Fannie Mae, Freddie Mac shares tumble after conservatorship comments

Introduction & Market Context

CCC (WA:CCCP) Intelligent Solutions Holdings Inc (NASDAQ:CCCS) presented its investor presentation on February 25, 2025, highlighting the company’s strong market position in the insurance technology sector and its strategic growth initiatives. The presentation comes as CCC recently reported its Q1 2025 earnings, where it achieved $251.6 million in revenue, representing a 10.7% year-over-year increase and slightly exceeding analyst expectations of $249.76 million.

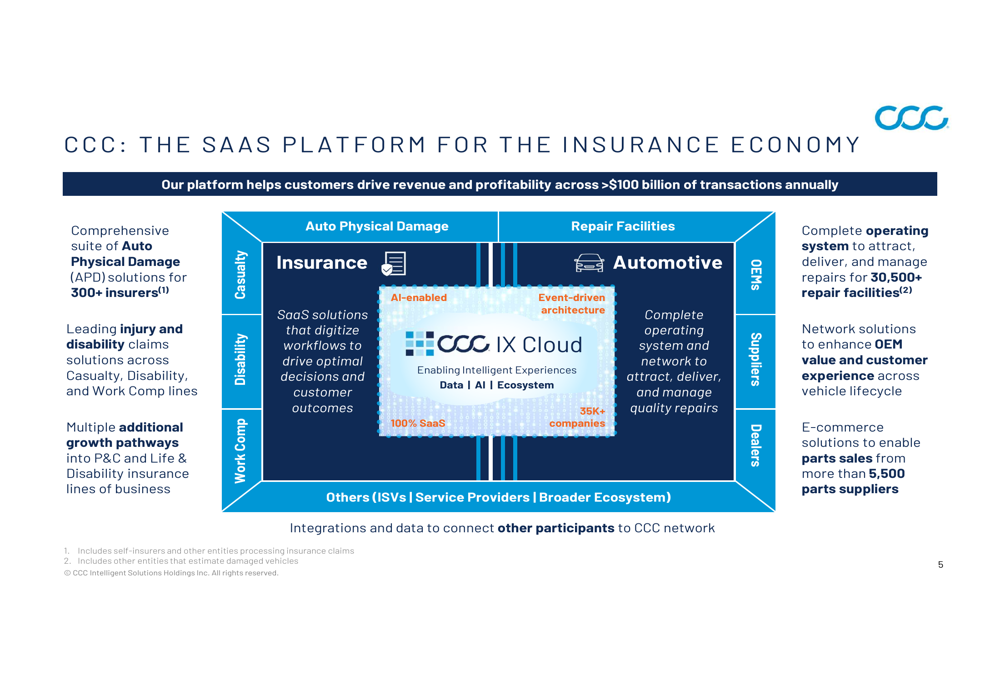

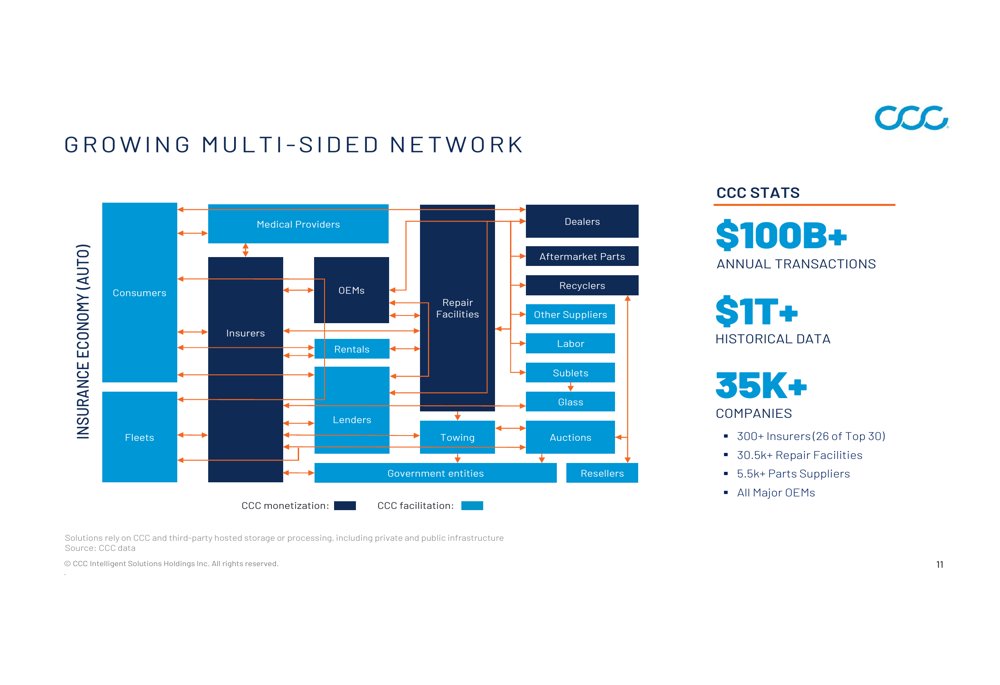

The company operates a SaaS platform that serves as a central hub for the insurance economy, processing over $100 billion in annual transactions across more than 35,000 companies. CCC’s platform connects insurers, repair facilities, parts suppliers, and other stakeholders in the automotive claims ecosystem, creating significant network effects that strengthen its competitive position.

As shown in the following visualization of CCC’s platform architecture, the company has built a comprehensive ecosystem that drives revenue and profitability across the insurance value chain:

Financial Performance Highlights

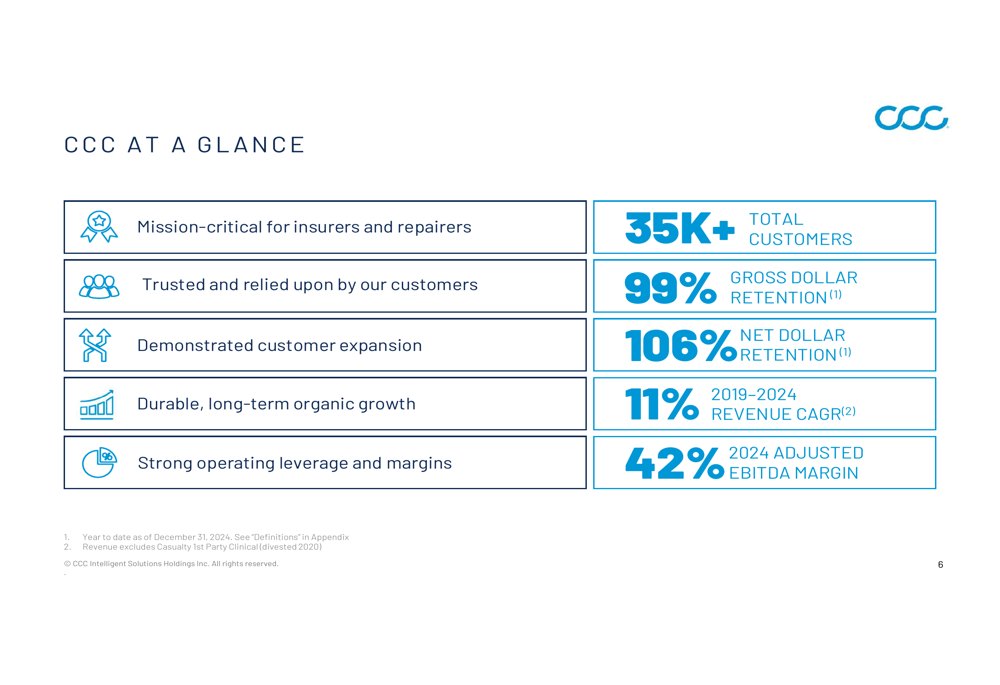

CCC Intelligent Solutions has demonstrated consistent financial performance with 20+ consecutive years of revenue growth and profitability. The company’s investor presentation highlighted key metrics including a 99% gross dollar retention rate and 106% net dollar retention rate, indicating strong customer loyalty and successful upselling efforts. These metrics align closely with the 99% software gross dollar retention and 107% net dollar retention reported in the company’s Q1 2025 earnings.

The following slide summarizes CCC’s key performance metrics, including its 11% revenue CAGR from 2019-2024 and 42% adjusted EBITDA margin:

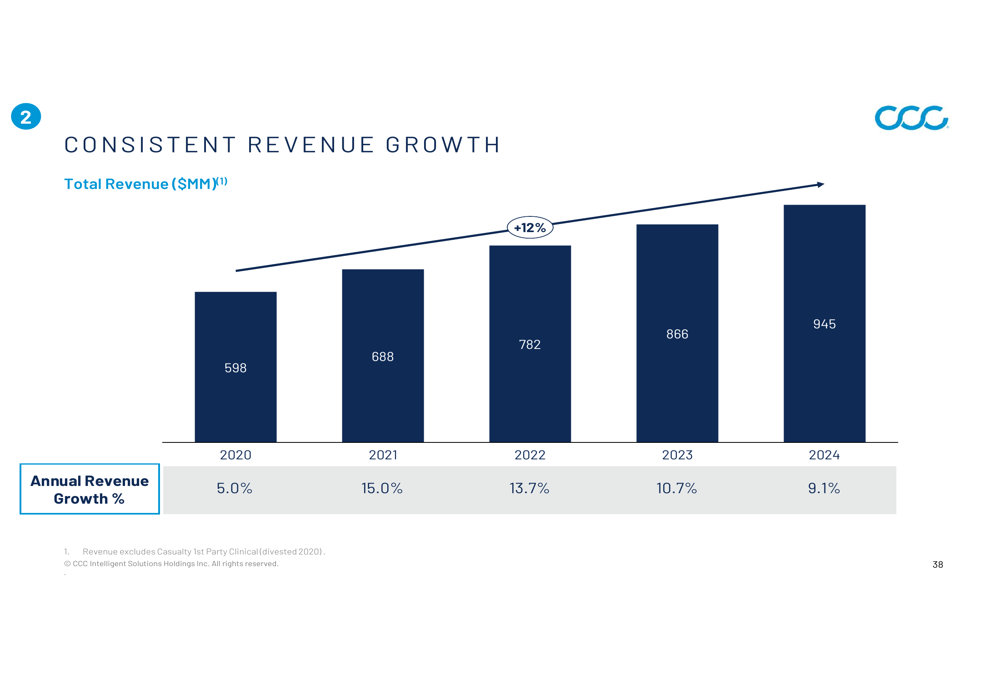

The company’s revenue has grown steadily from $598 million in 2020 to $946 million in 2024, with annual growth rates ranging from 5.0% to 9.1%. This trend has continued into 2025, with the company’s Q1 revenue growth of 10.7% year-over-year, as reported in its recent earnings release.

The following chart illustrates CCC’s consistent revenue growth trajectory:

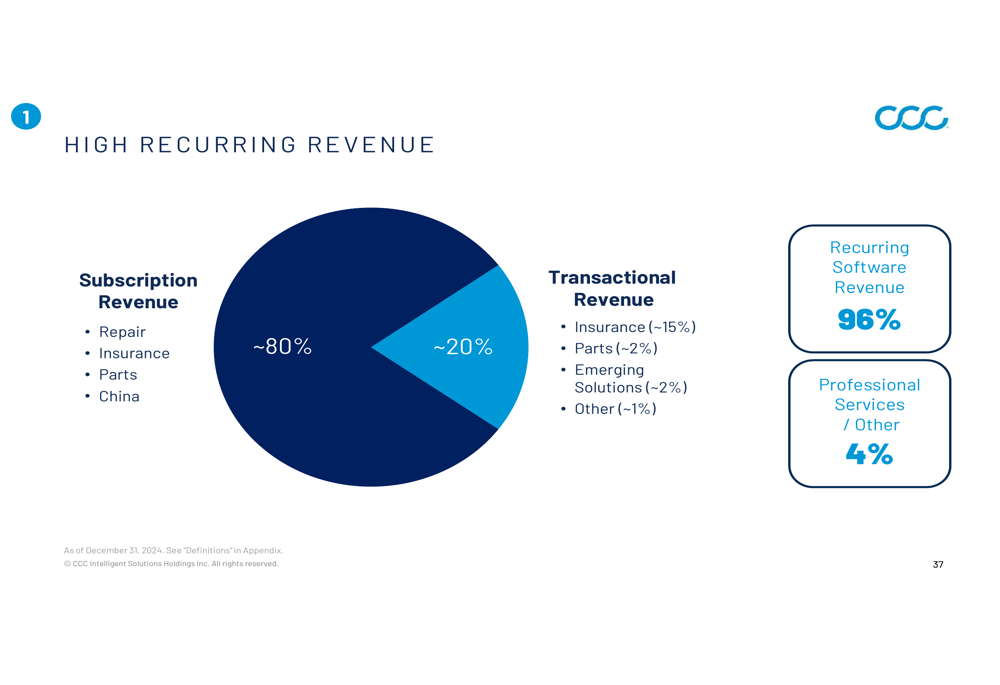

CCC’s business model is characterized by high recurring revenue, with 96% of its software revenue being recurring in nature. This provides the company with significant visibility into future financial performance and stability. The revenue mix consists of approximately 80% subscription revenue and 20% transactional revenue.

As shown in the following breakdown of revenue streams:

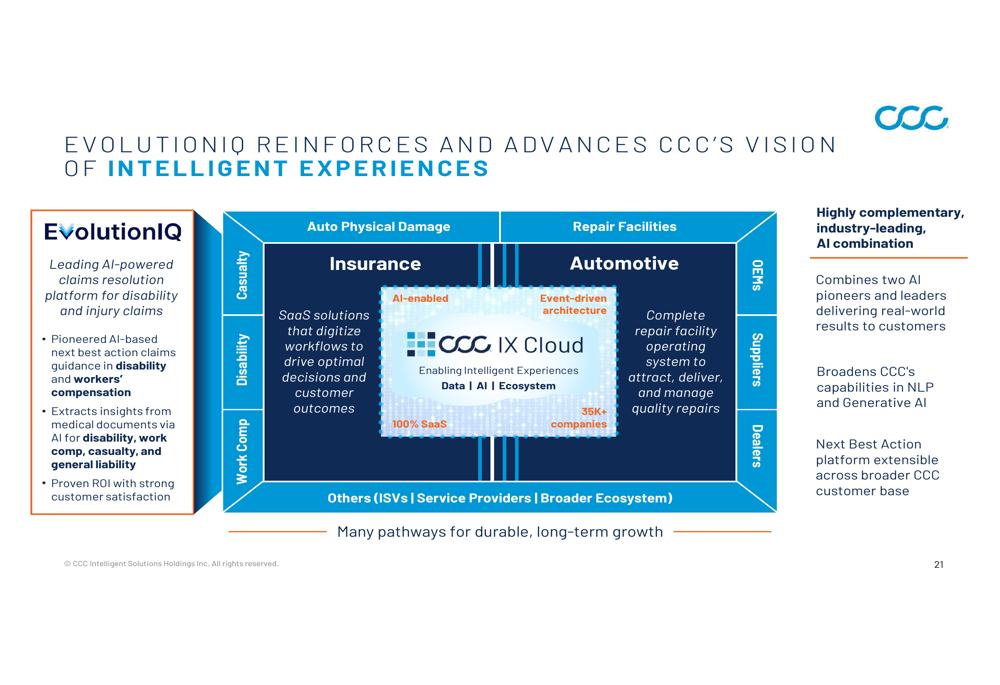

Strategic Acquisition of EvolutionIQ

A significant focus of CCC’s investor presentation was its acquisition of EvolutionIQ, an AI-powered disability and injury claims resolution platform. The $730 million transaction (59% cash/41% stock) expands CCC’s addressable market and enhances its AI capabilities in the disability and injury claims space.

The following slide illustrates how EvolutionIQ complements CCC’s existing business and advances its vision of "Intelligent Experiences":

EvolutionIQ brings a strong customer base that includes 7 of the top 15 disability carriers and processes over $10 billion in claims annually. The company was founded in 2019 and has achieved approximately 95% gross dollar retention, indicating strong customer loyalty. CCC expects EvolutionIQ to generate $45-50 million in revenue in 2025.

The following slide provides key details about EvolutionIQ’s business and capabilities:

During CCC’s Q1 2025 earnings call, management highlighted that EvolutionIQ’s performance in disability and workers’ compensation has been strong, validating the strategic rationale for the acquisition. The integration of EvolutionIQ is expected to contribute to CCC’s long-term revenue growth target of 7-10% annually.

Technology and AI Capabilities

CCC has invested over $1 billion in R&D over the past decade, building a modern cloud-based platform that handles 5.2 billion database transactions per day with 99.91% uptime. The company’s technology infrastructure enables it to deliver AI-powered solutions at scale, with 100+ insurers already using CCC AI in production and 300+ AI models developed.

The company’s network effect is a key competitive advantage, connecting 35,000+ companies including 300+ insurers, 30,500+ repair facilities, and 5,500+ parts suppliers. This extensive network creates significant barriers to entry and enables CCC to leverage its vast data assets to develop increasingly sophisticated AI solutions.

The following visualization illustrates the scale and scope of CCC’s network:

In its Q1 2025 earnings call, CEO Gitesh Ramamurti emphasized that "the global insurance economy is still at the early stages of a generational digital upgrade cycle," positioning CCC to capitalize on the industry’s ongoing digital transformation. The company’s AI capabilities are particularly relevant as insurers seek to improve efficiency and accuracy in claims processing amid increasing vehicle complexity and labor shortages.

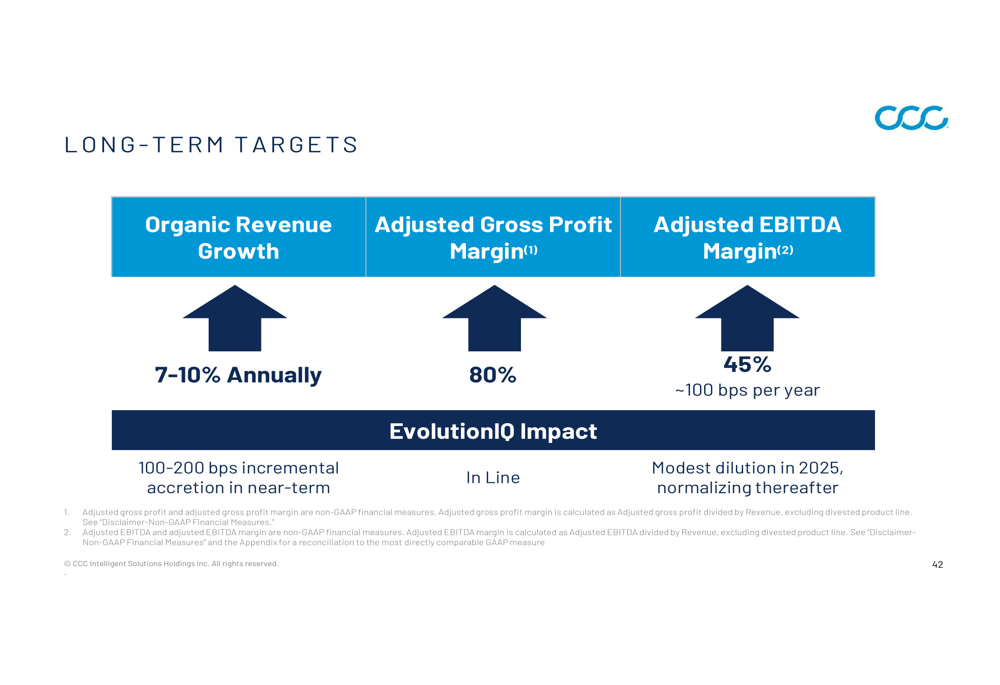

Long-Term Growth Strategy

CCC’s long-term growth strategy focuses on expanding its "Intelligent Experiences" across its platform, leveraging AI to enhance decision-making and automation in claims processing. The company has set ambitious long-term financial targets, including 7-10% annual organic revenue growth, 80% adjusted gross profit margin, and 45% adjusted EBITDA margin.

The following slide outlines these long-term targets:

To achieve these targets, CCC plans to shift its revenue mix from approximately 90% established solutions and 10% emerging solutions currently to a more balanced 50/50 split in the long term. This strategy is designed to accelerate revenue growth while maintaining strong profitability.

The company’s growth levers include expansion within existing customers, adding new customers, introducing new solutions, and strategic M&A activities like the EvolutionIQ acquisition. CCC’s high retention rates (99% gross dollar retention and 107% net dollar retention in Q1 2025) provide a strong foundation for this growth strategy.

Forward-Looking Statements

In its Q1 2025 earnings release, CCC provided guidance for full-year 2025 revenue between $1.046 billion and $1.056 billion, representing approximately 11% year-over-year growth. This aligns with the company’s long-term target of 7-10% organic revenue growth, with additional growth from acquisitions like EvolutionIQ.

However, the company also highlighted several risks and challenges in its earnings call, including declining auto insurance claim volumes (down 9% year-over-year in Q1 2025), economic uncertainties that could lengthen sales cycles, and increasing vehicle complexity. These factors could potentially impact the company’s ability to achieve its growth targets.

Despite these challenges, CCC’s strong market position, high recurring revenue model, and strategic investments in AI and emerging solutions position it well for continued growth. The company’s stock traded at $9.16 in the aftermarket session on June 23, 2025, down 1.93% from its previous close of $9.34, reflecting some investor caution amid broader market uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.