Stock market today: S&P 500 hits fresh record close on stronger economic growth

Introduction & Market Context

Celestica Inc . (NYSE:CLS) reported strong first-quarter 2025 results on April 25, with revenue growing 20% year-over-year to $2.649 billion. The company’s performance was driven primarily by robust growth in its Connectivity & Cloud Solutions (CCS) segment, particularly in Communications, which saw an 87% year-over-year increase. Based on this strong performance, Celestica (TSX:CLS) has raised its full-year 2025 outlook for both revenue and adjusted earnings per share.

The results continue the company’s momentum from 2024, when Celestica was already showing strong growth in similar business segments. The company’s focus on high-growth areas like networking for hyperscalers and AI/ML compute capabilities is paying dividends as reflected in the financial results.

Quarterly Performance Highlights

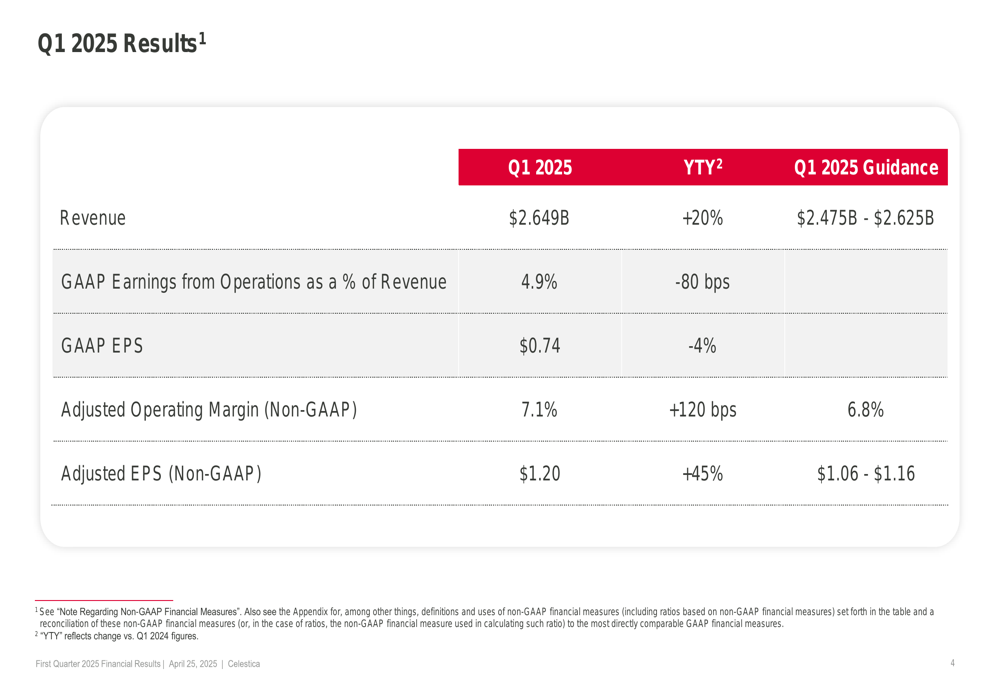

Celestica’s Q1 2025 results exceeded guidance across key metrics. Revenue of $2.649 billion was above the guided range of $2.475-$2.625 billion, representing a 20% increase year-over-year. While GAAP earnings per share decreased 4% to $0.74, adjusted (non-GAAP) EPS increased significantly by 45% to $1.20, exceeding the guidance range of $1.06-$1.16.

As shown in the following summary of Q1 2025 results:

The company’s adjusted operating margin (non-GAAP) improved by 120 basis points year-over-year to 7.1%, also exceeding guidance of 6.8%. This margin expansion occurred despite a slight decline in GAAP earnings from operations as a percentage of revenue, which decreased by 80 basis points to 4.9%.

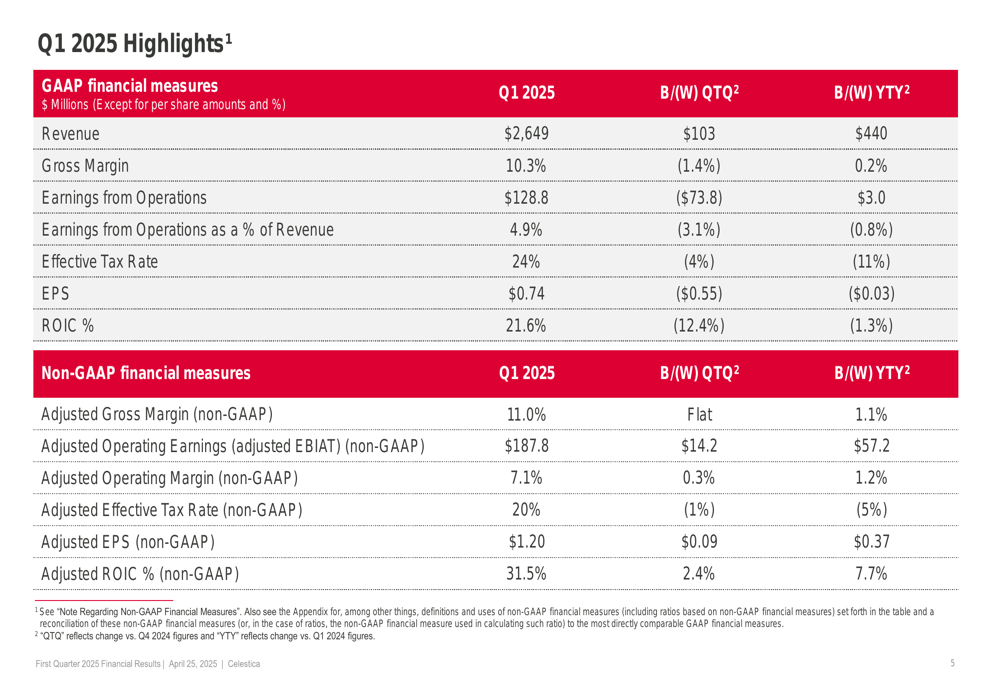

A more detailed breakdown of the financial performance shows improvements across multiple non-GAAP metrics:

Segment Analysis

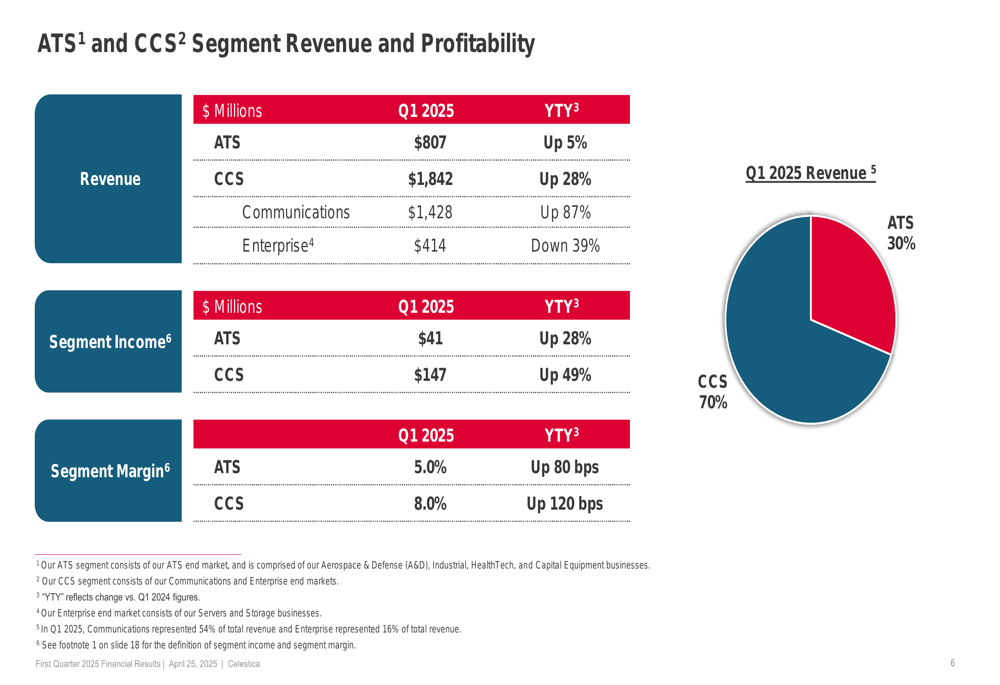

Celestica’s business is divided into two main segments: Advanced Technology Solutions (ATS) and Connectivity & Cloud Solutions (CCS). The performance between these segments varied significantly in Q1 2025.

The CCS segment was the primary growth driver, with revenue increasing 28% year-over-year to $1.842 billion. Within CCS, the Communications sub-segment saw exceptional growth of 87% year-over-year to $1.428 billion, while the Enterprise sub-segment declined by 39% to $414 million. Despite this mixed performance, CCS segment income increased by 49% year-over-year, and segment margin improved by 120 basis points to 8.0%.

The ATS segment showed more modest growth, with revenue increasing 5% year-over-year to $807 million. However, segment income for ATS increased by 28% year-over-year, and segment margin improved by 80 basis points to 5.0%.

The following chart illustrates the revenue split and performance metrics for both segments:

Balance Sheet and Cash Flow

Celestica demonstrated improved working capital management in Q1 2025, with inventory turns increasing to 5.4x (up 1.5x year-over-year). Inventory levels increased by $163 million year-over-year to $1.788 billion, while customer cash deposits for inventory decreased by $248 million to $472 million. Despite these changes, the company maintained a stable cash cycle of 69 days, just one day higher than the same period last year.

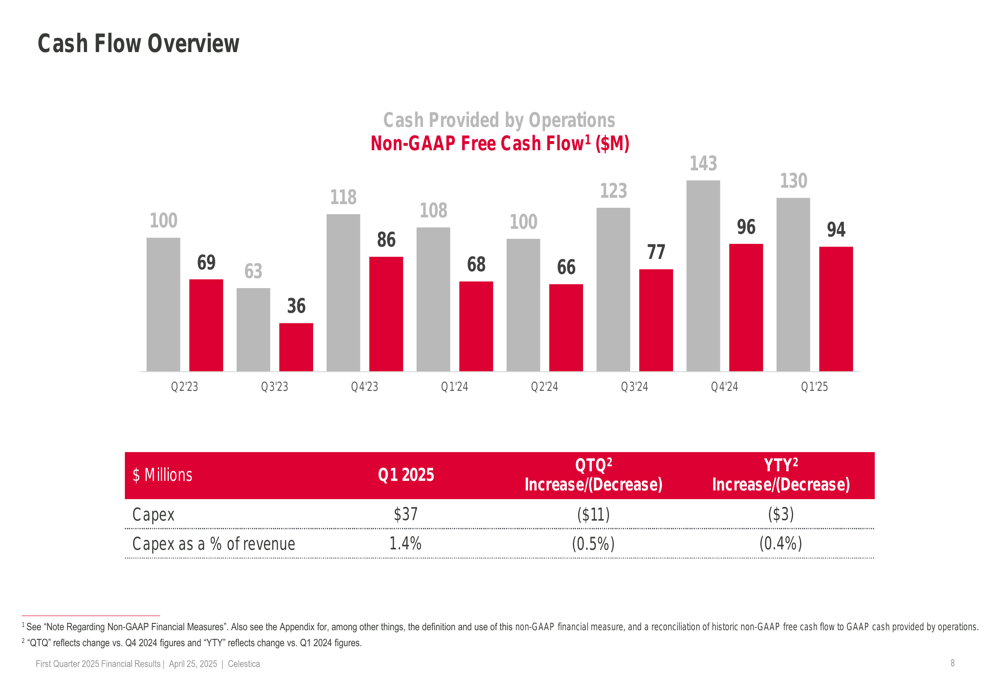

Free cash flow remained strong at $130 million for Q1 2025, continuing a positive trend over recent quarters. Capital expenditures for the quarter were $37 million, representing 1.4% of revenue.

The following chart shows the company’s free cash flow trend over recent quarters:

Celestica’s balance sheet remains solid with $303 million in cash and cash equivalents. The company reported net debt of $584 million, resulting in a non-GAAP adjusted trailing twelve-month debt leverage ratio of 1.1x. Total (EPA:TTEF) liquidity stood at approximately $900 million.

The company continued its share repurchase program, buying back $75 million worth of shares in Q1 2025 and $115 million year-to-date in 2025, demonstrating confidence in its business outlook and commitment to returning value to shareholders.

Forward Guidance

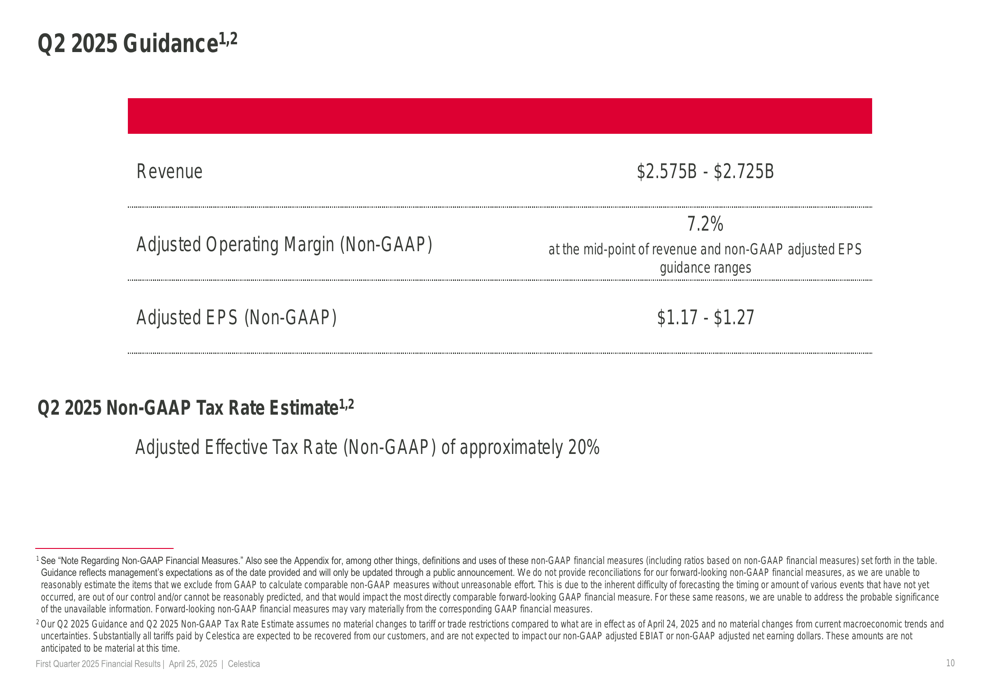

Based on its strong Q1 performance, Celestica provided optimistic guidance for Q2 2025 and raised its full-year 2025 outlook.

For Q2 2025, the company expects:

- Revenue between $2.575 billion and $2.725 billion

- Adjusted operating margin (non-GAAP) of 7.2%

- Adjusted EPS (non-GAAP) between $1.17 and $1.27

- Adjusted effective tax rate of approximately 20%

The Q2 guidance is presented in the following slide:

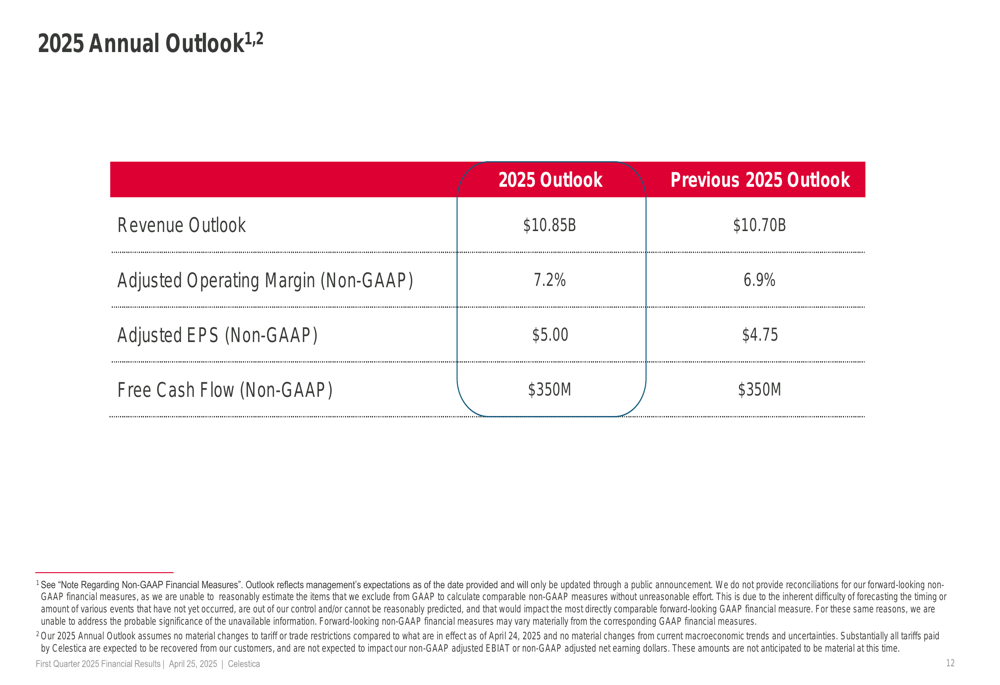

For the full year 2025, Celestica has raised its outlook:

The company now expects annual revenue of $10.85 billion, up from its previous outlook of $10.70 billion. Adjusted operating margin is projected to be 7.2%, improved from the previous 6.9% outlook. Adjusted EPS is now expected to be $5.00, up from the previous guidance of $4.75. The free cash flow outlook remains unchanged at $350 million.

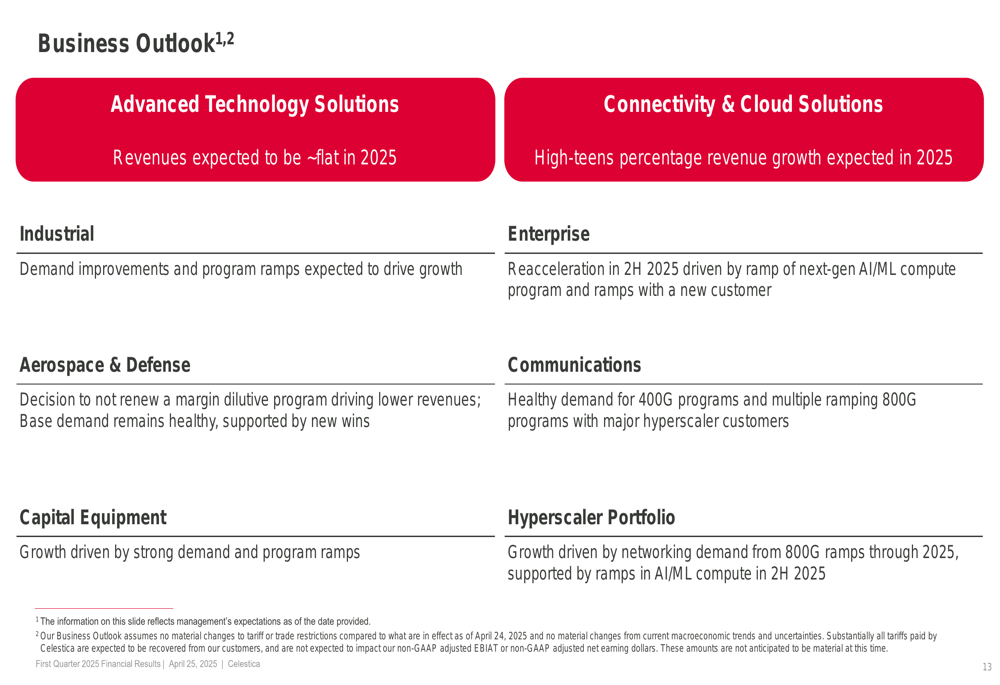

Business Outlook

Celestica provided a detailed business outlook by segment, highlighting both growth opportunities and challenges:

The ATS segment is expected to have flat revenue in 2025, with growth in Industrial and Capital Equipment offset by challenges in Aerospace & Defense, where the company decided not to renew a margin-dilutive program.

The CCS segment is expected to see high-teens percentage revenue growth in 2025. Communications growth will be driven by healthy demand for 400G programs and multiple ramping 800G programs with major hyperscaler customers. The Enterprise sub-segment is expected to reaccelerate in the second half of 2025, driven by the ramp of next-generation AI/ML compute programs and new customer relationships.

For Q2 2025 specifically, the company expects ATS revenue to be flat year-over-year, Communications revenue to increase in the high-fifties percentage range, and Enterprise revenue to decrease in the low-forties percentage range.

Executive Summary

Celestica’s Q1 2025 results demonstrate the company’s continued execution of its strategy to focus on high-growth areas like networking for hyperscalers and AI/ML compute capabilities. The strong performance in the Communications sub-segment, with 87% year-over-year growth, highlights the success of this approach.

The company’s improved profitability, with adjusted operating margin expanding by 120 basis points to 7.1%, shows that Celestica is not just growing revenue but also enhancing operational efficiency. The raised full-year outlook reflects management’s confidence in the company’s ability to maintain this momentum throughout 2025.

While challenges exist, particularly in the Enterprise sub-segment which saw a 39% year-over-year decline in Q1, the company expects a reacceleration in the second half of 2025 as new AI/ML compute programs ramp up. This suggests that Celestica is well-positioned to benefit from the ongoing digital transformation and AI revolution that is driving demand for advanced networking and computing infrastructure.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.