NVIDIA launches Jetson Thor robotics computers for physical AI systems

Introduction & Market Context

Automotive AI voice technology provider Cerence Inc . (NASDAQ:CRNC) reported strong Q2 FY25 results on May 7, 2025, showcasing a significant turnaround in profitability and exceeding guidance across all key metrics. The company’s shares jumped 5.59% in after-hours trading to $10.56, building on a 0.6% gain during the regular session.

The results mark a substantial improvement from the previous year, with Cerence continuing its strategic pivot toward generative AI solutions for the automotive industry. This quarter’s performance indicates the company’s cost-cutting measures and focus on high-margin license revenue are beginning to yield results.

Quarterly Performance Highlights

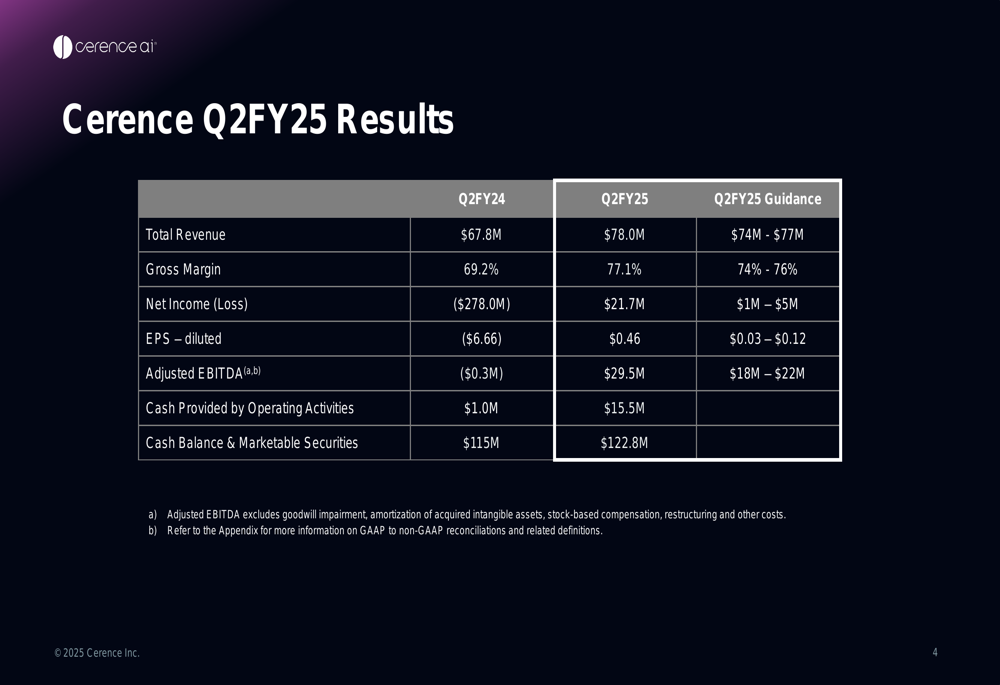

Cerence reported Q2 FY25 revenue of $78.0 million, exceeding both the company’s guidance range of $74-77 million and the year-ago figure of $67.8 million. More impressively, the company achieved a dramatic swing to profitability with net income of $21.7 million, compared to a substantial loss of $278.0 million in the same quarter last year.

As shown in the following comprehensive results table, Cerence outperformed its guidance across all metrics:

Gross margin showed remarkable improvement, reaching 77.1% compared to 69.2% in the prior year and exceeding guidance of 74-76%. This margin expansion reflects the company’s shift toward higher-margin license revenue and improved operational efficiency.

Adjusted EBITDA of $29.5 million significantly outpaced guidance of $18-22 million and represented a substantial improvement from the negative $0.3 million reported in Q2 FY24. Cash flow from operations strengthened to $15.5 million, up from $1.0 million in the prior-year period.

Detailed Financial Analysis

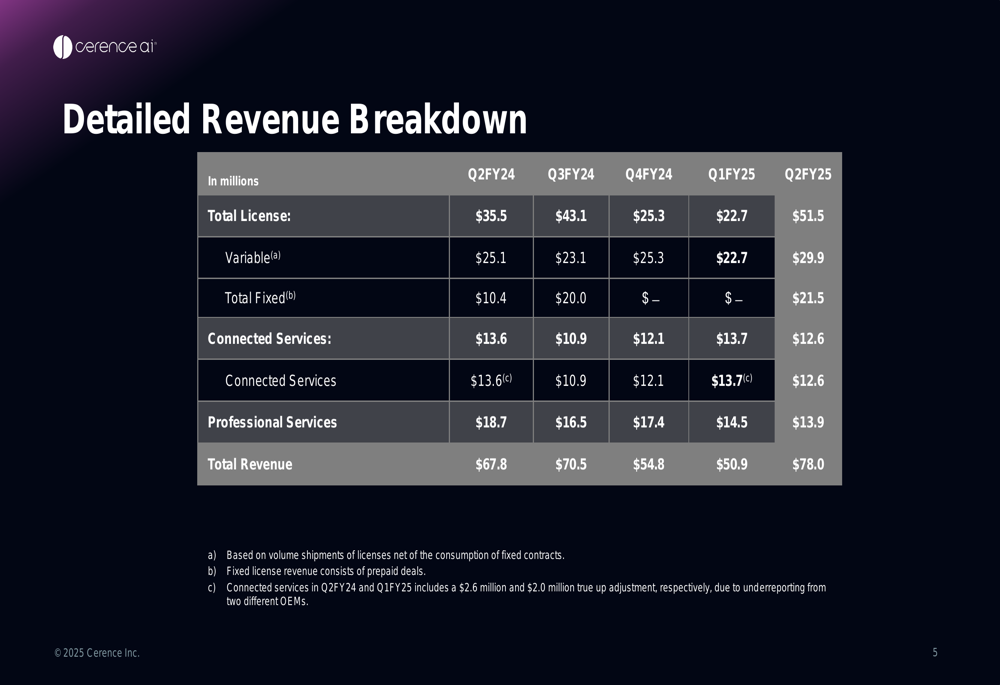

A closer examination of Cerence’s revenue streams reveals that license revenue was the primary driver of growth, particularly in fixed license contracts. The following breakdown illustrates the quarterly revenue trends:

Total (EPA:TTEF) license revenue reached $51.5 million in Q2 FY25, a 45% increase from $35.5 million in Q2 FY24. Within this category, fixed license revenue more than doubled to $21.5 million from $10.4 million a year earlier, while variable license revenue grew to $29.9 million from $25.1 million.

This growth in license revenue offset declines in connected services ($12.6 million, down from $13.6 million) and professional services ($13.9 million, down from $18.7 million). The shift toward license revenue is strategically important as it typically carries higher margins.

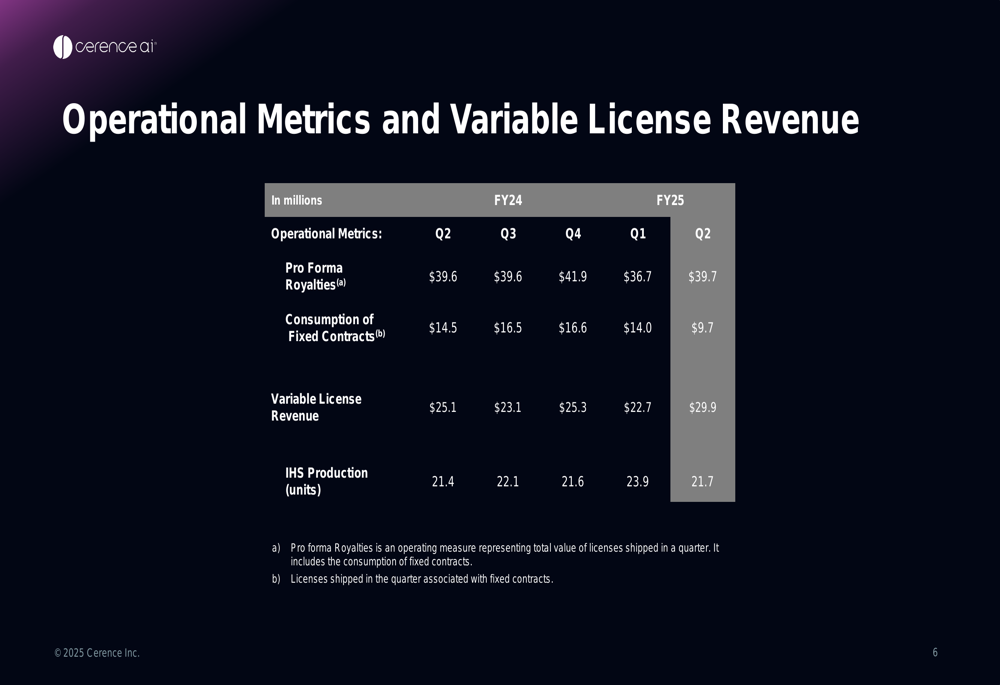

The company’s operational metrics provide additional context for understanding the revenue performance:

Cerence’s key performance indicators show improvement in several areas, particularly in pricing power and connected technology adoption:

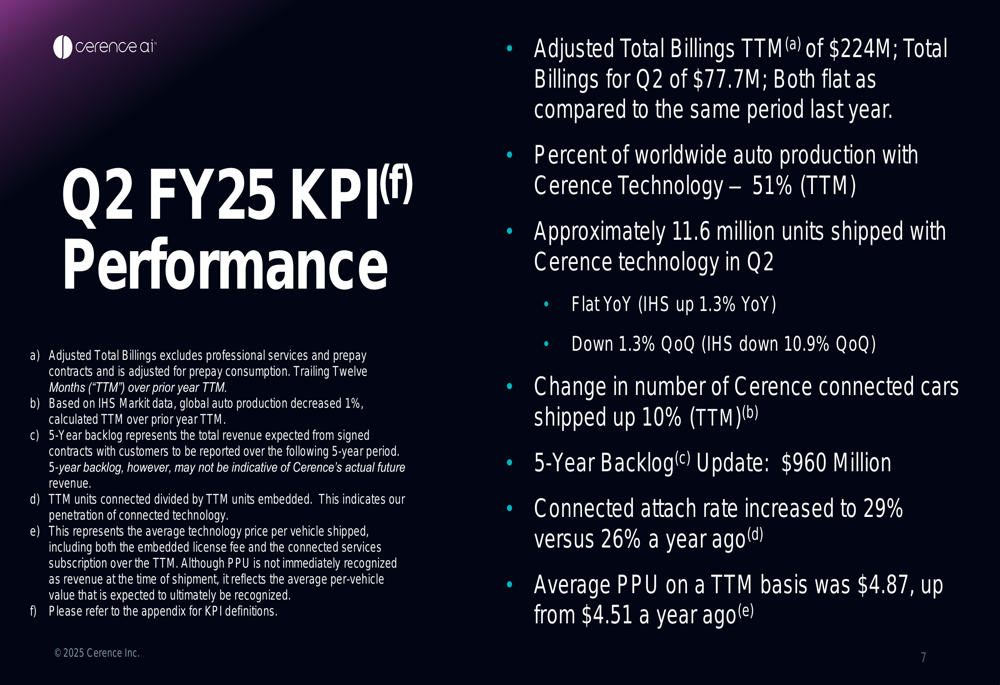

The average price per unit (PPU) increased to $4.87 on a trailing twelve-month basis, up from $4.51 a year ago, indicating improved monetization of the company’s technology. The connected attach rate rose to 29% from 26% a year earlier, showing growing adoption of Cerence’s connected services.

The company maintained its 5-year backlog at $960 million, providing visibility into future revenue streams. Cerence’s technology was present in approximately 51% of worldwide auto production on a trailing twelve-month basis, highlighting its significant market penetration.

Forward-Looking Statements

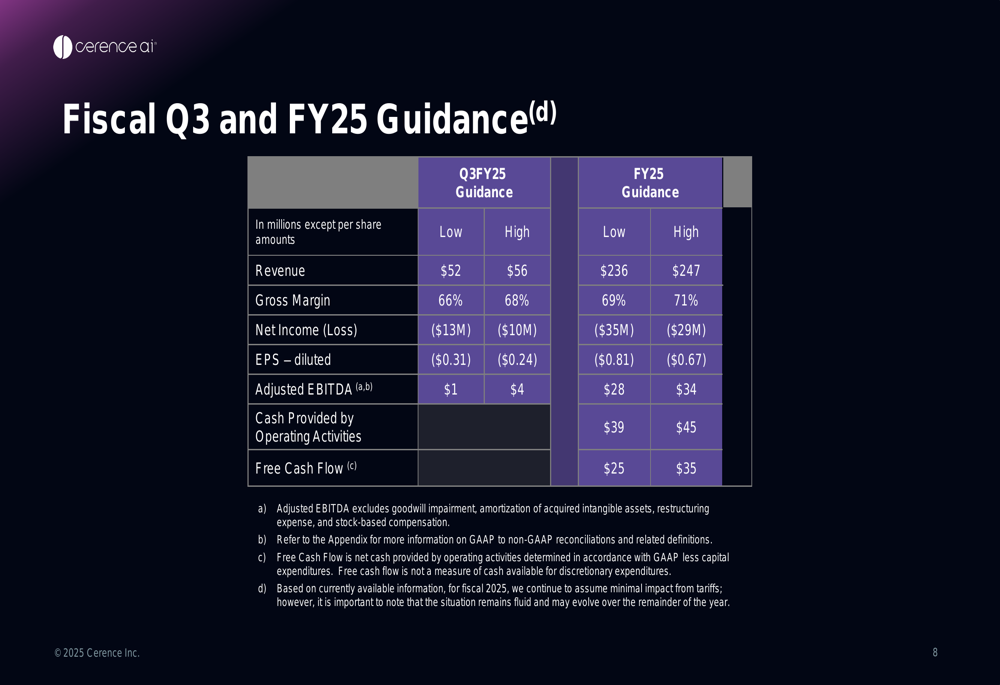

Despite the strong Q2 performance, Cerence maintained relatively conservative guidance for Q3 and the full fiscal year 2025:

For Q3 FY25, Cerence expects revenue between $52-56 million, which would represent a significant sequential decline from Q2’s $78 million. The company also anticipates a return to negative net income of $10-13 million for the quarter.

For the full fiscal year 2025, Cerence projects revenue of $236-247 million, adjusted EBITDA of $28-34 million, and free cash flow of $25-35 million. This guidance suggests management expects more challenging conditions in the second half of the fiscal year, potentially due to automotive production fluctuations or project timing.

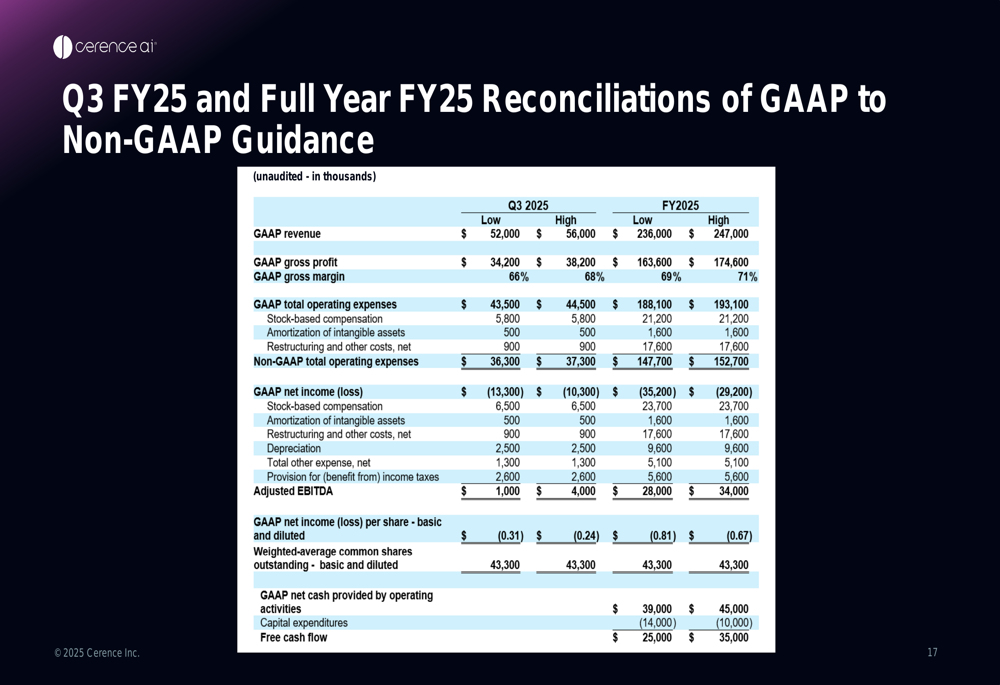

The reconciliation between GAAP and non-GAAP guidance provides additional insight into expected performance:

The maintained full-year guidance, despite the strong Q2 results, could indicate management’s cautious approach given ongoing industry challenges or potential seasonality in the business. Alternatively, it may suggest the company is setting conservative expectations that it hopes to exceed in coming quarters.

Cerence’s strategic focus on generative AI, which was highlighted in previous earnings calls, appears to be yielding results as the company continues its return to profitability. With a strengthened cash position of $122.8 million and improved operational metrics, Cerence appears better positioned to navigate the evolving automotive AI landscape than it was a year ago.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.