Bank of America just raised its EUR/USD forecast

Introduction & Market Context

Cementir Holding, part of the Caltagirone Group, presented its first quarter 2025 results on May 8, highlighting a period of stable overall performance despite facing significant regional variations and currency headwinds. The company managed to maintain revenue and EBITDA levels in line with the previous year, even as cement volumes declined and certain regional markets faced challenges.

The results come amid what the company described as a "very uncertain commercial and geopolitical backdrop," with specific mention of the Turkish government’s ban on exports to Israel (active since Q2 2024) and significant currency depreciation in both Turkey and Egypt.

Quarterly Performance Highlights

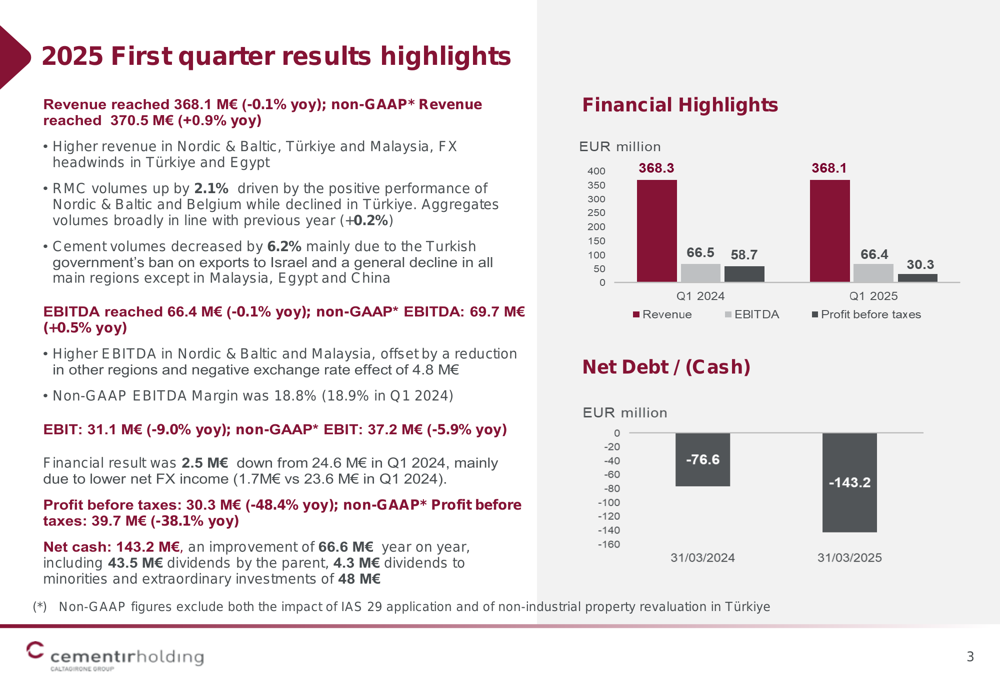

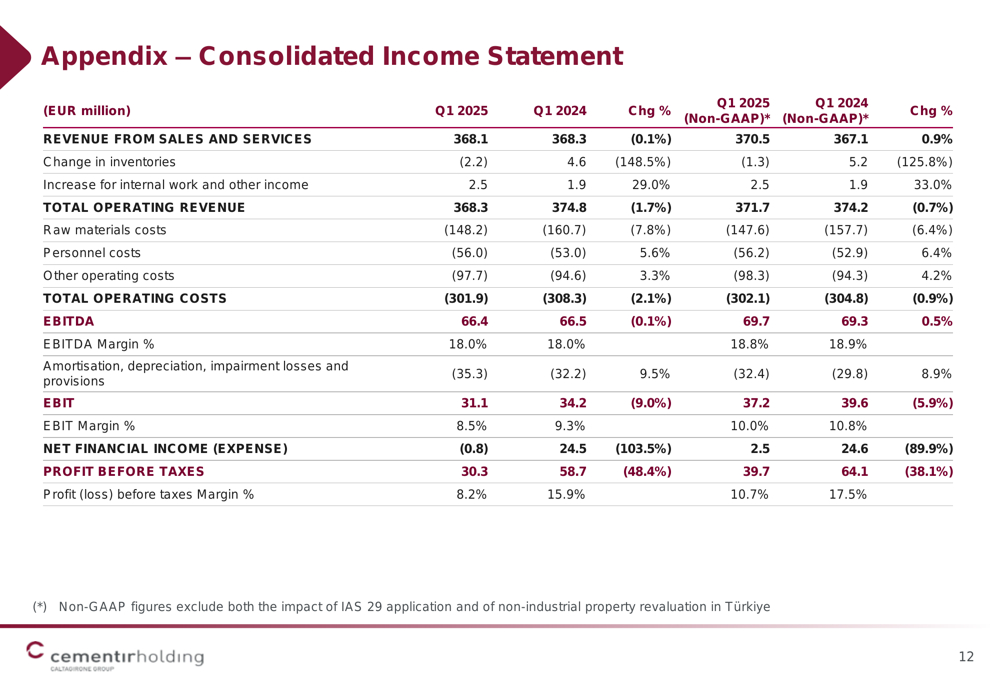

Cementir reported revenue of €368.1 million for Q1 2025, representing a marginal decline of 0.1% year-over-year. On a non-GAAP basis, revenue reached €370.5 million, up 0.9% compared to the same period in 2024. EBITDA remained essentially flat at €66.4 million (-0.1% year-over-year), with non-GAAP EBITDA at €69.7 million (+0.5%).

As shown in the following chart of quarterly financial performance, profit before taxes saw a significant decline of 48.4% to €30.3 million, down from €58.7 million in Q1 2024:

This substantial decrease in profit before taxes was primarily attributed to lower net foreign exchange income, which fell to €1.7 million from €23.6 million in Q1 2024. The previous year’s figure had included extraordinary income related to the Egyptian pound’s devaluation against the Euro.

Despite these challenges, Cementir’s balance sheet continued to strengthen, with net cash reaching €143.2 million, an improvement of €66.6 million year-over-year. This improvement came despite dividend payments of €43.5 million by the parent company, €4.3 million to minorities, and extraordinary investments of €48 million.

Regional Performance Analysis

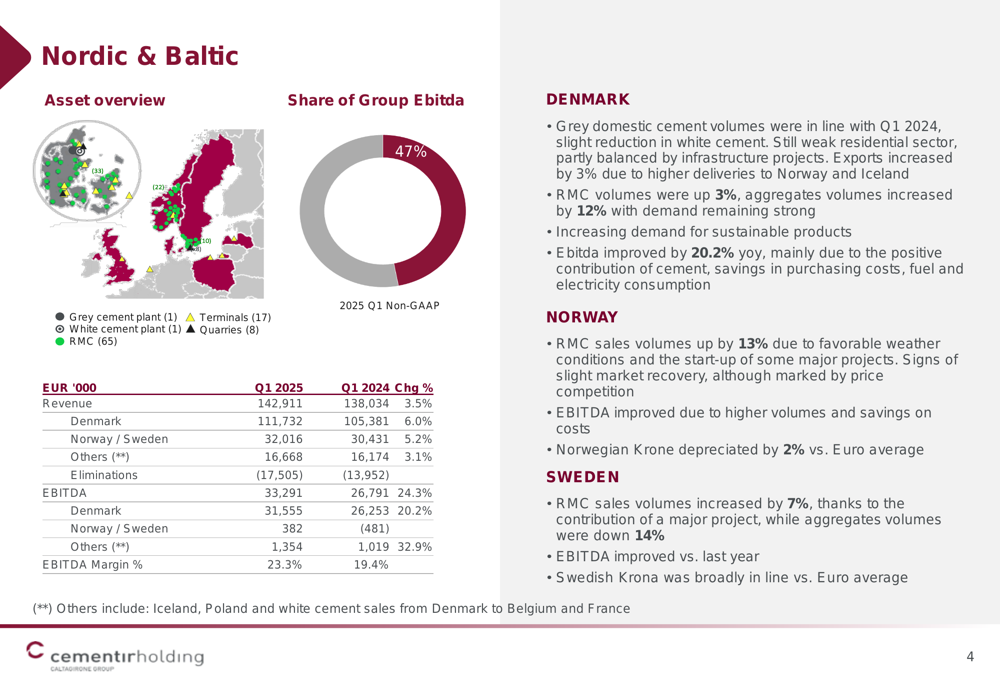

The company’s performance varied significantly across regions, with the Nordic & Baltic area emerging as the standout performer. This region, which contributes 47% of the Group’s EBITDA, saw revenue increase by 3.5% to €142.9 million and EBITDA jump by 24.3% to €33.3 million, resulting in an EBITDA margin improvement from 19.4% to 23.3%.

The following breakdown illustrates the Nordic & Baltic region’s strong performance:

In Denmark, grey domestic cement volumes remained in line with Q1 2024, while exports increased by 3% due to higher deliveries to Norway and Iceland. Ready-mix concrete (RMC) volumes were up 3%, and aggregates volumes increased by 12% with demand remaining strong. The region’s EBITDA improvement was mainly attributed to the positive contribution of cement, savings in purchasing costs, and reduced fuel and electricity consumption.

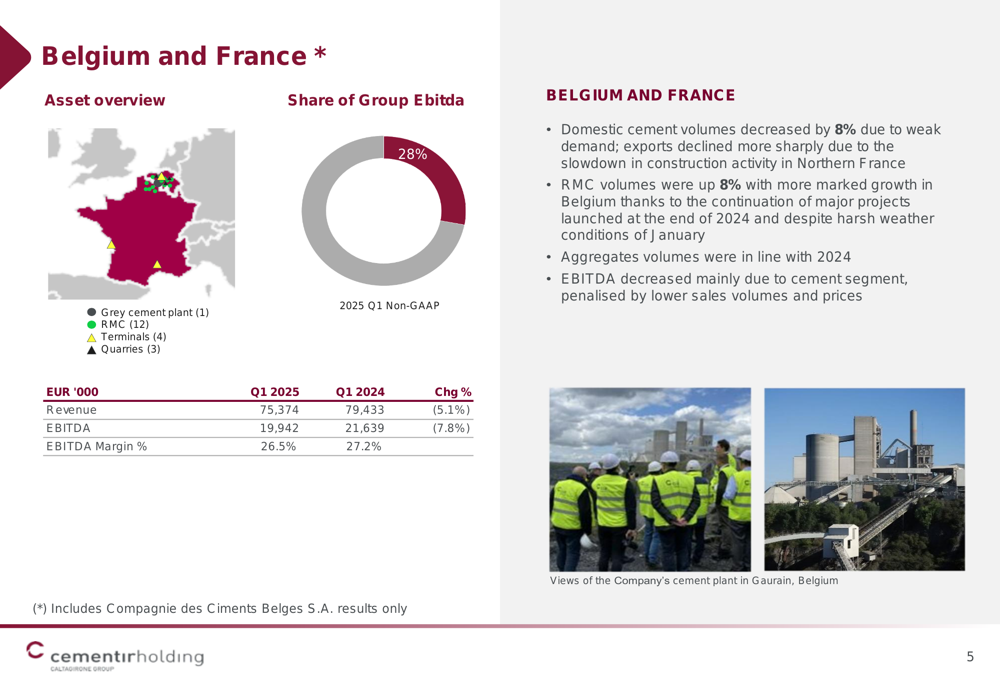

In contrast, Belgium and France, which account for 28% of Group EBITDA, experienced a 5.1% decline in revenue to €75.4 million and a 7.8% decrease in EBITDA to €19.9 million:

The Turkish market, representing 11% of Group EBITDA, faced significant challenges. While revenue increased by 5.7% to €77.4 million on a non-GAAP basis, EBITDA declined by 14.3% to €7.9 million. The Turkish lira’s 14% devaluation against the Euro contributed to these results, as did a 5% decrease in domestic cement volumes and a dramatic 54% decline in cement and clinker exports, largely due to the government’s ban on exports to Israel.

North America, contributing 6% of Group EBITDA, saw revenue decline by 3% to €41.3 million and EBITDA fall by 18.8% to €4.1 million, with white cement volumes down 7%. The U.S. dollar’s 3% revaluation against the Euro partially offset these declines.

The Asia Pacific region, accounting for 4% of Group EBITDA, delivered mixed results with overall revenue increasing by 6.8% to €22 million, driven by a 17% increase in Malaysia due to higher export volumes. However, EBITDA declined by 18.7% to €2.5 million, with China experiencing lower selling prices.

Egypt, representing 3% of Group EBITDA, saw revenue decline by 7.5% to €11.4 million and EBITDA decrease by 27.6% to €2.4 million, primarily due to the 38% depreciation of the Egyptian pound.

Forward-Looking Statements

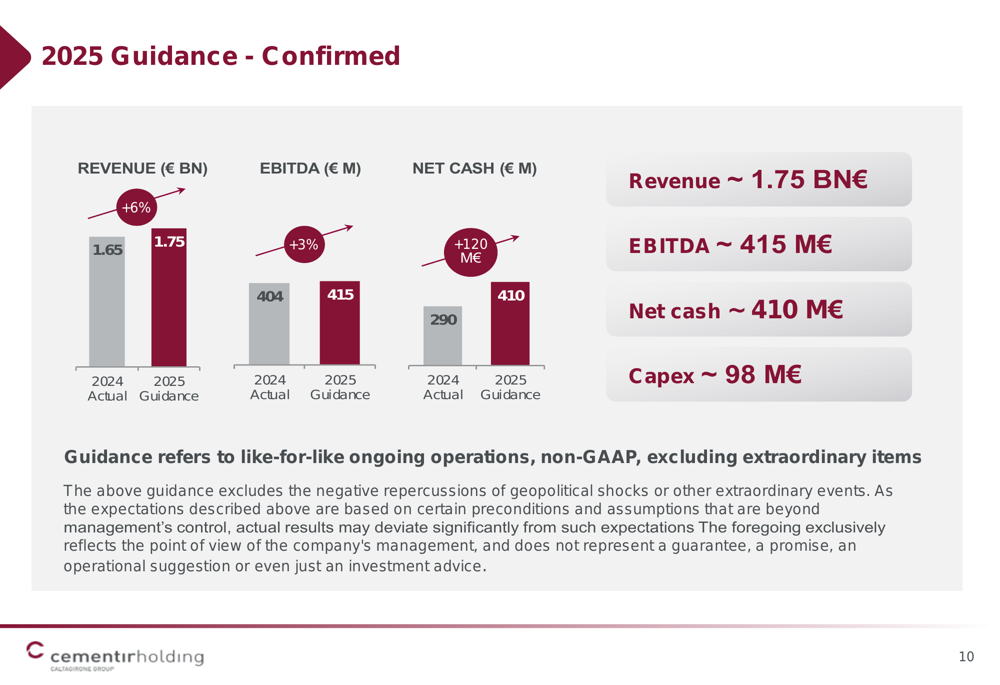

Despite the mixed regional performance and ongoing geopolitical uncertainties, Cementir confirmed its full-year 2025 guidance, projecting revenue of approximately €1.75 billion (a 6% increase from €1.65 billion in 2024) and EBITDA of around €415 million (up 3% from €404 million in 2024).

The company also forecasts its net cash position to improve to approximately €410 million by year-end, representing a substantial increase of €120 million compared to the €290 million reported at the end of 2024. Capital expenditures are expected to reach approximately €98 million for the year.

As illustrated in the following chart comparing 2025 guidance to 2024 actual results:

The company’s consolidated income statement provides additional context for understanding the financial performance and outlook:

Cementir’s ability to maintain stable overall performance despite regional challenges and currency headwinds demonstrates the benefits of its geographic diversification strategy. The strong performance in the Nordic & Baltic region has effectively counterbalanced weaknesses in other markets, allowing the company to maintain its full-year guidance despite acknowledging the uncertain commercial and geopolitical environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.