Caesars Entertainment misses Q2 earnings expectations, shares edge lower

Introduction & Market Context

CarGurus (NASDAQ:CARG) released its Q1 2025 earnings presentation on May 8, 2025, revealing a mixed performance across its business segments. The company’s stock responded positively in aftermarket trading, rising 4.65% to $29.25, suggesting investors were encouraged by the results despite overall revenue challenges.

The automotive marketplace company continues to navigate a complex industry landscape, with its core marketplace business showing resilience while its digital wholesale segment faces ongoing headwinds. This quarter’s results demonstrate CarGurus’ ability to maintain strong margins even as it manages through segment-specific challenges.

Quarterly Performance Highlights

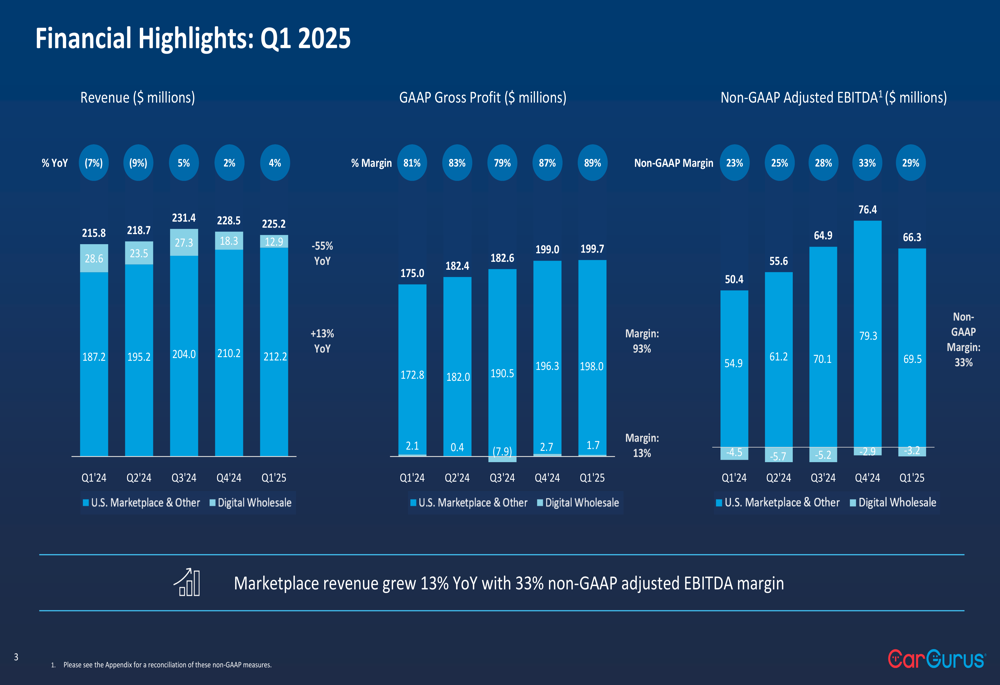

CarGurus reported Q1 2025 revenue of $225.2 million, representing a 55% year-over-year decrease. However, this headline figure masks the divergent performance between segments. The company’s U.S. Marketplace & Other segment generated $212.2 million in revenue, while the Digital Wholesale segment contributed $12.9 million.

As shown in the following financial highlights chart, the company maintained impressive gross profit margins of 89% and a non-GAAP adjusted EBITDA margin of 29%:

The company’s marketplace revenue grew 13% year-over-year with a 33% non-GAAP adjusted EBITDA margin, demonstrating the strength of CarGurus’ core business. This growth was driven by both an expanding dealer base and increasing revenue per dealer.

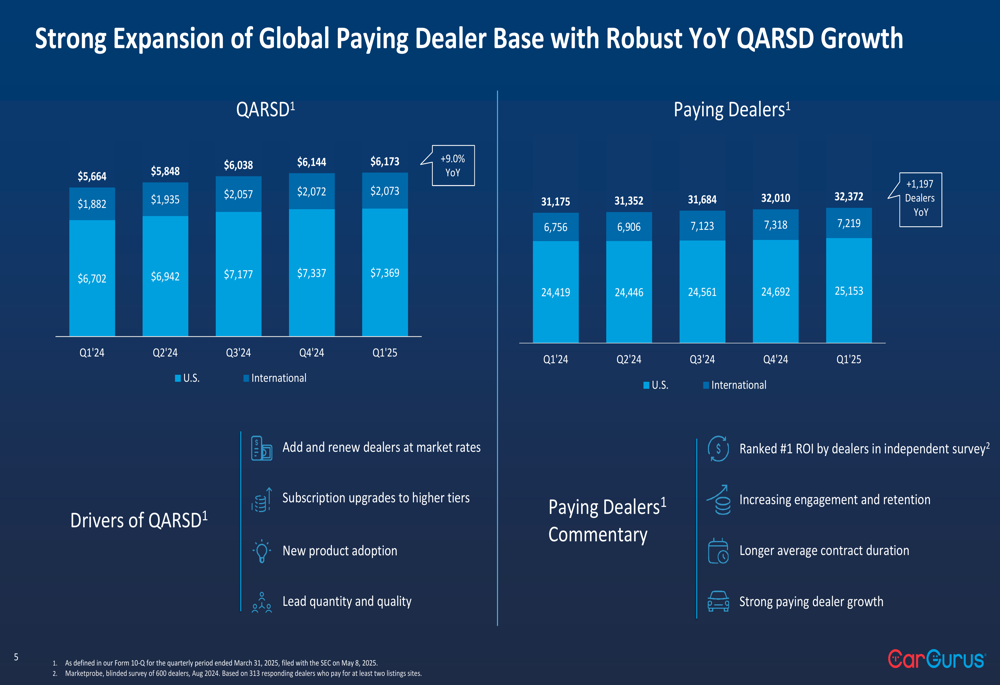

CarGurus’ global paying dealer count reached 32,372, representing a year-over-year increase of 1,197 dealers. Quarterly Average Revenue per Subscribing Dealer (QARSD) grew to $9,442, up 9.0% from the previous year. This growth was particularly strong in the U.S. market, where QARSD reached $7,369.

The following chart illustrates the consistent growth in both dealer count and revenue per dealer:

Detailed Financial Analysis

CarGurus’ financial performance reveals a tale of two segments, with the Marketplace business thriving while the Digital Wholesale segment continues to face challenges.

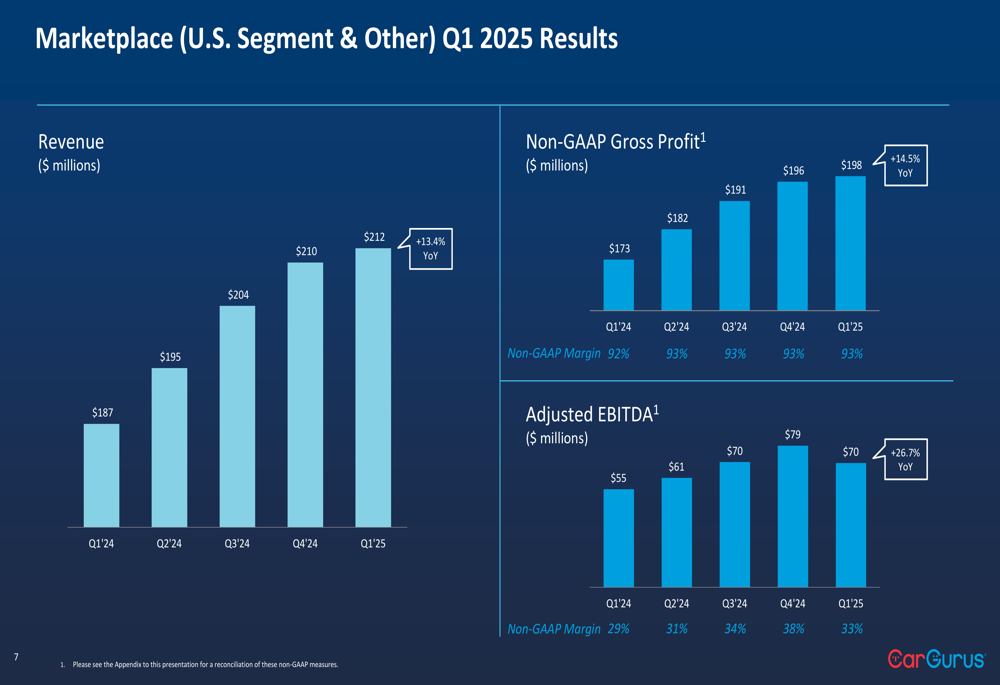

The U.S. Marketplace & Other segment delivered Q1 2025 revenue of $210 million, representing a 13.4% year-over-year increase. This segment maintained an impressive non-GAAP gross profit margin of 93% and generated adjusted EBITDA of $70 million, up 26.7% year-over-year with a 33% margin.

The following chart details the consistent growth trajectory of the Marketplace segment:

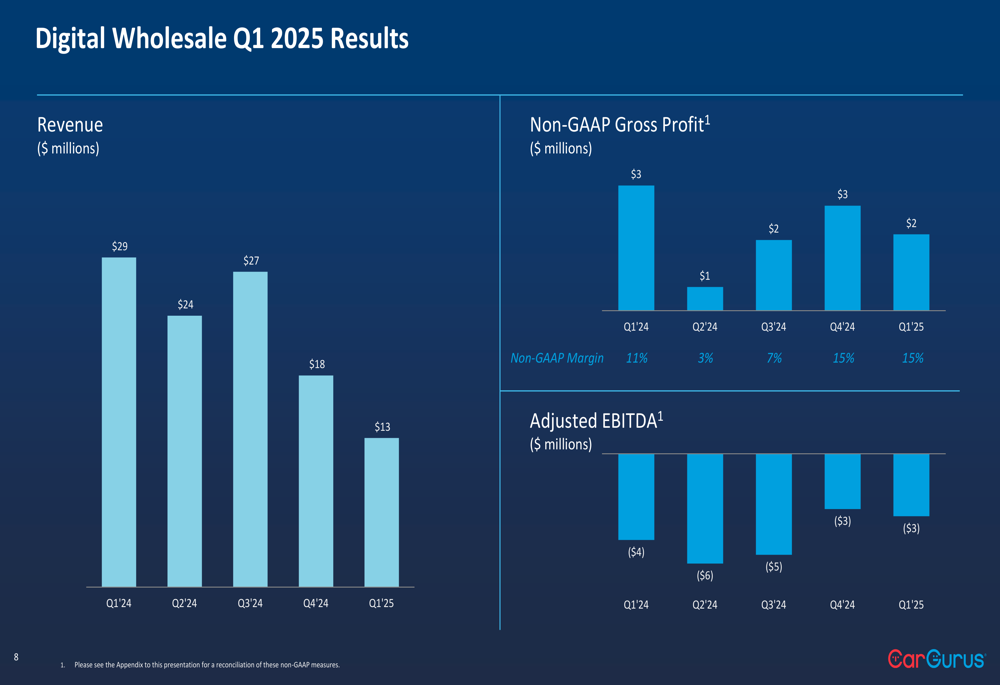

In contrast, the Digital Wholesale segment saw revenue decline to $13 million in Q1 2025 from $29 million in Q1 2024. While the segment maintained a 15% non-GAAP gross profit margin, it continued to generate adjusted EBITDA losses of $3 million, though this represents an improvement from the $6 million loss in the same period last year.

The Digital Wholesale segment’s performance is reflected in the following chart:

The decline in Digital Wholesale performance is further illustrated by transaction volume metrics, with Gross Merchandise Sales falling to $115 million in Q1 2025 from $250 million in Q1 2024, and total transactions dropping to 5,209 from 10,302 in the same period.

Competitive Industry Position

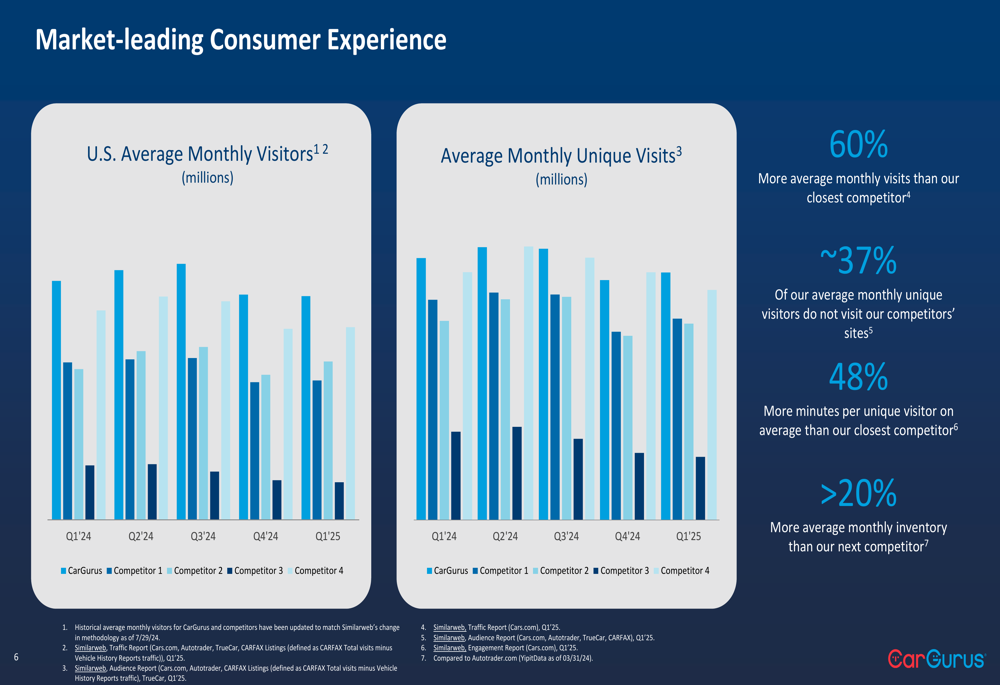

Despite challenges in the Digital Wholesale segment, CarGurus continues to maintain a dominant position in the automotive marketplace industry. The company reports significant advantages over competitors in terms of traffic and engagement metrics.

According to the presentation, CarGurus has 60% more average monthly visits than its closest competitor and approximately 37% of its average monthly unique visitors do not visit competitors’ sites. Additionally, users spend 48% more minutes per unique visitor on average than on the closest competitor’s site, and the platform offers over 20% more average monthly inventory than its next competitor.

The following chart illustrates CarGurus’ market-leading consumer experience metrics:

The company highlighted several strategic initiatives aimed at strengthening its competitive position. These include expanding its suite of data-driven dealer solutions, with 17,000 global dealers using its Next (LON:NXT) Best Deal Rating and 74% taking action on pricing recommendations. CarGurus also launched conversational AI search, with users who engage spending twice as much time on the site.

Additionally, the company’s Digital Deal feature is now available with over 11,000 dealers and nearly 1 million vehicle listings enabled. Digital Deal now accounts for over 25% of a dealer’s email leads, demonstrating growing adoption of CarGurus’ transaction-enabling technology.

Forward-Looking Statements

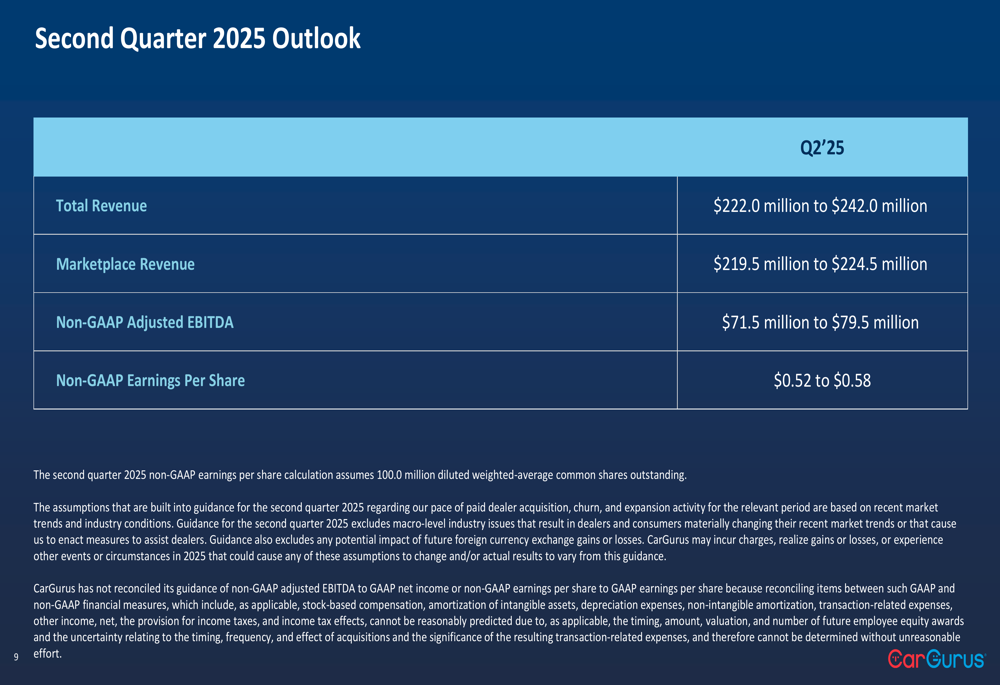

Looking ahead to Q2 2025, CarGurus provided guidance for total revenue between $222.0 million and $242.0 million, with marketplace revenue expected to be between $219.5 million and $224.5 million. The company projects non-GAAP adjusted EBITDA between $71.5 million and $79.5 million and non-GAAP earnings per share between $0.52 and $0.58.

The following slide details the company’s Q2 2025 outlook:

This guidance suggests management expects continued strength in the marketplace segment while managing through the challenges in the digital wholesale business. The projected adjusted EBITDA range indicates the company anticipates maintaining strong profitability despite the mixed revenue performance.

CarGurus’ focus on deepening engagement, expanding adoption, and reinforcing market leadership positions it to navigate the evolving automotive marketplace landscape. The company’s continued investment in AI-driven features and transaction-enabling technology demonstrates its commitment to enhancing both the dealer and consumer experience.

While the digital wholesale segment remains challenging, the strong performance of the marketplace business and the company’s healthy margins suggest CarGurus is effectively executing its core strategy while working to address underperforming segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.