Lisa Cook sues Trump over firing attempt, emergency hearing set

Introduction & Market Context

Celestica Inc (NYSE:CLS) released its second quarter 2025 financial results on July 29, 2025, showcasing robust performance across key metrics and prompting the company to raise its full-year outlook. The electronics manufacturing services provider continues to capitalize on strong demand in the communications sector, particularly from hyperscaler customers investing in networking infrastructure.

The company’s stock closed at $170.22 on July 28, 2025, representing a 1.85% gain for the day. In after-hours trading, the stock dipped slightly by 0.42% to $169.50. Over the past year, Celestica (TSX:CLS) shares have shown remarkable strength, trading near their 52-week high of $173.71, significantly above their 52-week low of $40.25.

Quarterly Performance Highlights

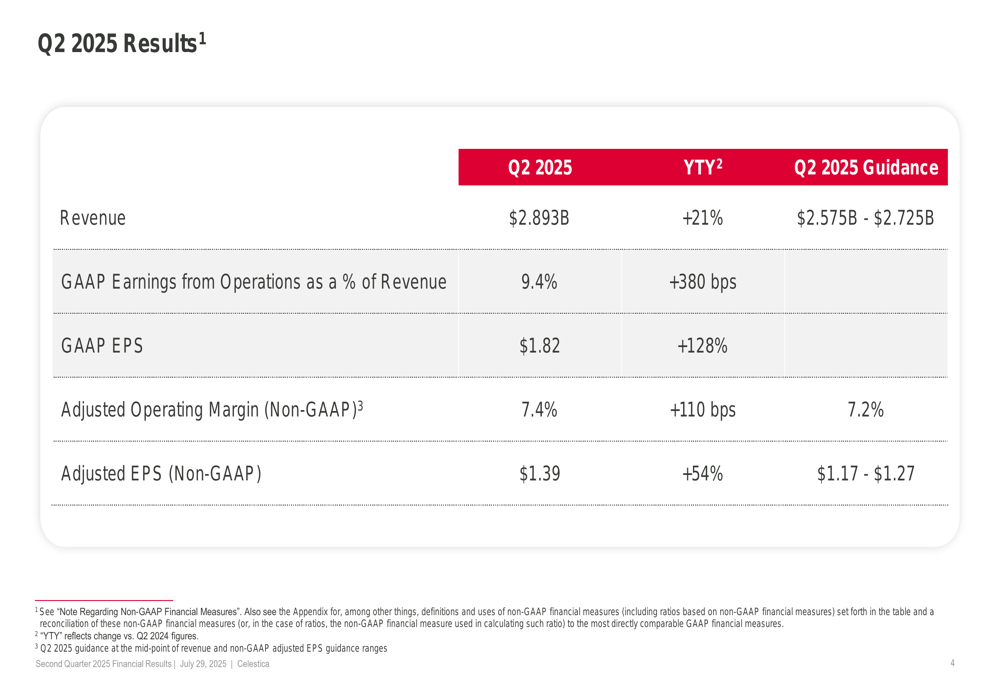

Celestica delivered exceptional second quarter results, substantially exceeding guidance across all key financial metrics. Revenue reached $2.893 billion, representing a 21% year-over-year increase and surpassing the company’s guidance range of $2.575-$2.725 billion.

As shown in the following quarterly results summary:

GAAP earnings from operations as a percentage of revenue reached 9.4%, an impressive 380 basis points improvement year-over-year. GAAP earnings per share soared to $1.82, representing a 128% increase compared to the same period last year.

On a non-GAAP basis, adjusted operating margin expanded to 7.4%, exceeding guidance of 7.2% and improving 110 basis points year-over-year. Adjusted EPS of $1.39 grew 54% year-over-year, significantly above the guided range of $1.17-$1.27.

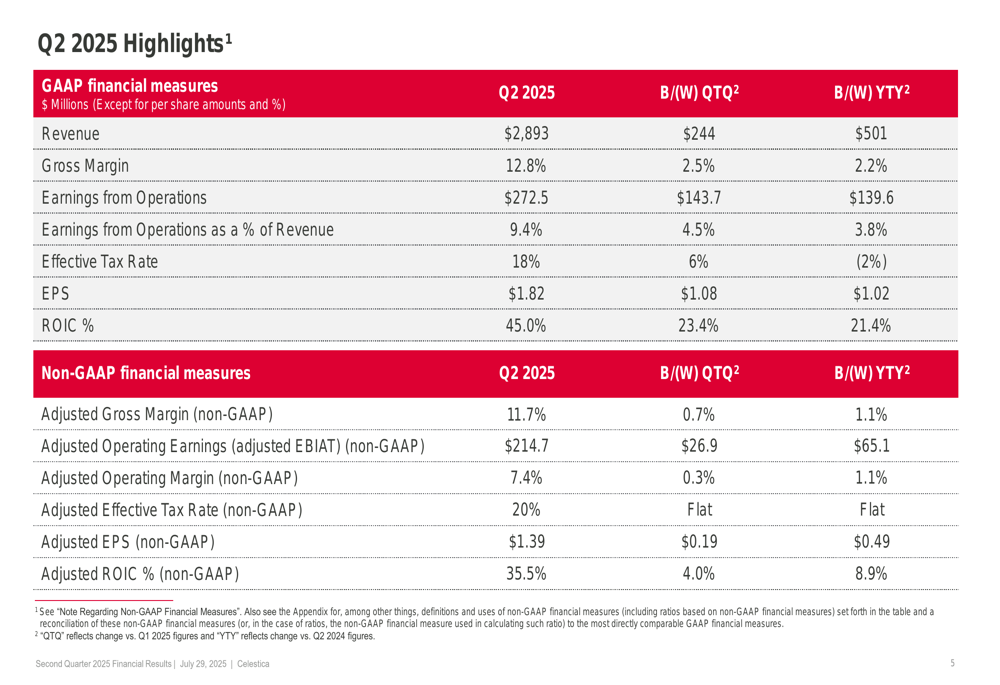

The detailed quarterly highlights further illustrate Celestica’s strong performance across multiple financial metrics:

Segment Analysis

Celestica’s business is divided into two main segments: Advanced Technology Solutions (ATS) and Connectivity & Cloud Solutions (CCS). The CCS segment, particularly the Communications sub-segment, was the primary growth driver in Q2 2025.

The segment breakdown reveals that CCS represented 72% of total revenue at $2.074 billion, growing 28% year-over-year. Within CCS, the Communications sub-segment surged 75% to $1.641 billion, while the Enterprise sub-segment declined 37% to $433 million. The ATS segment contributed $819 million, or 28% of total revenue, growing 7% year-over-year.

Profitability improved across both segments, with CCS segment margin expanding 130 basis points to 8.3% and ATS segment margin increasing 70 basis points to 5.3%.

Balance Sheet and Cash Flow

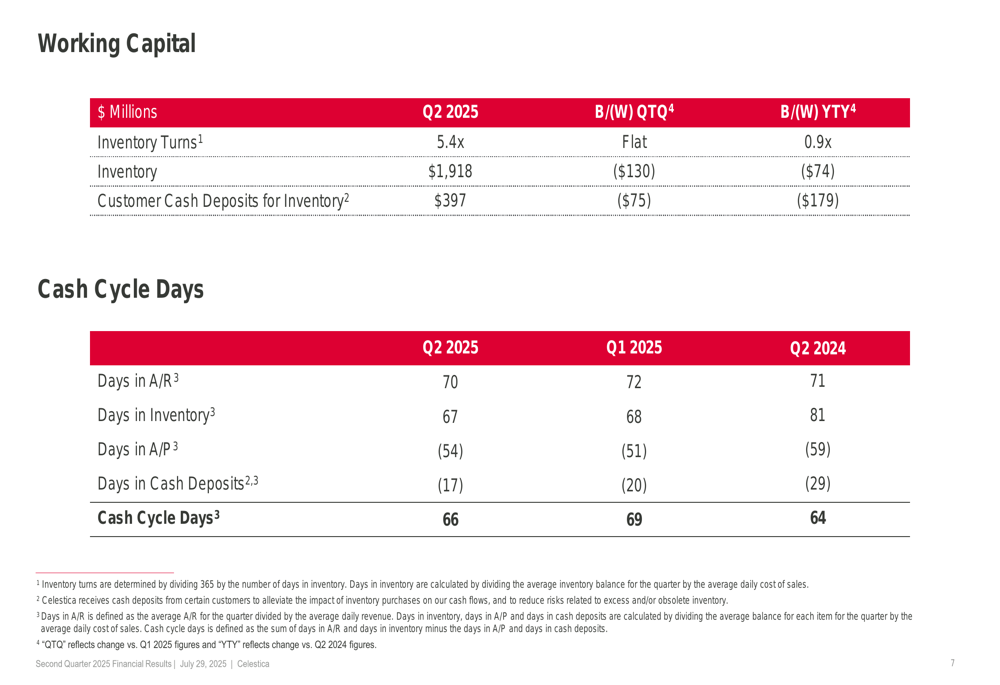

Celestica continues to demonstrate disciplined working capital management and strong cash generation. The company’s cash cycle days stood at 66 days in Q2 2025, slightly higher than the 64 days reported in Q2 2024 but improved from 69 days in Q1 2025.

Inventory management remains solid with inventory turns at 5.4x, flat quarter-over-quarter but improved by 0.9x year-over-year. Customer cash deposits for inventory increased to $397 million, up $179 million year-over-year, helping to offset the working capital impact of higher inventory levels.

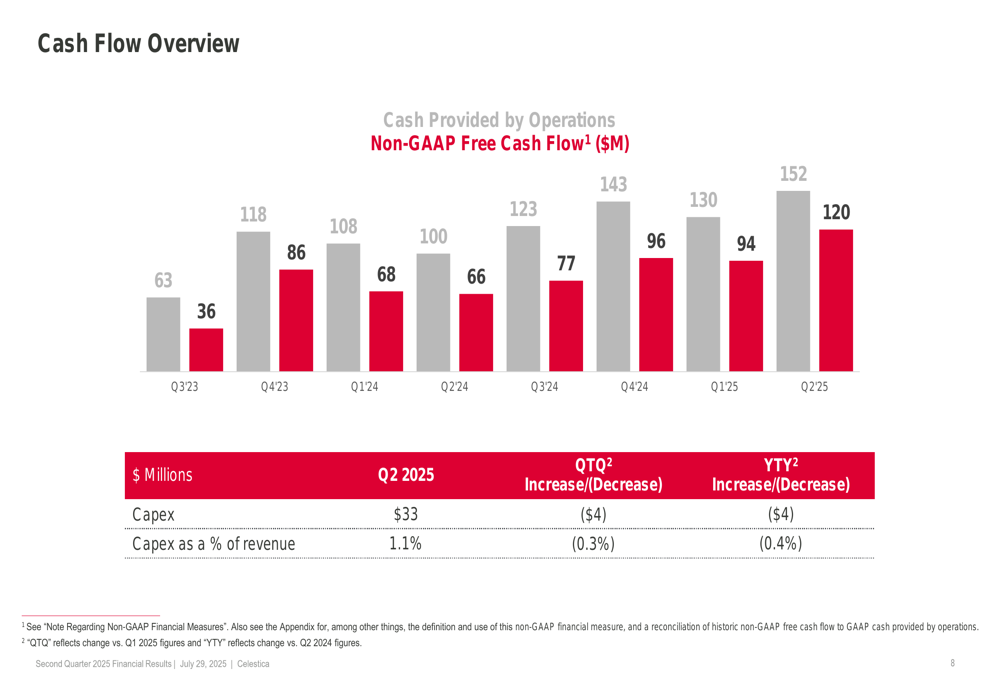

Free cash flow generation has shown consistent improvement over the past eight quarters, reaching $120 million in Q2 2025 compared to $66 million in Q2 2024. Capital expenditures were $33 million in the quarter, representing 1.1% of revenue.

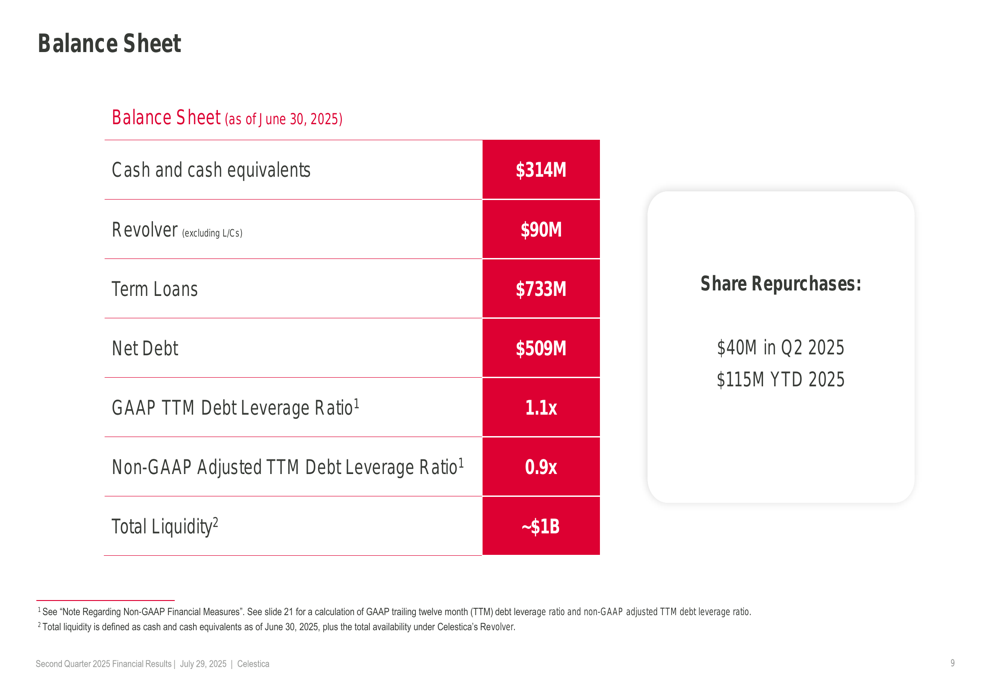

The balance sheet remains healthy with cash and cash equivalents of $314 million and total liquidity of approximately $1 billion as of June 30, 2025. Net debt stood at $509 million, resulting in a non-GAAP adjusted trailing twelve-month debt leverage ratio of 0.9x, indicating a conservative financial position.

During the quarter, Celestica continued its share repurchase program, buying back $40 million worth of shares, bringing the year-to-date total to $115 million.

Forward Guidance and Outlook

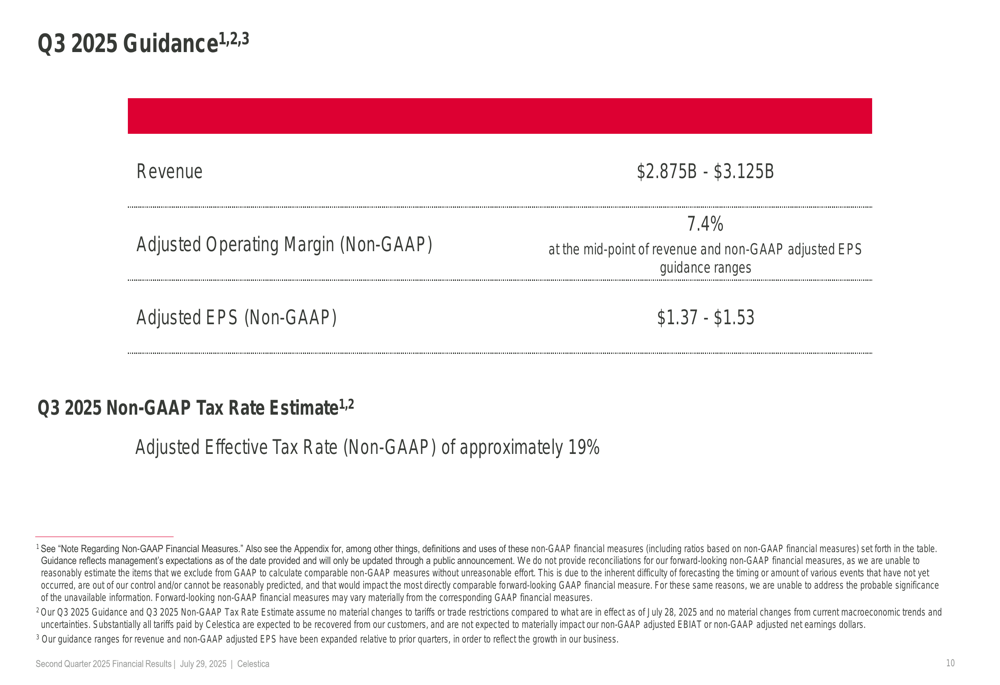

Based on its strong performance and positive business momentum, Celestica provided optimistic guidance for Q3 2025 and raised its full-year outlook.

For the third quarter, the company expects:

- Revenue between $2.875 billion and $3.125 billion

- Adjusted operating margin (non-GAAP) of 7.4%

- Adjusted EPS (non-GAAP) between $1.37 and $1.53

- Adjusted effective tax rate of approximately 19%

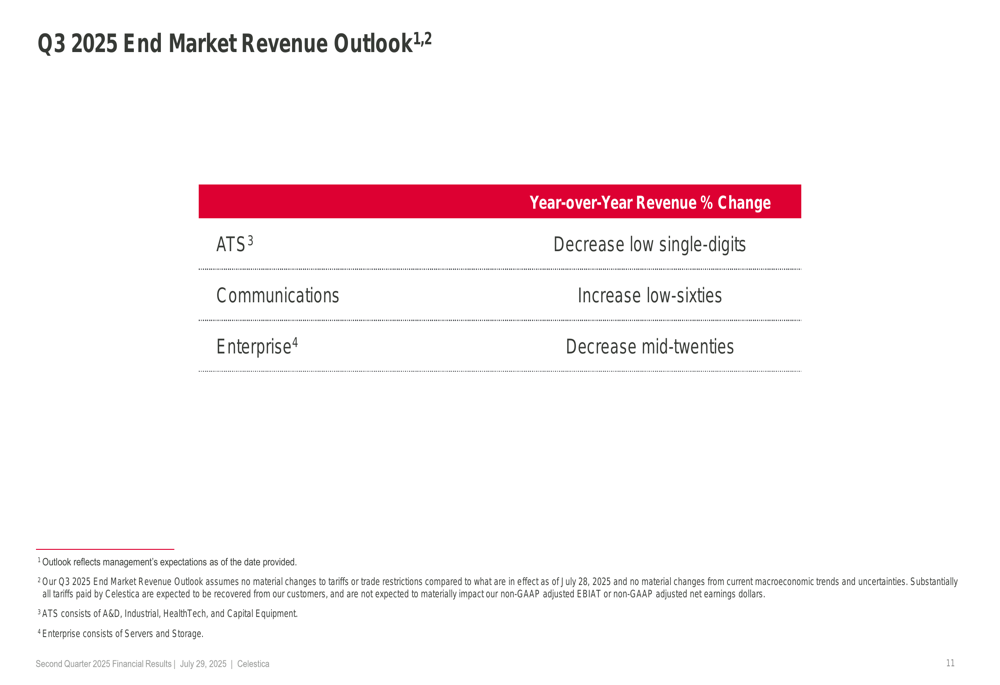

The Q3 2025 end market revenue outlook projects continued strength in Communications with a low-sixties percentage increase year-over-year, while Enterprise is expected to decrease in the mid-twenties percentage range. The ATS segment is forecasted to decrease in the low single-digits percentage range.

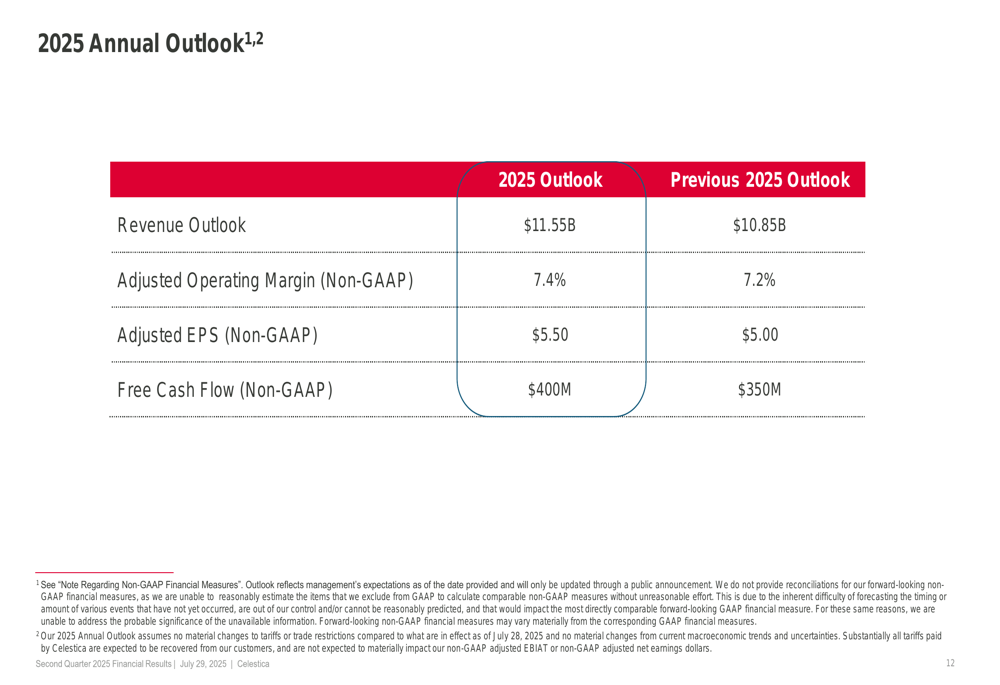

For the full year 2025, Celestica has raised its outlook across all key metrics:

- Revenue outlook increased to $11.55 billion (previously $10.85 billion)

- Adjusted operating margin (non-GAAP) raised to 7.4% (previously 7.2%)

- Adjusted EPS (non-GAAP) increased to $5.50 (previously $5.00)

- Free cash flow (non-GAAP) raised to $400 million (previously $350 million)

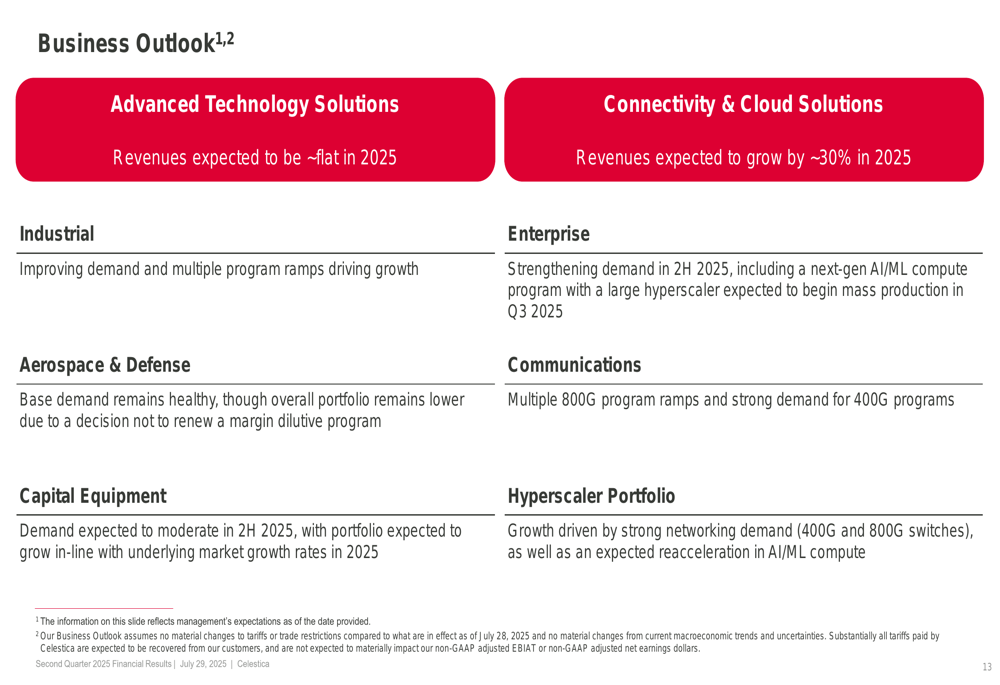

Strategic Initiatives and Business Outlook

Celestica’s business outlook for 2025 reflects the company’s strategic focus on high-growth areas, particularly in the Communications segment and hyperscaler customers. The Connectivity & Cloud Solutions segment is expected to grow by approximately 30% in 2025, driven by multiple 800G program ramps and strong demand for 400G programs.

The Advanced Technology Solutions segment is projected to be approximately flat in 2025, with varying performance across sub-segments. Industrial demand is improving with multiple program ramps driving growth. The Enterprise sub-segment is expected to strengthen in the second half of 2025, including a next-generation AI/ML compute program with a large hyperscaler beginning mass production in Q3 2025.

The Capital Equipment sub-segment demand is expected to moderate in the second half of 2025, while the Aerospace & Defense sub-segment maintains healthy base demand despite the decision not to renew a margin-dilutive program.

Overall, Celestica’s Q2 2025 results demonstrate the company’s continued execution excellence and ability to capitalize on strong demand in key growth markets, particularly in Communications and hyperscaler customers. The raised full-year outlook reflects management’s confidence in sustaining this momentum through the remainder of 2025, driven by networking infrastructure demand and emerging opportunities in AI/ML compute programs.

The company’s disciplined approach to working capital management, consistent free cash flow generation, and conservative balance sheet position it well to navigate potential market fluctuations while continuing to invest in strategic growth initiatives and return capital to shareholders through share repurchases.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.