ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Carnival Corporation (NYSE:CCL) delivered record-breaking financial results in its third quarter of 2025, according to the company's earnings presentation released on September 29. The cruise operator reported an adjusted net income of $2 billion, exceeding its previous guidance and prompting management to raise its full-year outlook for the third time this year.

Despite the strong performance, Carnival's stock showed volatility following the announcement. Shares initially surged 6.04% to $32.47 in pre-market trading but later reversed course, falling 4.38% to close at $30.62 during the regular session.

Quarterly Performance Highlights

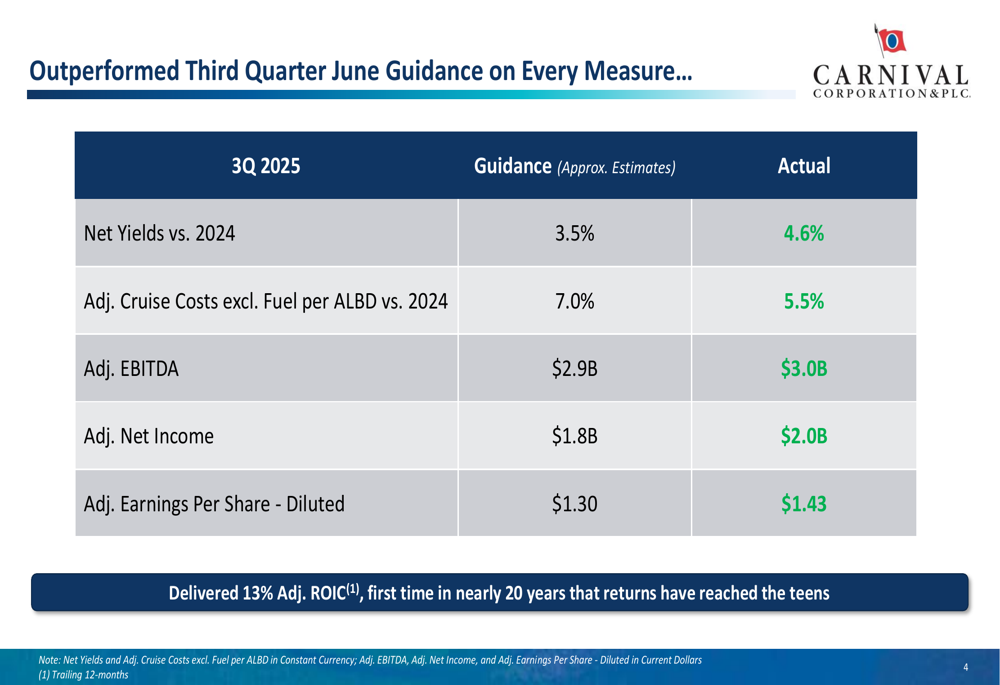

Carnival significantly outperformed its third-quarter guidance across all key metrics. The company achieved record revenues, net yields, adjusted EBITDA, operating income, and customer deposits, all while operating with 2.5% lower capacity than in Q3 2024.

As shown in the following comparison of guidance versus actual results:

Net yields increased by 4.6% compared to the same period in 2024, substantially exceeding the guided 3.5%. The company managed to control costs better than anticipated, with adjusted cruise costs excluding fuel per ALBD rising by 5.5% versus the guided 7.0%.

Adjusted EBITDA reached $3.0 billion, surpassing the $2.9 billion guidance, while adjusted earnings per share hit $1.43, compared to the guided $1.30. Notably, Carnival delivered a 13% adjusted return on invested capital (ROIC), marking the first time in nearly 20 years that returns have reached the teens.

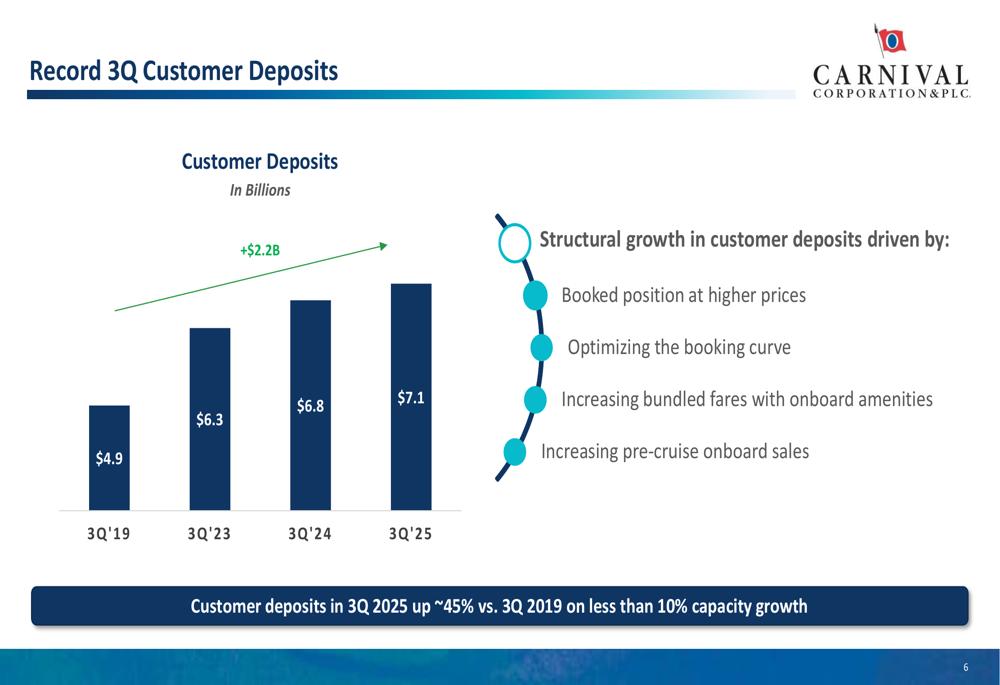

Customer deposits, a key indicator of future demand, reached an all-time high of $7.1 billion in the third quarter, representing a 45% increase compared to Q3 2019 on less than 10% capacity growth.

The following chart illustrates this growth trend:

Strategic Initiatives and Expansion

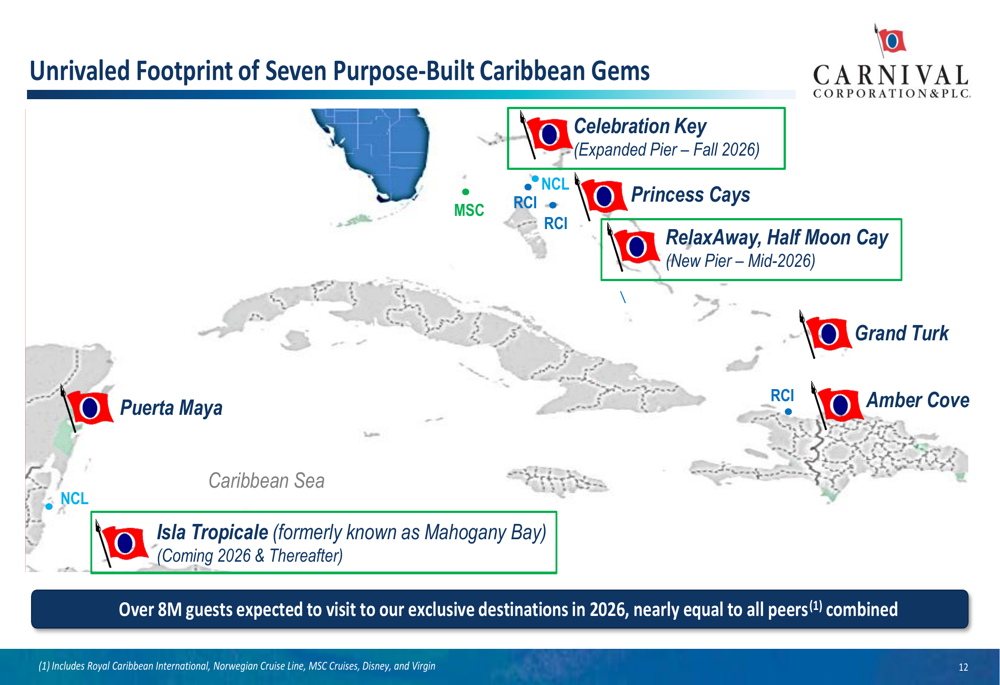

Carnival continues to strengthen its competitive position through strategic investments in exclusive destinations and fleet expansion. The company recently debuted Celebration Key, which opened on time and on budget, and has already welcomed nearly half a million guests with positive feedback.

The company expects nearly 3 million guests to visit Celebration Key in 2026, with a pier extension opening in fall 2026. Additionally, Carnival is enhancing and expanding RelaxAway, Half Moon Cay with a newly constructed pier set to open in mid-2026.

Carnival's Caribbean footprint represents a significant competitive advantage, as illustrated in this map of their exclusive destinations:

In Europe, Carnival maintains a dominant position across major markets. The company holds 60% market share in Germany, 57% in the UK, 43% in Italy, 33% in France, and 32% in Spain, making its brands number one or number two in every established European cruise market.

Debt Reduction and Financial Health

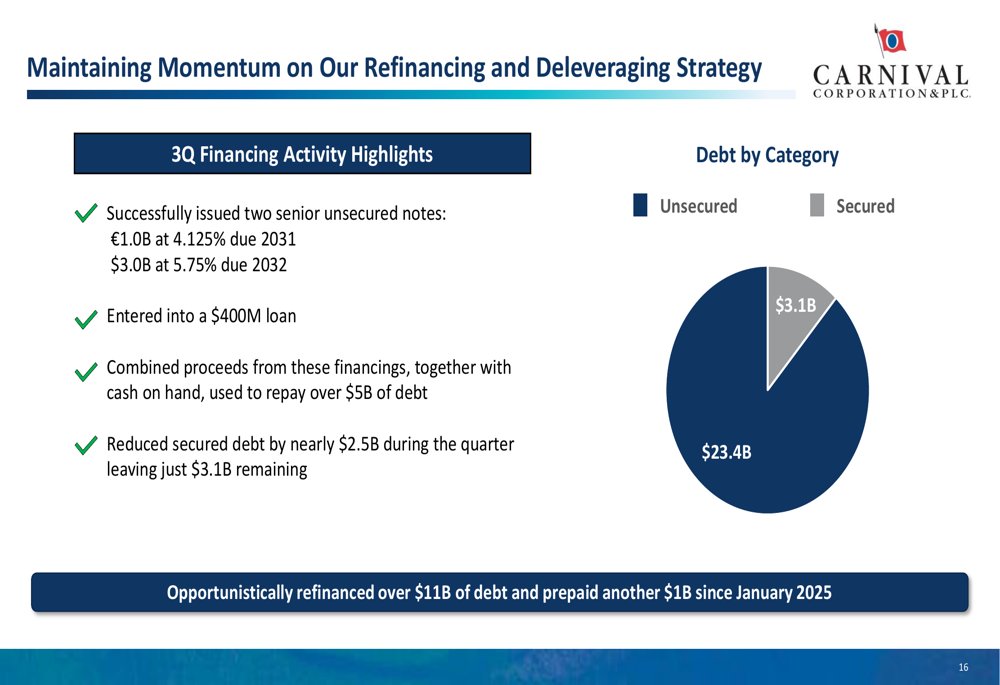

Carnival has made substantial progress in strengthening its balance sheet. During the quarter, the company successfully issued two senior unsecured notes (€1.0B at 4.125% due 2031 and $3.0B at 5.75% due 2032) and entered into a $400 million loan. These proceeds, together with cash on hand, were used to repay over $5 billion of debt.

The company reduced secured debt by nearly $2.5 billion during the quarter, leaving just $3.1 billion remaining, as shown in this breakdown:

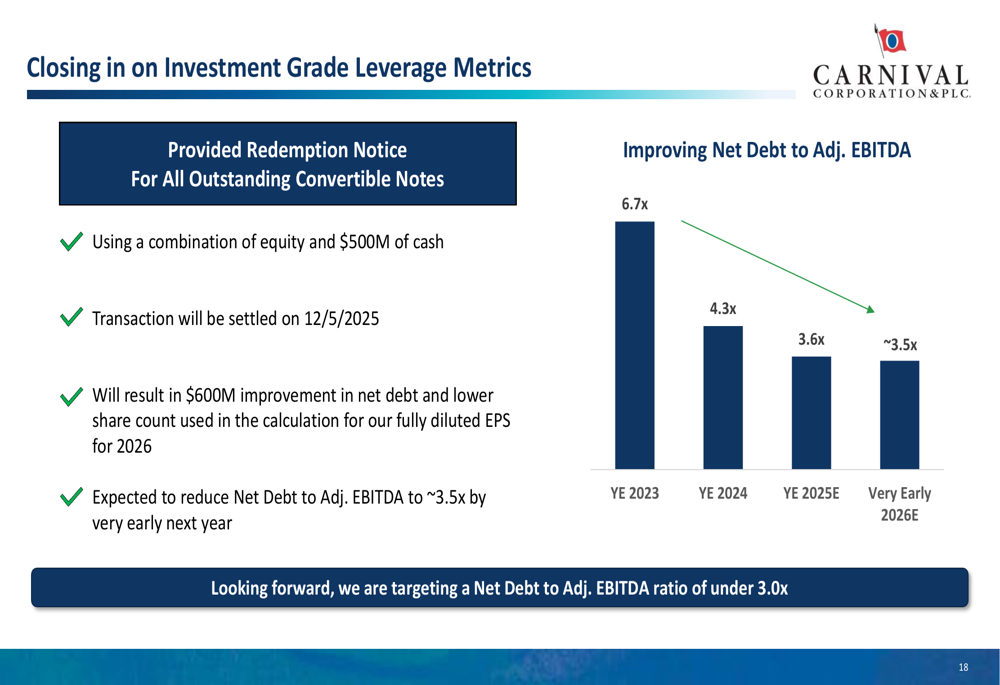

Carnival's credit ratings have seen multiple upgrades from all three major agencies over the past year, bringing the company within one notch of investment grade with S&P and Fitch. The company is also closing in on investment grade leverage metrics, with net debt to adjusted EBITDA expected to reach approximately 3.5x by early 2026.

The following chart shows the consistent improvement in Carnival's leverage ratio:

Forward-Looking Statements

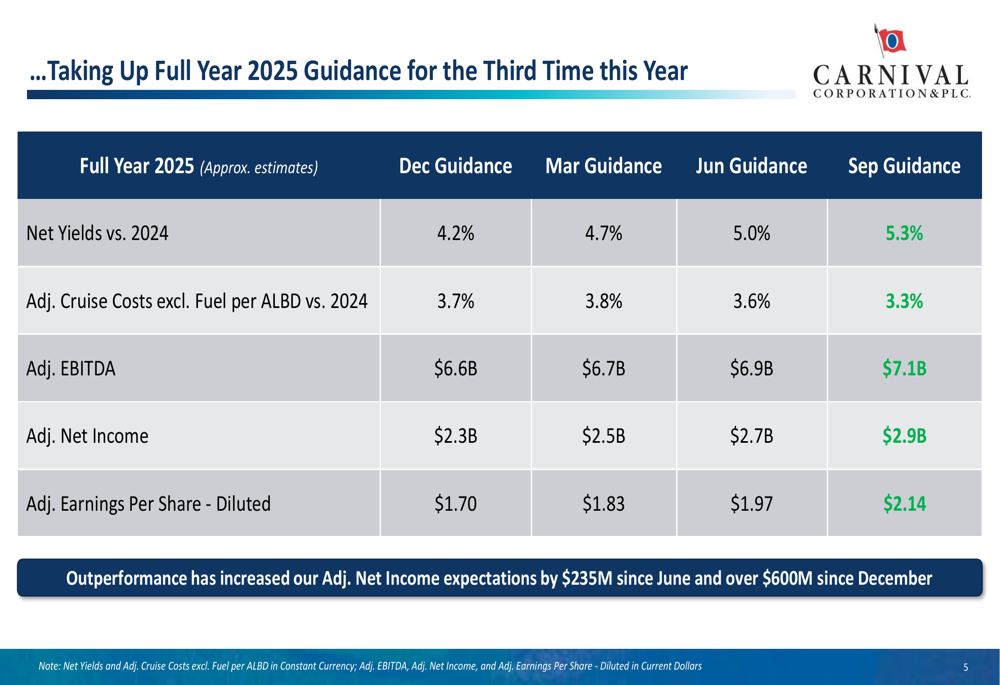

Based on its strong performance, Carnival has raised its full-year 2025 guidance for the third time this year. The company now expects net yields to increase by 5.3% compared to 2024, up from the 5.0% projected in June and 4.2% in December.

The progression of guidance increases throughout the year is illustrated below:

Adjusted EBITDA for the full year is now expected to reach $7.1 billion, with adjusted net income of $2.9 billion and adjusted earnings per share of $2.14. This represents a $235 million increase in adjusted net income expectations since June and over $600 million since December.

Looking ahead to 2026, Carnival reports that nearly half of the year is already booked at historical high prices. The company also noted an "unprecedented start to 2027 with record booking volumes during Q3."

Carnival is maintaining disciplined capacity growth, with only 1-2 ship deliveries expected per year through 2033, focusing on its highest-returning brands. The company is targeting a net debt to adjusted EBITDA ratio of under 3.0x going forward, which would solidify its investment grade metrics.

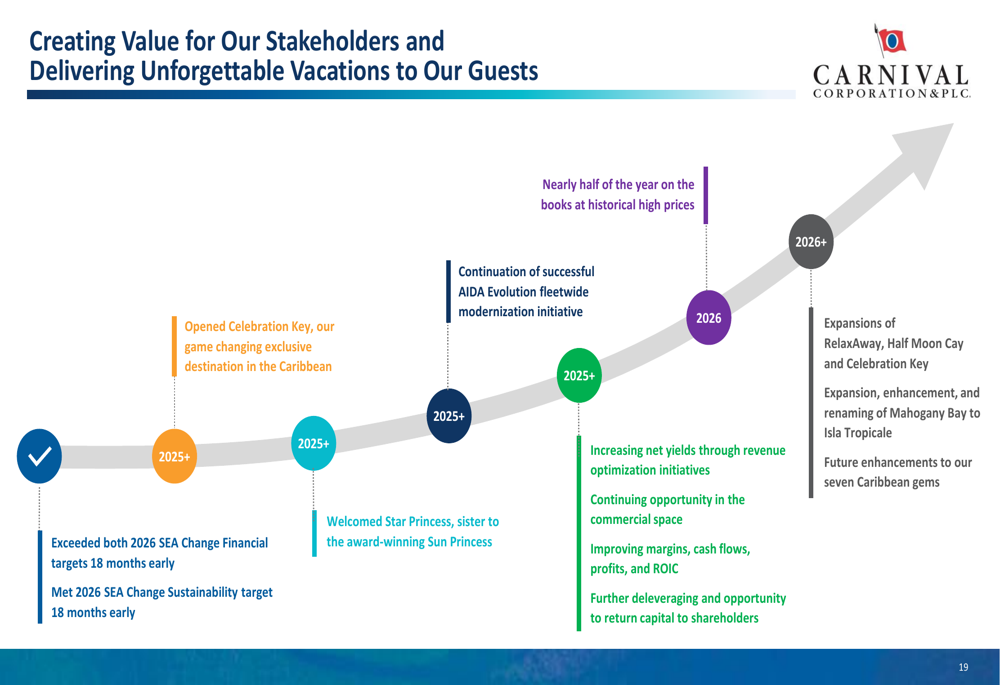

The company's roadmap for creating stakeholder value includes both completed initiatives and future plans:

With record financial results, strong future bookings, strategic destination investments, and significant progress on debt reduction, Carnival appears well-positioned to continue its positive momentum into 2026 and beyond, despite the mixed market reaction to its latest earnings report.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.