Verizon to cut 15,000 jobs amid growing competition pressures - WSJ

Introduction & Market Context

Capstone Copper Corp. (TSX:CS) presented its first quarter 2025 results on May 1, highlighting record quarterly revenue and significantly improved financial performance amid rising copper prices and operational improvements. The company’s shares closed at $6.64 on the presentation day, up 1.2% or $0.08.

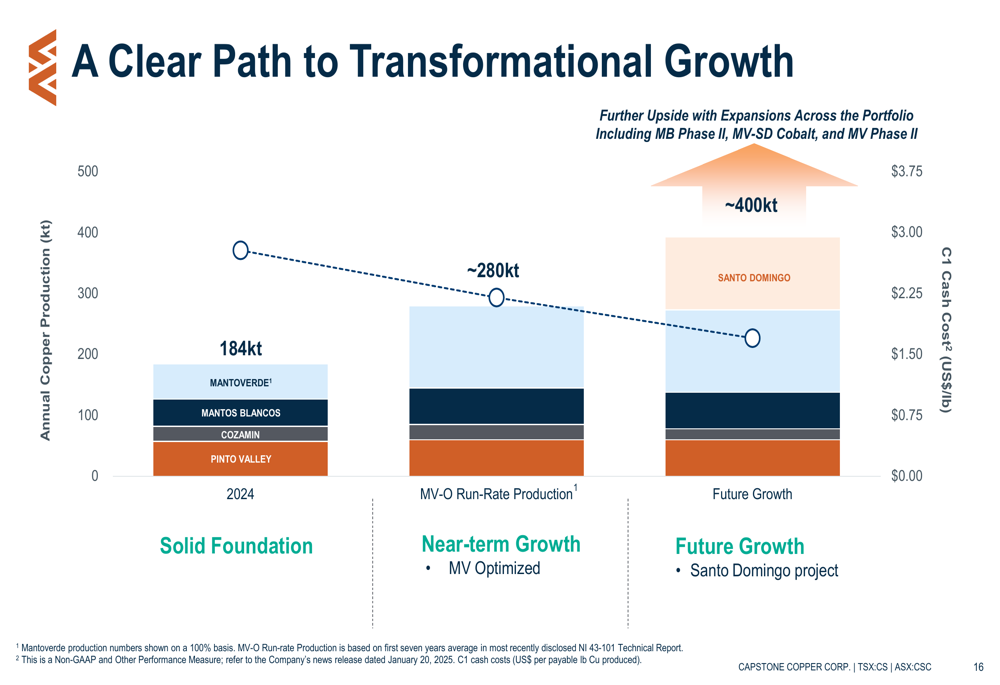

The copper producer, with operations across the Americas, is experiencing what management describes as an "inflection point" in 2025, with substantial production growth and cost reductions driving improved financial performance. The company’s presentation emphasized its transformation toward becoming a 400,000-tonne annual copper producer through expansion projects at existing operations and development of new assets.

Quarterly Performance Highlights

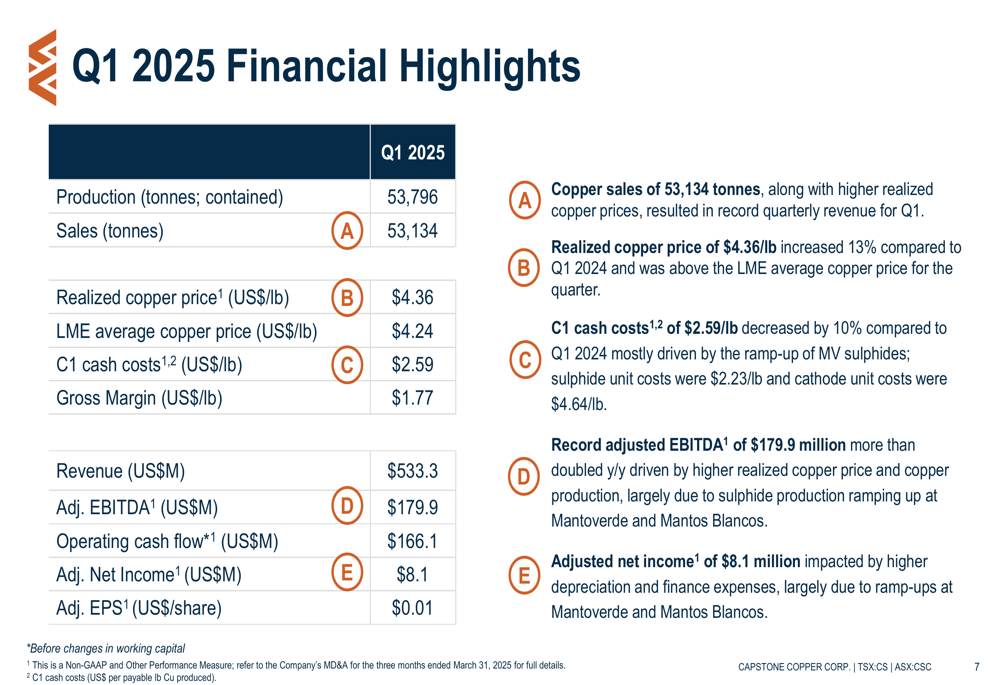

Capstone reported consolidated copper production of 53,796 tonnes for Q1 2025, consisting of 45,950 tonnes from sulphide operations and 7,846 tonnes from cathode production. The company achieved record quarterly revenue on copper sales of 53,134 tonnes, benefiting from a realized copper price of $4.36/lb, representing a 13% increase year-over-year.

As shown in the following financial highlights chart, the company’s adjusted EBITDA more than doubled year-over-year to $179.9 million, while C1 cash costs decreased 10% to $2.59/lb:

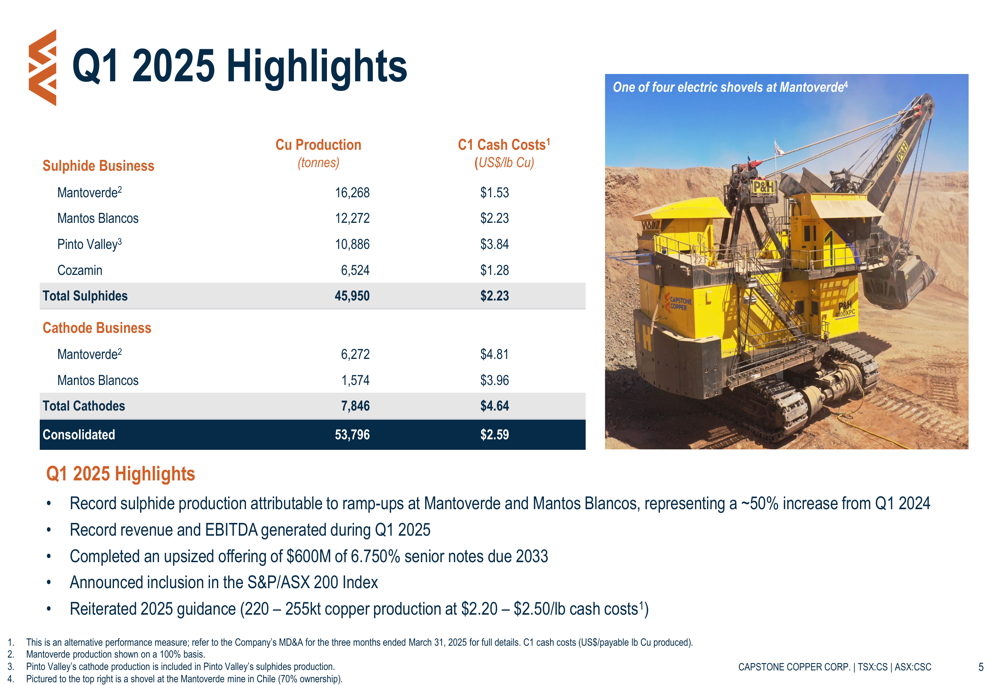

The company’s performance was driven by strong operational results across its portfolio, with particular strength at its Mantoverde operation in Chile, which produced 16,268 tonnes of copper from sulphides and 6,272 tonnes from cathodes. Mantos Blancos contributed 12,272 tonnes from sulphides and 1,574 tonnes from cathodes, while Pinto Valley and Cozamin added 10,886 tonnes and 6,524 tonnes respectively.

The following table summarizes the Q1 2025 production and cost performance across Capstone’s operations:

Detailed Financial Analysis

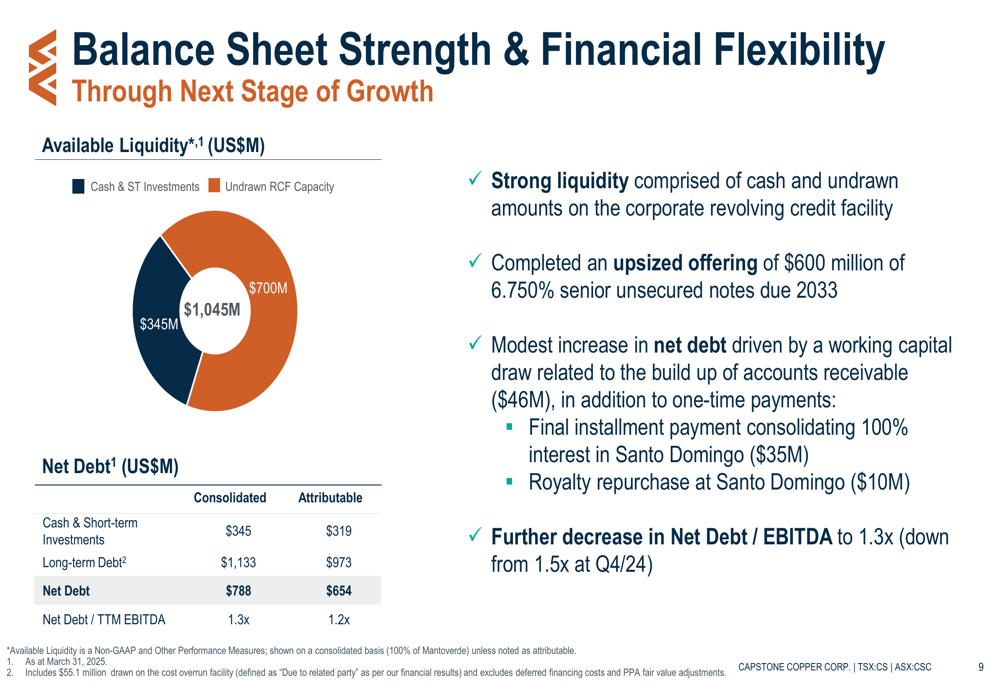

Capstone maintained a strong balance sheet with available liquidity of $1,045 million as of Q1 2025, including $345 million in cash and short-term investments and $700 million in undrawn revolving credit facility capacity. The company reported consolidated net debt of $788 million, resulting in a net debt to trailing twelve-month EBITDA ratio of 1.3x.

During the quarter, Capstone completed a $600 million senior unsecured notes offering with a 6.750% coupon maturing in March 2033. The company plans to use these proceeds to refinance the Mantoverde Project Facility in Q2 2025, as illustrated in the following capital structure overview:

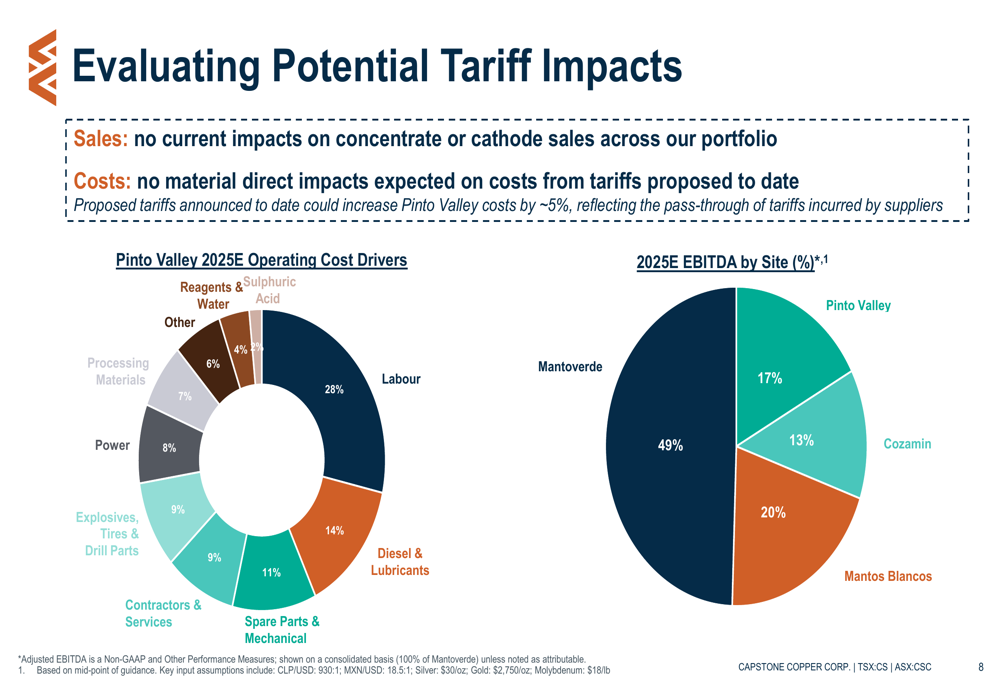

The company is also evaluating potential tariff impacts on its operations, particularly at Pinto Valley in Arizona, where proposed tariffs could increase costs by approximately 5%. However, management noted that Pinto Valley represents only 17% of the company’s expected 2025 EBITDA, with the majority coming from its Chilean operations:

Strategic Growth Initiatives

Capstone’s presentation emphasized 2025 as a transformational year, with production expected to increase 29% from 184,000 tonnes in 2024 to 220,000-255,000 tonnes in 2025. Simultaneously, consolidated C1 cash costs are projected to decrease 15% from approximately $2.77/lb in 2024 to $2.20-$2.50/lb in 2025.

The company’s growth trajectory is clearly illustrated in the following chart, showing the path to becoming a 400,000-tonne producer through the Mantoverde-Oxides (MV-O) project and Santo Domingo development:

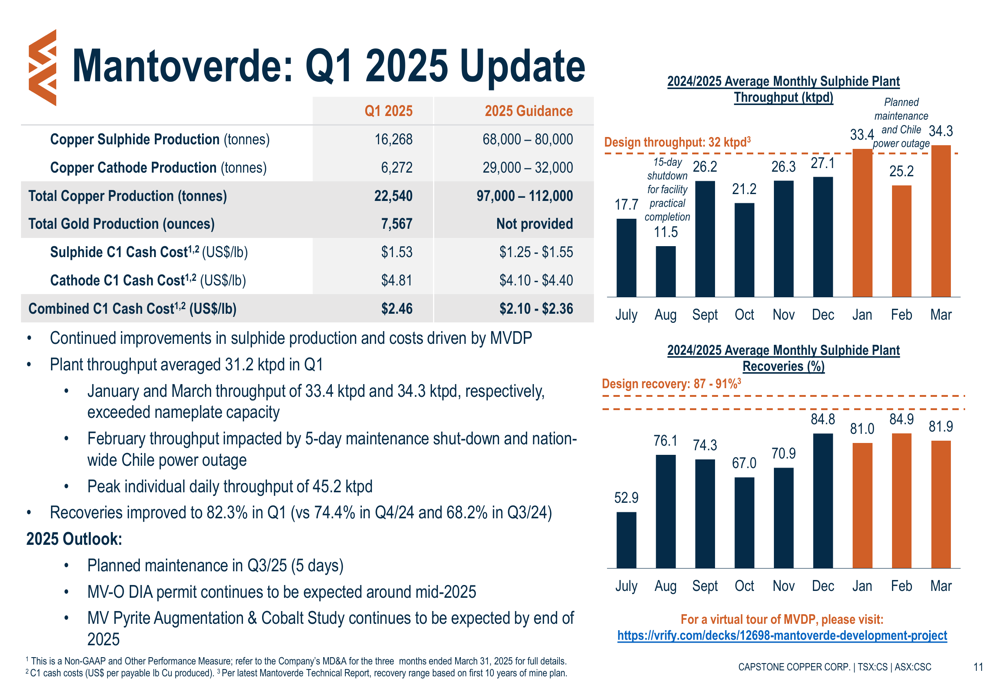

At Mantoverde, the company reported improving operational performance with plant throughput averaging 31.2 ktpd in Q1 2025, with individual daily peaks of 45.2 ktpd. Recoveries also improved to 82.3% during the quarter, as shown in the following operational update:

For the Santo Domingo project, Capstone outlined its development strategy focused on securing a potential joint venture partner, arranging approximately $1.2 billion in project financing, and optimizing infrastructure. Management indicated they are monitoring copper price trends and inflation as they advance the project.

Forward-Looking Statements

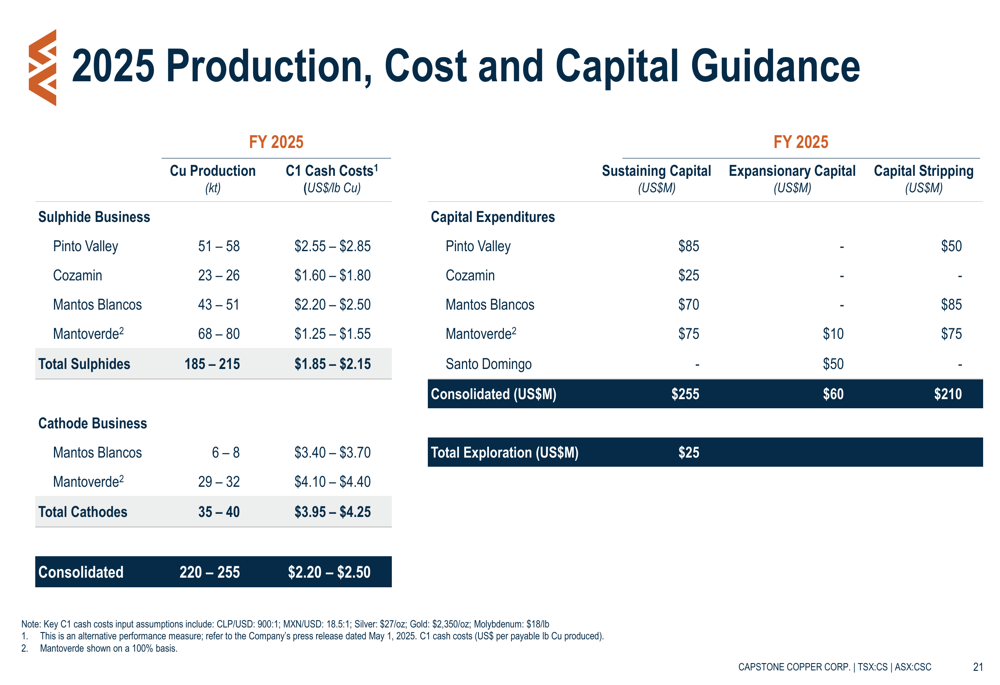

Capstone reiterated its 2025 guidance of 220,000-255,000 tonnes of copper production at C1 cash costs of $2.20-$2.50/lb. The company provided a detailed breakdown of production and cost expectations by operation:

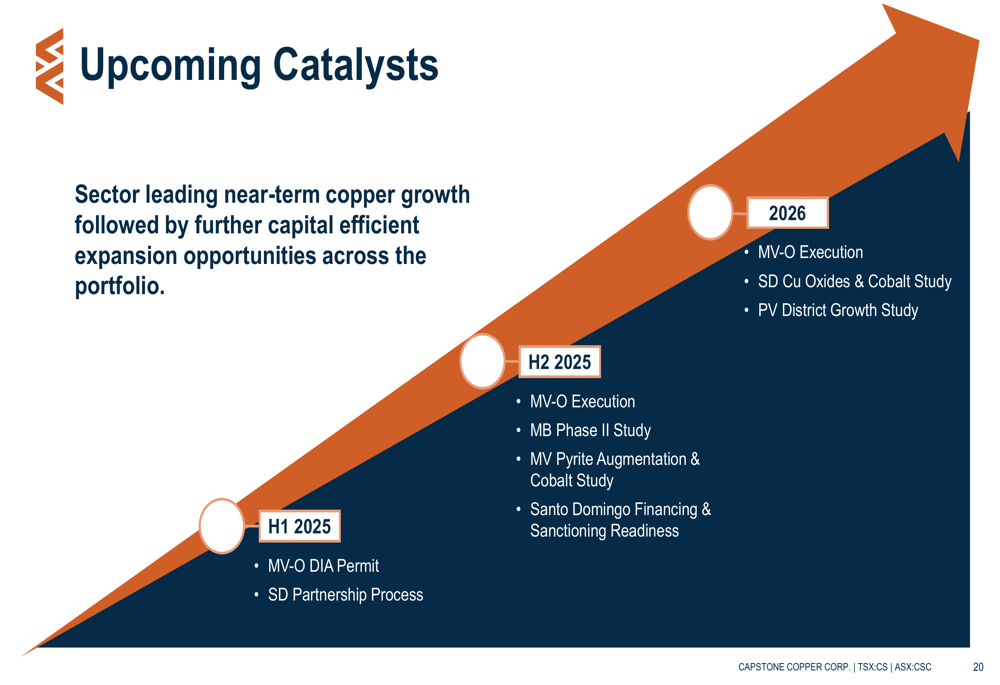

Management highlighted several upcoming catalysts for 2025-2026, including permitting for MV-O, advancement of the Santo Domingo partnership process and financing, and completion of various growth studies:

The company also emphasized its sustainability initiatives, including the adoption of a Water Stewardship Policy, securing a 35-year water agreement for Mantos Blancos, and achieving 50% conformance with the Global Industry Standard on Tailings Management. Capstone reported that 100% of electricity at Mantoverde and Mantos Blancos now comes from renewable sources, and solar panels have been installed at Pinto Valley.

With copper prices remaining strong and the company’s growth projects advancing, Capstone appears well-positioned to deliver on its transformation into a larger, lower-cost copper producer with operations in top-tier jurisdictions across the Americas.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.