Stock market today: S&P 500 hits fresh record close on stronger economic growth

Introduction & Market Context

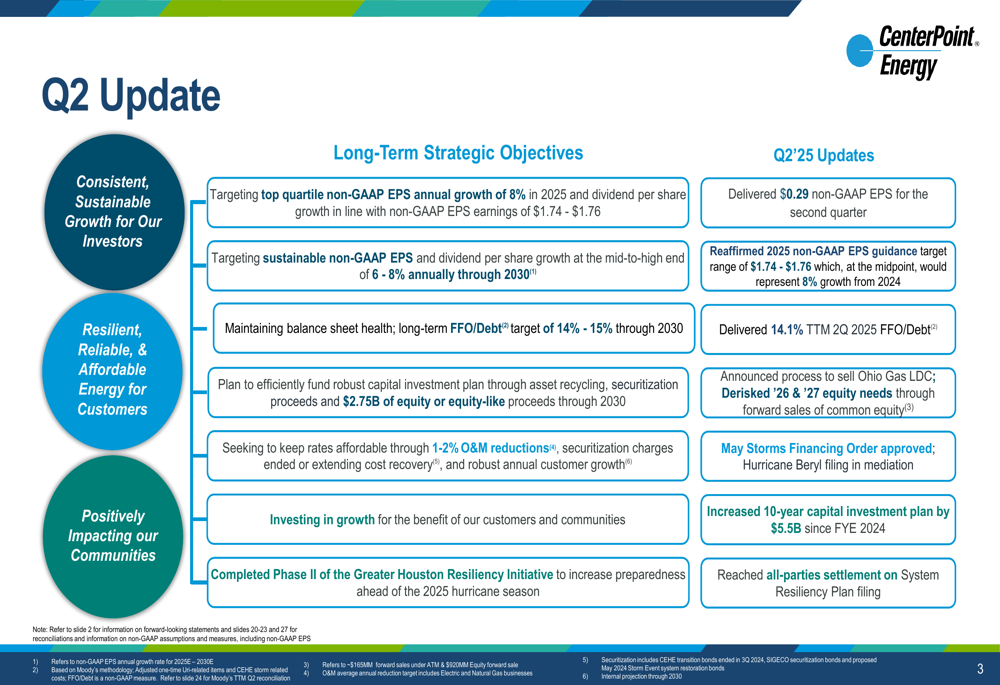

CenterPoint Energy (NYSE:CNP) released its second quarter 2025 investor presentation on July 24, revealing a decrease in quarterly earnings while maintaining its full-year guidance and announcing a significant expansion of its long-term capital investment plan. The utility reported non-GAAP earnings per share (EPS) of $0.29 for Q2 2025, down from $0.36 in the same period last year. Despite this decline, the company reaffirmed its 2025 guidance range of $1.74-$1.76 per share, which represents 8% growth at the midpoint compared to 2024.

The stock closed at $37.12 on July 23, 2025, down 1.69% for the day, but remains near its 52-week high of $39.31. Year-to-date, CenterPoint shares have delivered strong performance, reflecting investor confidence in the company’s long-term growth strategy despite the quarterly earnings dip.

As shown in the following strategic objectives and updates slide, CenterPoint delivered $0.29 non-GAAP EPS for the second quarter while maintaining strong balance sheet metrics:

Quarterly Performance Highlights

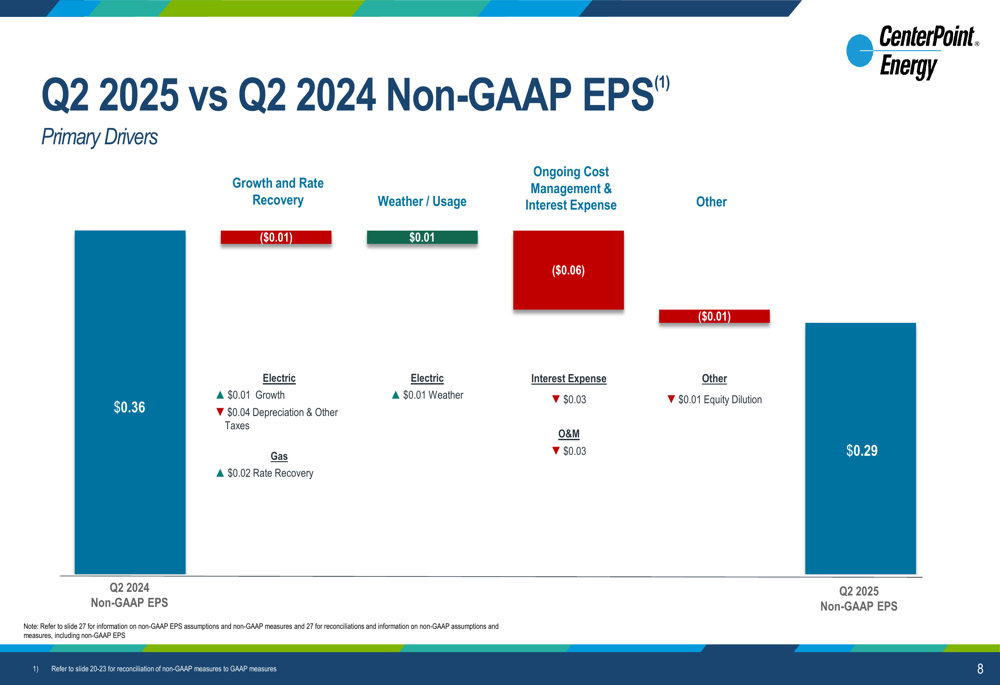

CenterPoint’s Q2 2025 non-GAAP EPS of $0.29 represented a 19.4% decrease from $0.36 in Q2 2024. The company attributed this decline to several factors, including higher interest expenses, increased operational costs, and equity dilution, which were partially offset by rate recovery and favorable weather conditions.

The following waterfall chart breaks down the key drivers of the year-over-year EPS change:

For the first half of 2025, CenterPoint has achieved cumulative non-GAAP earnings of $0.81 per share. The company noted that its 2025 earnings profile differs from typical years due to the timing of recovery for Texas investments following recent rate cases, with a higher proportion of earnings expected in the second half of the year.

Customer growth remained solid across both electric and natural gas segments, with electric customer count increasing 2% and natural gas customers growing 1% compared to Q2 2024. Total (EPA:TTEF) electric throughput rose 4% year-over-year, while natural gas throughput increased 3%, indicating healthy demand across CenterPoint’s service territories.

Strategic Initiatives

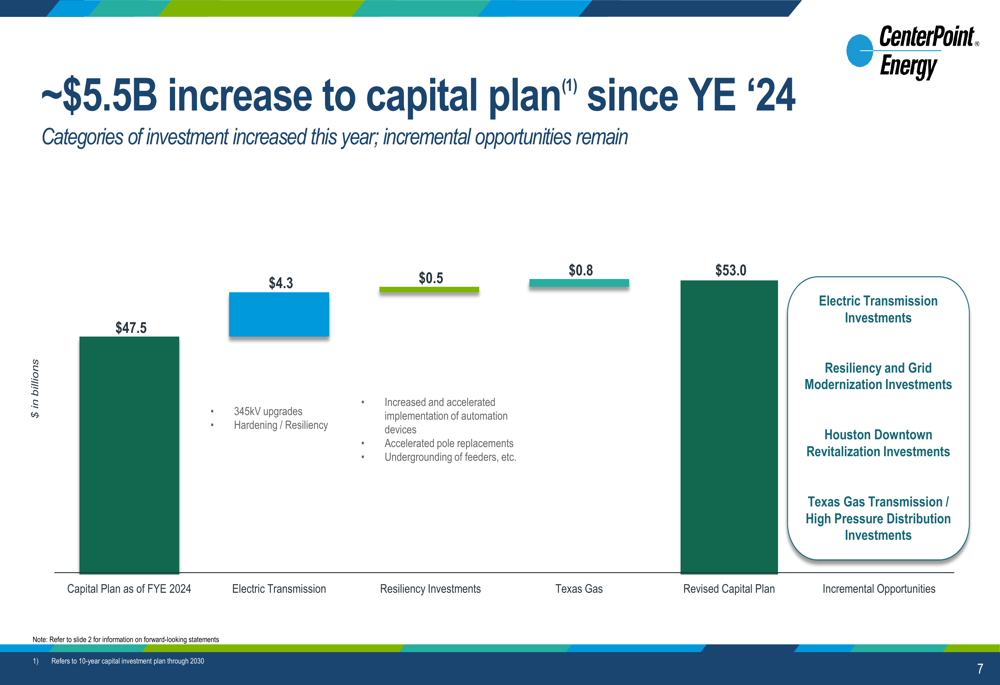

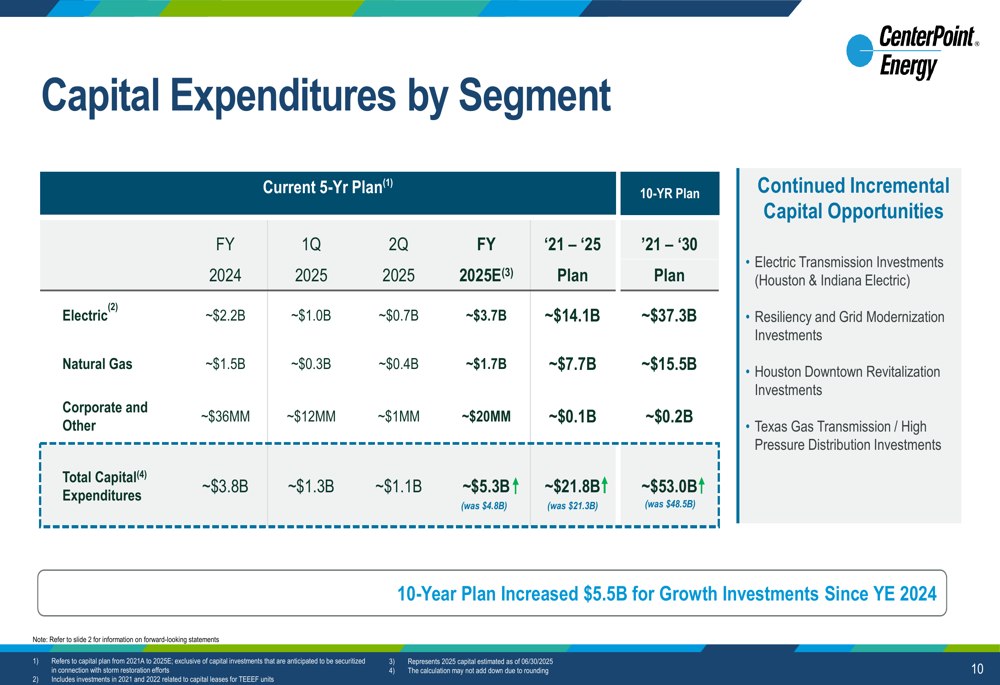

A centerpiece of CenterPoint’s presentation was the announcement of a $5.5 billion increase to its 10-year capital investment plan since year-end 2024, bringing the total to $53.0 billion through 2030. This expansion primarily targets electric transmission ($4.3B), resiliency investments ($0.5B), and Texas gas infrastructure ($0.8B).

The following chart illustrates the components of this capital plan increase:

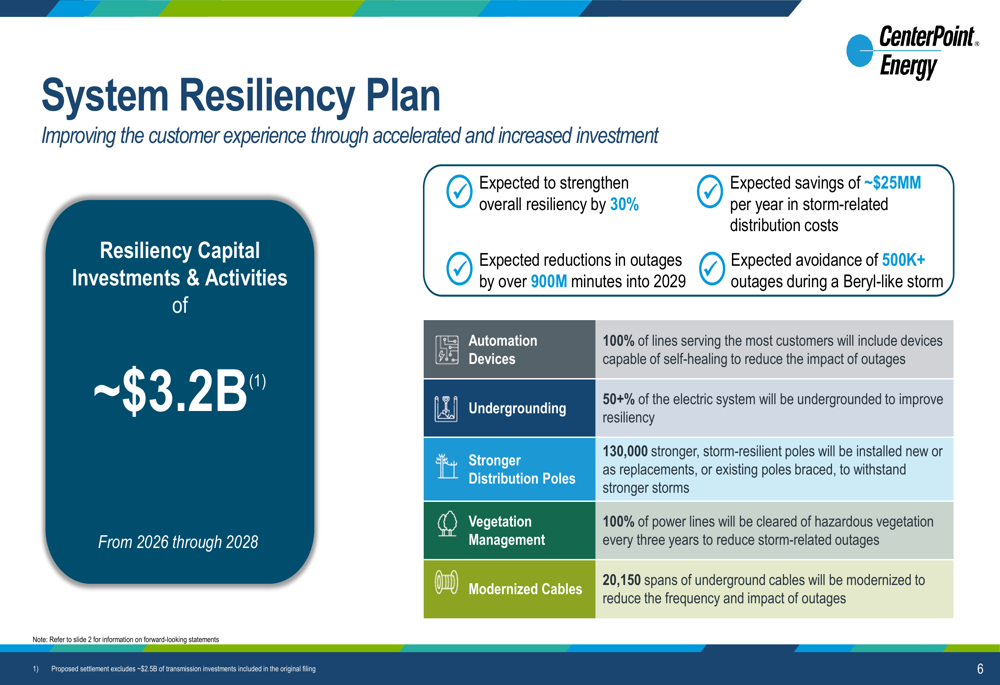

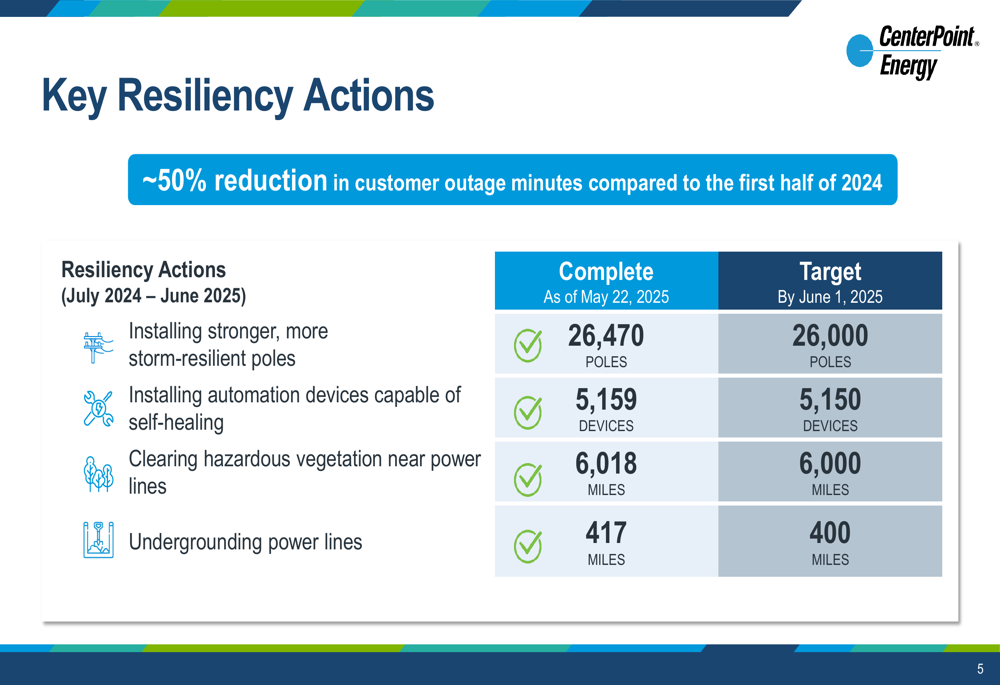

The company also highlighted its System Resiliency Plan, which includes approximately $3.2 billion in investments from 2026 through 2028. This plan aims to strengthen overall grid resiliency by 30%, reduce outages by over 900 million minutes into 2029, and save approximately $25 million per year in storm-related distribution costs.

As shown in the following slide, the resiliency plan encompasses multiple initiatives including automation devices, undergrounding, stronger distribution poles, vegetation management, and cable modernization:

CenterPoint reported significant progress on its current resiliency actions, noting an approximate 50% reduction in customer outage minutes compared to the first half of 2024. The company has exceeded its targets for installing storm-resilient poles, automation devices, vegetation clearing, and undergrounding power lines.

On the strategic front, CenterPoint announced it has initiated a process to sell its Ohio Gas local distribution company (LDC), which would further streamline its portfolio. The company also noted it has derisked its 2026 and 2027 equity needs through forward sales of common equity.

Detailed Financial Analysis

CenterPoint’s capital expenditures for Q2 2025 totaled $1.1 billion, with $0.7 billion allocated to electric operations and $0.4 billion to natural gas. For the full year 2025, the company expects capital expenditures of approximately $5.3 billion, as part of its expanded long-term investment plan.

The following table provides a detailed breakdown of capital expenditures by segment:

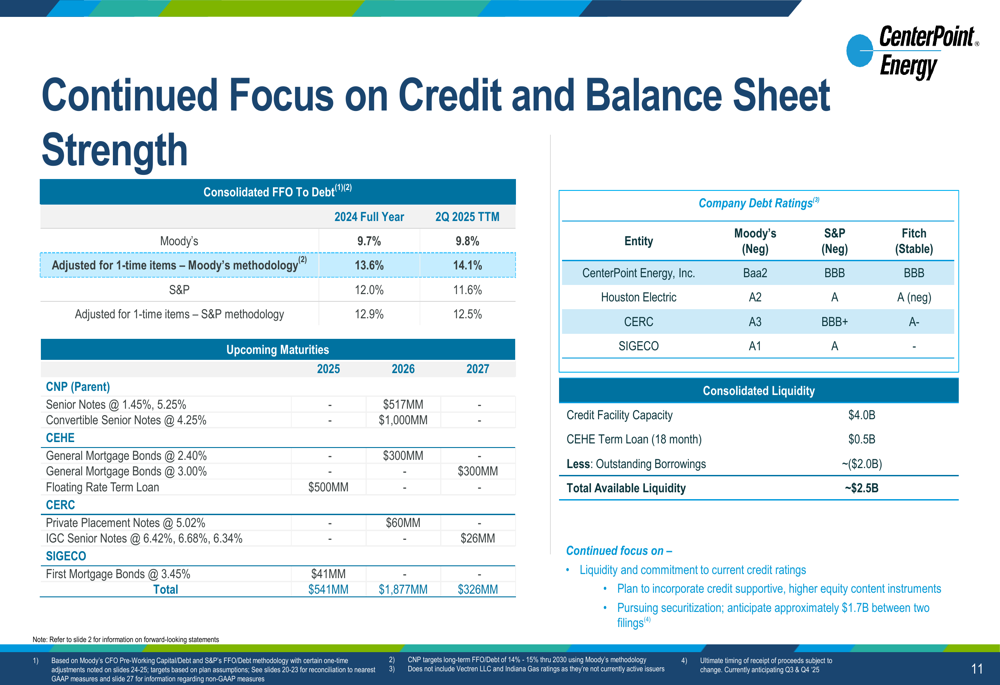

The company maintained strong credit metrics, reporting a trailing twelve-month funds from operations (FFO) to debt ratio of 14.1% using Moody’s methodology, adjusted for one-time items. This exceeds CenterPoint’s long-term FFO/Debt target of 14-15% through 2030.

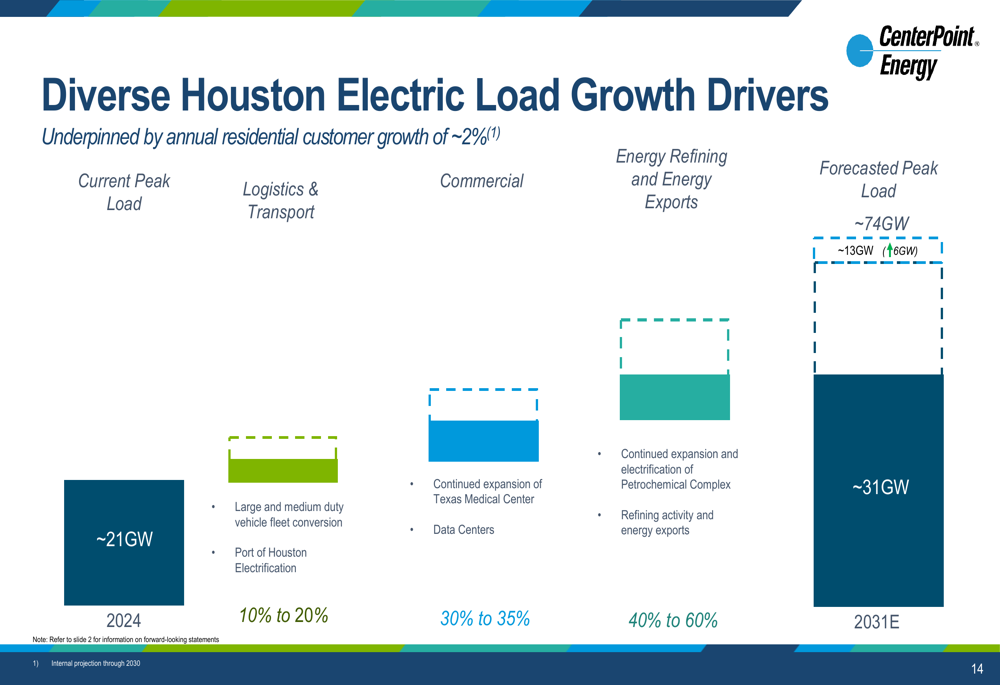

CenterPoint highlighted its diverse Houston electric load growth drivers, with energy refining and exports accounting for 40-60% of growth, commercial customers representing 30-35%, and logistics and transport contributing 10-20%. The company projects peak load to increase from approximately 21GW in 2024 to 74GW by 2031, underscoring the significant growth opportunities in its service territories.

Forward-Looking Statements

Despite the Q2 earnings decline, CenterPoint reaffirmed its 2025 non-GAAP EPS guidance range of $1.74-$1.76, which represents 8% growth at the midpoint compared to 2024. The company also reiterated its long-term objectives, including:

- Targeting sustainable non-GAAP EPS and dividend per share growth at the mid-to-high end of 6-8% annually through 2030

- Maintaining balance sheet health with a long-term FFO/Debt target of 14-15% through 2030

- Efficiently funding its capital investment plan through asset recycling, securitization proceeds, and $2.75 billion of equity or equity-like proceeds through 2030

- Keeping rates affordable through 1-2% O&M reductions, securitization charges ended or extending cost recovery, and robust annual customer growth

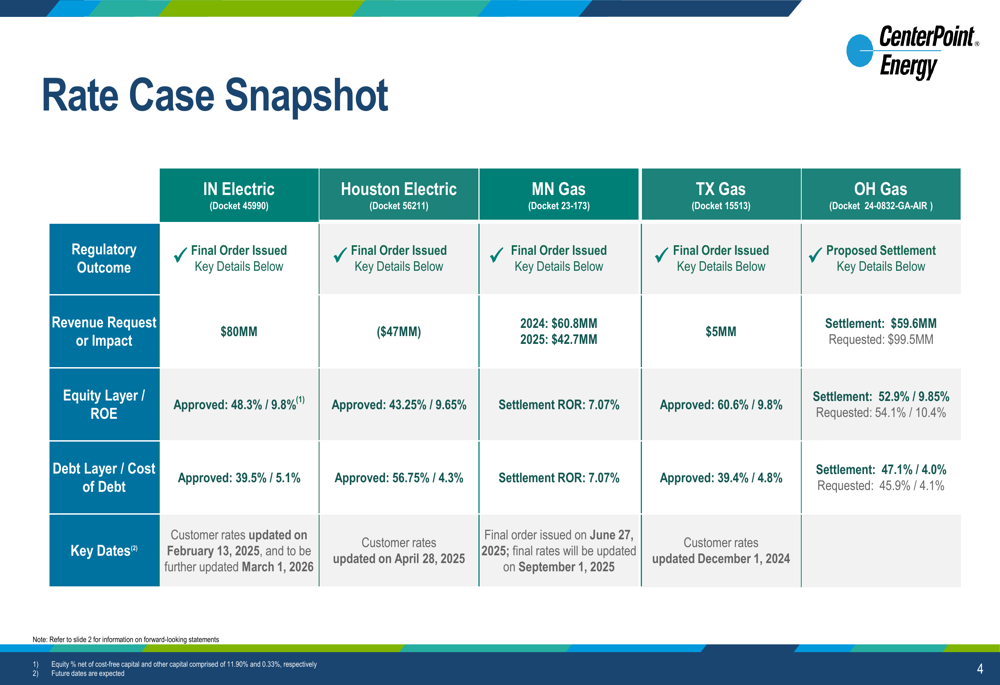

The company provided an update on its regulatory proceedings, noting that the May Storms Financing Order was approved, while the Hurricane Beryl filing is in mediation. CenterPoint also reached an all-parties settlement on its System Resiliency Plan filing, which should facilitate implementation of its infrastructure improvement initiatives.

CenterPoint’s presentation emphasized its continued focus on grid resiliency and infrastructure modernization, positioning the company to capitalize on the growing demand for reliable energy services while delivering sustainable long-term shareholder value despite the near-term earnings challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.