Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

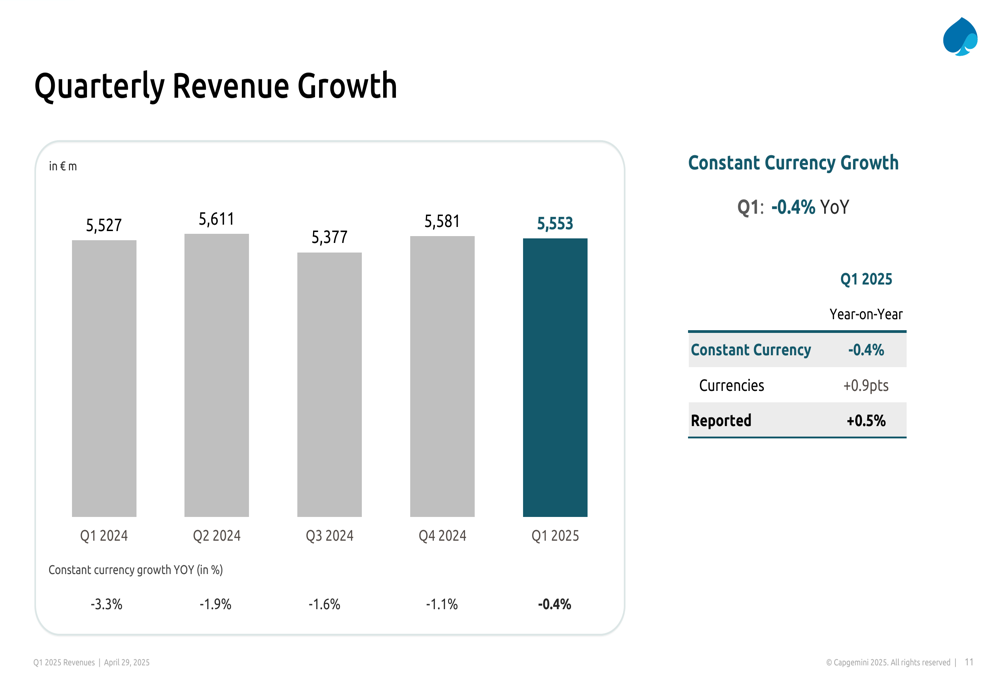

Capgemini (EPA:CAP) reported its Q1 2025 financial results on April 29, 2025, showing a slight revenue decline but performance that exceeded the company’s own expectations. The global IT services and consulting firm posted revenues of €5,553 million, representing a 0.4% year-over-year decrease at constant currency, while maintaining a healthy book-to-bill ratio of 1.06.

CEO Aiman Ezzat highlighted that the quarter’s performance was "slightly better than our expectations," despite continued challenges in certain regions and sectors. The company is increasingly focusing on high-growth areas such as Defense and Artificial Intelligence to offset weakness in traditional manufacturing clients.

Quarterly Performance Highlights

Capgemini’s Q1 2025 results revealed mixed performance across its business segments. While overall revenues declined slightly, bookings grew by 2.8% year-over-year, reaching €5.9 billion and resulting in a book-to-bill ratio of 1.06, indicating a solid pipeline for future business.

As shown in the following chart of quarterly performance highlights:

The company’s quarterly revenue trend shows relative stability over the past five quarters, with Q1 2025 revenues of €5,553 million representing a 0.4% decline at constant currency but a 0.5% increase on a reported basis, benefiting from a 0.9 percentage point positive currency impact.

Regional and Sector Analysis

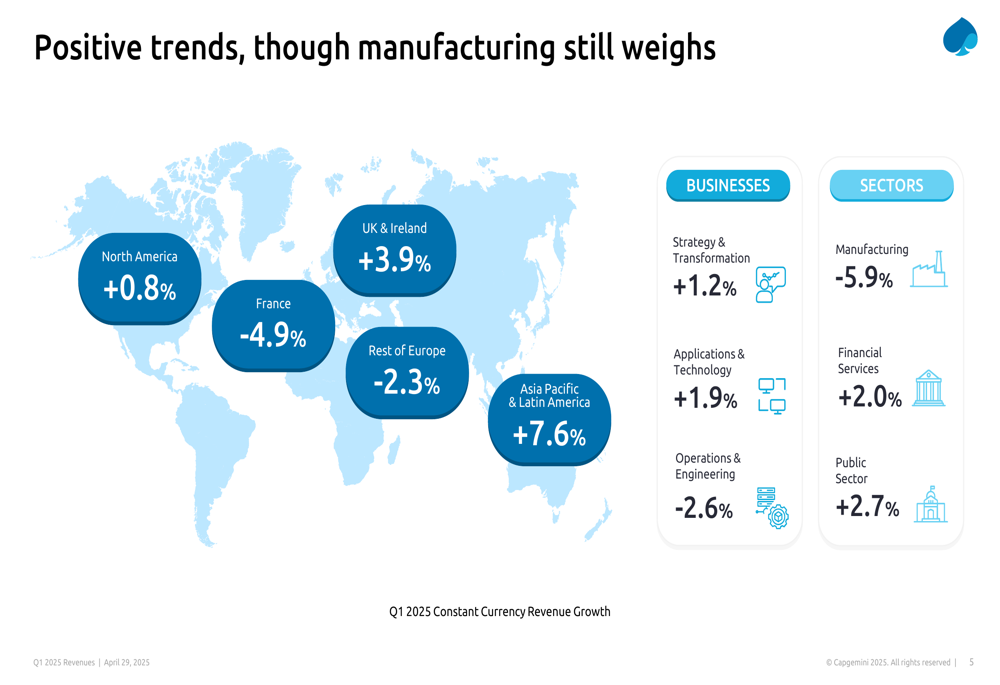

Capgemini’s performance varied significantly across geographical regions and industry sectors. The UK & Ireland and Asia-Pacific & Latin America regions demonstrated strong growth, while France and the Rest of Europe experienced declines.

The following geographical breakdown illustrates these regional disparities:

North America, representing 28% of FY2024 revenues, showed modest growth of 0.8%. The UK & Ireland region performed strongly with 3.9% growth, while France declined by 4.9%. The Rest of Europe, Capgemini’s largest region at 31% of revenues, contracted by 2.3%. The Asia-Pacific & Latin America region was the standout performer with 7.6% growth.

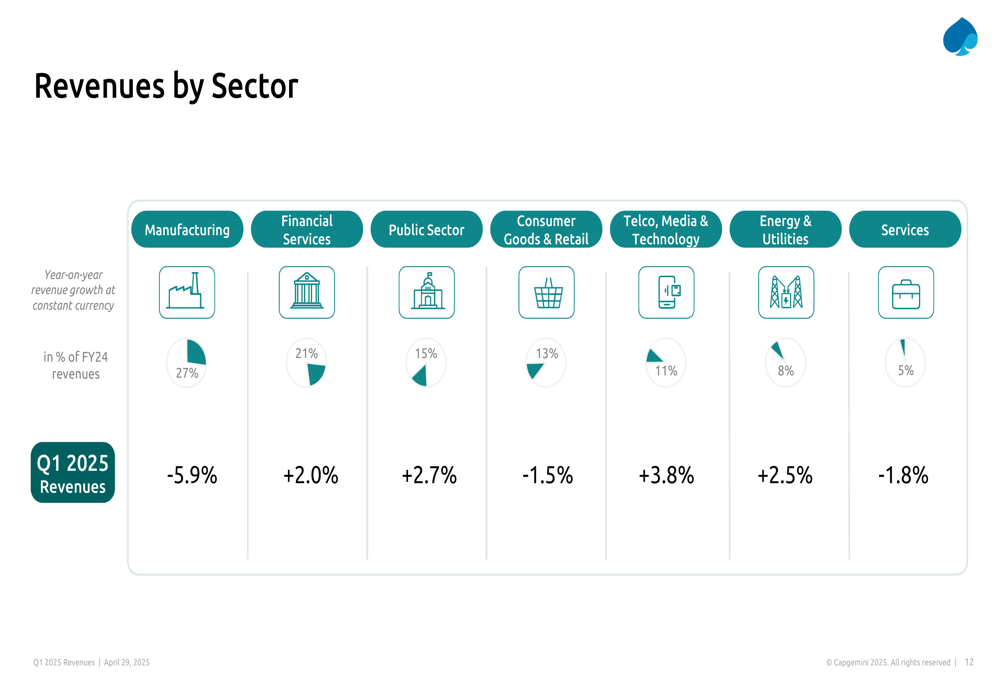

From a sector perspective, Manufacturing, which accounts for 27% of the company’s business, experienced the steepest decline at 5.9%. Financial Services, Public Sector, and Telco, Media & Technology all showed positive growth, as illustrated in the following breakdown:

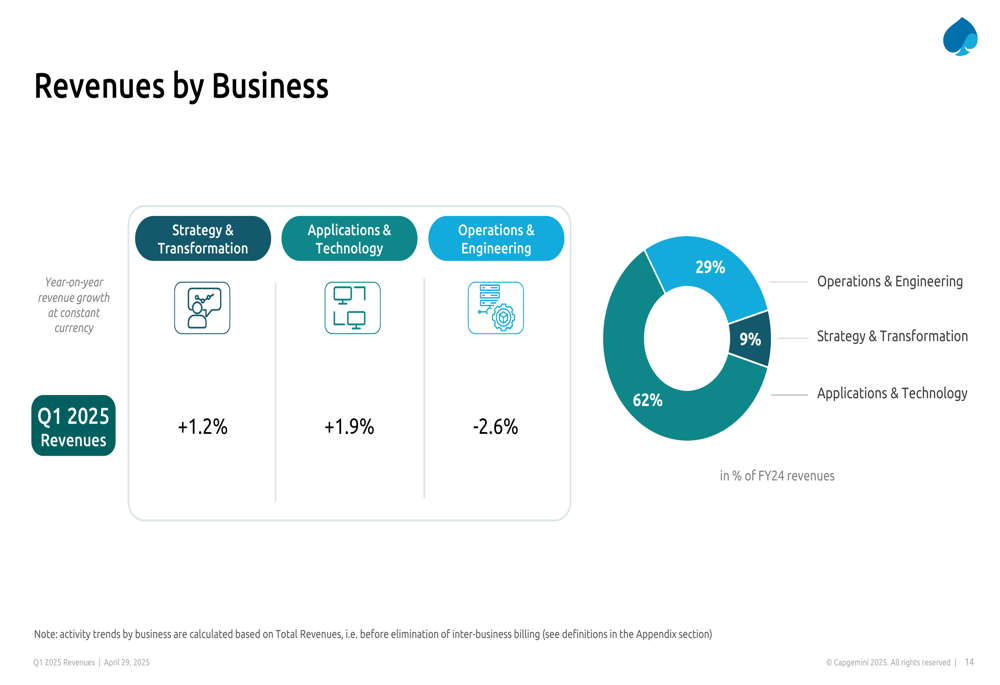

By business line, Strategy & Transformation grew by 1.2%, Applications & Technology by 1.9%, while Operations & Engineering declined by 2.6%. Applications & Technology remains Capgemini’s largest business segment, representing 62% of FY2024 revenues.

Strategic Initiatives

Capgemini highlighted two key strategic focus areas during its presentation: Defense sector expansion and Artificial Intelligence capabilities.

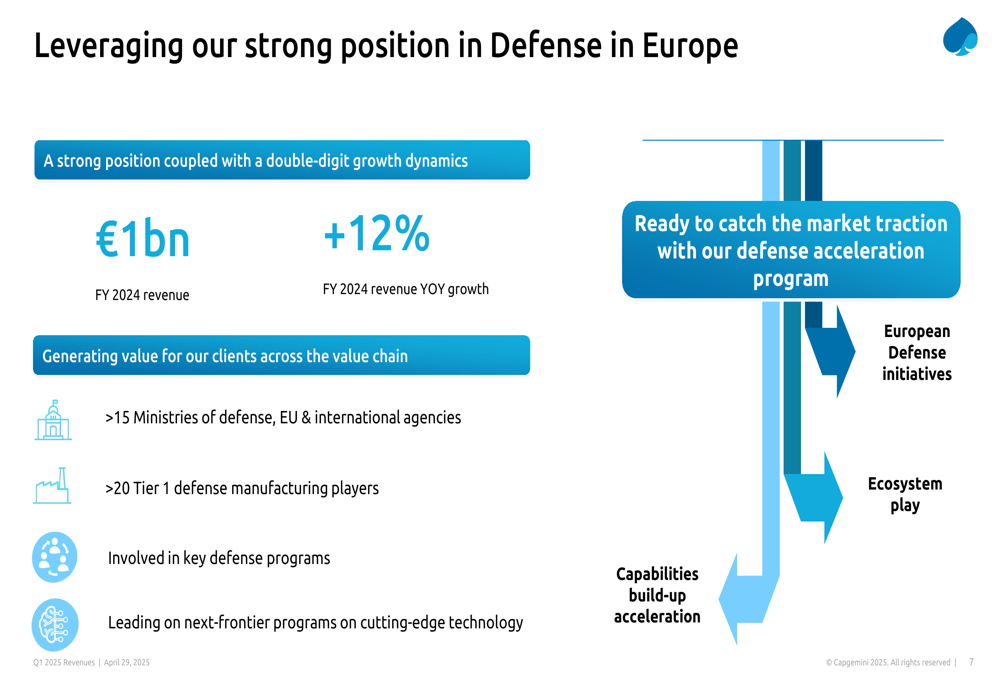

The company’s Defense business is experiencing robust growth, with FY2024 revenues of €1 billion and year-over-year growth of 12%. Capgemini serves over 15 Ministries of Defense and more than 20 Tier 1 defense manufacturing players, positioning it well to capitalize on increased defense spending across Europe.

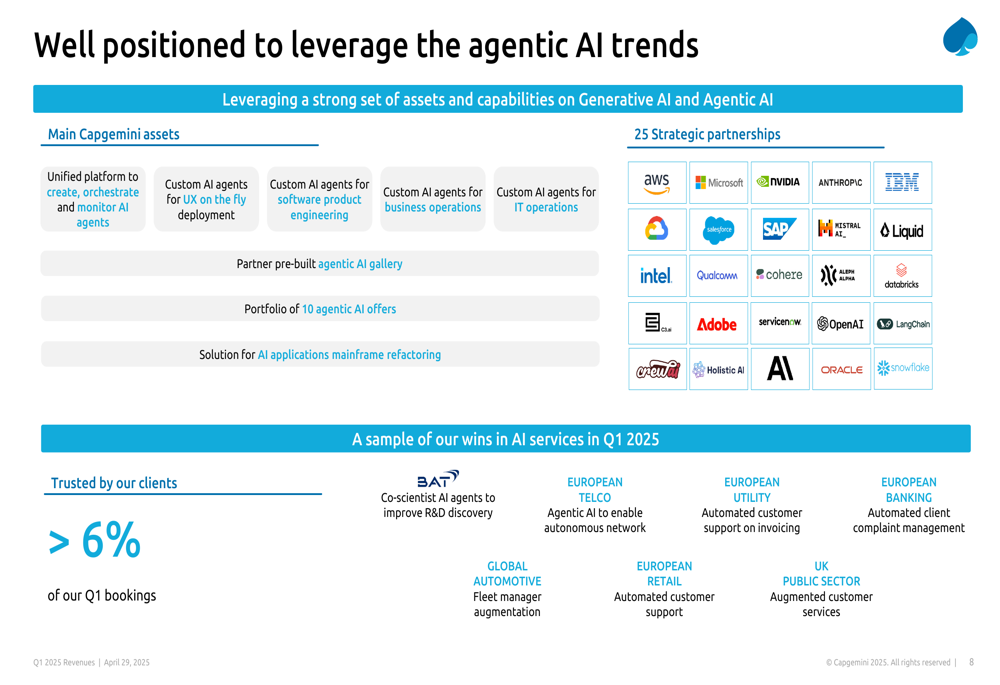

In the rapidly evolving field of Artificial Intelligence, Capgemini is leveraging both generative and agentic AI capabilities through strategic partnerships and proprietary assets. The company reported that over 6% of Q1 bookings were related to AI services, demonstrating growing client demand in this area.

Forward-Looking Statements

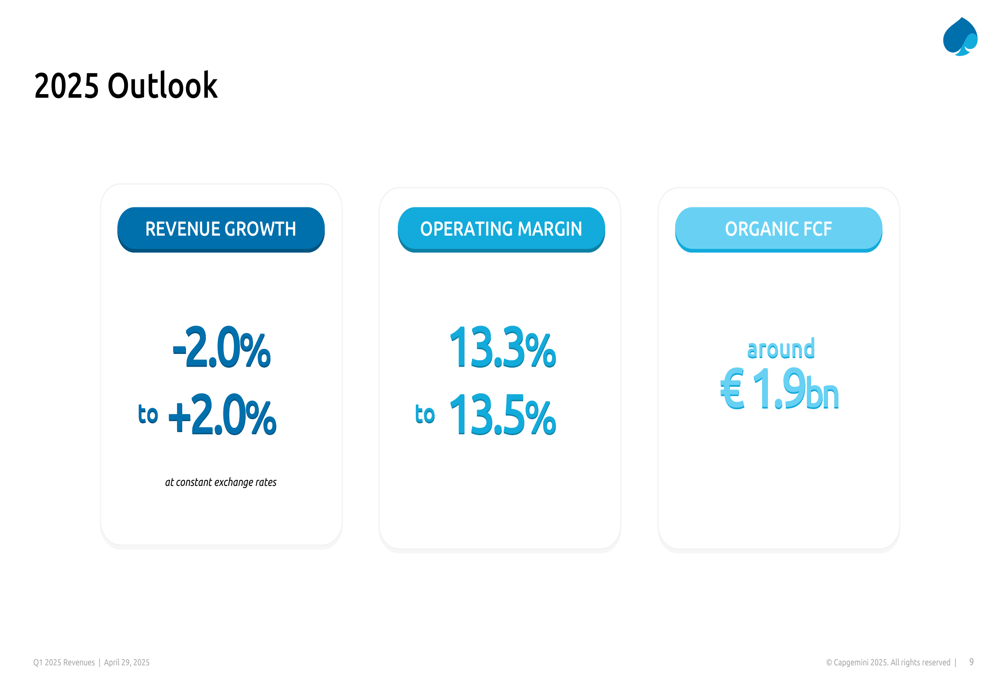

Looking ahead, Capgemini maintained its full-year 2025 outlook, projecting revenue growth between -2.0% and +2.0% at constant exchange rates. The company expects an operating margin between 13.3% and 13.5%, with organic free cash flow of approximately €1.9 billion.

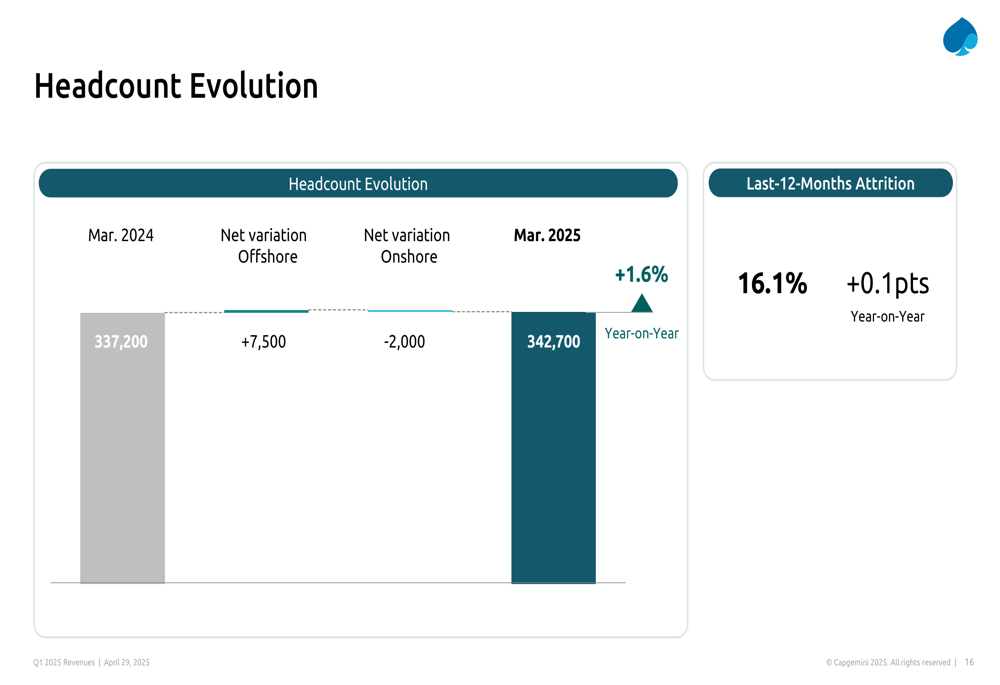

The company’s workforce grew by 1.6% year-over-year to 342,700 employees as of March 2025, with offshore headcount increasing by 7,500 while onshore headcount decreased by 2,000. The last-12-months attrition rate stood at 16.1%, up slightly by 0.1 percentage points compared to the previous year.

Capgemini’s focus on high-value services, particularly in Defense and AI, appears to be part of a strategic pivot to offset challenges in traditional sectors like Manufacturing. The company’s book-to-bill ratio of 1.06 suggests a reasonably healthy pipeline for the coming quarters, despite the cautious revenue growth outlook for the full year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.