Tonix Pharmaceuticals stock halted ahead of FDA approval news

CF Industries Holdings Inc (NYSE:CF), the world’s largest ammonia producer, released its second quarter 2025 financial results on August 6, 2025, showcasing robust performance with significant cash generation despite what the company describes as a disconnect between its market value and underlying fundamentals.

Quarterly Performance Highlights

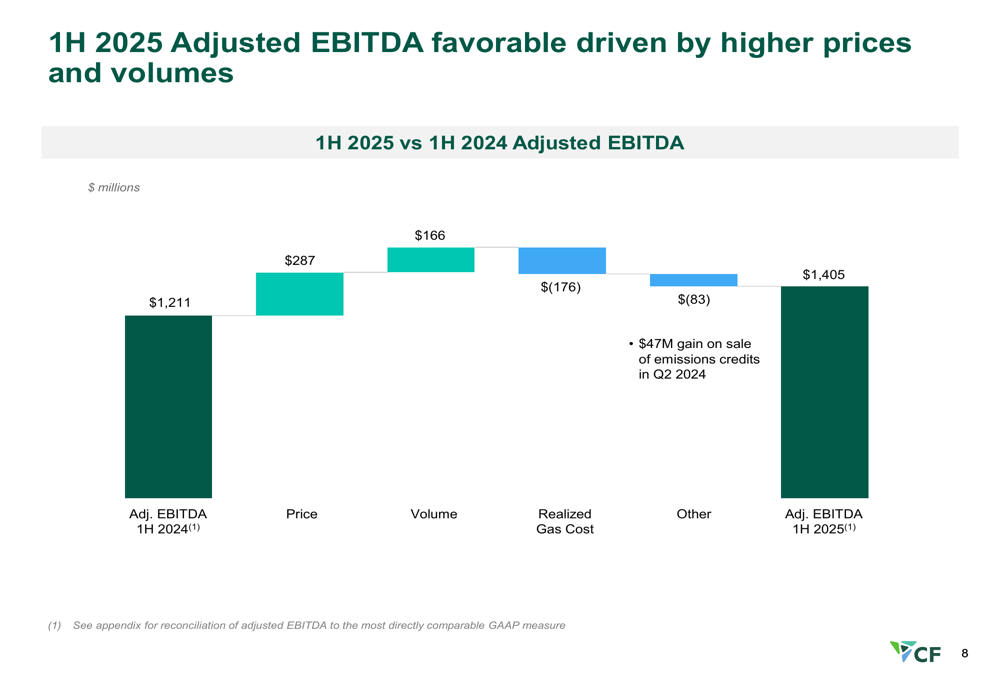

CF Industries reported Q2 2025 net earnings of $386 million and adjusted EBITDA of $761 million, representing a slight increase from $752 million in Q2 2024. For the first half of 2025, the company achieved net earnings of $698 million and adjusted EBITDA of $1.4 billion, marking a 16% increase compared to the first half of 2024.

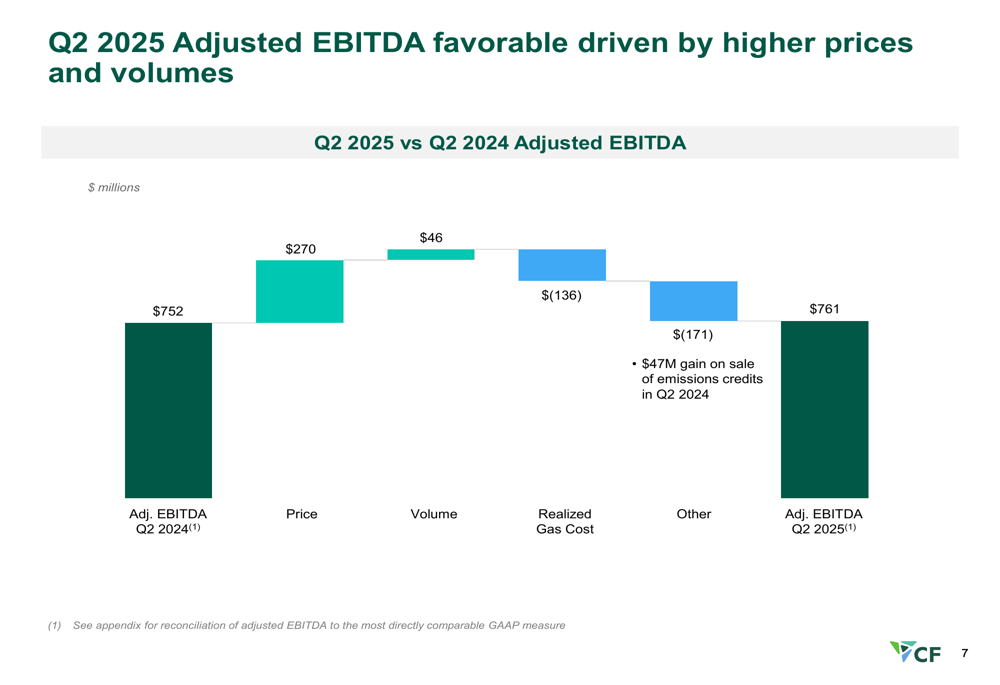

As shown in the following chart breaking down the drivers of Q2 2025 adjusted EBITDA performance:

The company’s quarterly performance was primarily driven by higher selling prices, which contributed an additional $270 million to EBITDA, and increased sales volumes adding $46 million. These positive factors were partially offset by higher realized gas costs, which reduced EBITDA by $136 million, and other factors that decreased EBITDA by $171 million, including a $47 million gain on the sale of emission credits in Q2 2024 that did not recur.

The first half of 2025 showed similar trends but with more substantial volume contributions:

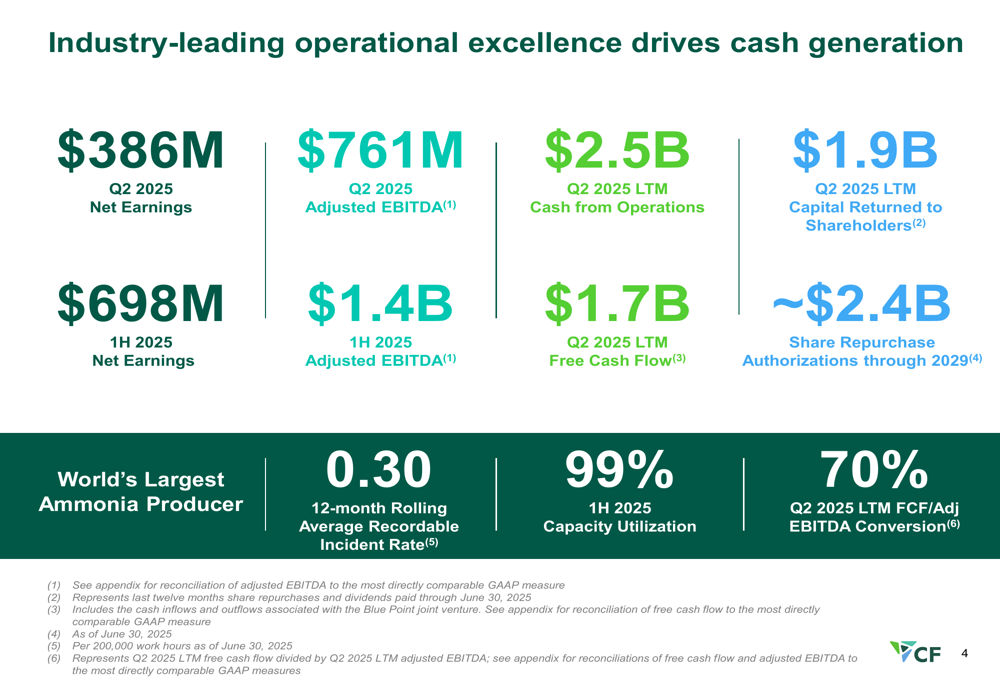

CF Industries maintained exceptional operational efficiency with a 99% capacity utilization rate in the first half of 2025, reinforcing its position as an industry leader. The company’s last twelve months (LTM) cash from operations reached $2.5 billion, with free cash flow of $1.7 billion.

The following slide highlights the company’s key operational and financial metrics:

Capital Allocation and Shareholder Returns

CF Industries continues to demonstrate strong commitment to shareholder returns, having returned over $800 million to shareholders in the first half of 2025. The company has approximately $425 million remaining in its $3 billion share repurchase authorization and has announced an additional $2 billion authorization expiring in December 2029.

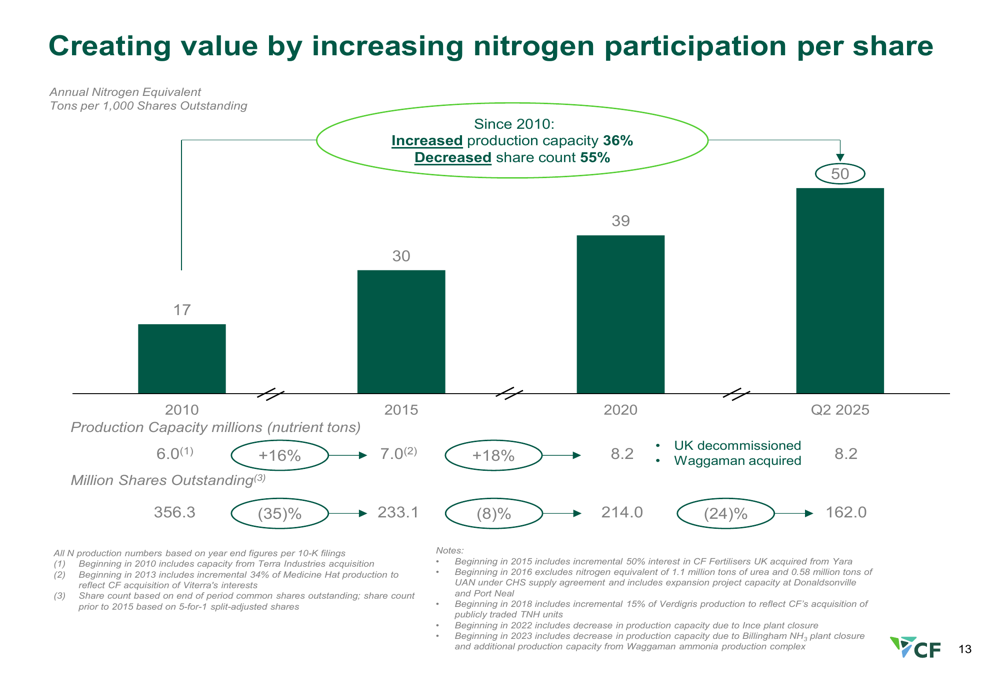

The company’s share repurchase program has significantly reduced outstanding shares from 208 million in 2021 to 162 million by Q2 2025, enhancing per-share value for remaining shareholders. This reduction, combined with increased production capacity, has substantially increased nitrogen participation per share.

As illustrated in the following chart showing the company’s increasing nitrogen participation per share:

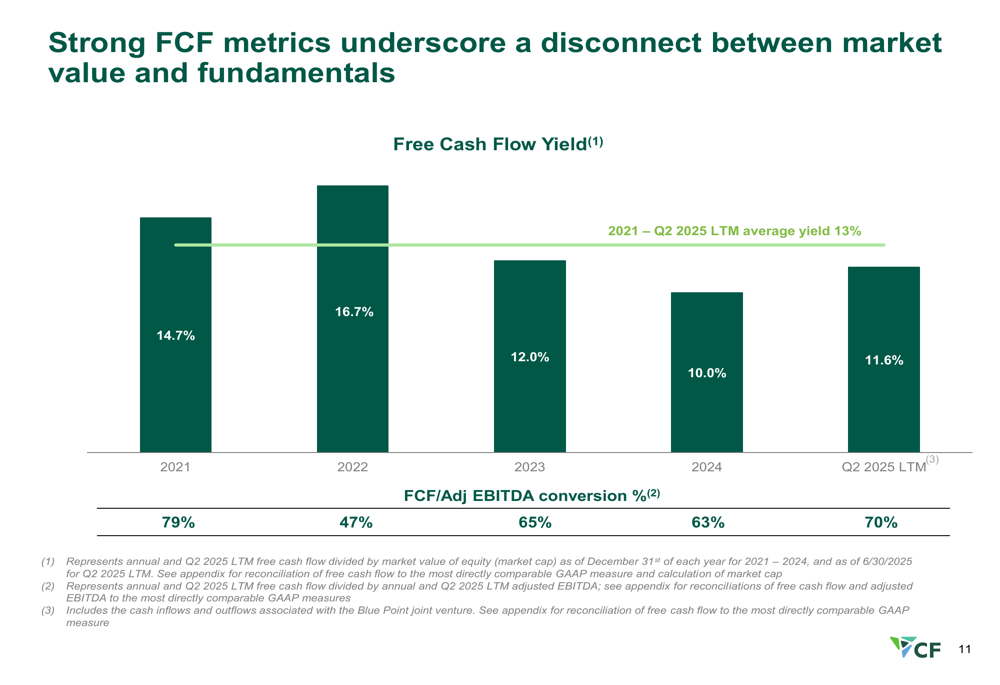

CF Industries highlighted its strong free cash flow yield, which has averaged 13% from 2021 through Q2 2025 LTM, with a current yield of 11.6%. The company’s free cash flow to adjusted EBITDA conversion rate stands at an impressive 70% for Q2 2025 LTM.

The following chart demonstrates the company’s free cash flow yield performance:

Strategic Initiatives in Low-Carbon Ammonia

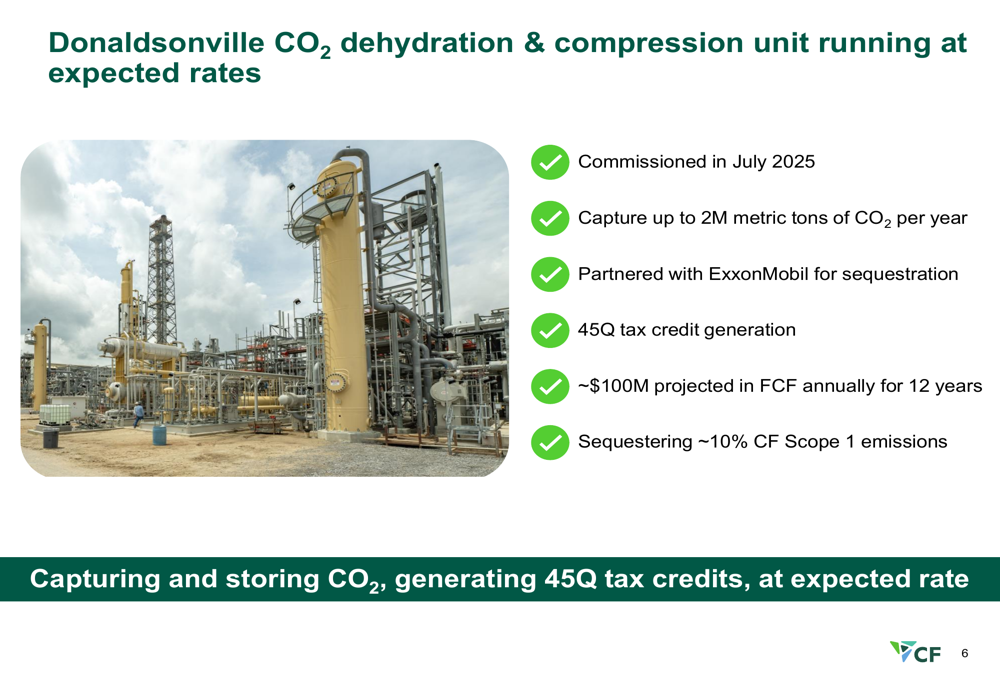

A significant milestone for CF Industries is the successful commissioning of its Donaldsonville CO2 dehydration and compression unit in July 2025. This facility is now running at expected rates and is capable of capturing up to 2 million metric tons of CO2 annually, representing approximately 10% of CF’s Scope 1 emissions.

The following image shows the Donaldsonville facility:

The company has partnered with ExxonMobil (NYSE:XOM) for CO2 sequestration and expects the project to generate approximately $100 million in free cash flow annually for 12 years through 45Q tax credits.

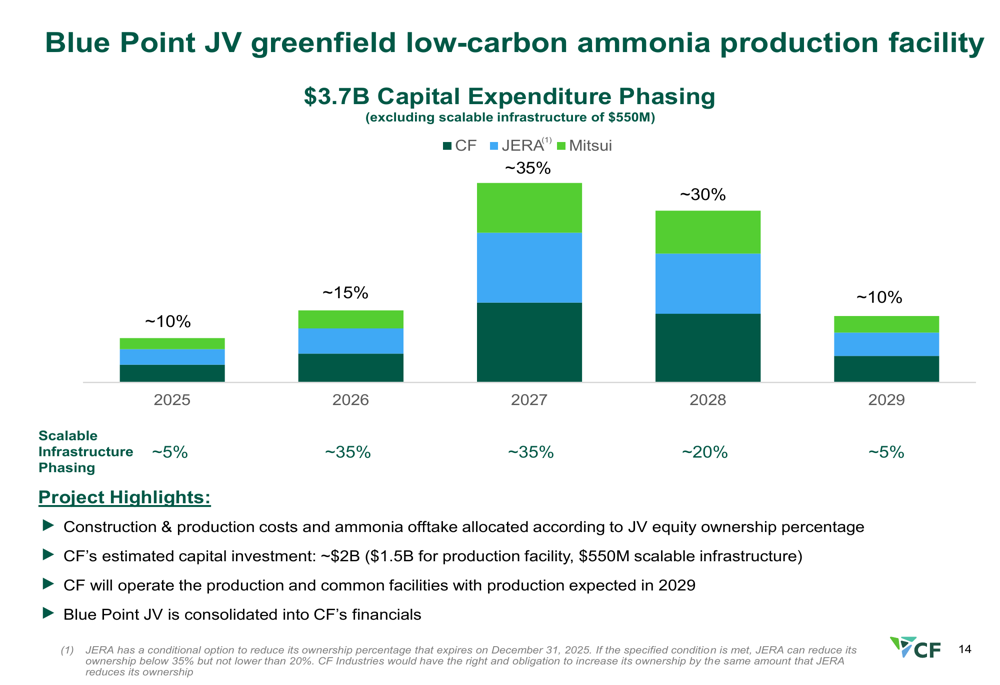

CF Industries is also making progress on its Blue Point joint venture with JERA and Mitsui, a greenfield low-carbon ammonia production facility. The company’s estimated capital investment in this project is approximately $2 billion, with production expected to begin in 2029.

The following chart outlines the capital expenditure phasing for the Blue Point project:

Industry Outlook and Positioning

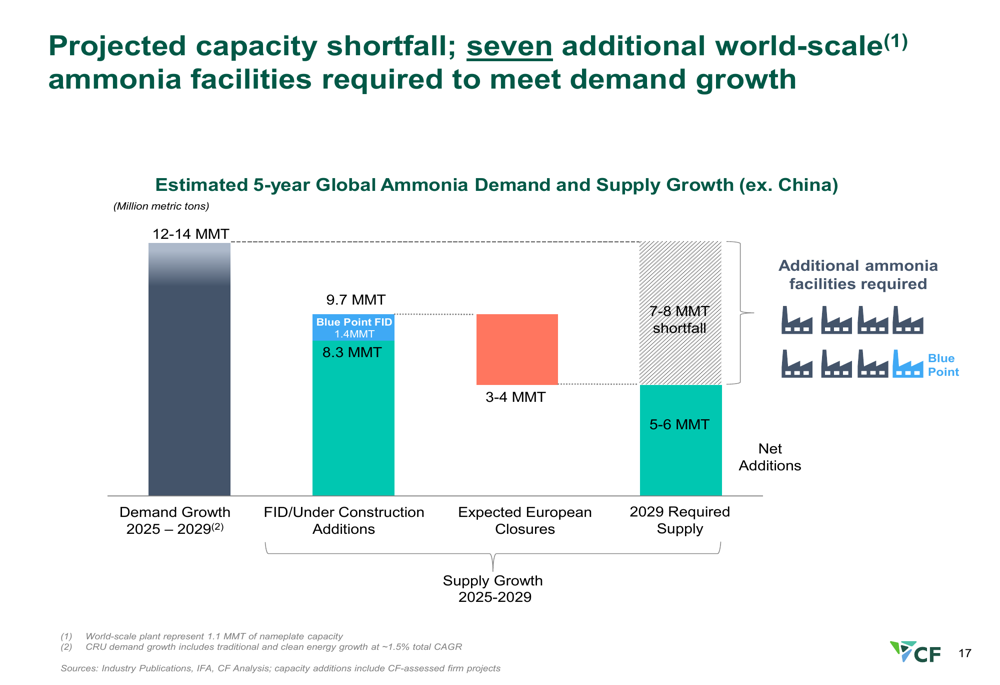

CF Industries expects the global nitrogen supply-demand balance to tighten in the coming years. The company projects a 7-8 million metric ton shortfall in global ammonia supply by 2029, driven by growing demand and limited new capacity additions.

The following chart illustrates the projected capacity shortfall:

Near-term market dynamics include continued geopolitical and gas-related supply disruptions, limited Chinese urea exports (restricted to 3 MMT authorized quota), robust import demand from India and Brazil in the second half of 2025, and Russian nitrogen exports remaining approximately 15% below pre-war levels.

CF Industries also benefits from significant margin opportunities due to global energy price differences, with North American natural gas prices (Henry Hub) remaining substantially lower than European (TTF) and Asian (JKM) prices.

Market Reaction and Outlook

Despite the strong operational and financial performance, CF Industries’ stock closed at $89.90 on August 6, 2025, down 3.04% for the day, suggesting some disconnect between market perception and the company’s fundamentals as highlighted in the presentation. The stock remains well above its 52-week low of $67.34 but below its 52-week high of $104.45.

Looking ahead, CF Industries expects capital expenditures of approximately $650 million in 2025, with about $150 million related to the Blue Point project. The company anticipates gross ammonia production of approximately 10 million tons in 2025.

CF Industries’ long-term outlook projects a 20% increase in mid-cycle EBITDA to approximately $3 billion by 2030, and a 33% increase in free cash flow to approximately $2 billion, driven by strategic initiatives and tightening global supply-demand dynamics in the nitrogen market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.