Bitcoin price today: struggles at $111k as trade tensions, risk aversion weigh

Introduction & Market Context

Carvana Co (NYSE:CVNA), the second-largest used car retailer in the United States, has released its Q3 2024 supplemental financial tables, revealing continued momentum across key business metrics. The company’s presentation demonstrates significant year-over-year improvements in retail unit sales, gross profit per unit (GPU), and adjusted EBITDA, reinforcing its successful business transformation.

The company’s stock closed at $369.29 on September 26, 2025, representing substantial growth from its 52-week low of $148.25, though still below its 52-week high of $413.34. With a market capitalization of approximately $72.6 billion, Carvana continues to execute on its ambitious growth strategy in the fragmented used car market.

Quarterly Performance Highlights

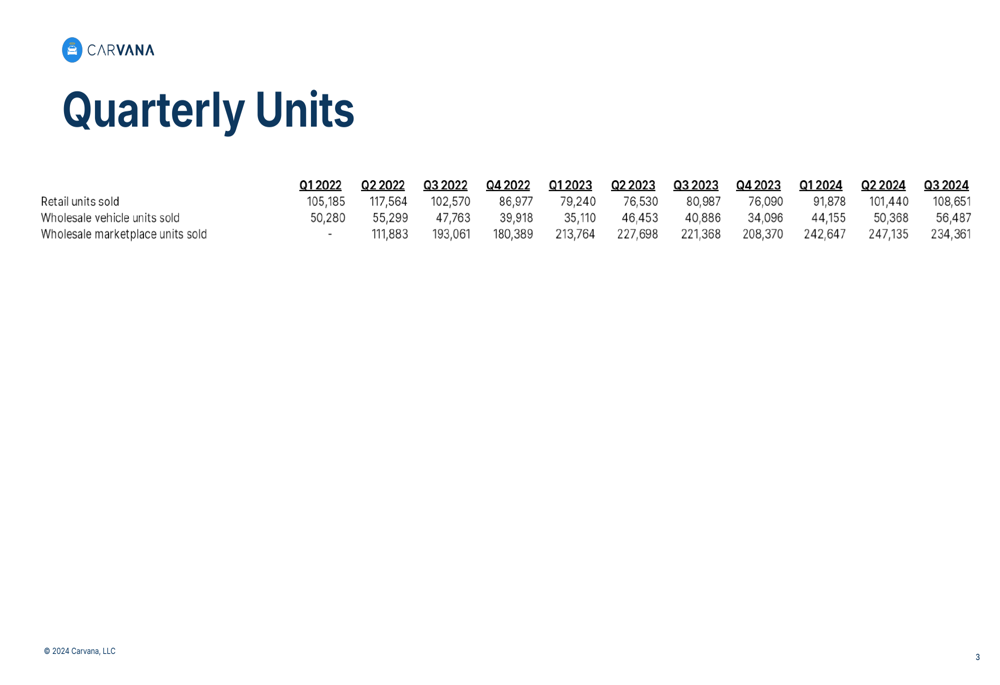

Carvana reported substantial growth in its retail business for Q3 2024, with 108,651 retail units sold, representing a 34.2% increase from 80,987 units in Q3 2023. This growth trajectory has been consistent over recent quarters, with retail units showing sequential improvement throughout 2024.

As shown in the following quarterly units data, the company also saw significant increases in its wholesale vehicle and marketplace operations:

The company’s wholesale vehicle units sold increased to 56,487 in Q3 2024, up 38.2% from 40,886 in Q3 2023. Similarly, wholesale marketplace units sold reached 247,135, an 8.5% increase from the same period last year. These figures demonstrate Carvana’s growing scale across multiple business segments.

Detailed Financial Analysis

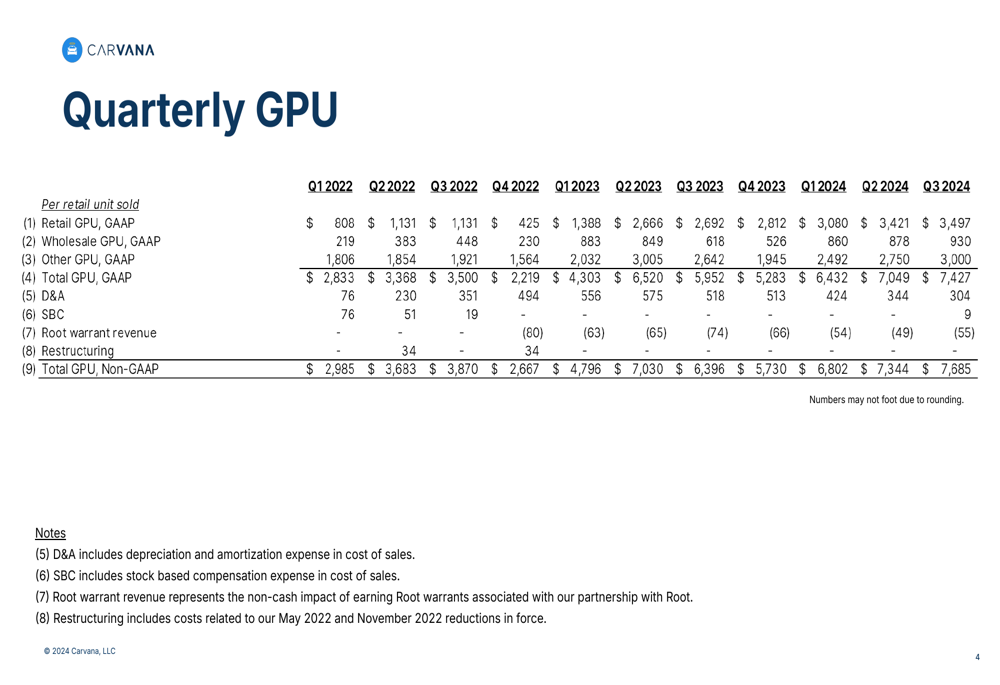

Carvana’s financial performance in Q3 2024 was marked by substantial improvements in profitability metrics. Total GPU (Gross Profit per Unit) reached $7,427 in Q3 2024, a 24.8% increase from $5,952 in Q3 2023, highlighting the company’s ability to generate more revenue and profit from each vehicle sold.

The following chart illustrates the consistent improvement in Carvana’s GPU metrics over the past several quarters:

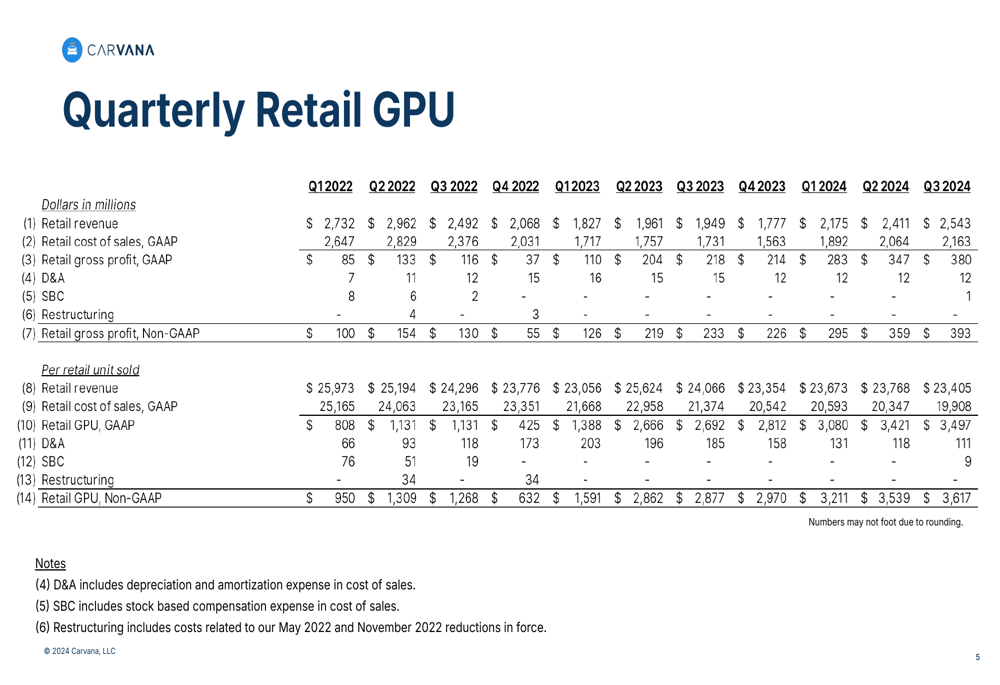

Breaking down the GPU components further, retail GPU showed particularly strong performance, reaching $3,497 in Q3 2024, up 29.9% from $2,692 in Q3 2023. This improvement reflects Carvana’s enhanced vehicle acquisition strategies, pricing optimization, and operational efficiencies.

The detailed retail GPU breakdown demonstrates consistent improvement across multiple quarters:

Wholesale vehicle operations also contributed significantly to the company’s profitability, with wholesale vehicle GPU reaching $562 in Q3 2024, a 62% increase from $347 in Q3 2023. This improvement reflects Carvana’s growing expertise in vehicle remarketing and its ability to optimize returns from non-retail inventory.

Strategic Initiatives & Efficiency Gains

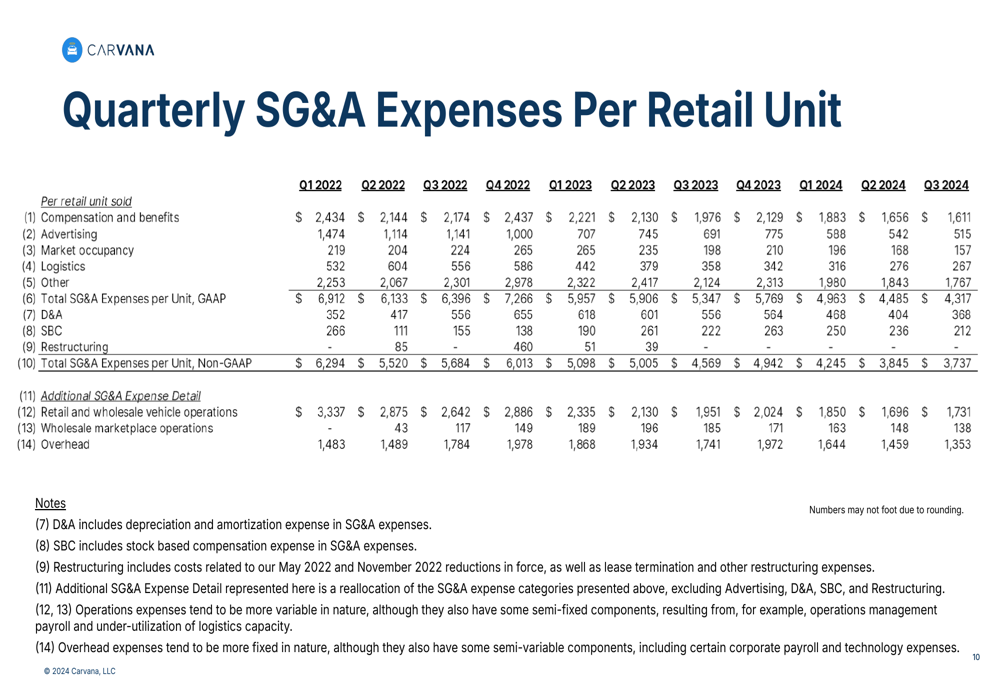

A key element of Carvana’s improved financial performance has been its focus on operational efficiency. Despite growing its business substantially, the company has managed to reduce SG&A expenses per retail unit to $4,317 in Q3 2024, down 19.3% from $5,347 in Q3 2023.

The following table details the company’s SG&A expenses per retail unit over time:

This improvement in operational efficiency is particularly notable given the company’s growth trajectory. Total SG&A expenses increased modestly to $469 million in Q3 2024 from $433 million in Q3 2023, but the per-unit metrics demonstrate that Carvana is successfully scaling its operations while controlling costs.

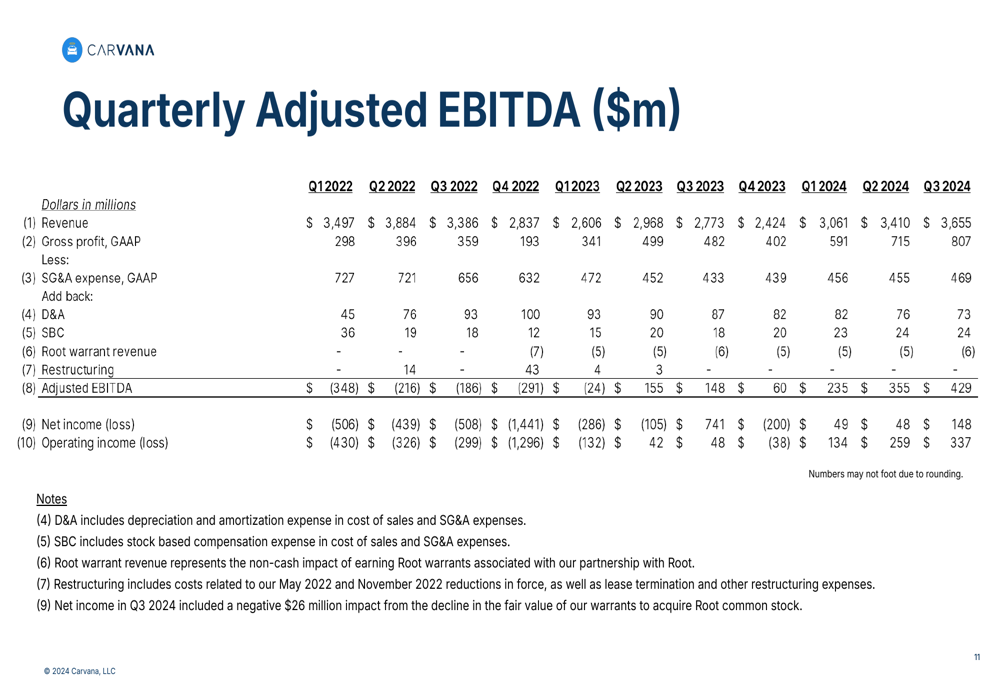

The company’s strategic focus on efficiency has contributed significantly to its bottom line. Adjusted EBITDA reached $429 million in Q3 2024, a remarkable 189.9% increase from $148 million in Q3 2023, highlighting the successful transformation of Carvana’s business model.

The quarterly Adjusted EBITDA figures show the company’s dramatic financial improvement:

This strong Adjusted EBITDA performance represents a significant turnaround from the negative figures reported in 2022, demonstrating Carvana’s successful execution of its business transformation strategy.

Forward-Looking Statements

While the Q3 2024 presentation does not include specific forward guidance, Carvana’s previous statements indicate ambitious long-term goals. The company aims to sell 3 million cars annually and achieve a 13.5% adjusted EBITDA margin within the next 5 to 10 years.

The consistent improvement in key metrics demonstrated in the Q3 2024 presentation suggests Carvana is making steady progress toward these goals. The company’s focus on operational efficiency, as evidenced by decreasing SG&A expenses per unit, positions it well for continued growth and profitability improvement.

Carvana’s current market position, representing approximately 1.5% of the U.S. used car market, leaves substantial room for expansion. The company’s continued investment in customer experience, inventory selection, and operational efficiency appears to be yielding positive results as demonstrated by the strong performance metrics in the Q3 2024 presentation.

As Carvana continues to execute its growth strategy, investors will be watching closely to see if the company can maintain its momentum in unit sales growth while further improving its profitability metrics. The Q3 2024 results suggest the company remains on a positive trajectory toward its ambitious long-term goals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.