CCH Holdings prices IPO at $4 per share on NASDAQ

Introduction & Market Context

Capital Power Corporation (TSX:CPX) presented its Q2 2025 analyst presentation on July 30, 2025, highlighting the company’s strategic transformation through significant U.S. expansion. Despite the positive narrative presented by management, Capital Power’s stock declined 6.95% on the day to close at $57.95, suggesting investors may have expected even stronger results or guidance.

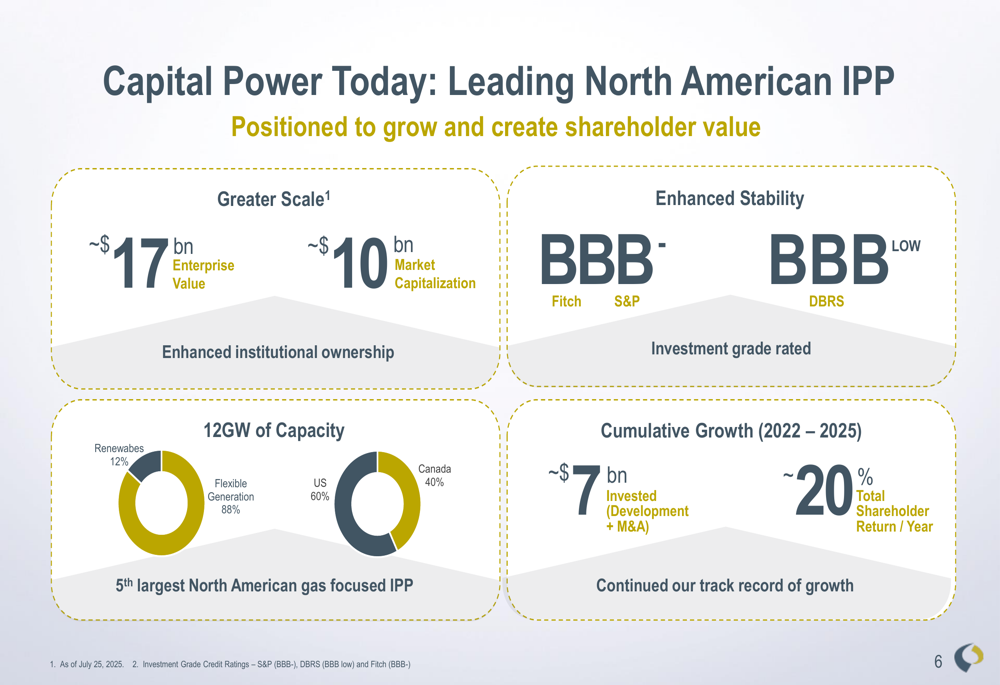

The presentation, led by President and CEO Avik Dey and CFO Sandra Haskins, detailed how the company has evolved into a leading North American independent power producer with an enterprise value of approximately $17 billion and market capitalization of around $10 billion.

Quarterly Performance Highlights

Capital Power reported Q2 2025 revenues of $769 million, representing a $64 million increase year-over-year. Adjusted EBITDA remained relatively flat at $322 million (down $1 million YoY), while Adjusted Funds from Operations (AFFO) showed strong growth at $235 million, up $57 million from the previous year.

For the first half of 2025, the company’s financial performance demonstrated more substantial improvements, with revenues reaching $1,684 million (+$63M YoY), adjusted EBITDA of $689 million (+$77M YoY), and AFFO of $453 million (+$126M YoY).

The company’s quarterly financial performance is illustrated in the following chart:

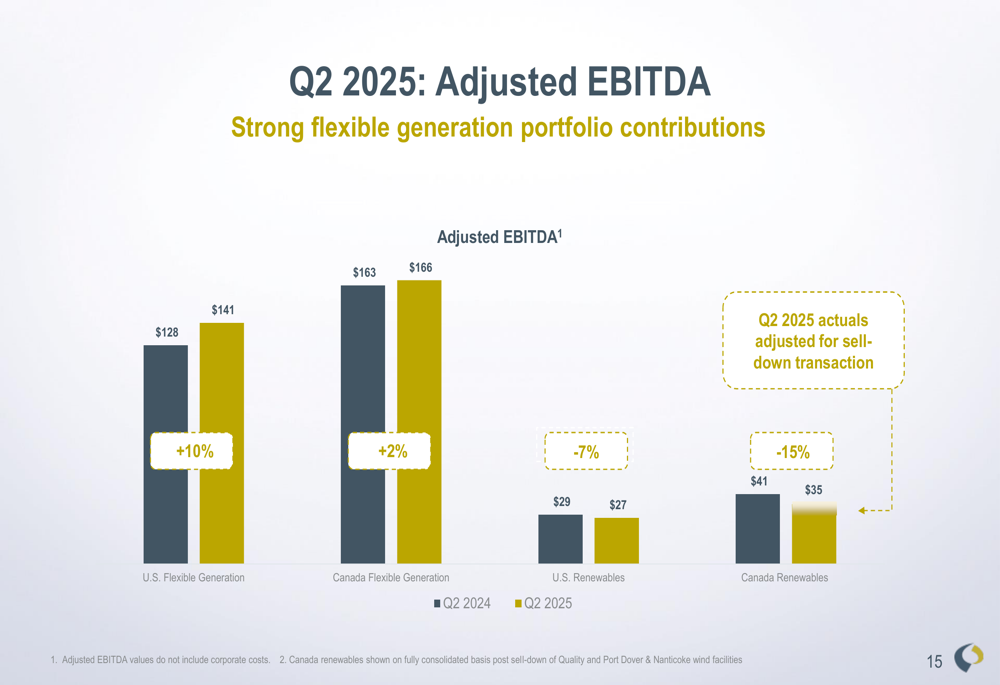

Looking at segment performance, U.S. Flexible Generation continues to be a key driver of growth, with Q2 2025 adjusted EBITDA of $141 million, representing a 10% increase from Q2 2024. Canadian Flexible Generation also showed modest growth of 2%, while both U.S. and Canadian Renewables segments experienced declines of 7% and 15% respectively.

As shown in this breakdown of adjusted EBITDA by segment:

Strategic Initiatives

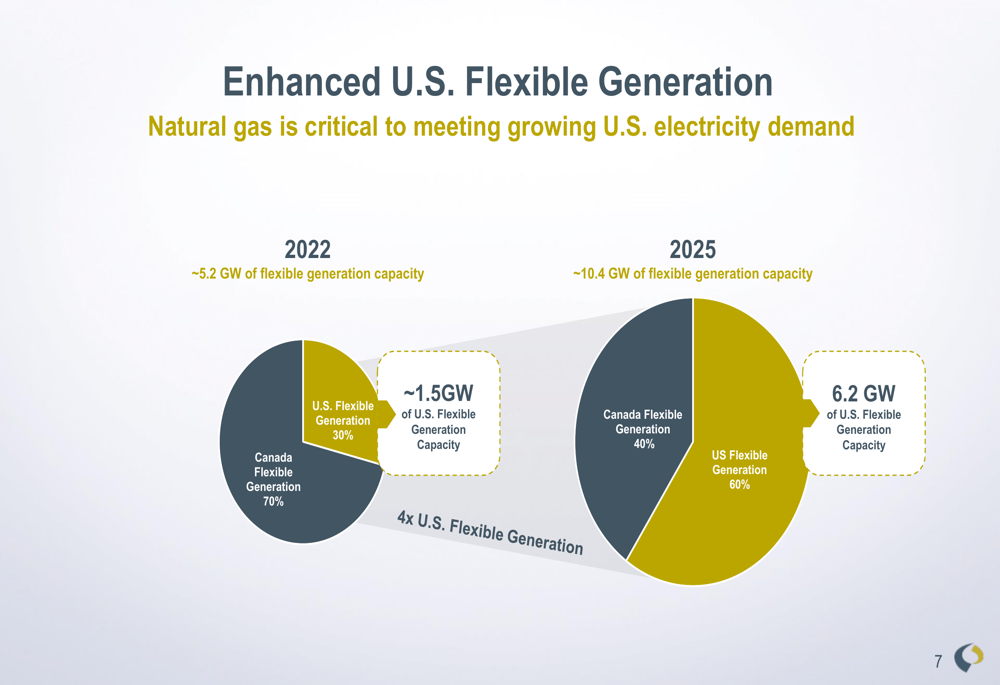

The cornerstone of Capital Power’s strategy has been its dramatic expansion in the U.S. market. The company closed what it described as its "largest acquisition in company history" in the PJM market, adding approximately 2.2 GW of generation capacity. This strategic move has fundamentally transformed the company’s portfolio, with U.S. flexible generation now representing 60% of total capacity, up from just 30% in 2022.

This transformation is clearly illustrated in the following chart showing the shift in flexible generation capacity:

The company’s overall capacity now stands at 12 GW, with 88% coming from flexible generation and 12% from renewables. Geographically, 60% of capacity is located in the U.S. with the remaining 40% in Canada. Since 2022, Capital Power has invested approximately $7 billion in development and acquisitions, delivering a total shareholder return of around 20% per year.

The current scale and composition of Capital Power’s portfolio is shown here:

Competitive Industry Position

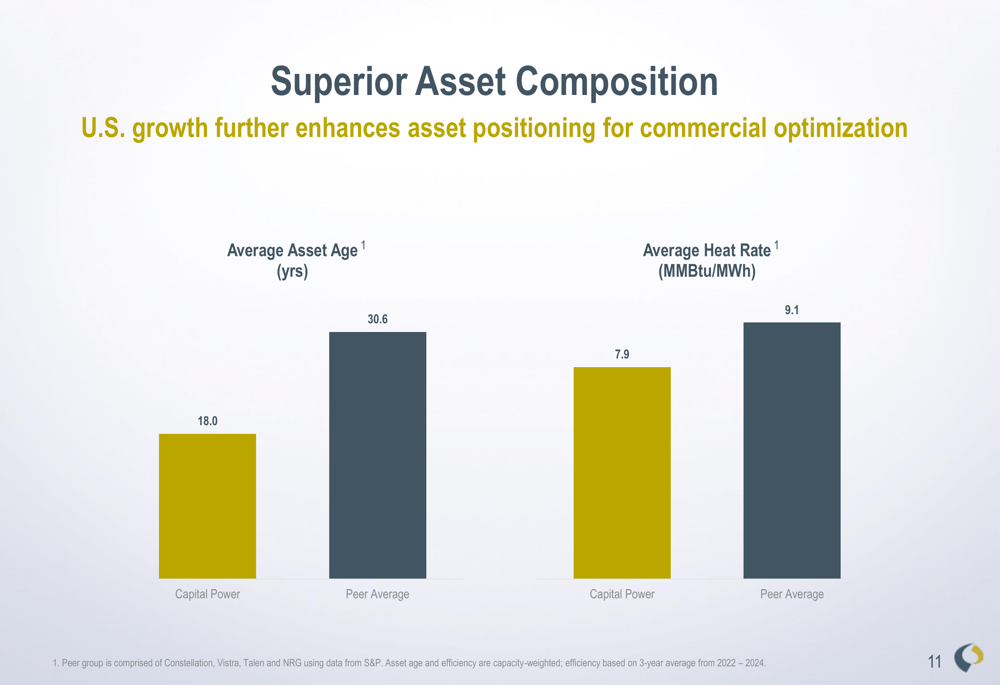

Capital Power highlighted several competitive advantages in its presentation, particularly its superior asset composition compared to peers. The company’s generation assets have an average age of 18.0 years, significantly younger than the peer average of 30.6 years. Additionally, Capital Power’s average heat rate of 7.9 MMBtu/MWh outperforms the peer average of 9.1 MMBtu/MWh, indicating greater efficiency.

This competitive positioning is illustrated in the following comparison:

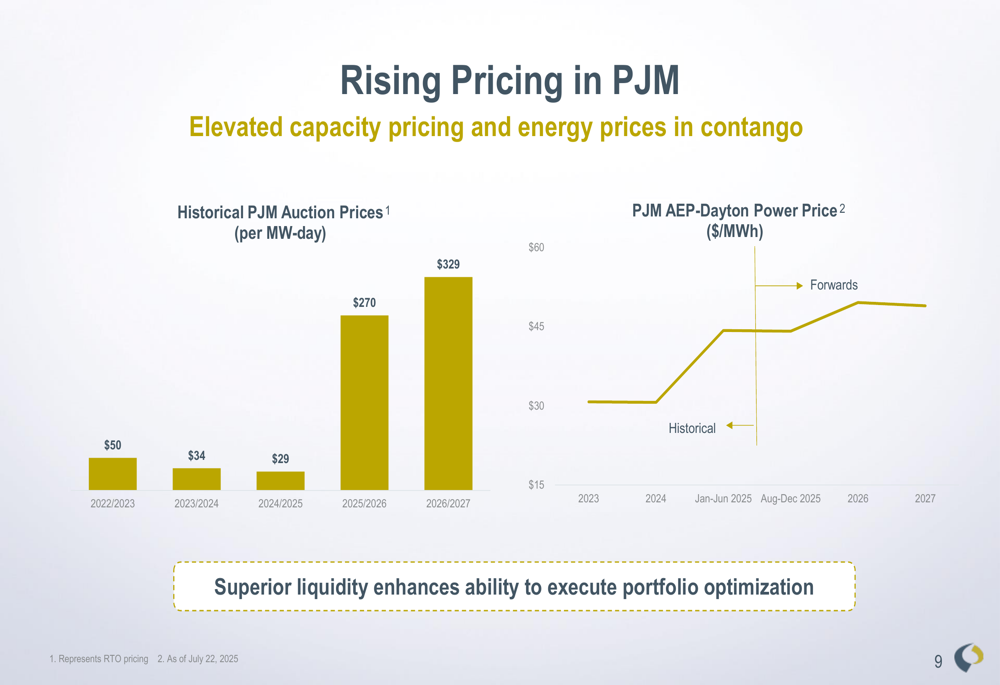

The company also emphasized strong market fundamentals across its operating regions, particularly in the PJM market where capacity prices have risen dramatically from $29 per MW-day for 2024/2025 to $329 per MW-day for 2026/2027. This favorable pricing environment is expected to benefit Capital Power’s expanded U.S. portfolio.

The rising pricing trend in the PJM market is shown in this chart:

Forward-Looking Statements

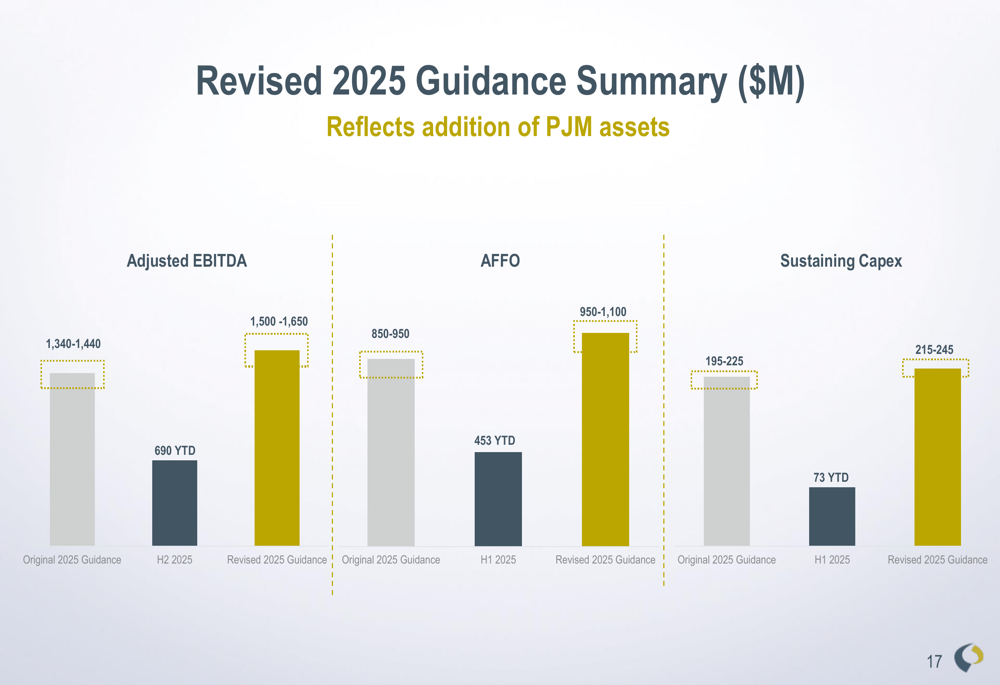

Based on strong performance in the first half of the year, Capital Power has revised its 2025 guidance upward. Adjusted EBITDA is now projected to be between $1,500-1,650 million, up from the original guidance of $1,340-1,440 million. Similarly, AFFO guidance has been increased to $950-1,100 million from the original $850-950 million.

The revised guidance is summarized in the following table:

Capital Power continues to maintain financial discipline while pursuing growth, with a dividend payout ratio within its targeted range of 30-50%. The company has delivered a dividend CAGR of 6% and an AFFO per share CAGR of 7% from 2020 to 2025.

The company’s diverse funding sources for its growth initiatives include 44% debt, 20% common equity, 18% internal cash flow, 11% partnerships, 4% asset sales, and 3% hybrids. This balanced approach to capital allocation has supported the company’s expansion while maintaining investment grade credit ratings (BBB- from Fitch and S&P, BBB low from DBRS).

Outlook

Looking ahead, Capital Power is well-positioned to capitalize on strong market fundamentals across its operating regions. The company’s younger, more efficient asset base provides competitive advantages, while its increased scale and geographic diversification enhance stability.

The company announced it will host an Investor Day on December 9-10, 2025, in Toronto, which will include a tour of the Goreway Power Station and detailed presentations on future strategy.

This presentation follows Capital Power’s strong Q1 2025 performance, where the company significantly exceeded market expectations with EPS of $1.03 (vs. forecast of $0.5664) and revenue of $988 million (vs. forecast of $711.91 million). The continued strong performance through Q2 and the upward revision of full-year guidance suggest Capital Power is successfully executing its transformation strategy, despite the market’s cautious reaction to the latest results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.