Japan PPI inflation slips to 11-mth low in July

Introduction & Market Context

Central Pacific Financial Corp (NYSE:CPF), the parent company of Central Pacific Bank, presented its first quarter 2025 earnings results on April 23, 2025, highlighting improved profitability driven by net interest margin expansion and a resilient Hawaii economy. The company’s stock has responded positively, rising 3.32% to $26.97 following the earnings release, with premarket trading showing continued momentum with an additional 1.15% gain.

The bank’s Q1 2025 performance shows meaningful improvement over the previous quarter, with net income reaching $17.8 million compared to $11.3 million in Q4 2024. This performance comes amid a favorable economic backdrop in Hawaii, characterized by low unemployment, strong real estate values, and a recovering tourism sector.

Quarterly Performance Highlights

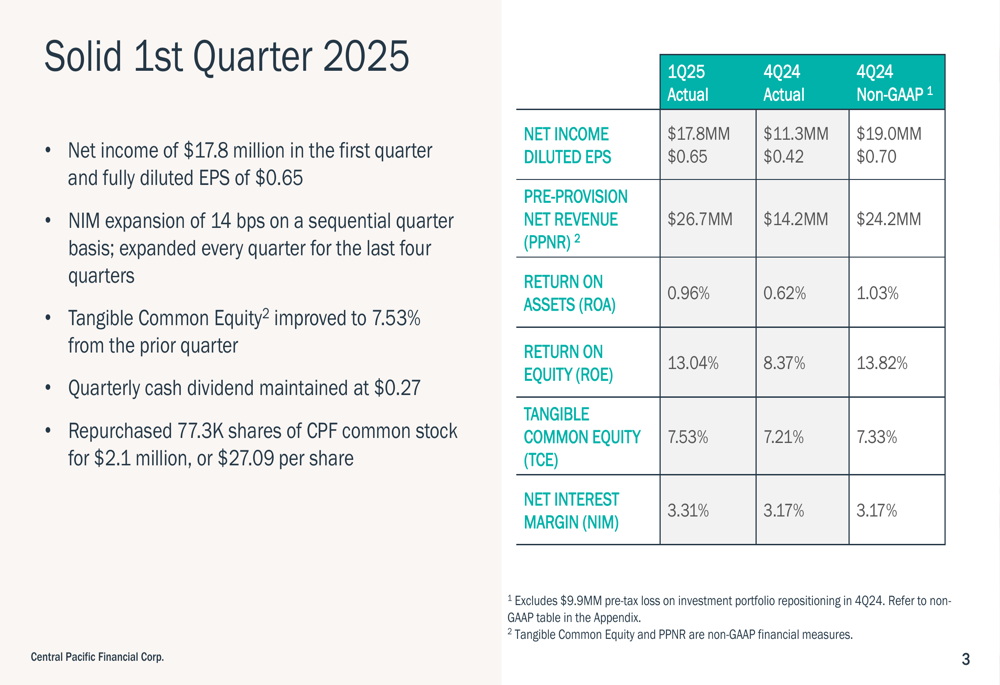

Central Pacific Financial reported solid financial results for the first quarter of 2025, with net income of $17.8 million and fully diluted earnings per share (EPS) of $0.65. This represents a significant improvement from the $11.3 million ($0.42 per share) reported in Q4 2024 on a GAAP basis, though slightly below the non-GAAP adjusted figure of $19.0 million ($0.70 per share) from the previous quarter, which excluded a one-time investment securities loss.

As shown in the following performance summary, the company saw improvements across several key metrics, including pre-provision net revenue (PPNR), return on assets (ROA), return on equity (ROE), and tangible common equity (TCE):

A standout achievement was the expansion of the net interest margin (NIM) by 14 basis points to 3.31%, continuing the positive momentum from the previous quarter. This NIM improvement reflects the company’s effective management of its funding costs while maintaining asset yields, demonstrating disciplined pricing and spread management in a changing interest rate environment.

Hawaii Economic Environment

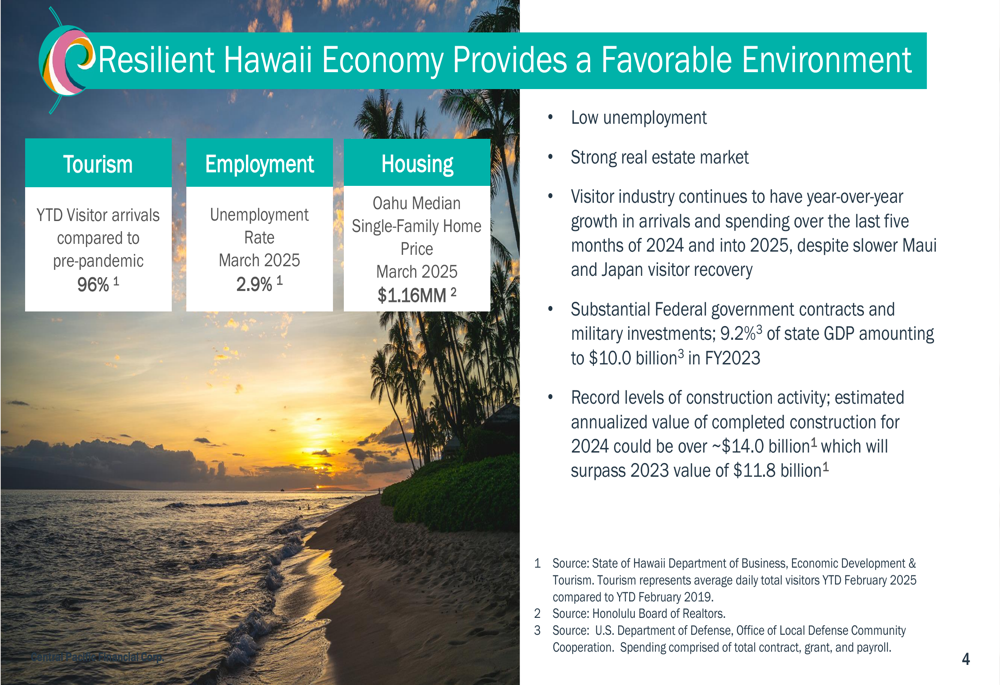

Central Pacific Financial’s performance is underpinned by Hawaii’s resilient economy, which continues to show strength across multiple sectors. The state’s unemployment rate of 2.9% remains well below the national average of 4.1%, while the real estate market maintains robust valuations with the median single-family home price on Oahu reaching $1.16 million.

The tourism sector, a critical component of Hawaii’s economy, has recovered to 96% of pre-pandemic levels, while substantial federal government contracts and military investments totaling $10 billion provide additional economic stability. The construction industry is also experiencing record activity, with an estimated annualized value of completed construction for 2024 exceeding $14 billion.

As illustrated in the following slide, these economic indicators create a favorable operating environment for the bank:

Balance Sheet Strength and Diversification

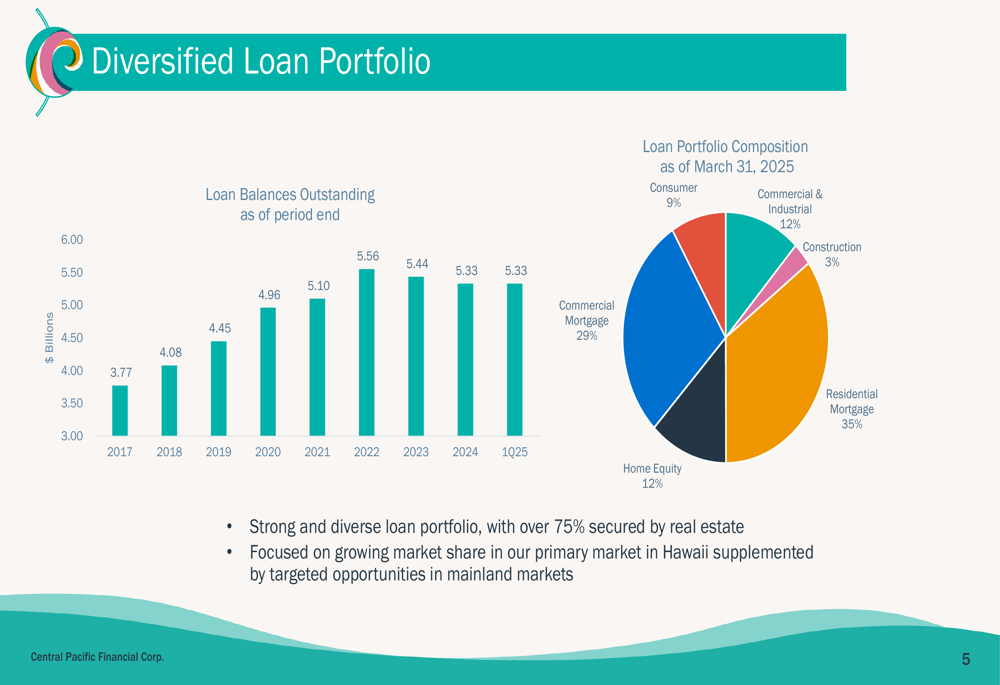

Central Pacific Financial maintains a well-diversified loan portfolio totaling $5.33 billion as of Q1 2025. The portfolio composition reflects a balanced approach to lending, with residential mortgages representing the largest segment at 35%, followed by commercial mortgages at 29%. Over 75% of the loan portfolio is secured by real estate, providing additional risk mitigation.

The following chart illustrates the company’s loan portfolio diversification and historical growth trends:

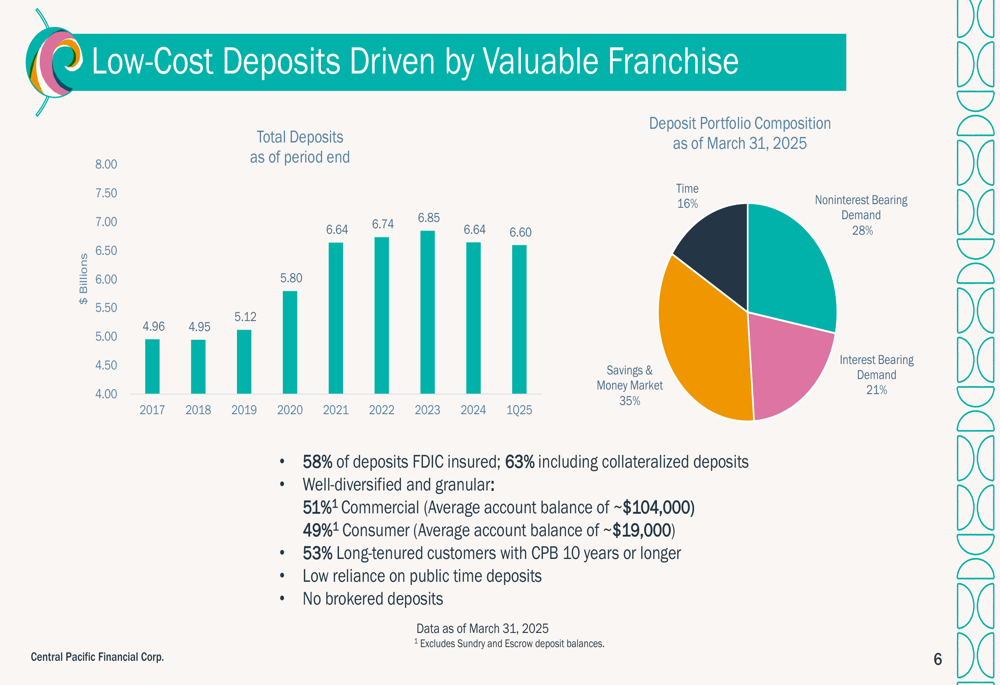

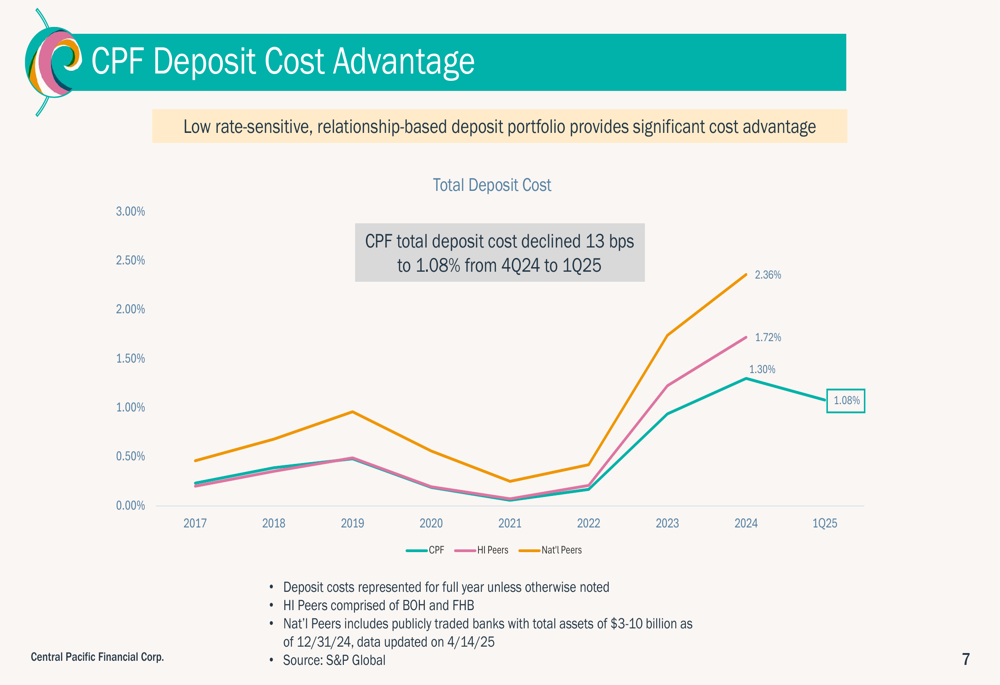

On the funding side, the bank reported total deposits of $6.64 billion, with a favorable mix that includes 28% non-interest bearing demand deposits. This deposit composition contributes to the bank’s relatively low cost of funds, with total deposit costs declining by 13 basis points to 1.08% in Q1 2025.

The deposit base is well-diversified and granular, with 58% of deposits FDIC insured (63% including collateralized deposits). The bank’s customer relationships are stable, with 53% being long-tenured customers of 10+ years, and there is low reliance on public time deposits and no brokered deposits.

The following chart shows the deposit composition and trends:

Central Pacific Financial maintains a competitive advantage with its deposit costs, which are lower than both Hawaii and national peers. This advantage has been maintained consistently over time, as illustrated in the following comparison:

Credit Quality and Risk Management

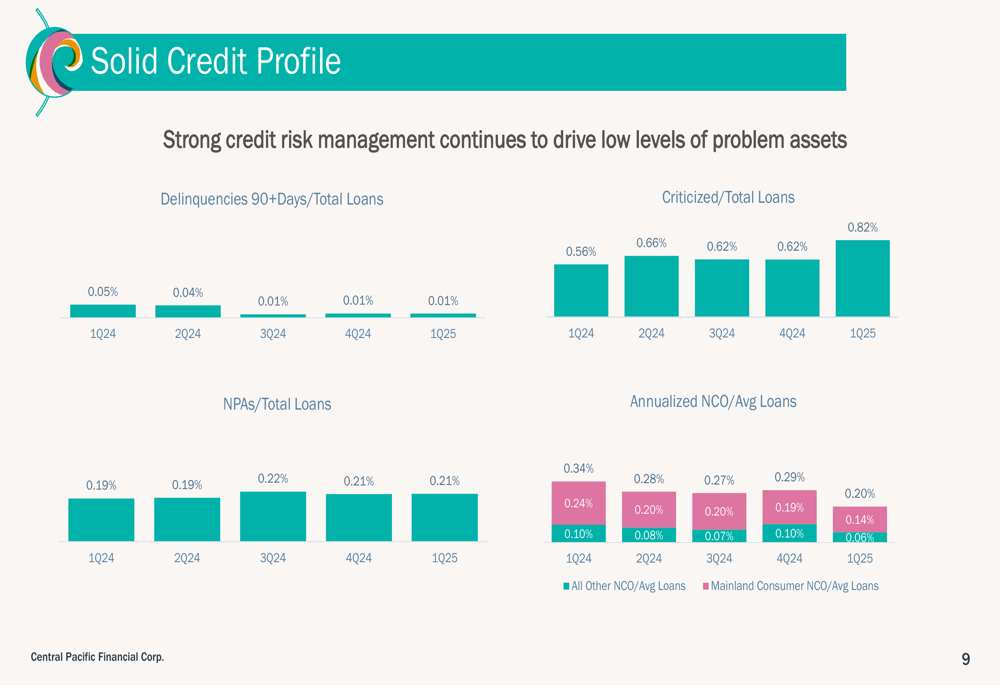

The bank’s credit quality remains strong, with low levels of delinquencies, criticized loans, and non-performing assets. As of Q1 2025, loans delinquent 90+ days represented just 0.01% of total loans, while criticized loans were 0.82% and non-performing assets to total loans stood at 0.21%.

The following chart demonstrates the bank’s solid credit profile:

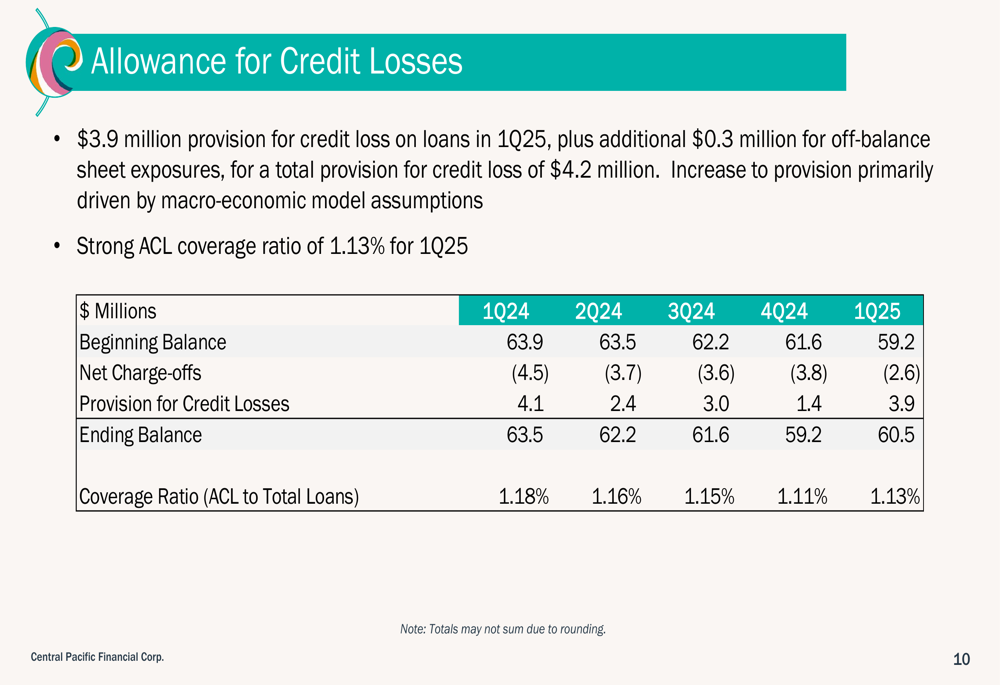

Central Pacific Financial recorded a provision for credit losses of $4.2 million in Q1 2025, which included $3.9 million for loans and $0.3 million for off-balance sheet exposures. The increase in provision was primarily driven by macroeconomic model assumptions. The allowance for credit losses (ACL) stood at $60.5 million, representing a coverage ratio of 1.13%.

Capital Management and Shareholder Returns

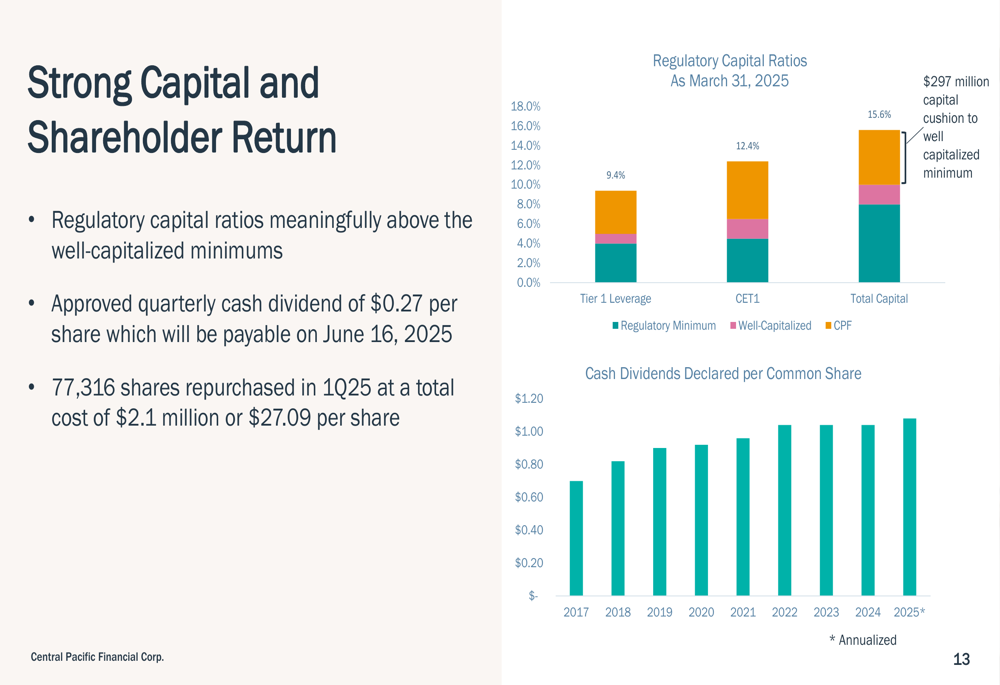

The company maintains strong capital levels, with regulatory ratios significantly above well-capitalized minimums. This capital strength allows Central Pacific Financial to continue returning value to shareholders through dividends and share repurchases.

In Q1 2025, the bank maintained its quarterly cash dividend at $0.27 per share and repurchased 77,316 shares at a total cost of $2.1 million, or an average price of $27.09 per share. These shareholder returns reflect the company’s commitment to balancing growth investments with direct returns to investors.

Forward Outlook

Looking ahead, Central Pacific Financial appears well-positioned for continued success, supported by its strong balance sheet, diversified loan portfolio, low-cost deposit base, and the resilient Hawaii economy. The company’s focus on maintaining disciplined pricing and spread management should continue to support net interest margin expansion.

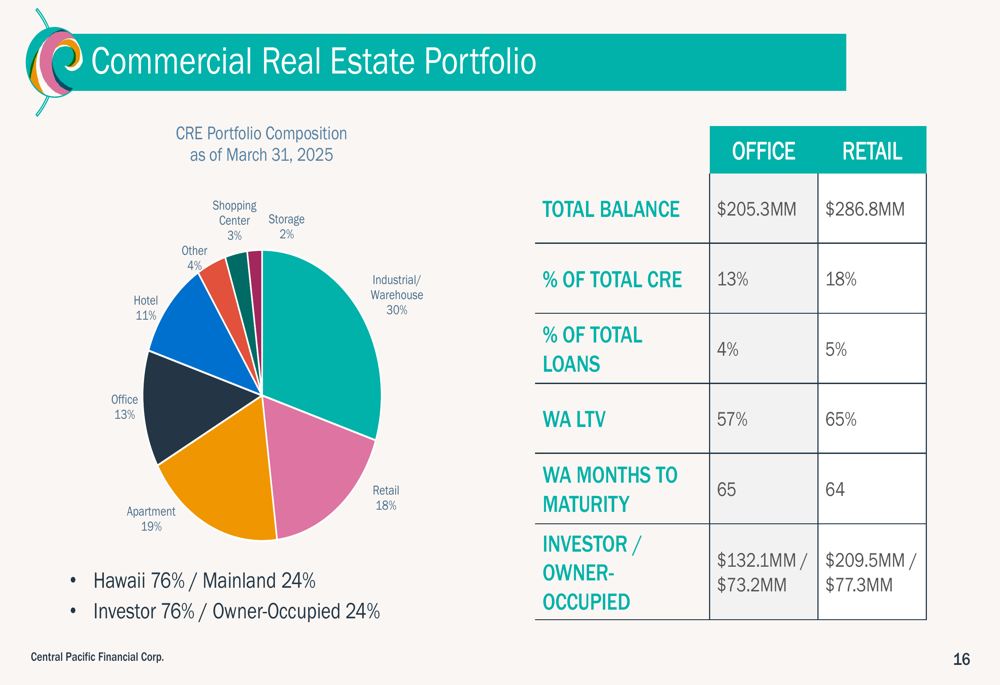

The bank’s commercial real estate portfolio remains well-diversified across property types, with limited exposure to potentially challenging segments such as office space (13% of CRE, 4% of total loans) and retail (18% of CRE, 5% of total loans). Both segments maintain healthy weighted average loan-to-value ratios of 57% and 65%, respectively.

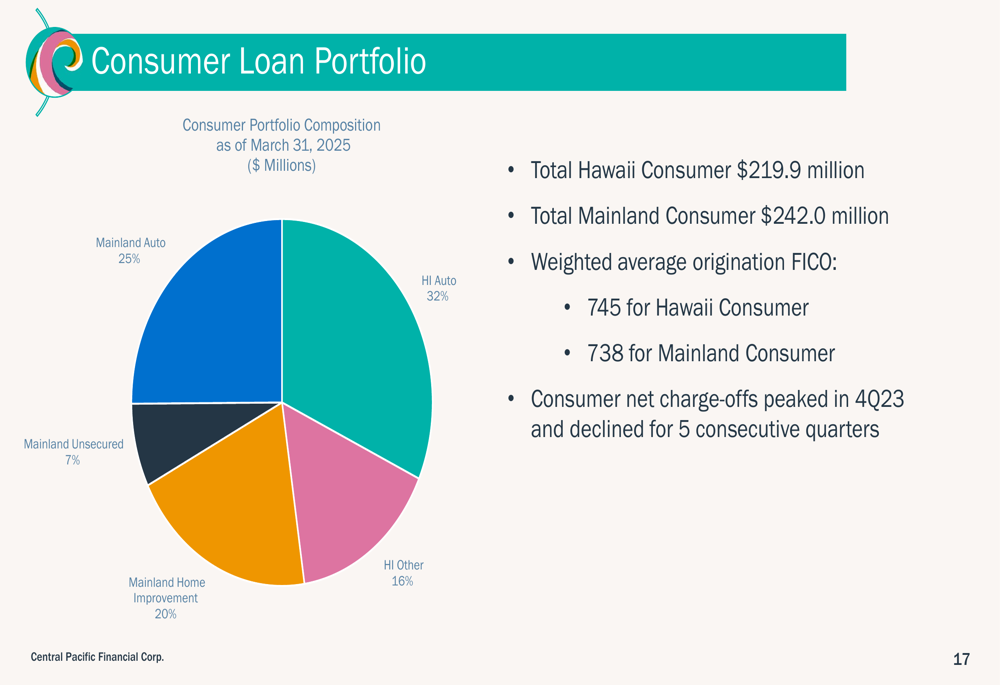

In the consumer loan segment, the bank has a balanced mix between Hawaii (48%) and mainland (52%) exposures, with strong weighted average FICO scores of 745 and 738, respectively. The company noted that consumer net charge-offs peaked in Q4 2023 and have declined for five consecutive quarters, indicating improving trends in this segment.

Central Pacific Financial’s Q1 2025 results demonstrate the company’s ability to navigate a changing economic environment while delivering improved profitability. With its strong market position in Hawaii, diversified balance sheet, and disciplined approach to risk management, the bank appears well-positioned to continue this positive momentum throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.