Can anything shut down the Gold rally?

Introduction & Market Context

CellaVision AB (STO:CEVI) presented its Q1 2025 results on April 29, showcasing strong performance across all regions despite a challenging market environment. The company’s stock has responded positively to these results, with shares trading at SEK 197.6 as of April 30, representing a 2.23% increase on the day and continuing the momentum from the initial 25.16% surge following the earnings announcement.

The medical technology company, which specializes in digital cell morphology solutions, demonstrated resilience and growth in a quarter marked by solid execution of its strategic initiatives. CellaVision’s performance reflects the growing adoption of its digital solutions in laboratory hematology workflows worldwide.

Quarterly Performance Highlights

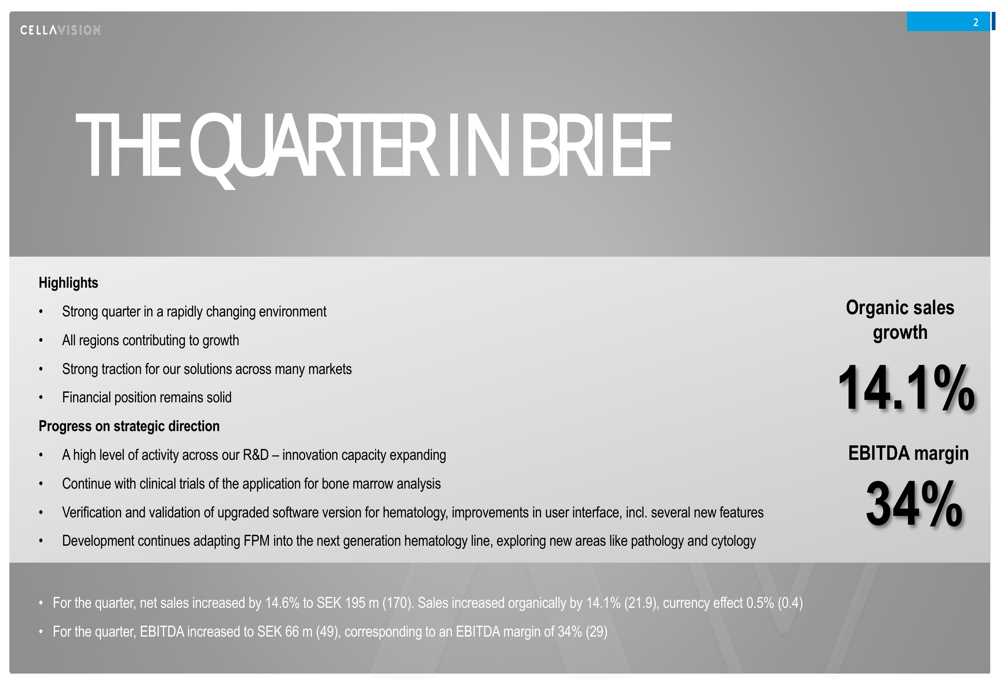

CellaVision reported impressive financial results for Q1 2025, with net sales increasing by 14.6% to SEK 195 million compared to SEK 170 million in the same period last year. Organic growth reached 14.1%, with a modest currency effect of 0.5%.

As shown in the following quarterly summary:

Profitability metrics showed significant improvement, with EBITDA increasing to SEK 66 million from SEK 49 million in Q1 2024. This resulted in an EBITDA margin of 34%, up from 29% in the previous year. The company maintained its strategic focus on innovation, with R&D spending at 22% of sales, slightly higher than the 21% reported in Q1 2024.

CEO Simon Østergaard emphasized the company’s strong position, stating during the earnings call: "We do believe that in isolation, Q1 is a strong quarter." He also highlighted the company’s strategic focus, saying: "We are fully committed to execute on the power of focus."

Detailed Financial Analysis

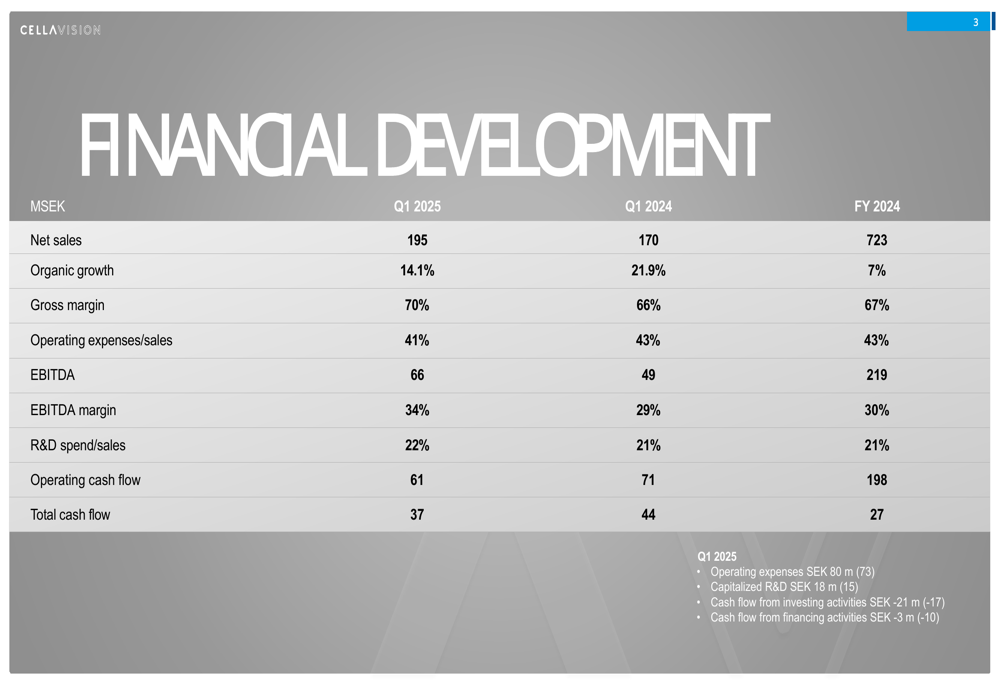

CellaVision’s financial performance shows improvement across multiple metrics. The company achieved a gross margin of 70% in Q1 2025, up from 66% in the same period last year, indicating enhanced operational efficiency and a favorable product mix.

The detailed financial breakdown reveals:

Operating expenses as a percentage of sales improved to 41% from 43% in Q1 2024, demonstrating the company’s ability to scale efficiently. Operating cash flow remained strong at SEK 61 million, though slightly lower than the SEK 71 million reported in Q1 2024. The company maintained a solid balance sheet with minimal debt, positioning it well for continued investment in growth initiatives.

The financial results align with CellaVision’s long-term ambitions of achieving a compound annual growth rate (CAGR) of approximately 15% and an EBITDA margin exceeding 30% over the economic cycle.

Regional Performance

CellaVision reported growth across all its geographical regions, with particularly strong performance in EMEA. The regional breakdown provides insights into the company’s global market penetration:

The EMEA region led growth with a 21% increase in sales to SEK 96 million, driven primarily by CellaVision™ DI-60 and CellaVision® DC-1 instruments. Reagent sales in this region also showed healthy growth of 12% compared to Q1 2024, reflecting the success of the company’s close collaboration with strategic distribution partners.

The Americas region saw an 8% increase in sales to SEK 78 million, with growth driven by software and CellaVision® DC-1 instruments in the U.S. market. Meanwhile, the APAC region delivered 12% growth to SEK 21 million, with strong momentum in key markets like Japan and China, where demand for CellaVision™ DI-60 instruments remained robust.

Product Group Analysis

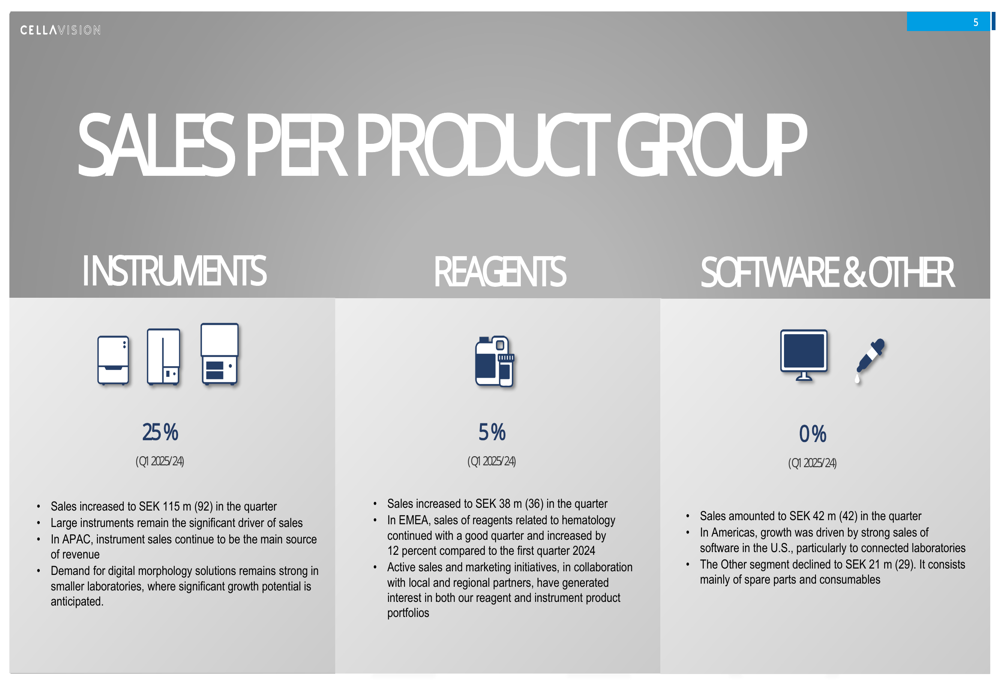

CellaVision’s product portfolio performance reveals varying growth rates across its three main product categories:

Instruments emerged as the strongest growth driver, with sales increasing by 25% to SEK 115 million compared to SEK 92 million in Q1 2024. Large instruments continued to be a significant contributor to overall sales.

Reagent sales grew by 5% to SEK 38 million, with increased sales specifically in hematology-related reagents. The Software (ETR:SOWGn) & Other category remained flat at SEK 42 million year-over-year, though the company noted strong software sales in the Americas region.

This product mix shift toward instruments suggests laboratories are continuing to invest in CellaVision’s core technology platforms, creating opportunities for future recurring revenue through reagents and software.

Strategic Initiatives & Outlook

CellaVision continues to invest in research and development, with multiple initiatives underway to enhance its product offerings. The company highlighted ongoing clinical trials for bone marrow analysis and verification and validation of upgraded software for hematology improvements.

The company’s key takeaways and financial ambitions are summarized in the following slide:

Looking forward, CellaVision remains optimistic about its growth prospects, maintaining its financial ambitions of approximately 15% CAGR and an EBITDA margin exceeding 30% over the economic cycle. The company’s solid financial position, with minimal debt and growing cash reserves, provides a strong foundation for continued investment in innovation and market expansion.

The company has scheduled its Annual General Meeting for May 6, 2025, with subsequent financial reports planned for July 18 (Q2) and November 6 (Q3), followed by the 2025 year-end bulletin on February 5, 2026.

With its continued focus on innovation, strategic partnerships, and global market expansion, CellaVision appears well-positioned to maintain its growth trajectory in the digital cell morphology market, despite potential challenges from regulatory compliance costs, supply chain disruptions, and competitive pressures in key markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.