Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Certara Inc (NASDAQ:CERT), a leading biosimulation technology provider, presented its second quarter 2025 financial results on August 6, 2025, highlighting continued revenue growth despite challenges in profitability. The company, which supports drug development through its modeling and simulation platforms, reported a 12% year-over-year revenue increase while swinging to a net loss after a profitable first quarter.

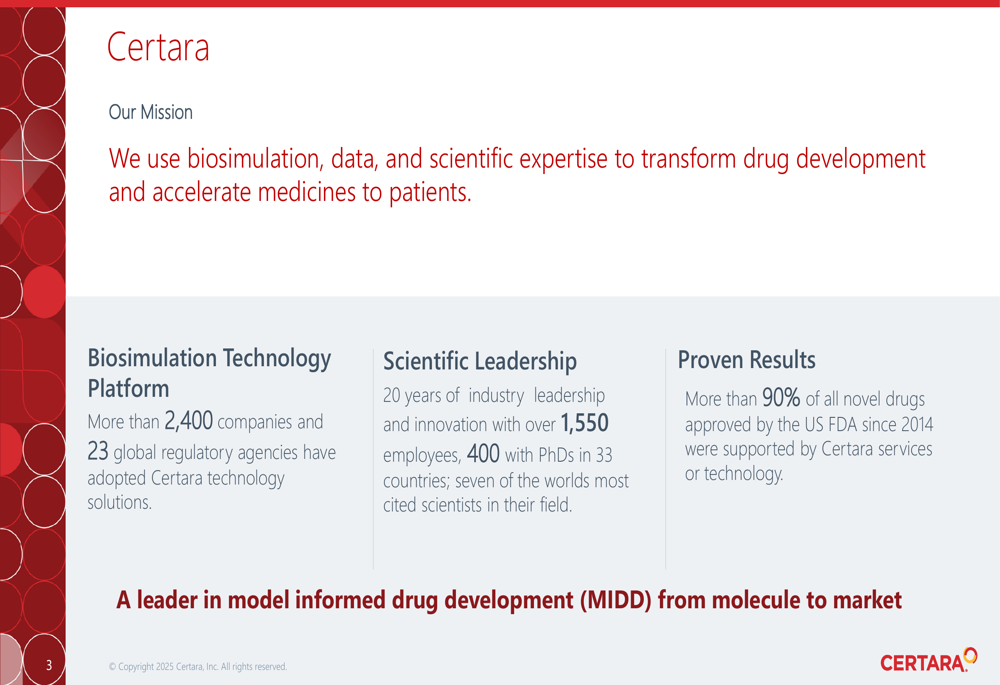

The presentation emphasized Certara’s dominant position in the pharmaceutical development space, with its solutions supporting more than 90% of all novel drugs approved by the FDA since 2014. The company serves over 2,600 customers across 70 countries, with its software adopted by 23 global regulatory agencies.

As shown in the following chart illustrating Certara’s value proposition and market position:

Quarterly Performance Highlights

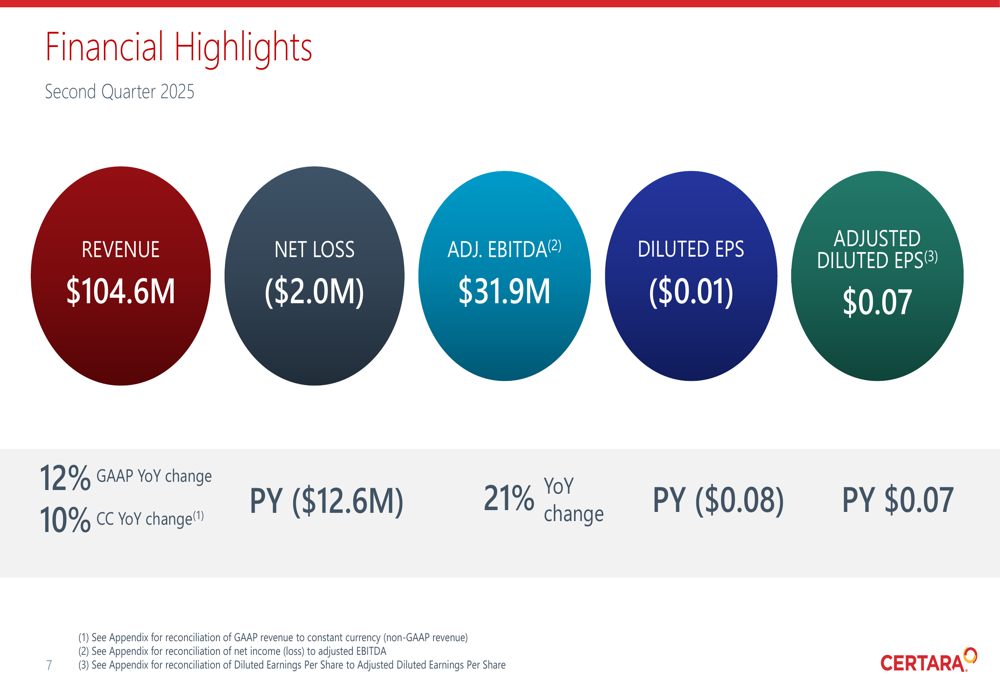

Certara reported Q2 2025 revenue of $104.6 million, representing 12% growth compared to the same period last year. However, the company posted a net loss of $2.0 million, a significant shift from the $4.7 million net income reported in Q1 2025, though still an improvement from the $12.6 million loss in Q2 2024. Adjusted EBITDA reached $31.9 million, growing 21% year-over-year, with an adjusted EBITDA margin of 31%.

The company’s adjusted diluted earnings per share remained flat at $0.07, matching the prior year period. This performance comes against a backdrop of continued investment in product development and strategic acquisitions.

The following slide summarizes the key financial metrics for the quarter:

Certara’s stock closed at $9.86 on August 6, down 3.35% for the day, with after-hours trading showing a further decline of 0.51% to $9.81. This represents a significant drop from the $12.82 price reported after Q1 2025 earnings, suggesting investor concerns despite the revenue growth.

Segment Analysis

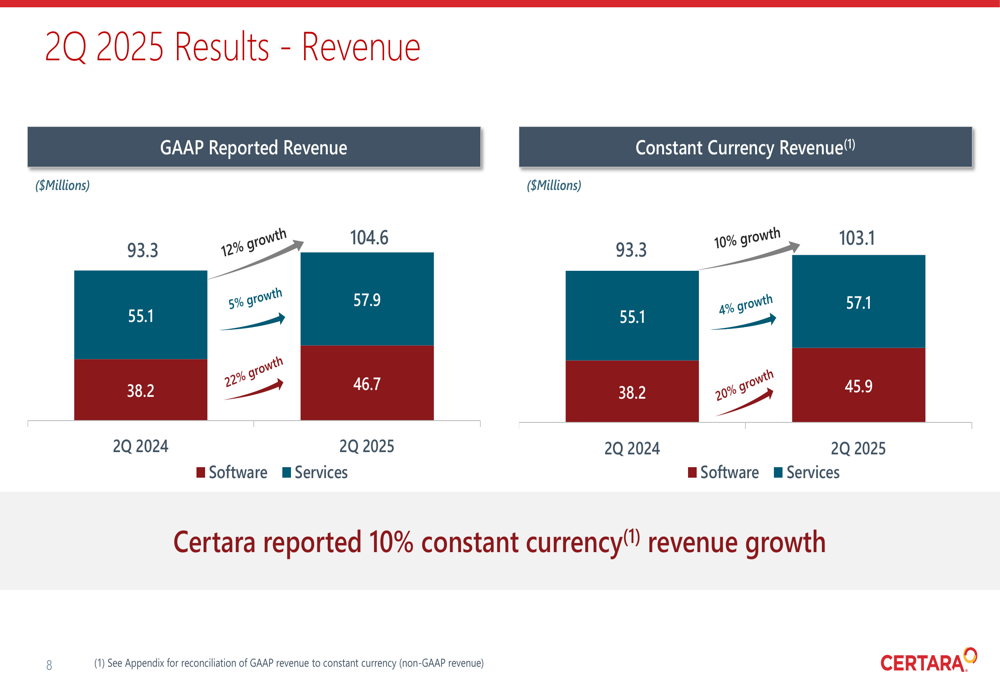

The company’s performance showed a clear divergence between its software and services segments. Software (ETR:SOWGn) revenue grew an impressive 22% to $46.7 million, while services revenue increased by a more modest 5% to $57.9 million. On a constant currency basis, software and services grew by 20% and 4%, respectively.

This detailed breakdown of revenue performance illustrates the strength of the software segment:

Net bookings, a leading indicator of future revenue, increased 13% year-over-year to $112.0 million. Software bookings grew 11% to $46.6 million, while services bookings increased 15% to $65.4 million. The company maintained a healthy book-to-bill ratio of 1.16x, indicating continued demand for its solutions.

A positive sign for the software business was the recovery in the Net Retention Rate (NRR), which improved to 107.6% in Q2 2025 from a low of 102.4% in Q1 2025. This metric measures the company’s ability to retain and expand revenue from existing software customers.

Acquisition Impact and Organic Growth

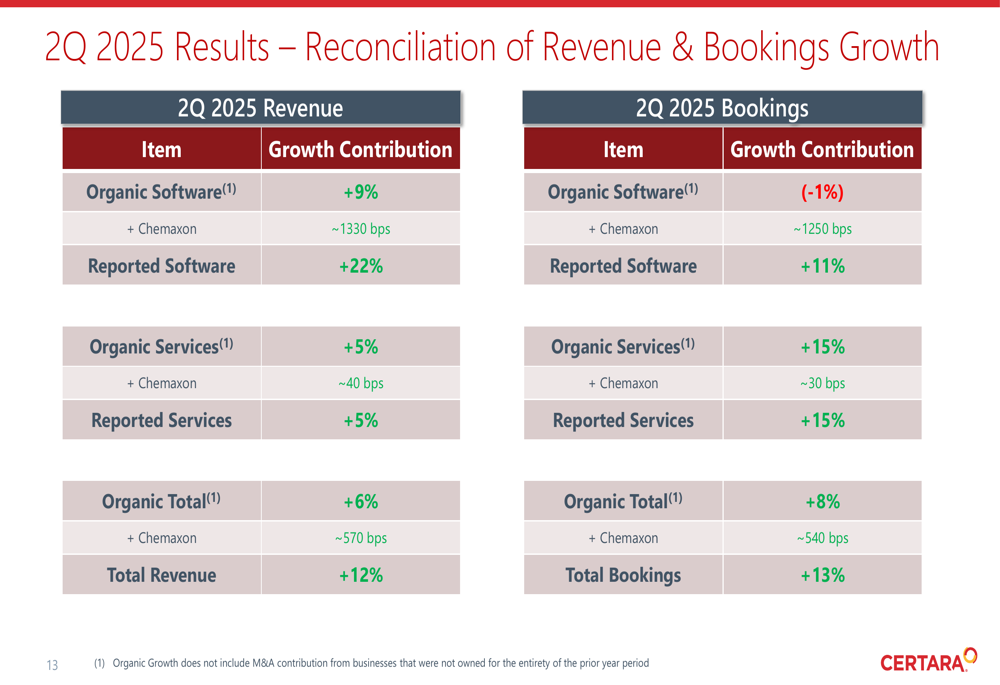

The presentation provided transparency on the impact of the Chemaxon acquisition on Certara’s growth figures. While reported software revenue grew 22%, organic software growth was 9%, with Chemaxon contributing approximately 13 percentage points to the growth rate. Similarly, total revenue growth of 12% consisted of 6% organic growth and about 6 percentage points from the acquisition.

The following slide breaks down the organic versus acquisition-driven growth components:

This analysis reveals that while the Chemaxon acquisition significantly boosted software revenue growth, the organic business continues to expand at a healthy rate, particularly in services where organic growth of 15% in bookings suggests strong future performance.

Strategic Initiatives

Certara highlighted several strategic developments during the quarter, including continued growth in Quantitative Systems Pharmacology (QSP) services, spurred by FDA guidance for monoclonal antibodies. The company announced plans to launch a new QSP Software Platform called CertaraIQ in the second half of 2025, expanding its product portfolio.

Additionally, Certara signed a strategic agreement with pharmaceutical giant Merck (NSE:PROR) and launched version 8.7 of its Phoenix platform, demonstrating ongoing product innovation and customer engagement.

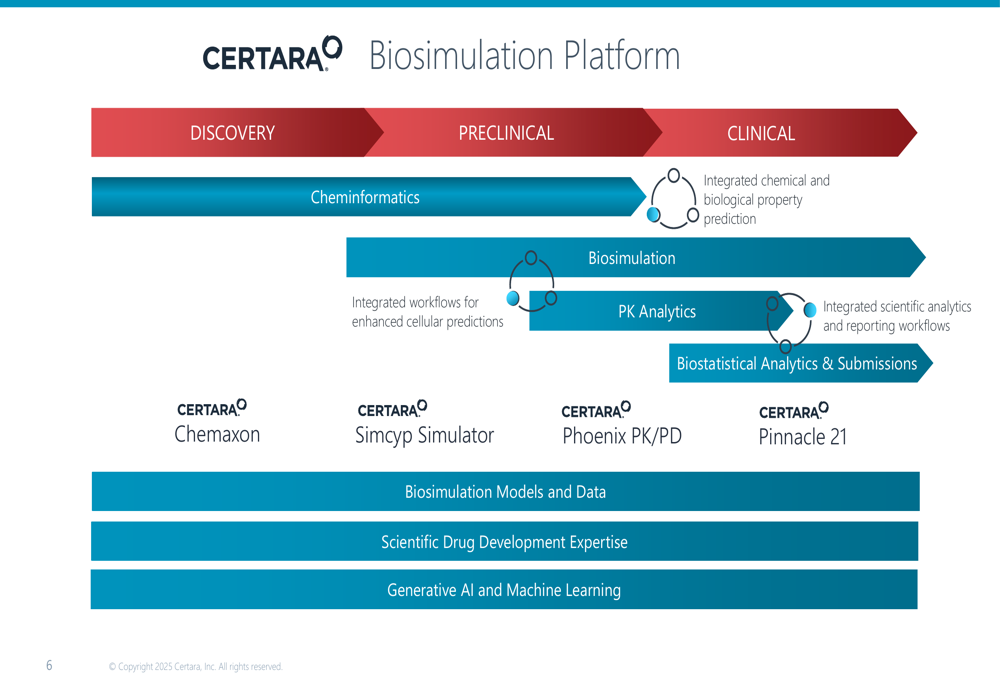

The company’s biosimulation platform spans the entire drug development process, from discovery to clinical stages:

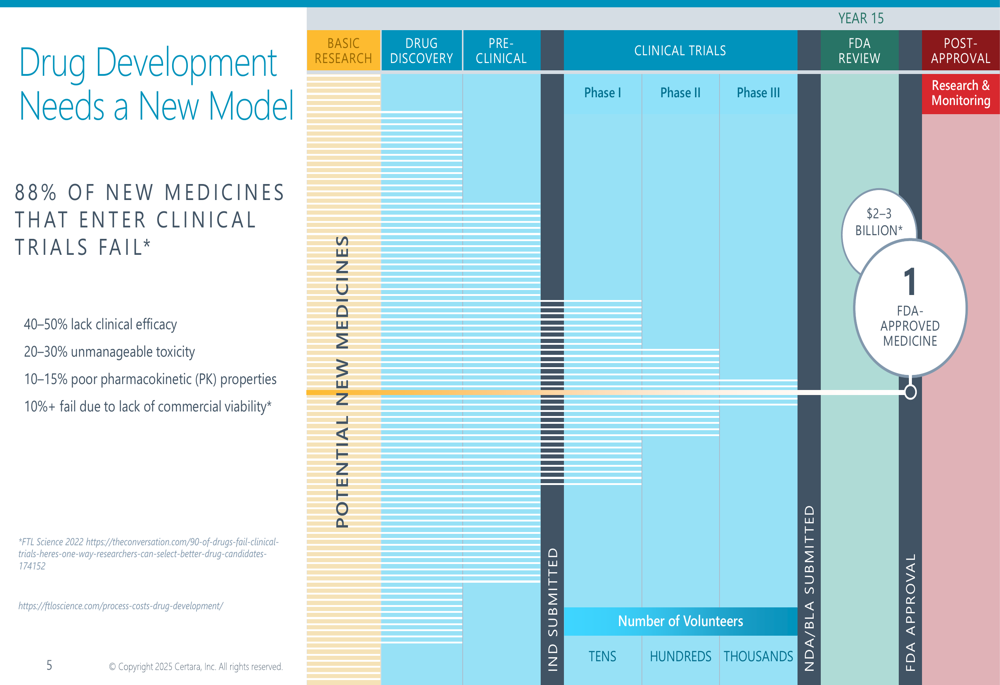

Certara also presented data showing that drug development faces significant challenges, with 88% of new medicines entering clinical trials ultimately failing. This context underscores the value proposition of the company’s biosimulation technology, which aims to improve success rates and reduce development costs.

As illustrated in this slide detailing the challenges in drug development:

Customer Segment Performance

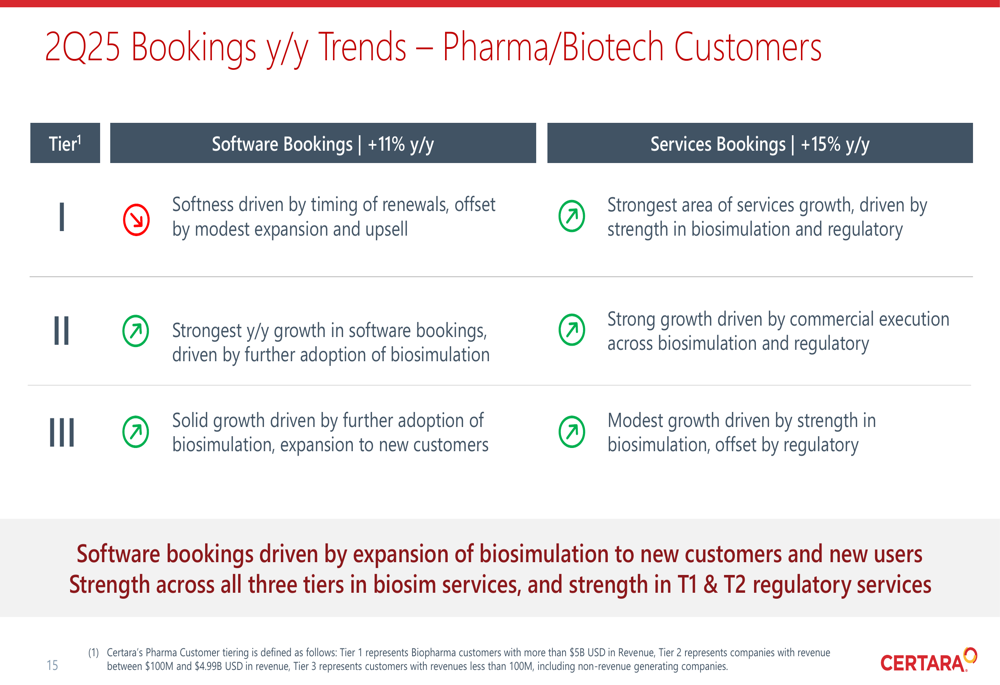

The presentation provided insights into bookings trends across different customer tiers. Tier 1 pharmaceutical companies showed 11% year-over-year growth in software bookings and 15% growth in services bookings. Tier 2 customers demonstrated the strongest growth, particularly in software adoption, while Tier 3 customers showed solid growth in software but more modest performance in services.

This segmentation analysis offers valuable perspective on where Certara is gaining the most traction:

Forward Guidance

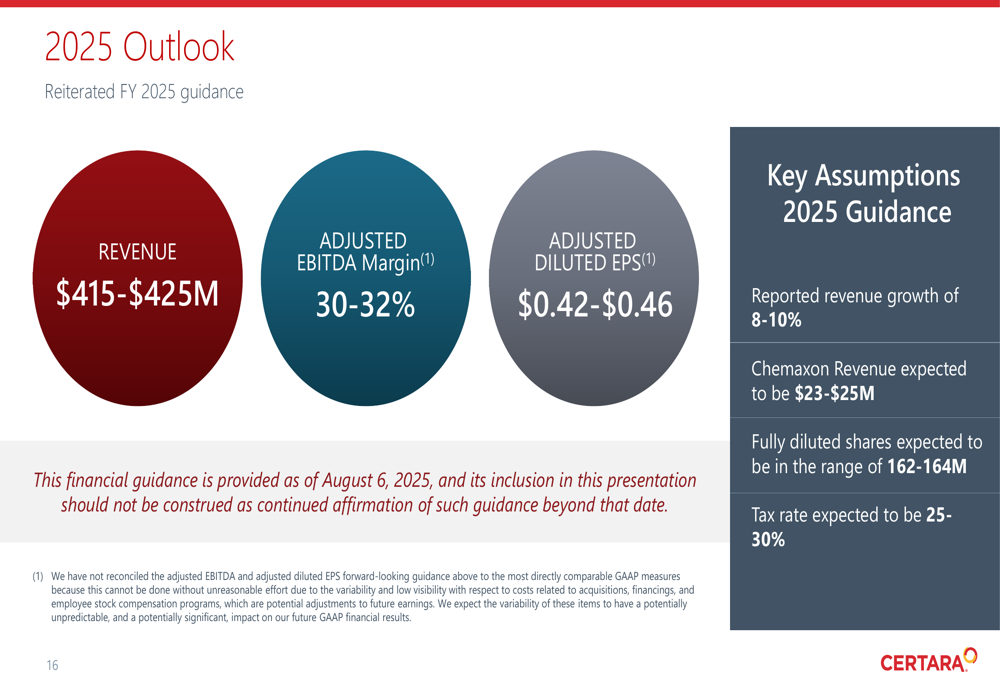

Certara maintained its full-year 2025 guidance, projecting revenue between $415-425 million (representing 8-10% growth), adjusted EBITDA margin of 30-32%, and adjusted diluted EPS of $0.42-$0.46. The guidance includes expected revenue of $23-25 million from the Chemaxon acquisition.

The following slide details the company’s outlook for the remainder of 2025:

Conclusion

Certara’s Q2 2025 results present a mixed picture: strong revenue growth and bookings performance, particularly in the software segment, but a swing to net loss after a profitable first quarter. The recovery in software retention rates and consistent book-to-bill ratio above 1.0 suggest underlying business strength, while the significant contribution from the Chemaxon acquisition highlights the company’s strategic focus on expanding its technology portfolio.

As the company continues to invest in new products like the upcoming CertaraIQ platform and strategic relationships with major pharmaceutical companies, investors will be watching closely to see if Certara can translate its growing bookings into improved profitability in future quarters. The recent stock price decline suggests the market remains cautious despite the revenue growth story.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.