TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

Carriage Services Inc (NYSE:CSV), one of only two publicly traded funeral and cemetery services companies in the United States, presented its March 2025 investor presentation highlighting strong financial performance and strategic initiatives under its new management team. The company, with a market capitalization of approximately $625 million as of February 25, 2025, has seen its stock price rise to $48.29 as of August 12, 2025, reflecting positive investor sentiment following recent earnings results.

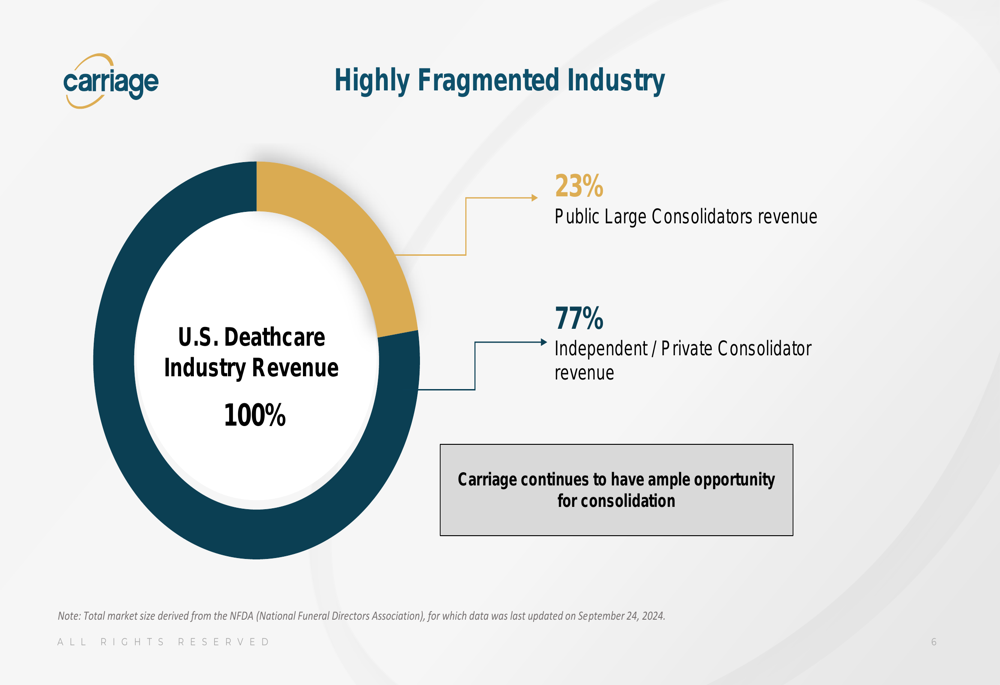

Operating in a highly fragmented industry where 77% of revenue remains controlled by independent and private operators, Carriage Services has positioned itself to capitalize on consolidation opportunities and favorable demographic trends as the U.S. population continues to age.

As shown in the following chart illustrating industry fragmentation, Carriage sees significant growth potential through strategic acquisitions:

Executive Summary

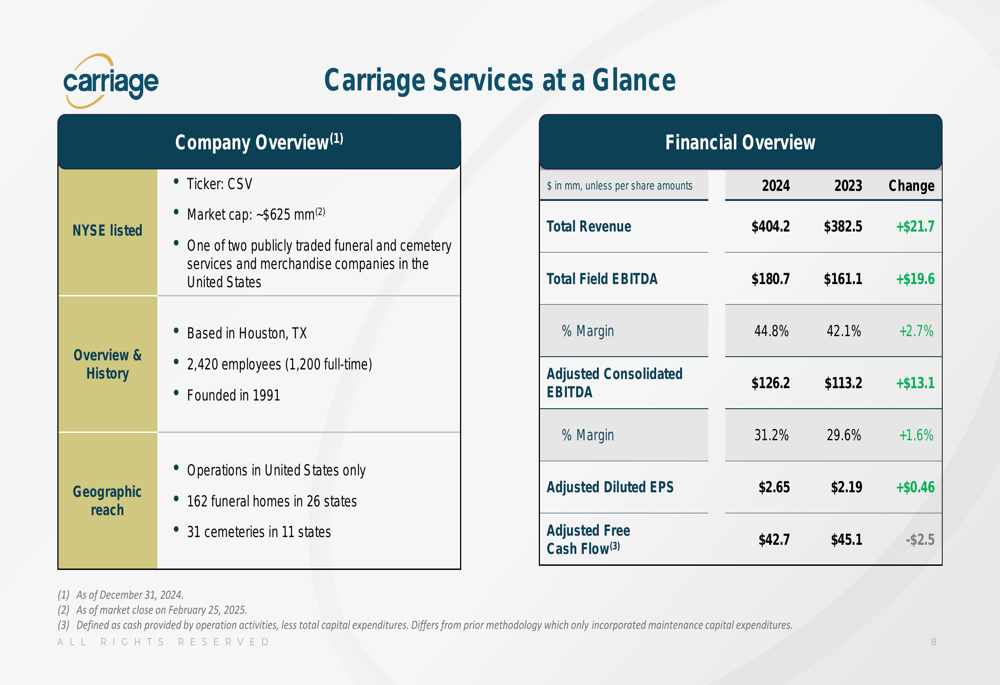

Carriage Services operates 162 funeral homes across 26 states and 31 cemeteries in 11 states, employing approximately 2,420 people. The company reported solid financial performance for 2024, with total revenue of $404.2 million, representing a $21.7 million increase from 2023. More importantly, profitability metrics showed significant improvement, with adjusted consolidated EBITDA margins expanding to 31.2% from 29.6% in the prior year.

The company’s comprehensive overview is illustrated in this snapshot:

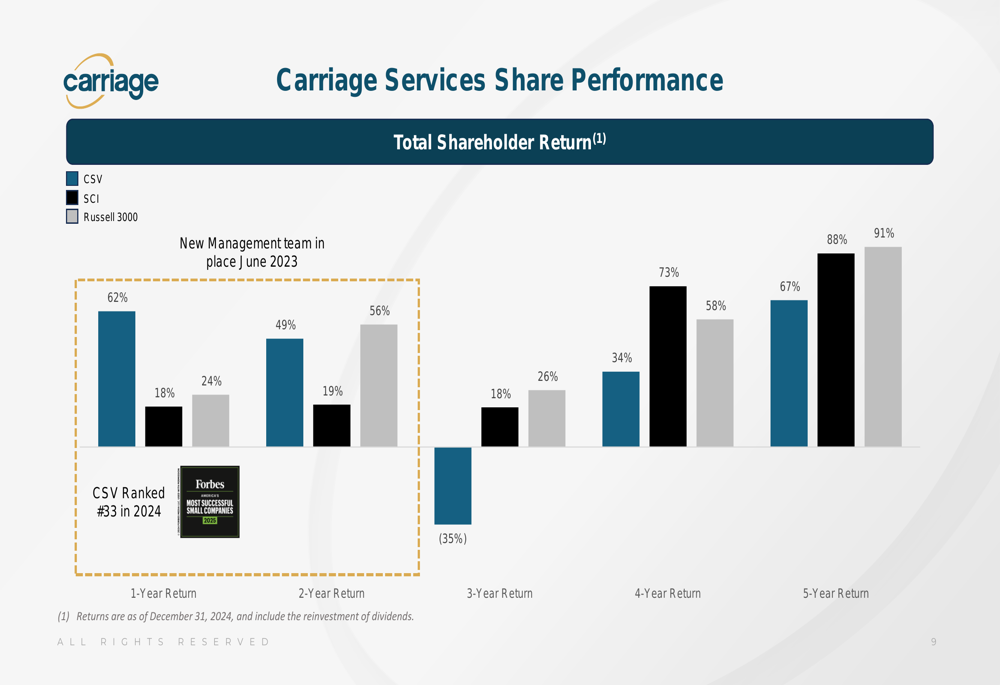

Under the leadership of CEO Carlos R. Quezada, who assumed the role in June 2023, Carriage Services has outperformed both its primary competitor Service Corporation International (NYSE:SCI) and the broader Russell 3000 index over the past year, delivering a 62% one-year return compared to 18% for SCI and 24% for the Russell 3000.

This performance comparison is clearly shown in the following chart:

Detailed Financial Analysis

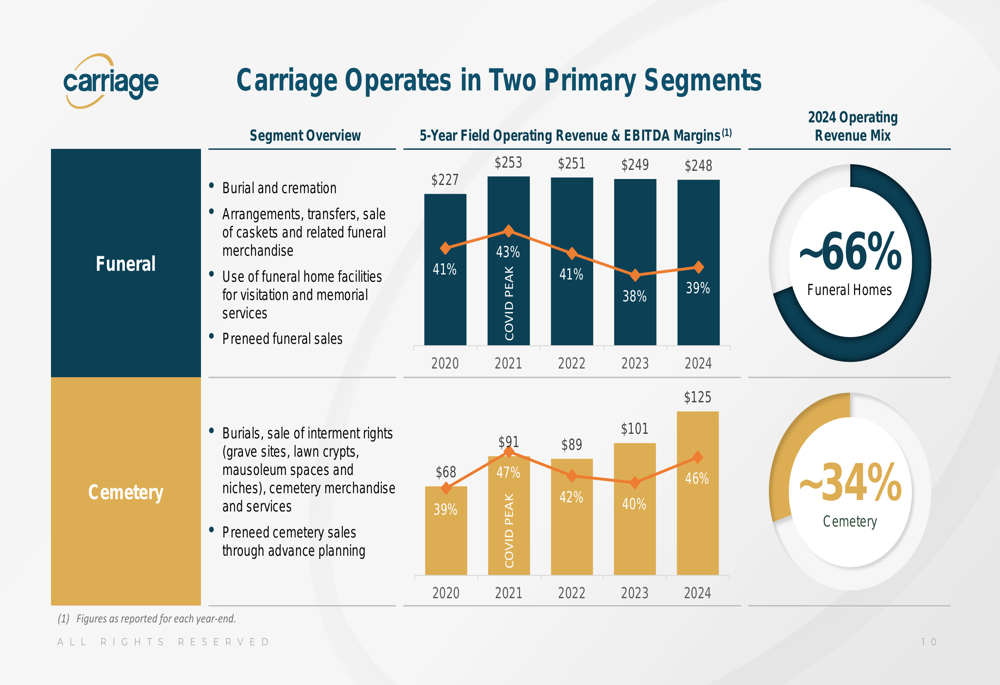

Carriage Services operates through two primary segments: Funeral (66% of 2024 revenue) and Cemetery (34%). Both segments have demonstrated strong profitability, with funeral home operations achieving a 39% EBITDA margin in 2024, up from 38% in 2023, while cemetery operations reached an impressive 46% margin, up from 40% in the prior year.

The segment breakdown and historical performance are illustrated below:

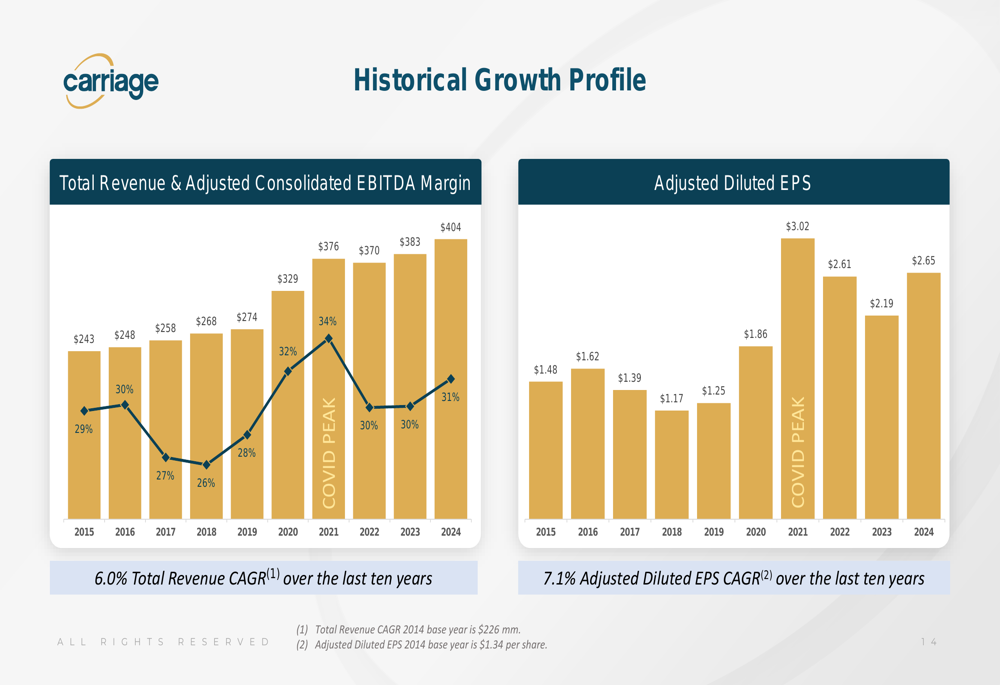

The company has maintained consistent growth over the past decade, with a 6.0% revenue CAGR and a 7.1% adjusted diluted EPS CAGR over the ten-year period. This long-term performance demonstrates the resilience of Carriage’s business model through various economic cycles.

The historical growth trajectory is visualized in this chart:

In its most recent quarterly results (Q2 2025), Carriage Services reported earnings per share of $0.74, slightly beating analyst expectations of $0.73, while revenue came in at $102.15 million, marginally above the forecasted $101.36 million. While quarterly revenue was flat year-over-year, the company saw growth in funeral operating revenue (+1.4%) and financial revenue (+18.8%), offsetting a slight decline in cemetery operating revenue (-0.6%).

Strategic Growth Initiatives

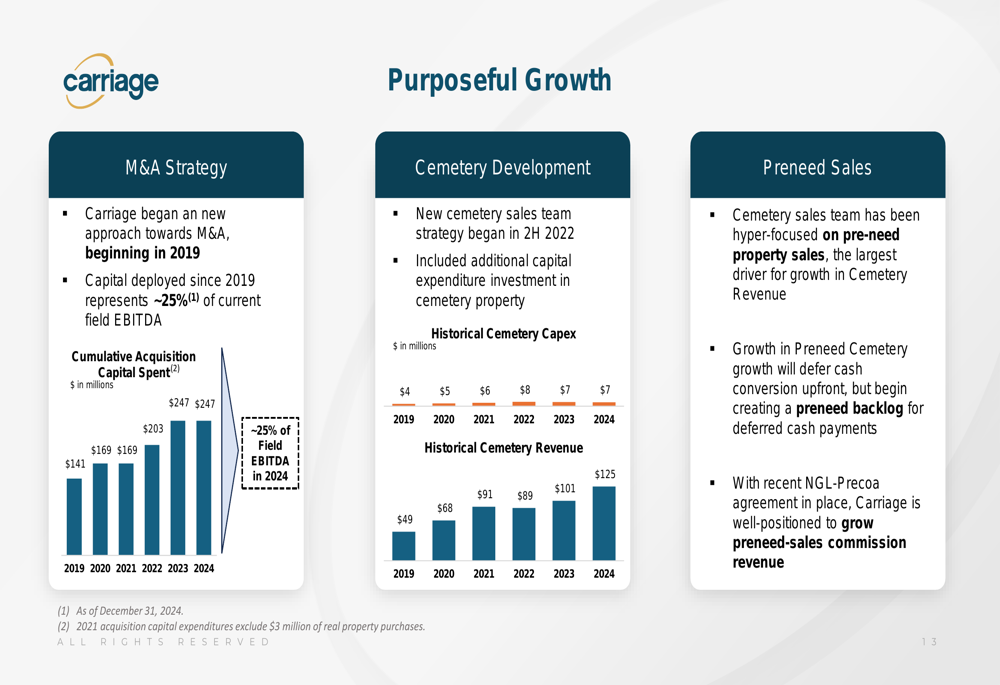

Carriage Services has outlined a three-pronged approach to growth, focusing on acquisitions, cemetery development, and preneed sales. Since 2019, the company has deployed approximately $250 million for acquisitions, representing about 25% of its current field EBITDA. This strategic approach to M&A has allowed Carriage to establish a stronger presence in key markets.

The company’s growth strategy is detailed in the following chart:

Carriage has also increased its investment in cemetery property development, with capital expenditures rising from $4 million in 2019 to $7 million in 2024. This investment has contributed to significant growth in cemetery revenue, which increased from $49 million to $125 million over the same period.

The company’s preneed sales strategy has focused on building a backlog of future revenue, particularly in the cemetery segment. With a recent agreement with NGL-Precoa, Carriage is well-positioned to grow its preneed sales commission revenue.

Industry Position & Competitive Landscape

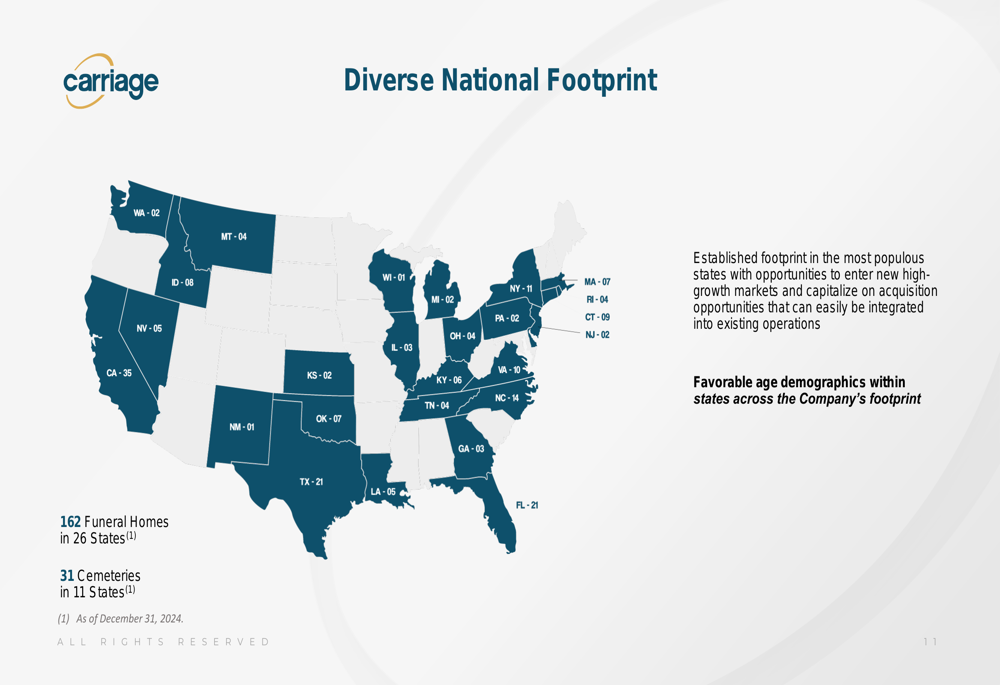

Carriage Services has established a diverse national footprint, with particular strength in populous states. The company’s geographic presence provides a solid foundation for both organic growth and strategic acquisitions in high-growth markets.

The company’s national presence is illustrated in this map:

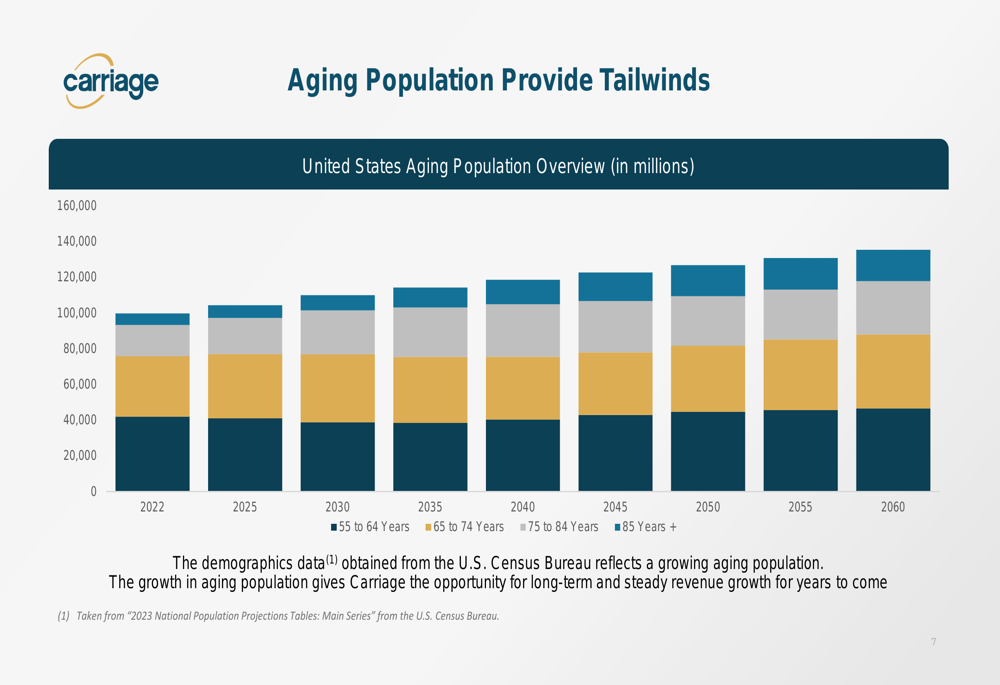

The funeral and cemetery services industry benefits from favorable demographic trends, with the aging U.S. population providing long-term tailwinds. As the baby boomer generation continues to age, the demand for funeral and cemetery services is expected to increase steadily over the coming decades.

This demographic trend is clearly visualized in the following chart:

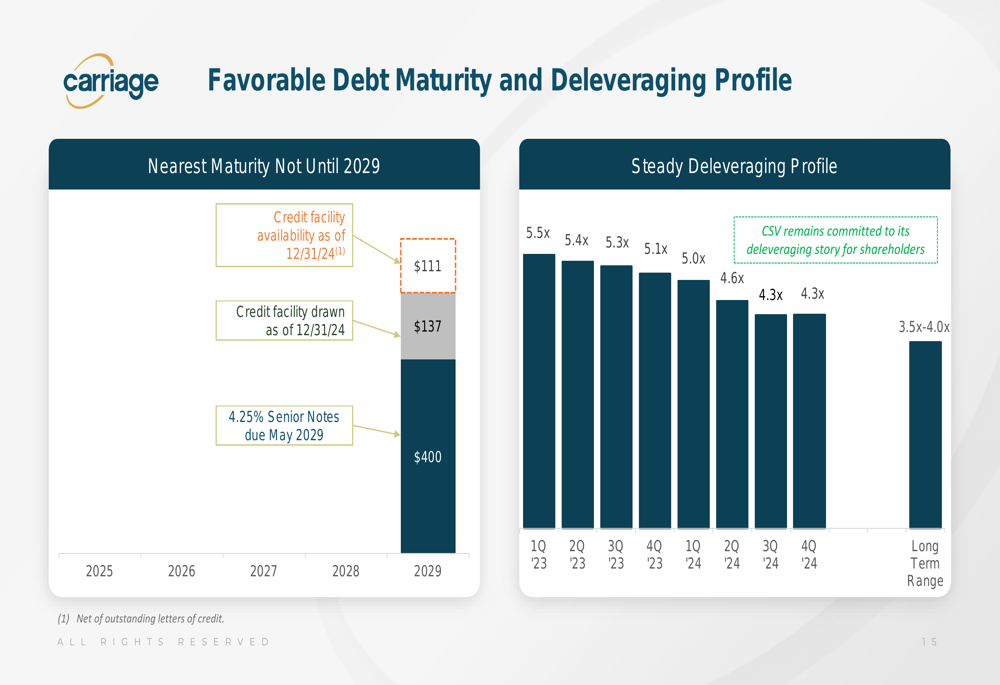

From a financial perspective, Carriage Services maintains a solid balance sheet with no debt maturities until 2029. The company has demonstrated a commitment to deleveraging, with a target leverage ratio range of 3.5x to 4.0x, providing financial flexibility for future growth initiatives.

The debt maturity and deleveraging profile is shown here:

Forward-Looking Statements

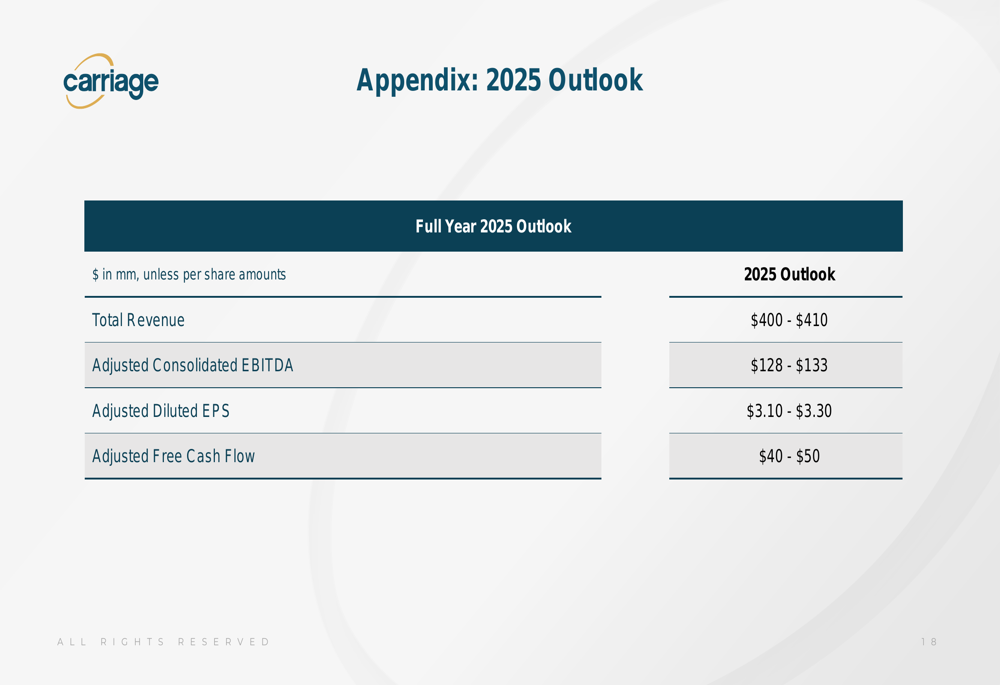

For the full year 2025, Carriage Services initially projected revenue between $400 million and $410 million, adjusted consolidated EBITDA of $128-$133 million, adjusted diluted EPS of $3.10-$3.30, and adjusted free cash flow of $40-$50 million. However, in its Q2 2025 earnings report, the company raised its guidance slightly, now anticipating full-year revenue of $410-$420 million, adjusted EBITDA of $129-$134 million, and adjusted EPS of $3.15-$3.35.

The company’s initial 2025 outlook is summarized in this table:

CEO Carlos Quezada emphasized the company’s return to "growth mode" during the Q2 2025 earnings call, highlighting the company’s focus on service excellence and selective M&A strategy. With a robust acquisition pipeline and plans to close multiple transactions in Q3 2025, Carriage Services is targeting approximately $50 million in acquisition revenue.

The company’s strategic framework focuses on three key pillars: disciplined capital allocation, purposeful growth, and relentless improvement. By executing on these priorities, Carriage Services aims to continue delivering strong financial results and shareholder value in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.