Asia FX muted, dollar fragile as CPI data boosts Sept rate cut bets

Introduction & Market Context

CarGurus (NASDAQ:CARG) presented its second quarter 2025 earnings results on August 7, showing continued revenue growth despite mixed performance across business segments. The online automotive marketplace reported a 7% year-over-year increase in total revenue, reaching $234 million, while maintaining strong profitability metrics.

The company’s stock closed at $31.41 prior to the earnings release, representing a position well above its 52-week low of $24.65 but still below its high of $41.33. CarGurus continues to position itself as a market leader in the online automotive space, claiming significantly higher traffic and engagement metrics than competitors.

Quarterly Performance Highlights

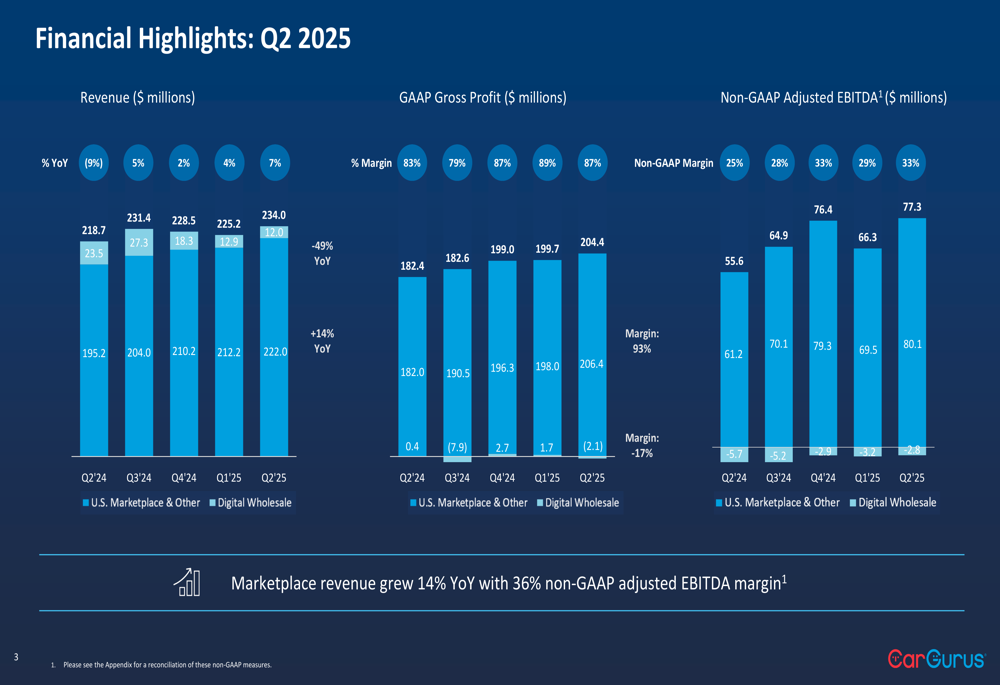

CarGurus reported total revenue of $234 million for Q2 2025, a 7% increase compared to the same period last year. This growth was primarily driven by the company’s marketplace segment, which grew 14% year-over-year, while the digital wholesale segment continued to decline.

As shown in the following chart of quarterly financial performance:

The company maintained strong profitability with GAAP gross profit of $204.4 million (87% margin) and non-GAAP adjusted EBITDA of $77.3 million (33% margin). These results demonstrate CarGurus’ ability to grow revenue while maintaining healthy margins, particularly in its core marketplace business.

Detailed Financial Analysis

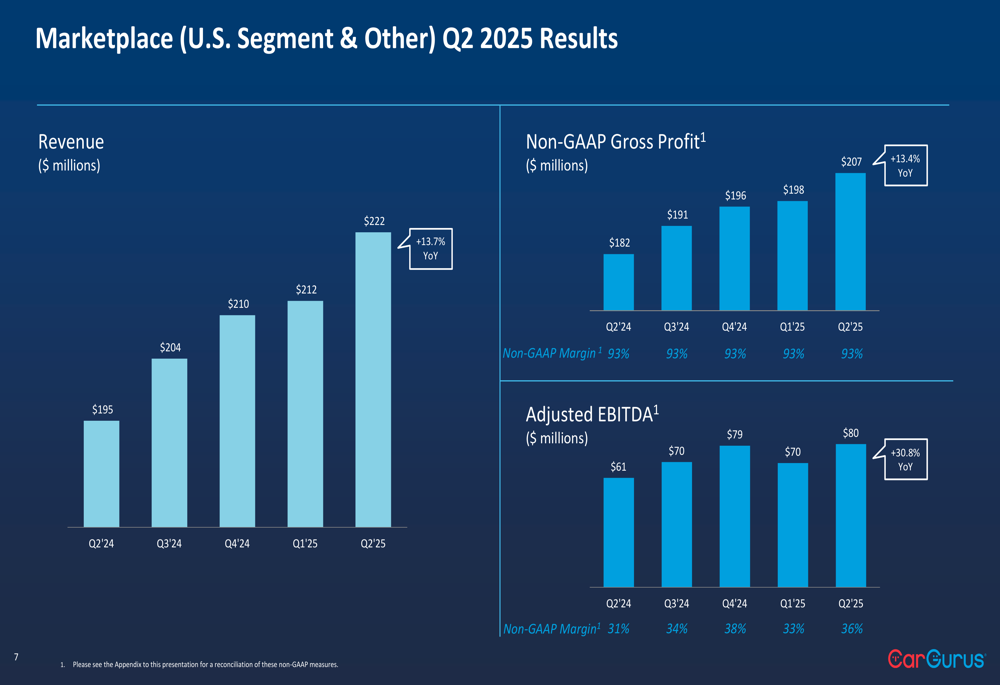

CarGurus’ financial performance reveals a tale of two segments. The marketplace business, which includes the U.S. marketplace segment and other operations, continues to show robust growth and profitability.

The marketplace segment’s financial metrics illustrate this strength:

Marketplace revenue reached $222 million in Q2 2025, representing a 13.7% increase year-over-year. This segment maintained an impressive 93% non-GAAP gross profit margin and generated $80 million in adjusted EBITDA, a 30.8% increase from Q2 2024.

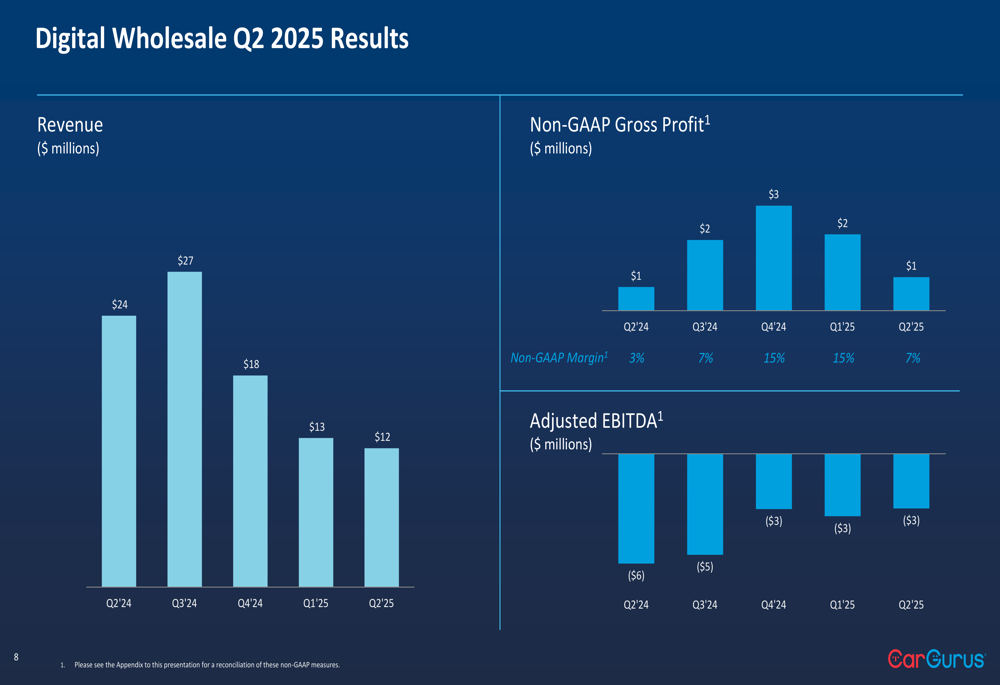

In contrast, the digital wholesale segment continues to struggle:

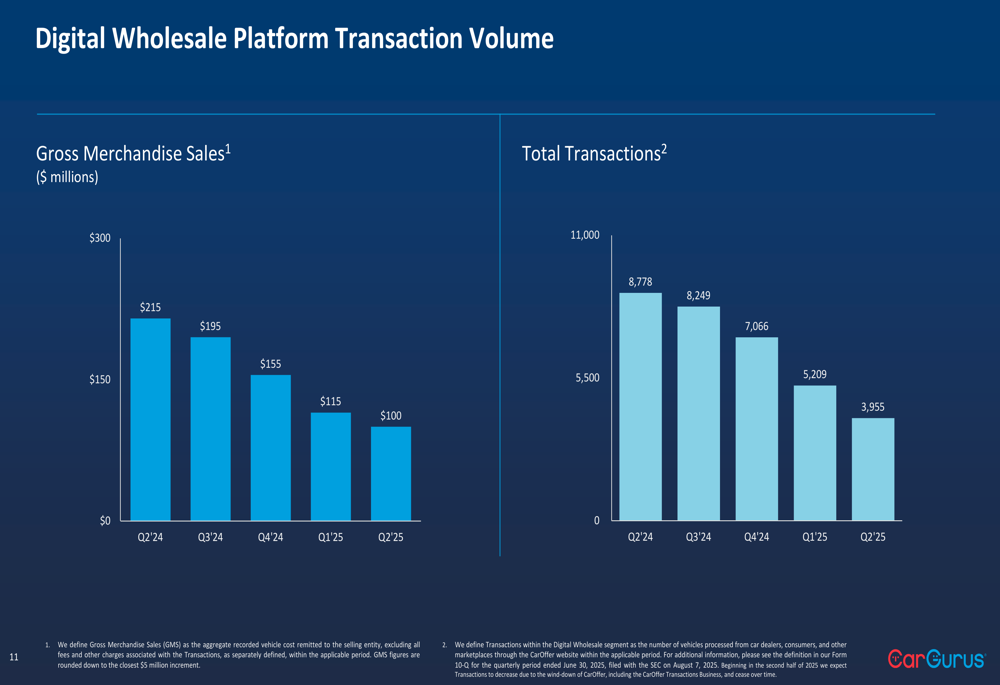

Digital wholesale revenue declined to $12 million in Q2 2025 from $24 million in Q2 2024, with adjusted EBITDA remaining negative at -$3 million, though improved from -$6 million a year ago. The transaction volume in this segment has been steadily declining:

Strategic Initiatives

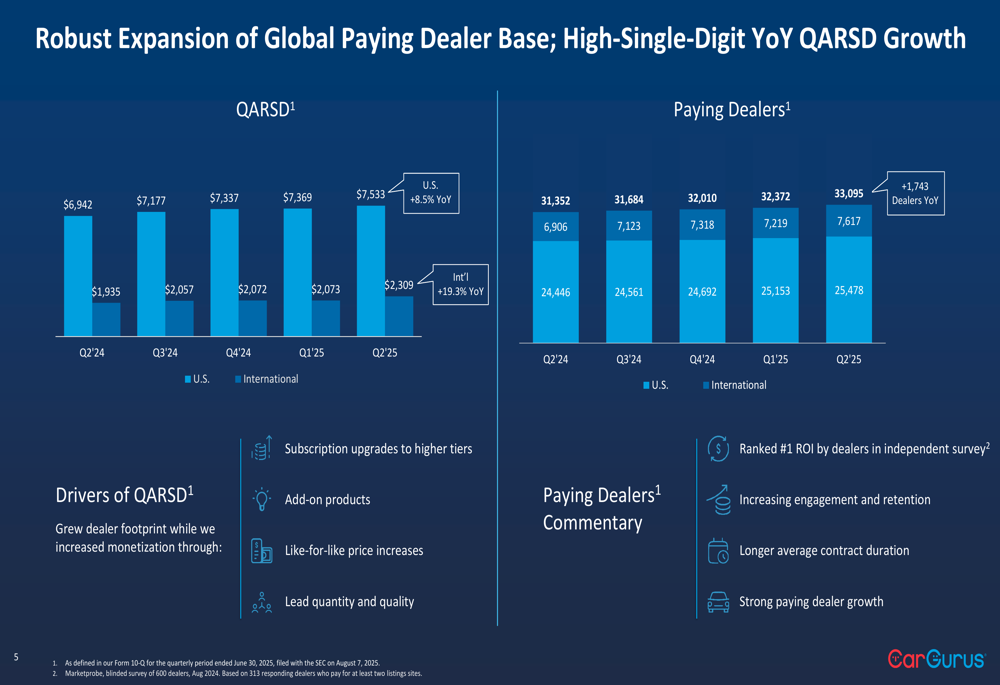

CarGurus’ strategy focuses on expanding its dealer network while increasing revenue per dealer. The company reported significant growth in both metrics during Q2 2025:

The global paying dealer base expanded to 33,095, adding 1,743 dealers year-over-year. Simultaneously, the company increased its quarterly average revenue per subscription dealer (QARSD) to $7,533 in the U.S. (+8.5% YoY) and $2,309 internationally (+19.3% YoY).

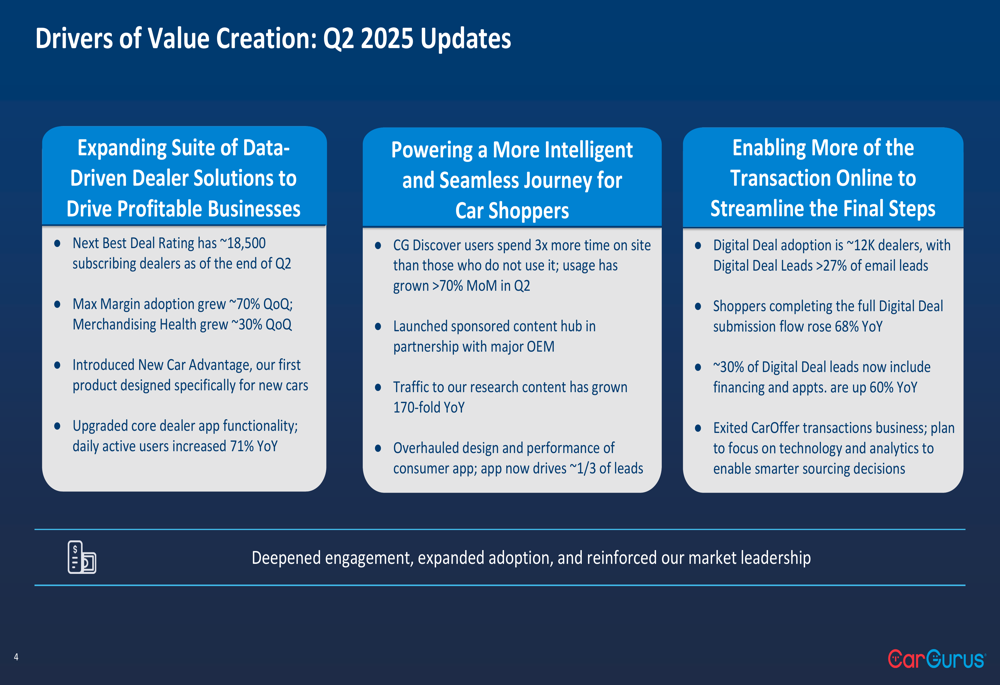

The company is driving value through three key strategic initiatives:

CarGurus is expanding its suite of data-driven dealer solutions, with approximately 18,500 dealers subscribing to its Next (LON:NXT) Best Deal Rating product. The company also introduced New Car Advantage, its first product specifically designed for new cars, and reported significant growth in adoption of its Max Margin and Merchandising Health products.

For consumers, CarGurus is enhancing the car shopping experience through features like CG Discover, which has shown strong engagement with users spending three times more time on site. The company has also overhauled its consumer app, which now drives approximately one-third of leads.

On the transaction front, CarGurus has expanded its Digital Deal adoption to approximately 12,000 dealers, with Digital Deal leads representing over 27% of email leads. Notably, the company announced its exit from the CarOffer transactions business to focus on technology and analytics for sourcing decisions.

Forward-Looking Statements

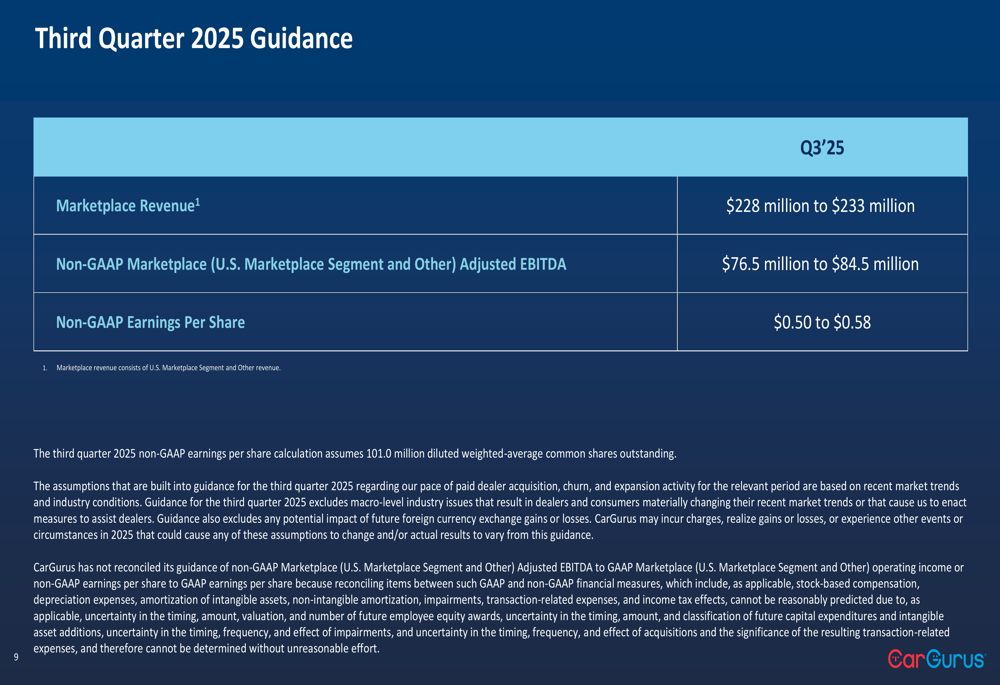

Looking ahead to Q3 2025, CarGurus provided the following guidance:

The company expects marketplace revenue between $228 million and $233 million, with non-GAAP marketplace adjusted EBITDA between $76.5 million and $84.5 million. Non-GAAP earnings per share is projected to be between $0.50 and $0.58, based on 101 million diluted weighted-average common shares outstanding.

This guidance suggests continued growth in the marketplace segment while the company navigates its strategic pivot away from wholesale transactions. The projected earnings per share range represents potential growth from the $0.46 reported in Q1 2025, indicating management’s confidence in the company’s core business despite challenges in the wholesale segment.

CarGurus’ strategic decision to exit the CarOffer transactions business while focusing on technology and analytics aligns with the company’s broader focus on high-margin marketplace operations and data-driven solutions for dealers. This pivot appears designed to address the consistent underperformance of the wholesale segment while capitalizing on the company’s strengths in the marketplace business.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.