Gold bars to be exempt from tariffs, White House clarifies

Caterpillar Inc. (NYSE:CAT) reported a 10% year-over-year decline in revenue for the first quarter of 2025, while simultaneously achieving record organic backlog growth and returning substantial capital to shareholders. The heavy equipment manufacturer released its financial results on April 30, 2025, as the company celebrates its 100-year anniversary.

Quarterly Performance Highlights

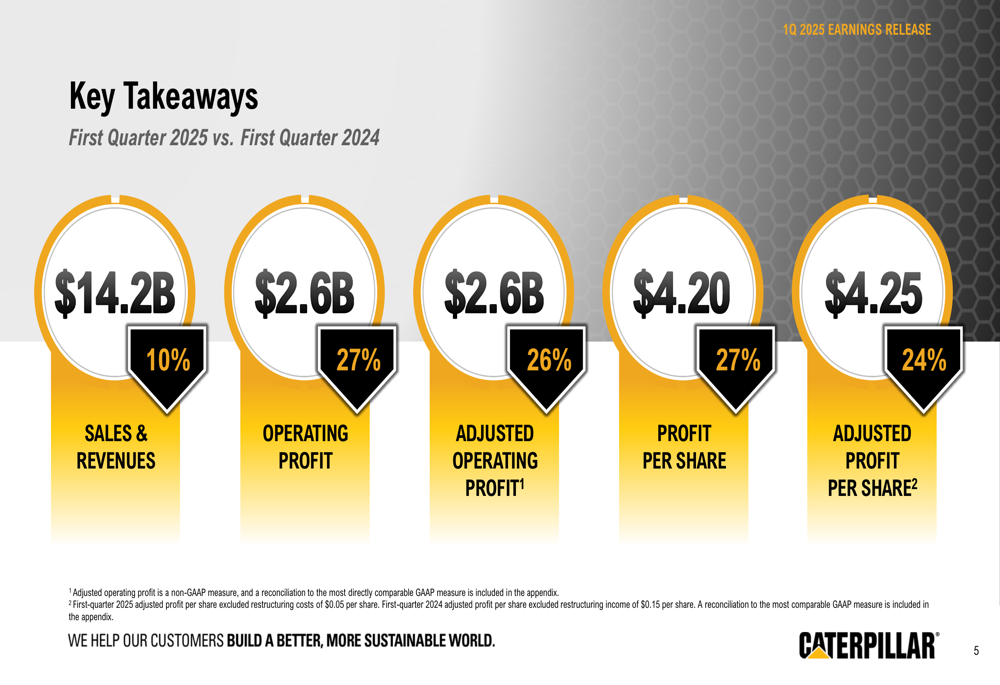

Caterpillar’s first quarter results showed significant declines across key financial metrics compared to the same period in 2024. Sales and revenues fell to $14.2 billion, down 10% from $15.8 billion in Q1 2024. Operating profit decreased by 27% to $2.6 billion, while adjusted profit per share dropped 24% to $4.25.

As shown in the following key financial comparison:

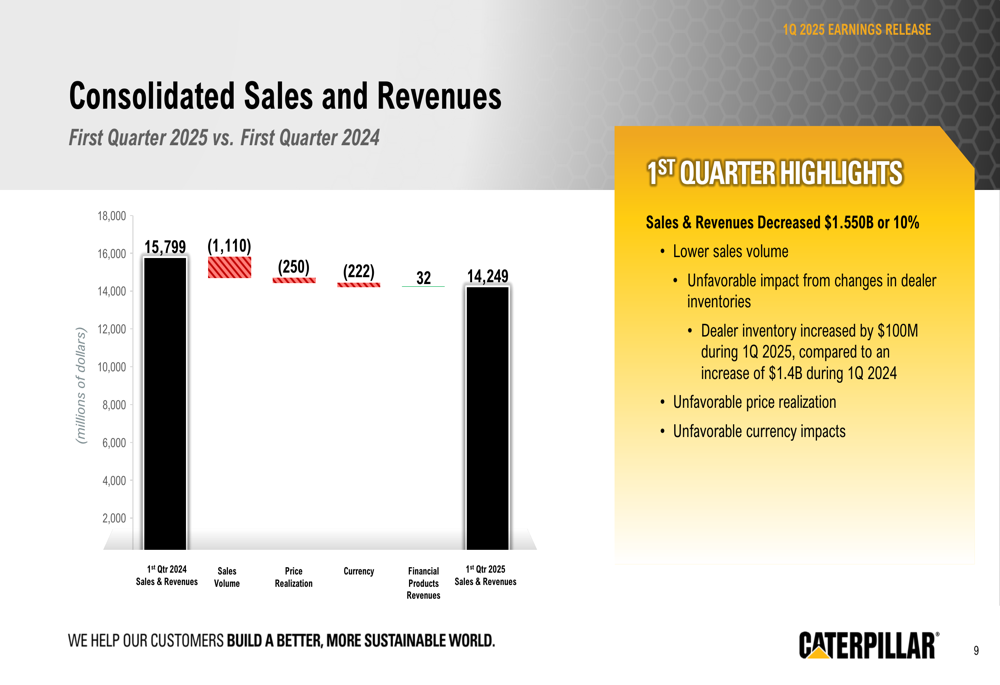

The company attributed the revenue decline primarily to lower sales volume, unfavorable price realization, and unfavorable currency impacts. A significant factor was the change in dealer inventory dynamics, with dealers increasing inventory by only $100 million in Q1 2025 compared to a $1.4 billion increase during Q1 2024.

The following chart illustrates the breakdown of consolidated sales and revenue changes:

Despite these challenges, Caterpillar highlighted an all-time record organic backlog growth of $5 billion in the quarter, suggesting potential future revenue strength. The company’s backlog increased by $7.1 billion compared to Q1 2024.

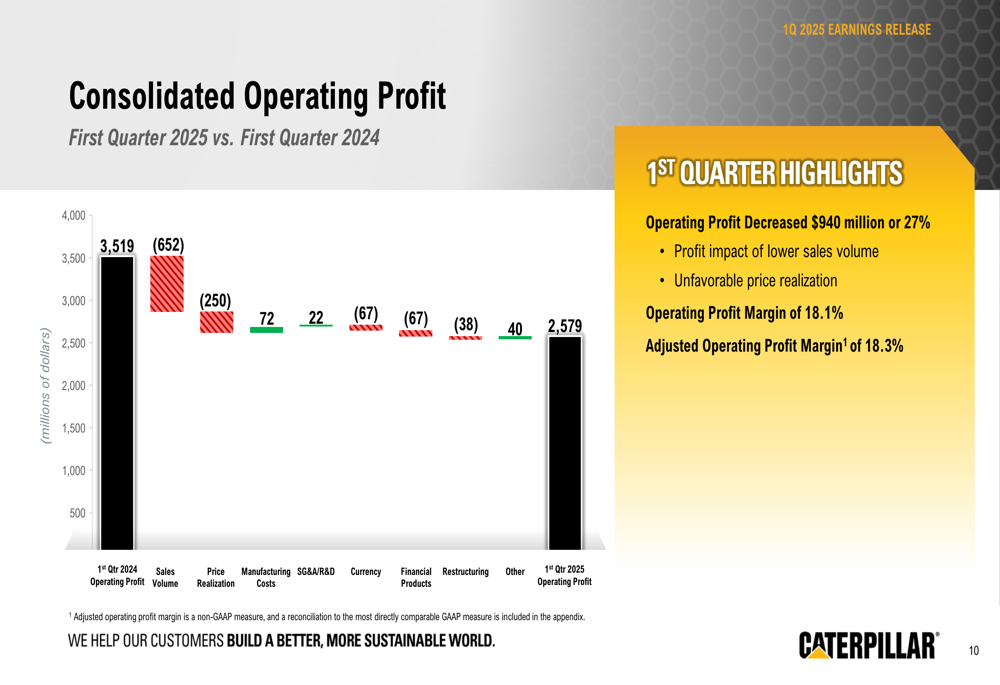

Operating profit margin stood at 18.1% for the quarter, with adjusted operating profit margin at 18.3%. The following waterfall chart details the factors affecting operating profit:

Segment Performance Analysis

All of Caterpillar’s major business segments except Financial Products experienced revenue declines, with Construction Industries showing the steepest drop.

Construction Industries saw total sales decrease by 19% to $5.2 billion, with segment profit falling 42% to $1.0 billion. This significant decline was attributed to lower sales volume and unfavorable price realization.

Resource Industries reported a 10% sales decrease to $2.9 billion, with segment profit down 18% to $599 million, primarily due to lower sales volume.

Energy & Transportation demonstrated more resilience with only a 2% sales decline to $6.6 billion, while segment profit actually increased by 1% to $1.3 billion. This segment benefited from favorable price realization, which mostly offset lower sales volume and unfavorable manufacturing costs.

Financial Products was the only segment to report revenue growth, with a 2% increase to $1.0 billion. However, segment profit declined 27% to $215 million due to the absence of an insurance settlement, higher provision for credit losses, and unfavorable impacts from lower net yield on average earning assets and equity securities.

Cash Flow and Shareholder Returns

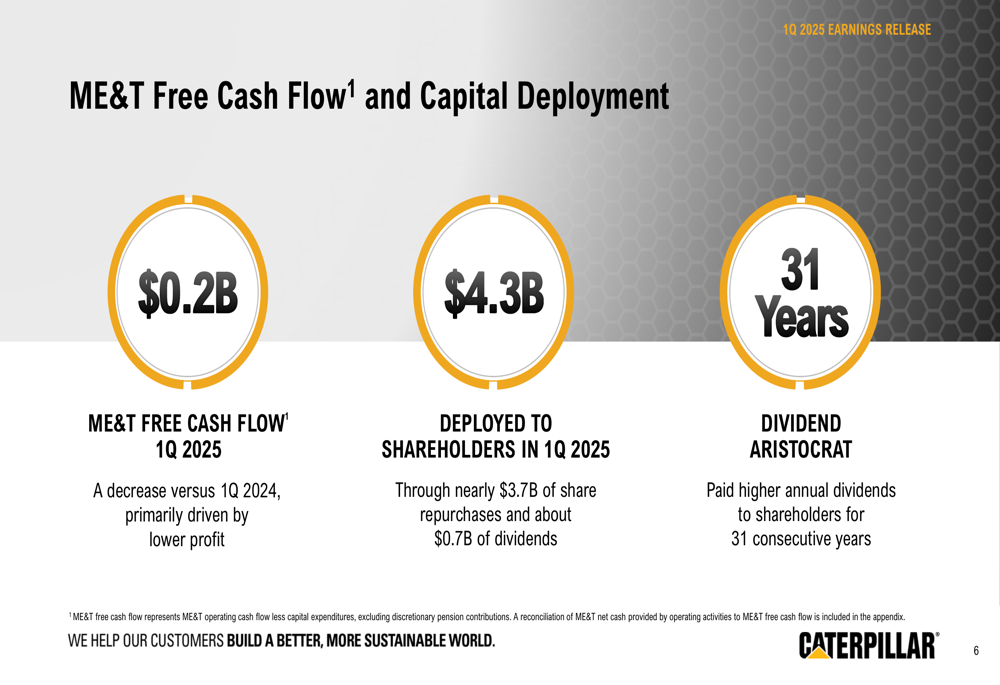

Despite performance challenges, Caterpillar maintained its commitment to shareholder returns. The company deployed $4.3 billion to shareholders during Q1 2025, including nearly $3.7 billion in share repurchases and approximately $0.7 billion in dividends.

The following image illustrates Caterpillar’s cash flow and capital deployment:

Machinery, Energy & Transportation (ME&T) free cash flow was $0.2 billion in Q1 2025, down from $1.3 billion in Q1 2024, primarily due to lower profit. The company maintained a strong enterprise cash balance of $3.6 billion, with an additional $1.2 billion in slightly longer-dated liquid marketable securities.

Caterpillar highlighted its status as a Dividend Aristocrat, having paid higher annual dividends to shareholders for 31 consecutive years.

Forward Outlook and Guidance

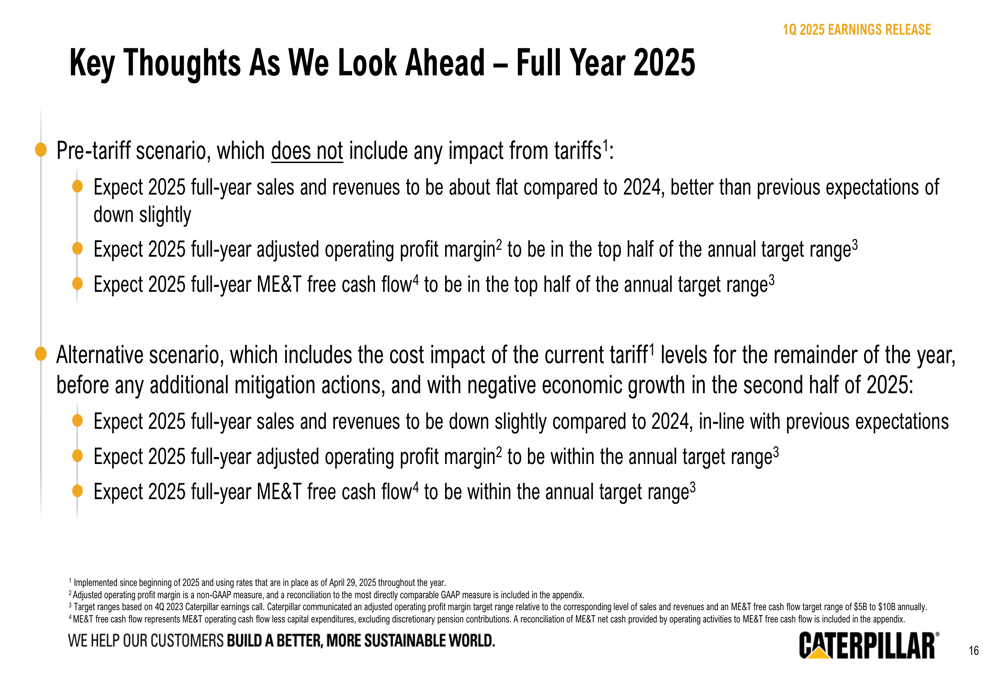

Caterpillar provided guidance for the full year 2025 under two scenarios, reflecting uncertainty around tariff impacts. In the pre-tariff scenario, the company expects full-year sales and revenues to be about flat compared to 2024, with adjusted operating profit margin and ME&T free cash flow in the top half of their respective annual target ranges.

In an alternative scenario that includes the cost impact of current tariff levels for the remainder of the year, Caterpillar expects slightly lower full-year sales and revenues compared to 2024, with adjusted operating profit margin and ME&T free cash flow within (but not in the top half of) the annual target ranges.

The following slide details these outlook scenarios:

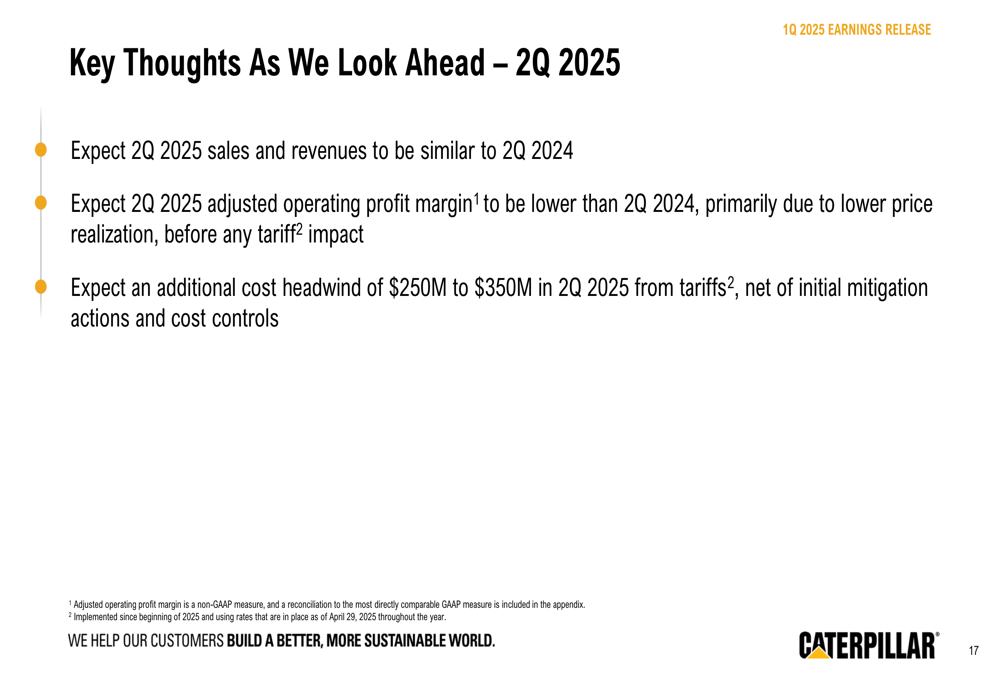

For Q2 2025 specifically, Caterpillar expects sales and revenues to be similar to Q2 2024, but with lower adjusted operating profit margin primarily due to lower price realization, before any tariff impact. The company anticipates an additional cost headwind of $250 million to $350 million in Q2 2025 from tariffs, net of initial mitigation actions and cost controls.

Strategic Positioning

Despite current challenges, Caterpillar emphasized that its results "reflect the benefit of the diversity of our end markets." The company continues to execute its strategy for long-term profitable growth, supported by a strong balance sheet and liquidity position.

The record backlog growth suggests strong customer demand, which could translate into future revenue as supply chain and production capacity allow. Caterpillar expects machine dealer inventory to remain about flat by the end of 2025.

As the company celebrates its centennial year, management expressed confidence in Caterpillar’s ability to navigate current market conditions while positioning for future growth, as summarized in these key takeaways:

In premarket trading on April 30, Caterpillar shares were down 1.83% to $301.76, suggesting investors may have concerns about the revenue and profit declines despite the company’s strong backlog growth and shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.