- SportChek’s second Destination Sport store

The company also extended its Pro Hockey Life (PHL) presence into Saskatchewan and has co-located 15 of 17 previously stand-alone Atmosphere sites within SportChek stores, optimizing its retail footprint.

In a significant brand portfolio expansion, Canadian Tire entered into an agreement to acquire iconic Canadian brands and intellectual property from the Hudson (NYSE:HUD)’s Bay Company, though specific details about this acquisition were not elaborated in the presentation.

The company also noted that reorganization of corporate teams is expected to be completed by the end of Q3 2025, with initial savings beginning in Q4 2025.

Detailed Financial Analysis

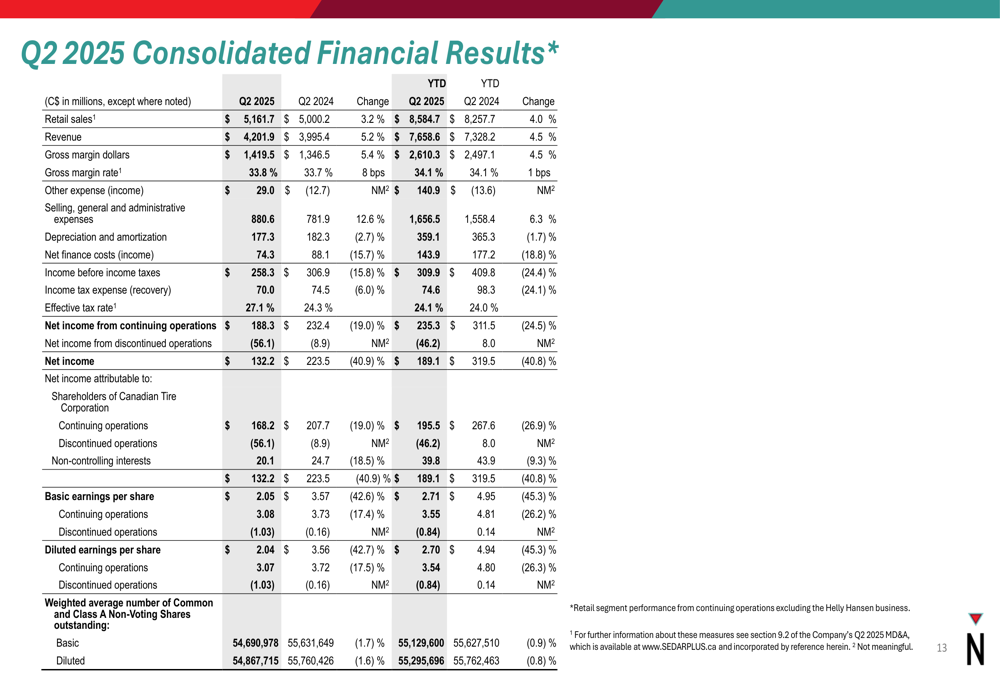

Canadian Tire’s consolidated financial results show both revenue growth and the impact of transformation costs. The following table provides a comprehensive view of the company’s Q2 2025 performance:

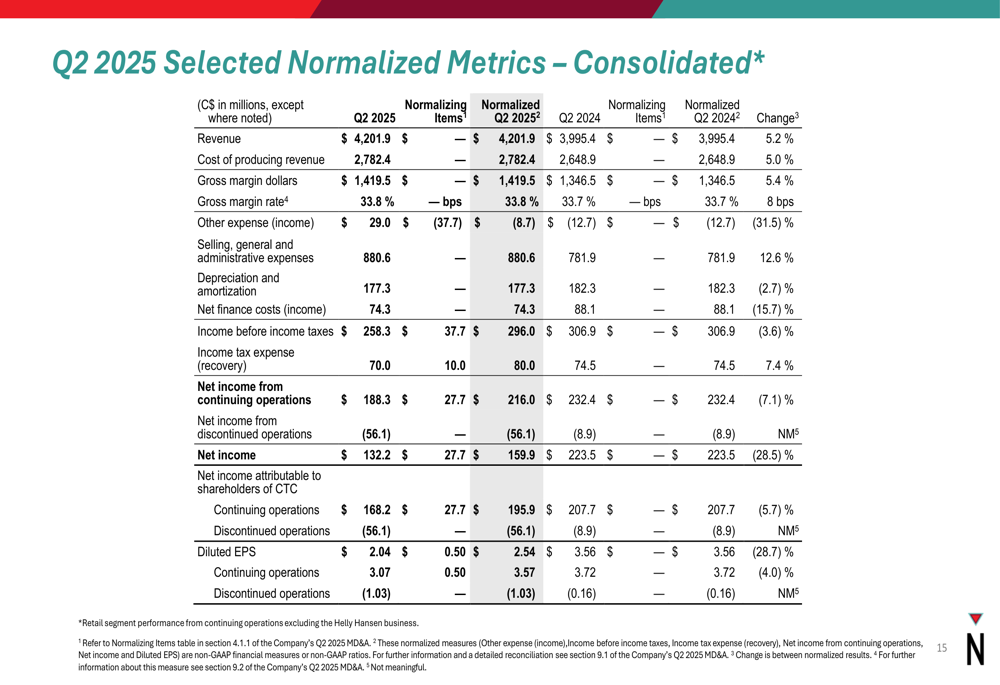

The company recorded $37.7 million in transformation and advisory costs in Q2 2025, contributing to a total of $151.8 million year-to-date before income taxes. After normalizing for these one-time expenses, the company’s performance metrics show a clearer picture of underlying business strength:

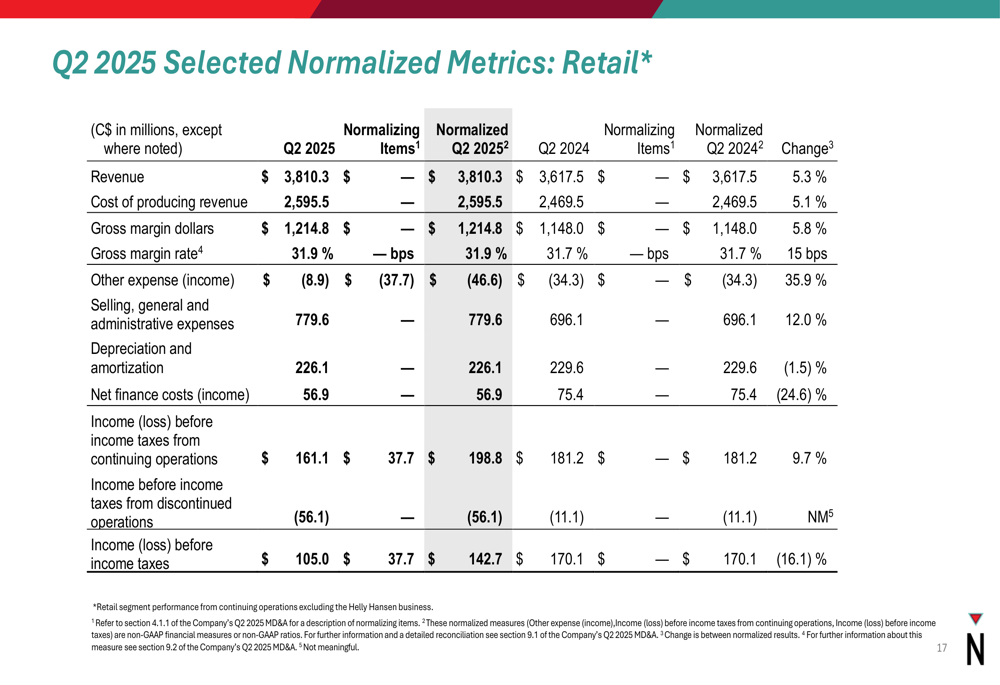

Looking at segment performance, the Retail segment showed strong growth with revenue up 5.3% to $3,810.3 million. After normalizing for transformation costs, the Retail segment’s income before income taxes from continuing operations was $198.8 million:

The Financial Services segment showed more modest growth, with revenue up 2.3% to $392.1 million and income before income taxes down 16.3% to $74.1 million.

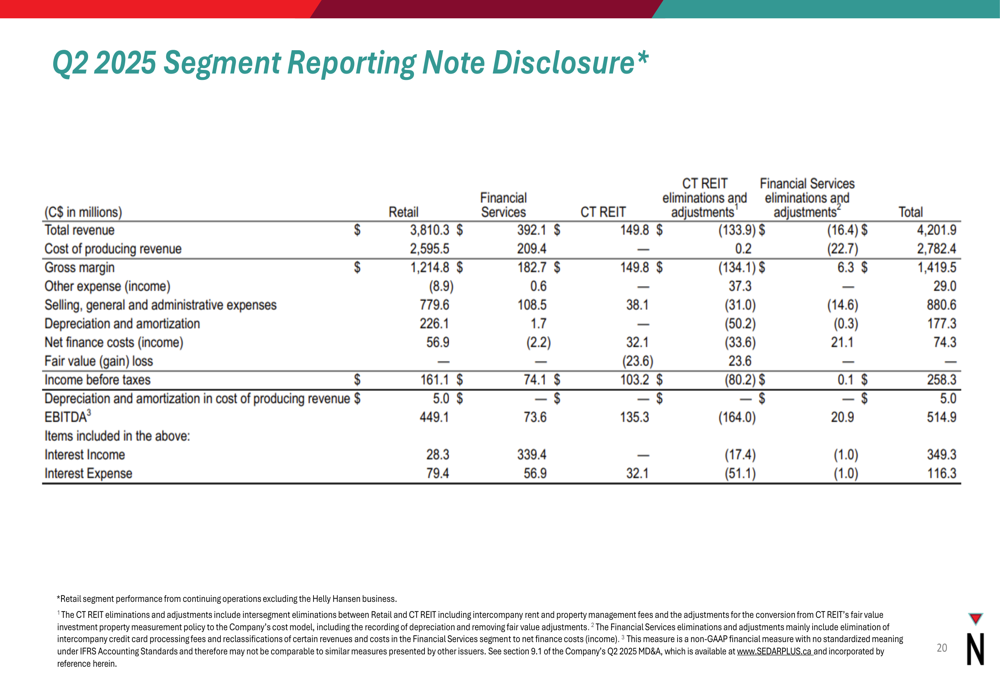

For a complete view of how the different segments contribute to the overall results, the following segment reporting disclosure provides detailed breakdowns:

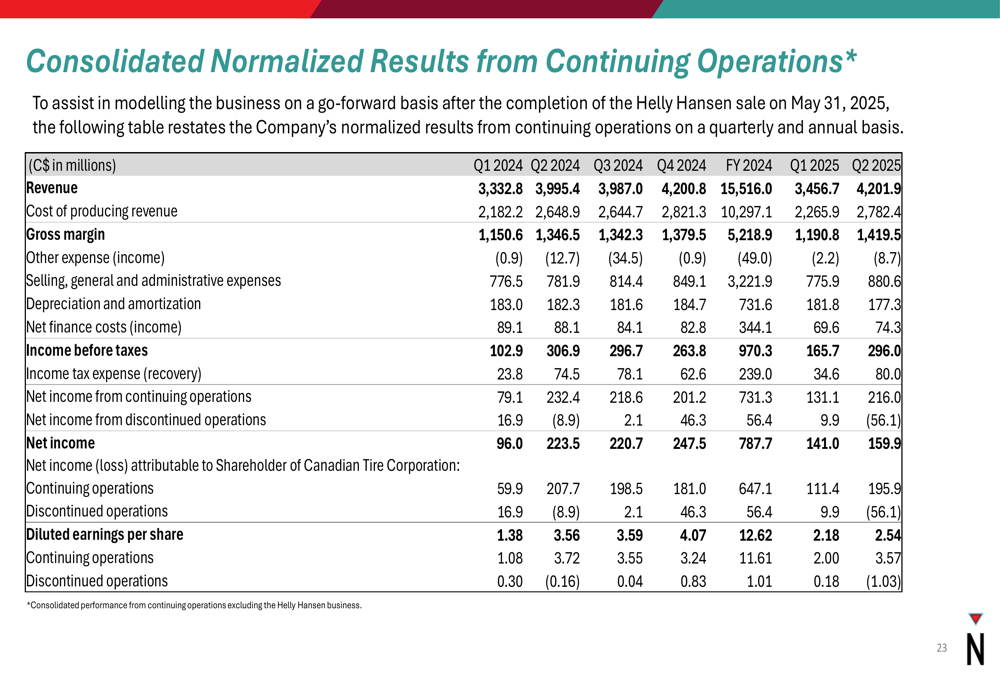

Looking at historical performance trends, the normalized results from continuing operations show the company’s quarterly performance over time:

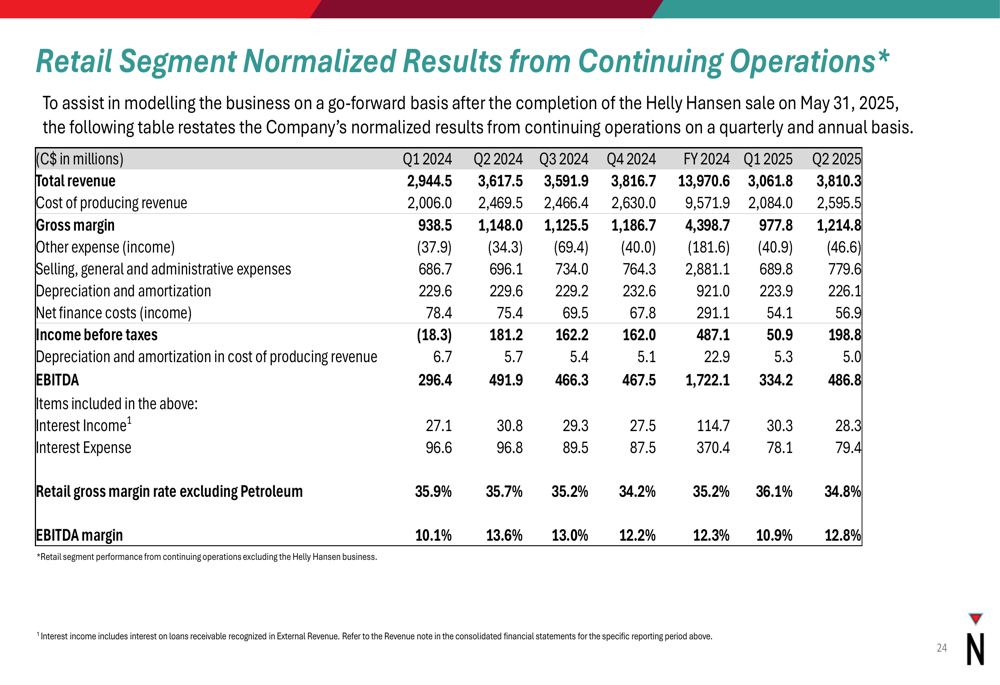

The Retail segment’s normalized results similarly show the quarterly trend:

Forward-Looking Statements

Canadian Tire’s presentation suggests continued focus on implementing its True North transformation strategy throughout 2025. With corporate reorganization expected to be completed by the end of Q3 2025, the company anticipates beginning to realize cost savings in Q4 2025.

The company remains committed to its store enhancement projects, with 33 more projects planned for completion in the second half of 2025. The expansion of the Triangle Rewards program also remains on track, though specific details about future initiatives were limited in the presentation.

While the company faces short-term costs related to its transformation initiatives, the improved ROIC and strong comparable sales growth across all banners suggest that the underlying business remains resilient. The acquisition of iconic Canadian brands from Hudson’s Bay Company also indicates continued investment in brand portfolio expansion despite the transformation costs.

As Canadian Tire progresses through its transformation, investors will likely focus on whether the company can maintain its sales momentum while beginning to realize the cost savings and operational efficiencies expected from its True North strategy in late 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.