Fannie Mae, Freddie Mac shares tumble after conservatorship comments

Introduction & Market Context

CareDx, Inc. (NASDAQ:CDNA), a leading transplant diagnostics company, presented its Q1 2025 financial results on April 30, 2025, highlighting continued growth across all business segments. Despite the positive financial results, CareDx’s stock declined 7.06% during the regular trading session, closing at $16.88, with a slight additional decline of 0.47% in after-hours trading.

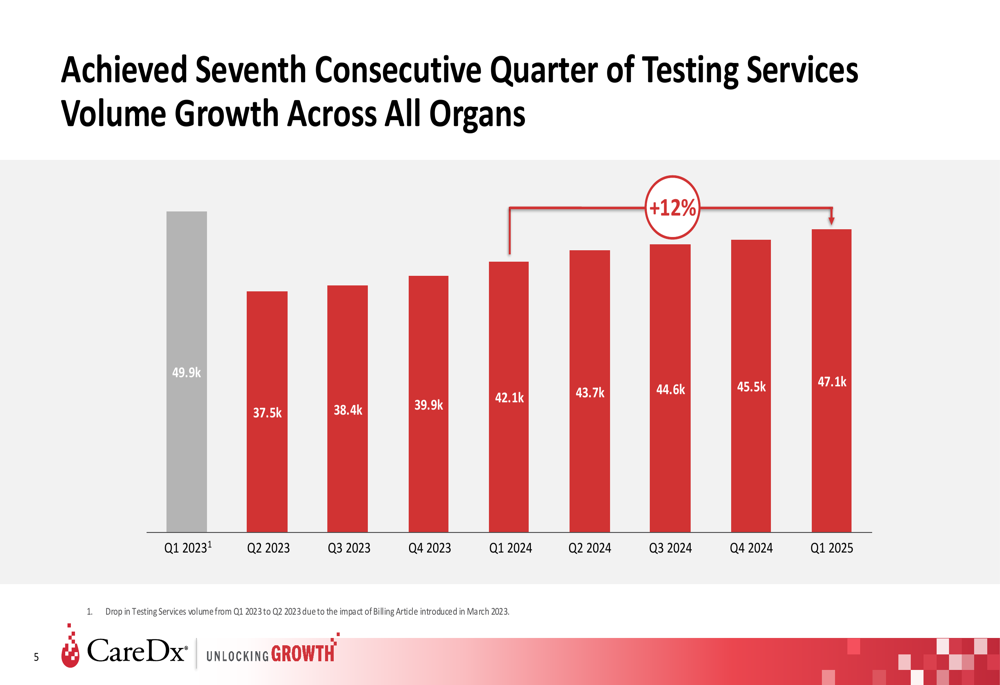

The company’s presentation emphasized its seventh consecutive quarter of testing services volume growth, maintaining the positive momentum seen in its Q4 2024 results when it reported a surprising EPS of $0.18 against forecasted losses.

Quarterly Performance Highlights

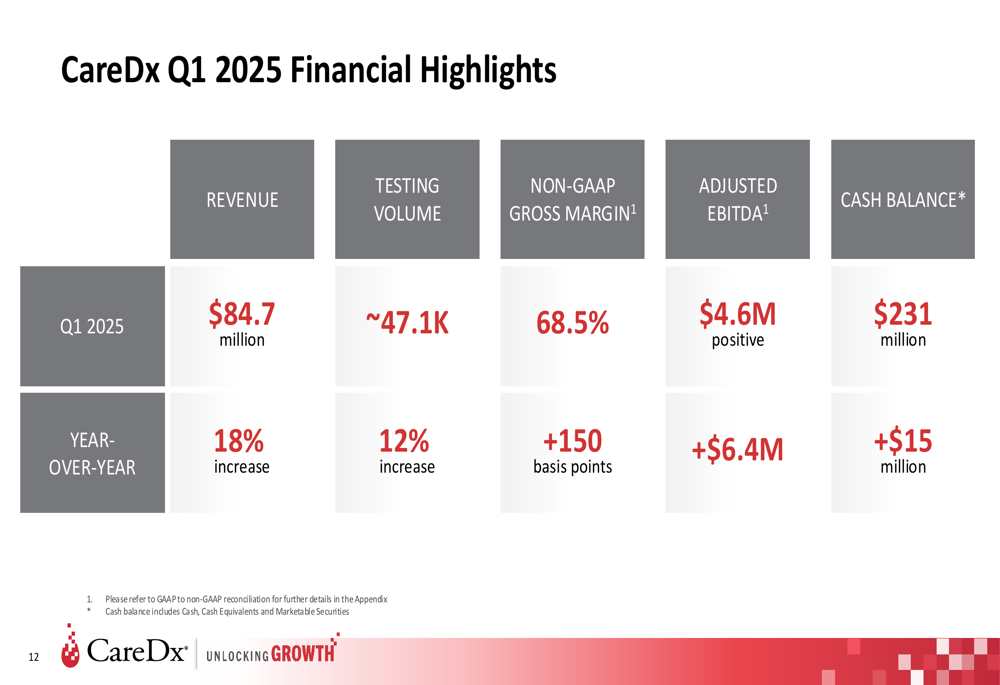

CareDx reported total revenue of $84.7 million for Q1 2025, representing an 18% increase year-over-year. The company delivered approximately 47,100 tests during the quarter, a 12% increase compared to Q1 2024.

As shown in the following chart of quarterly testing services volume growth:

The company has maintained consistent growth in testing volume since Q2 2023, when volumes were impacted by the introduction of a new Billing Article. This steady recovery demonstrates CareDx’s ability to navigate regulatory challenges while expanding its testing services.

The financial highlights for Q1 2025 show improvement across key metrics:

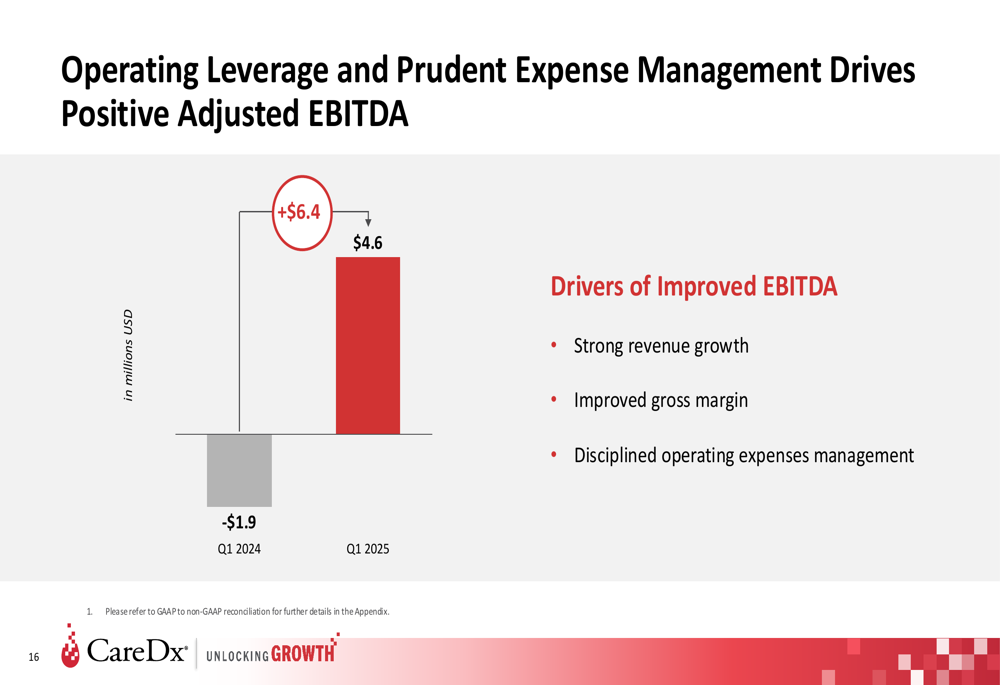

CareDx achieved a non-GAAP gross margin of 68.5%, representing a 150 basis point improvement year-over-year. The company also reported positive adjusted EBITDA of $4.6 million, a significant improvement from the negative $1.9 million reported in Q1 2024.

Detailed Financial Analysis

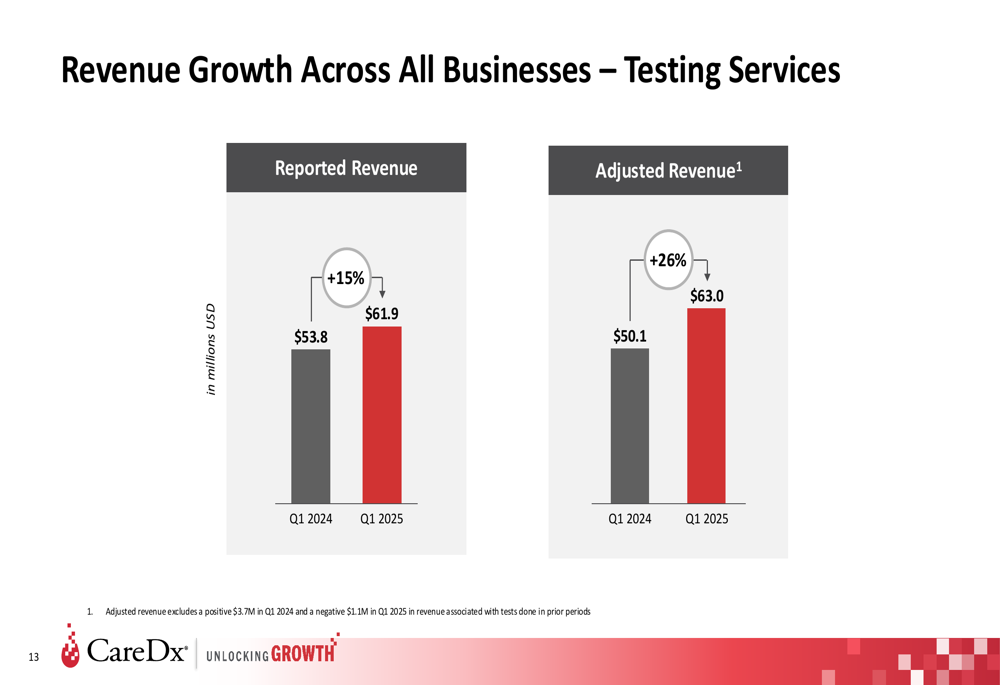

Revenue growth was consistent across all business segments. Testing Services, which represents the largest portion of CareDx’s revenue, grew by 15% on a reported basis and 26% on an adjusted basis:

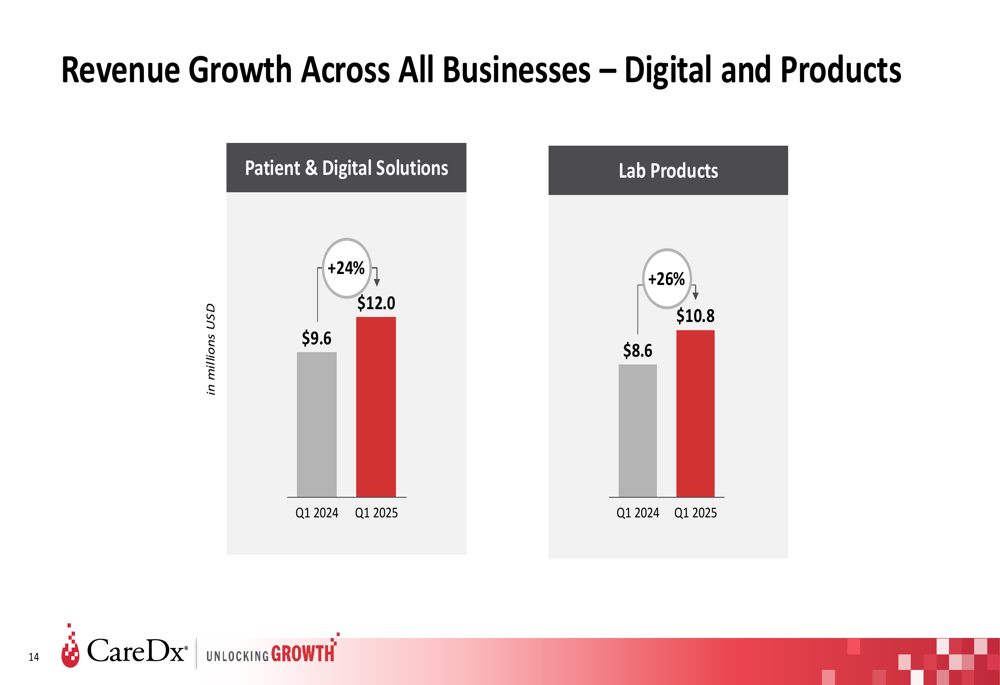

The company’s Patient & Digital Solutions segment saw 24% growth, while Lab Products increased by 26% compared to Q1 2024:

One of the most significant improvements was in adjusted EBITDA, which turned positive at $4.6 million compared to negative $1.9 million in Q1 2024:

This $6.4 million improvement in adjusted EBITDA was driven by strong revenue growth, improved gross margins, and disciplined operating expense management, according to the company.

Despite these positive results, CareDx reported a GAAP net loss of $10.4 million for the quarter, which contrasts with the positive EPS of $0.18 reported in Q4 2024. The company maintained a strong cash position of $231 million with no debt, though this represents a decrease from the $261 million reported at the end of 2024.

Strategic Initiatives & Product Pipeline

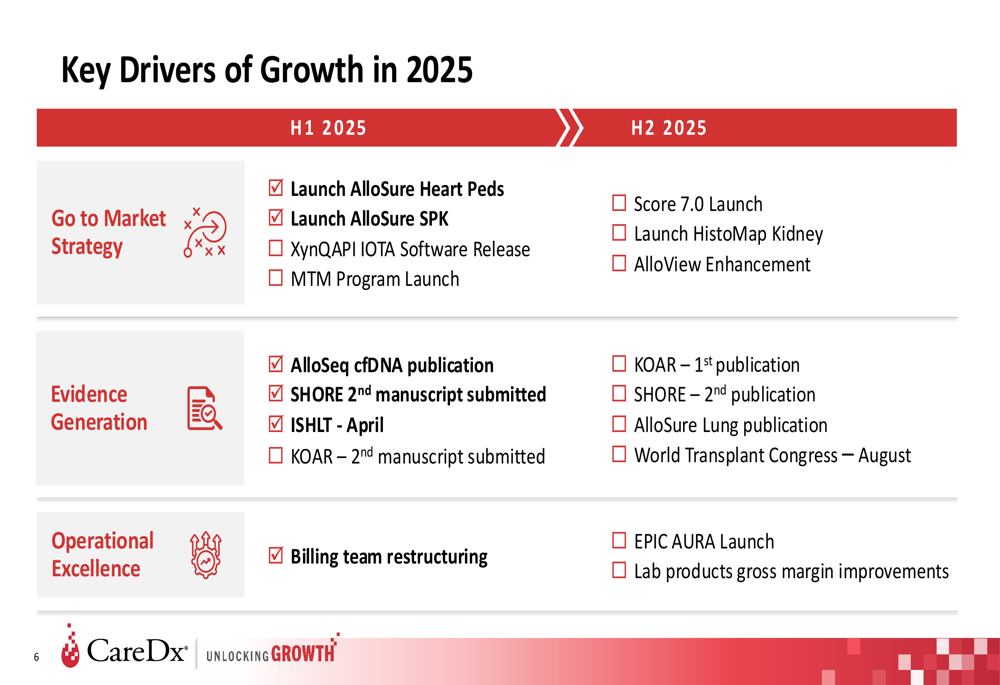

CareDx outlined its key growth drivers for 2025, which include several product launches and operational improvements:

The company plans to launch AlloSure Heart for pediatric patients and AlloSure SPK (simultaneous pancreas-kidney transplant) in the first half of 2025, followed by Score 7.0 and HistoMap Kidney in the second half. These launches align with the company’s long-term strategy of expanding its transplant diagnostic solutions across multiple organs.

CareDx also highlighted its expanded commercial coverage, adding 3.5 million commercial lives for AlloMap Heart and 15.5 million new commercial covered lives for AlloSure, strengthening its market position.

Clinical Evidence & Product Value

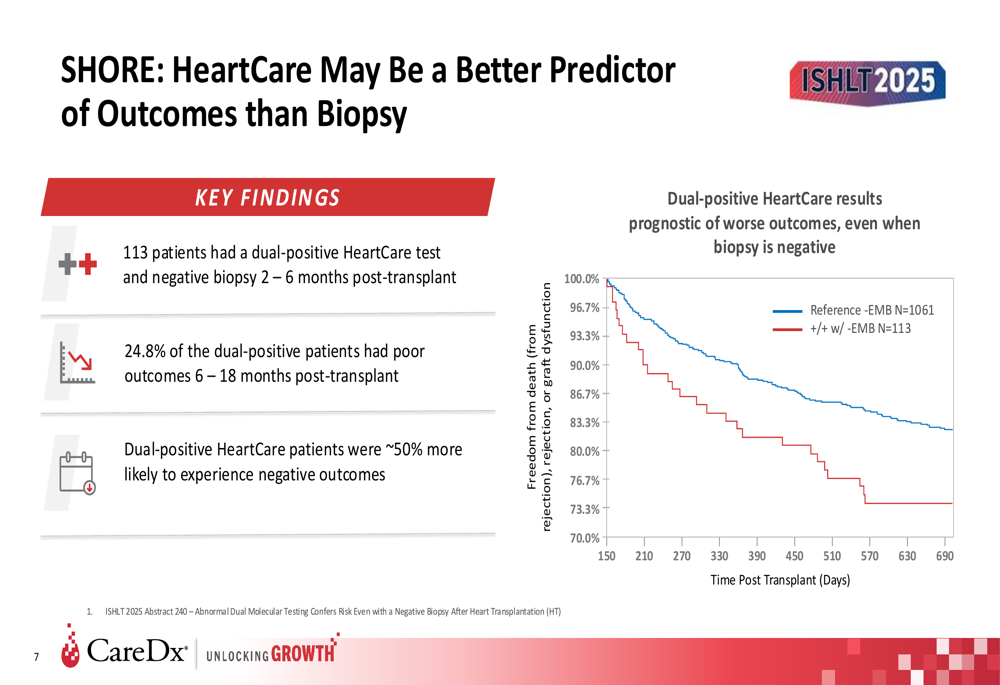

The presentation emphasized clinical evidence supporting the value of CareDx’s diagnostic solutions. The SHORE study (Surveillance HeartCare Outcomes Registry) demonstrated that HeartCare may be a better predictor of outcomes than traditional biopsy:

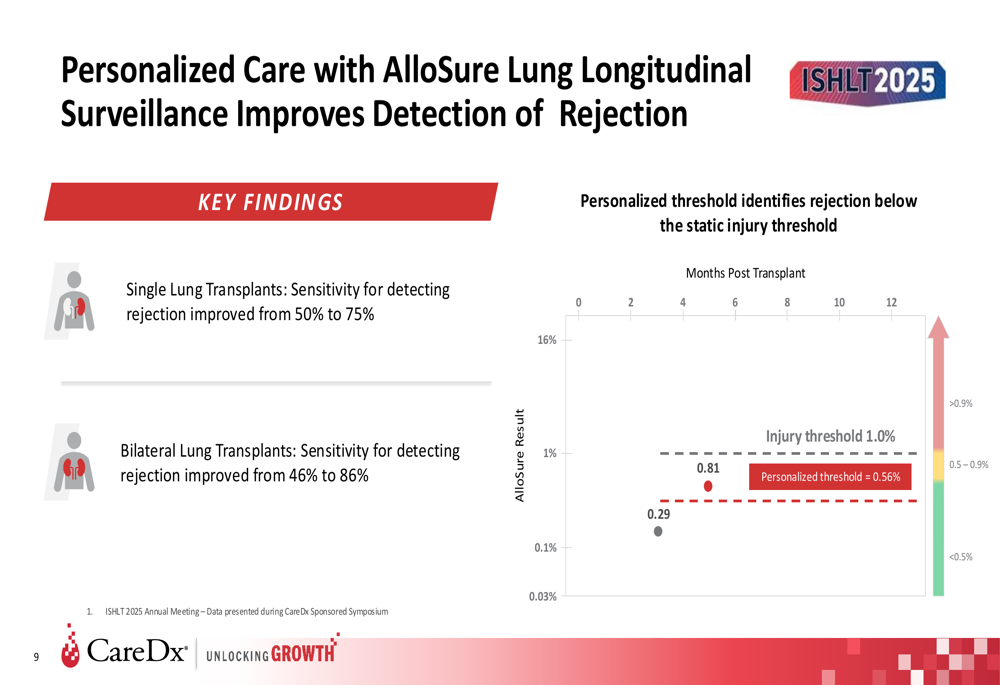

Additionally, the company presented data showing the value of AlloSure Lung in detecting and managing rejection in lung transplant patients:

These clinical findings support CareDx’s value proposition and differentiate its products in the transplant diagnostics market.

Forward-Looking Statements

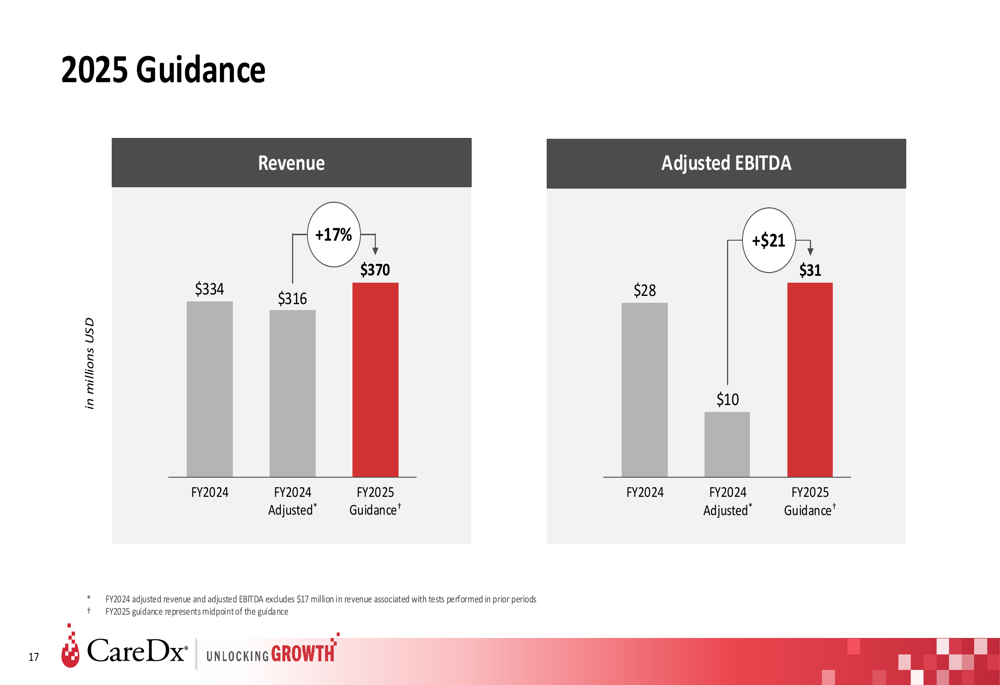

CareDx reaffirmed its full-year 2025 guidance, projecting revenue between $365-375 million, representing approximately 17% growth from adjusted 2024 revenue:

The company expects adjusted EBITDA to reach $29-33 million in 2025, a significant improvement from the adjusted $10 million in 2024. This guidance is based on mid-teens growth in testing volume year-over-year, with an estimated average selling price of approximately $1,360 per test on a blended basis.

CareDx’s continued focus on operational excellence and strategic product launches positions it for sustained growth, though investors will be watching closely to see if the company can translate its revenue growth into consistent profitability. The market’s negative reaction to the Q1 results suggests some investors may have expected even stronger performance or were concerned about the GAAP net loss despite the positive adjusted EBITDA.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.