Aston Martin cuts 2025 volume and profit guidance amid weak demand, tariff risks

Introduction & Market Context

ChargePoint Holdings Inc (NYSE:CHPT) released its first quarter fiscal 2026 financial results on June 4, 2025, showing improved margins and reduced losses despite a year-over-year revenue decline. The electric vehicle charging infrastructure provider’s stock rose 13.08% during regular trading hours to $0.772, with an additional 4.28% gain in after-hours trading to $0.805.

The company’s results come amid continued growth in the electric vehicle market, though at a more measured pace than in previous years. ChargePoint has been focusing on operational efficiency and margin improvement as it progresses toward its stated goal of achieving positive non-GAAP adjusted EBITDA during fiscal 2026.

Quarterly Performance Highlights

ChargePoint reported total revenue of $97.64 million for Q1 FY2026, representing a 8.8% decrease from $107.04 million in the same period last year. Despite the revenue decline, the company demonstrated significant improvements in profitability metrics.

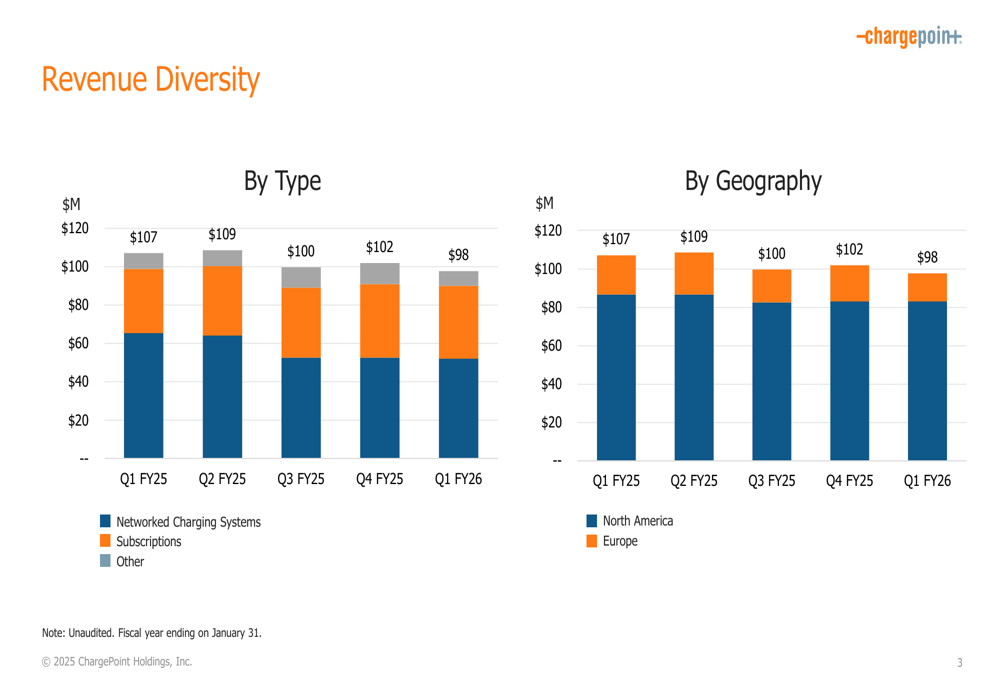

The company’s revenue is diversified across product types and geographies, with networked charging systems contributing the largest portion of revenue, followed by subscription services which are becoming increasingly important to the company’s business model.

As shown in the following chart of revenue diversity:

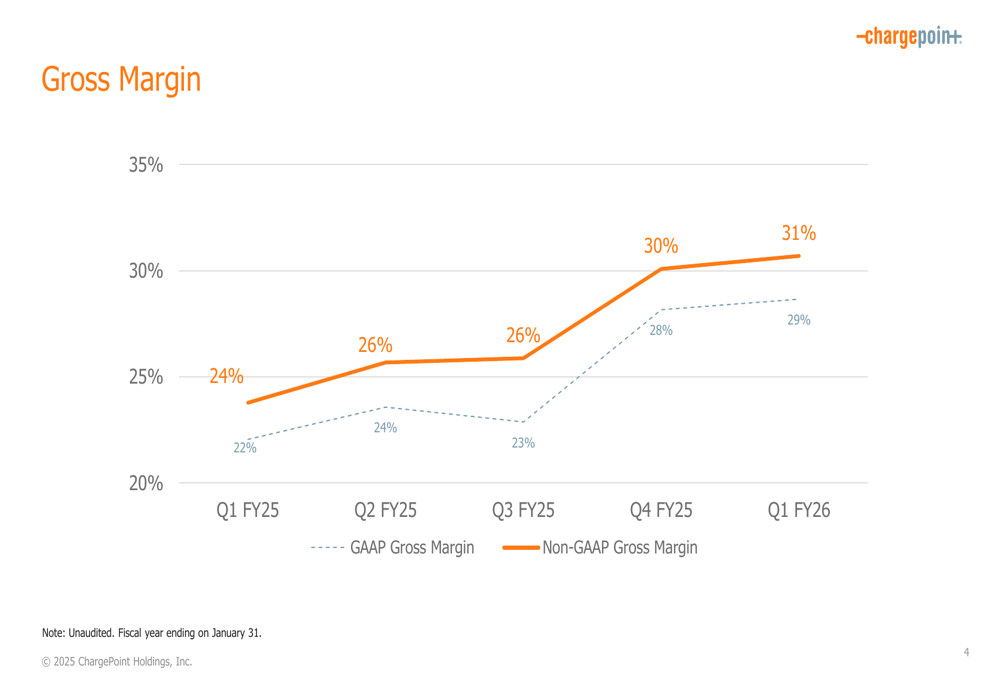

Gross margin showed substantial year-over-year improvement, with GAAP gross margin reaching 29% in Q1 FY2026, up from 22% in Q1 FY2025. Non-GAAP gross margin similarly improved to 31% from 24% in the prior year period, continuing a positive trend over the past five quarters.

The following chart illustrates ChargePoint’s consistent gross margin improvement:

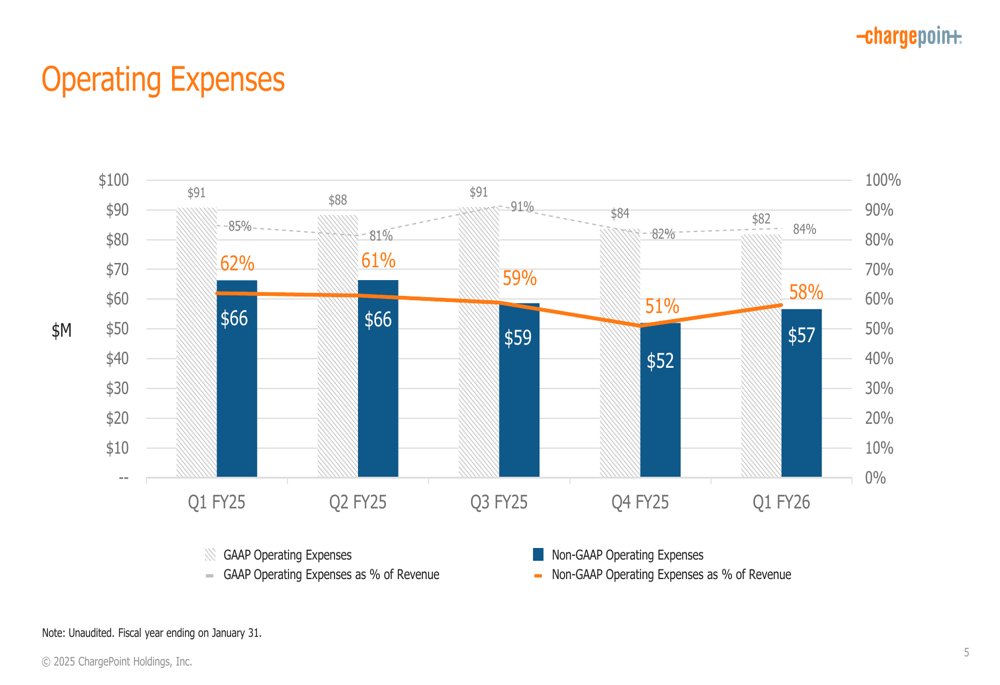

The company has made significant progress in controlling costs, with GAAP operating expenses of $81.83 million in Q1 FY2026, down from $90.75 million in Q1 FY2025. Non-GAAP operating expenses were $57 million, representing 58% of revenue compared to 62% in the prior year period.

The operating expense trends can be seen in this chart:

Detailed Financial Analysis

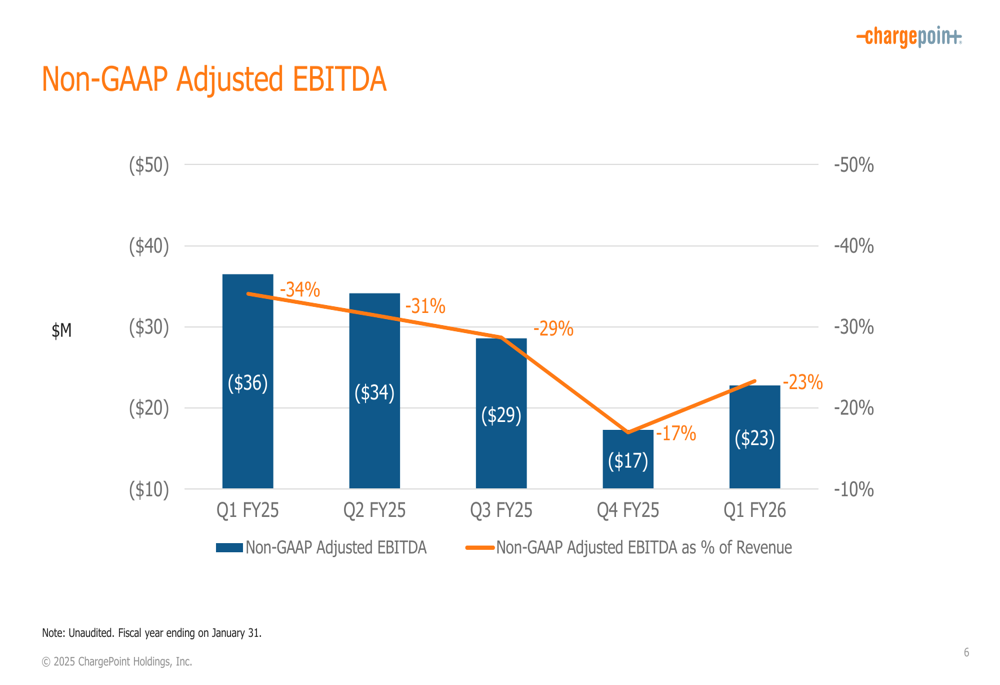

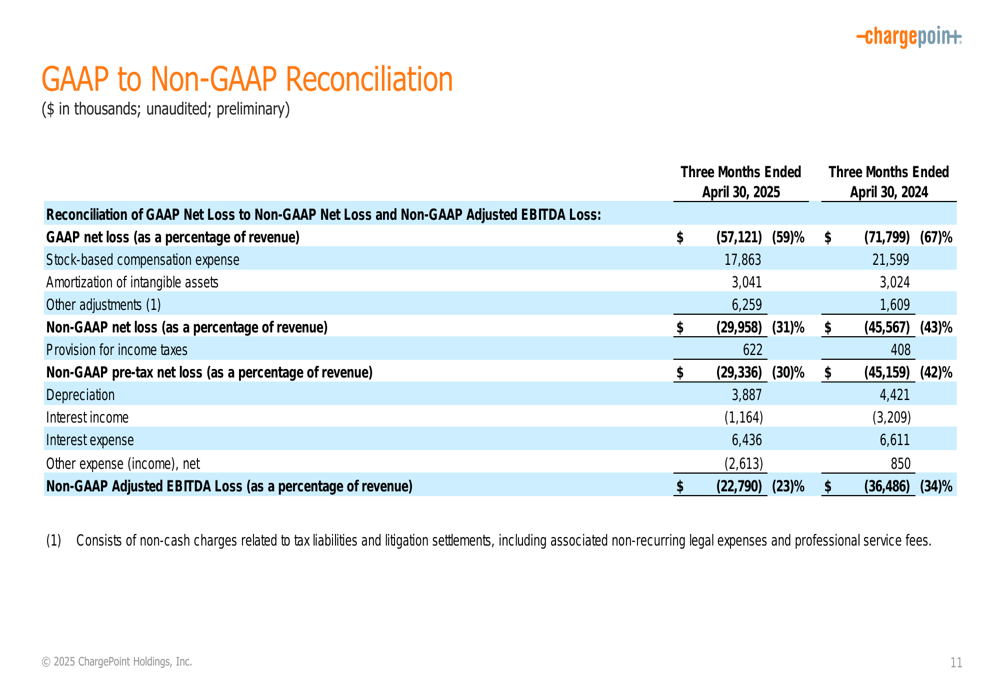

ChargePoint’s net loss improved to $(57.12) million in Q1 FY2026 from $(71.80) million in Q1 FY2025, representing a 20.4% reduction in losses year-over-year. The company’s non-GAAP adjusted EBITDA loss narrowed to $(22.79) million, or 23% of revenue, compared to $(36.49) million, or 34% of revenue, in the same quarter last year.

The following chart shows the improvement in non-GAAP adjusted EBITDA over the past five quarters:

Cash and cash equivalents stood at $195.95 million as of April 30, 2025, down from $224.57 million at the end of the previous quarter. The company’s cash burn has slowed significantly compared to the previous year, with net cash used in operating activities at $(32.97) million in Q1 FY2026, compared to $(62.54) million in Q1 FY2025, representing a 47.3% improvement.

The GAAP to non-GAAP reconciliation provides insight into the adjustments made to the company’s financial results:

Revenue by geography shows that North America remains ChargePoint’s largest market, contributing approximately $60 million in Q1 FY2026, while Europe generated about $38 million. The subscription segment has maintained stability at around $30 million per quarter, while networked charging systems revenue has fluctuated more significantly.

Forward-Looking Statements

ChargePoint continues to make progress toward its goal of achieving positive non-GAAP adjusted EBITDA in fiscal 2026. The company’s focus on improving gross margins and reducing operating expenses aligns with this objective, despite the year-over-year revenue decline.

In the previous quarter’s earnings call, CEO Rick Wilmer emphasized that "the move to EVs is inevitable" and that "free market forces will win the day." The company’s strategy appears focused on building a sustainable business model through improved operational efficiency and a growing base of recurring subscription revenue.

The reduction in cash burn rate and the sequential improvement in non-GAAP adjusted EBITDA suggest that ChargePoint is moving in the right direction, though challenges remain in driving top-line growth. With $195.95 million in cash and cash equivalents, the company has financial resources to continue executing its strategy while working toward profitability.

As the EV market continues to evolve, ChargePoint’s ability to balance growth investments with financial discipline will be crucial for long-term success. The company’s improving margins and reduced losses demonstrate progress, even as revenue growth remains a challenge in the current market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.