Affirm stock soars as Q1 earnings smash expectations, guidance lift

Introduction & Market Context

Charter Communications (NASDAQ:CHTR) presented its third-quarter 2025 results on October 31, revealing a mixed performance with declining traditional metrics but growing mobile and streaming segments. The company’s stock fell 6.03% in premarket trading after missing earnings expectations, with shares trading at $217, approaching its 52-week low of $215.93.

The cable and broadband provider reported an EPS of $8.34, missing analyst expectations of $9.27 by 10.03%, while revenue came in at $13.67 billion, slightly below forecasts of $13.75 billion. These results reflect ongoing challenges in a competitive telecommunications landscape characterized by low housing activity and increased competition from fiber and cellular internet providers.

Quarterly Performance Highlights

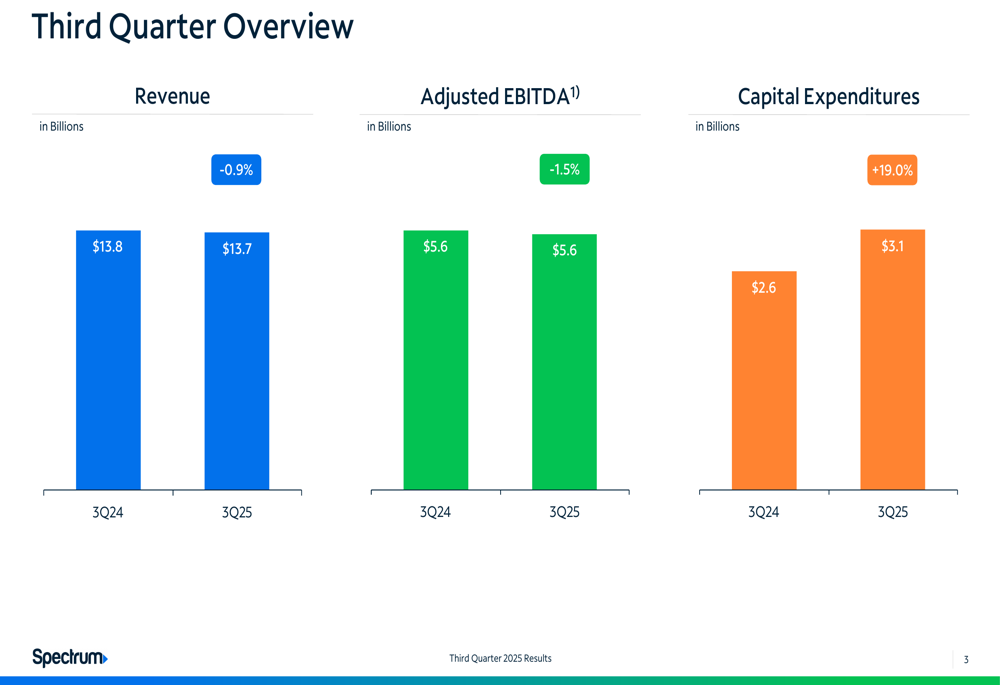

Charter’s third-quarter financial results showed year-over-year declines in key metrics. Revenue decreased by 0.9% to $13.7 billion, while adjusted EBITDA fell by 1.5% to $5.6 billion compared to the same period in 2024. Capital expenditures increased significantly by 19.0% to $3.1 billion.

As shown in the following chart of quarterly financial performance:

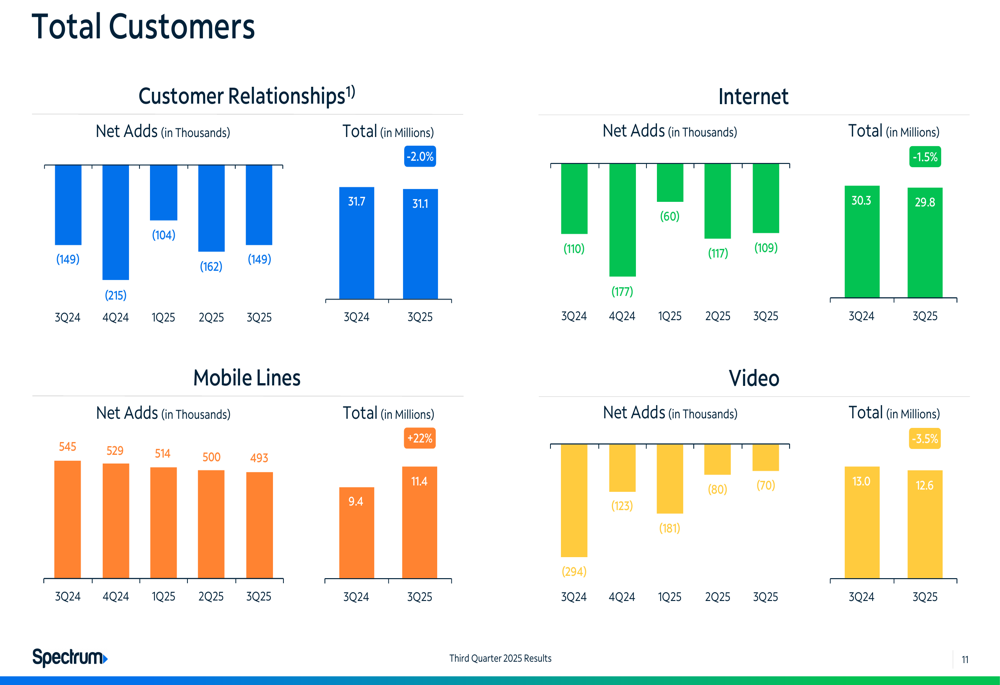

The company’s customer metrics revealed contrasting trends across different segments. Total customer relationships declined to 31.1 million, down from 31.7 million in Q3 2024. Internet customers decreased by 109,000 during the quarter to 29.8 million, while video subscribers fell by 70,000 to 12.6 million.

However, Charter’s mobile business continued to show strong momentum, with 493,000 line additions bringing the total to 11.4 million, up from 9.4 million a year ago. This represents a 21% penetration rate of Charter’s internet customer base.

Strategic Initiatives

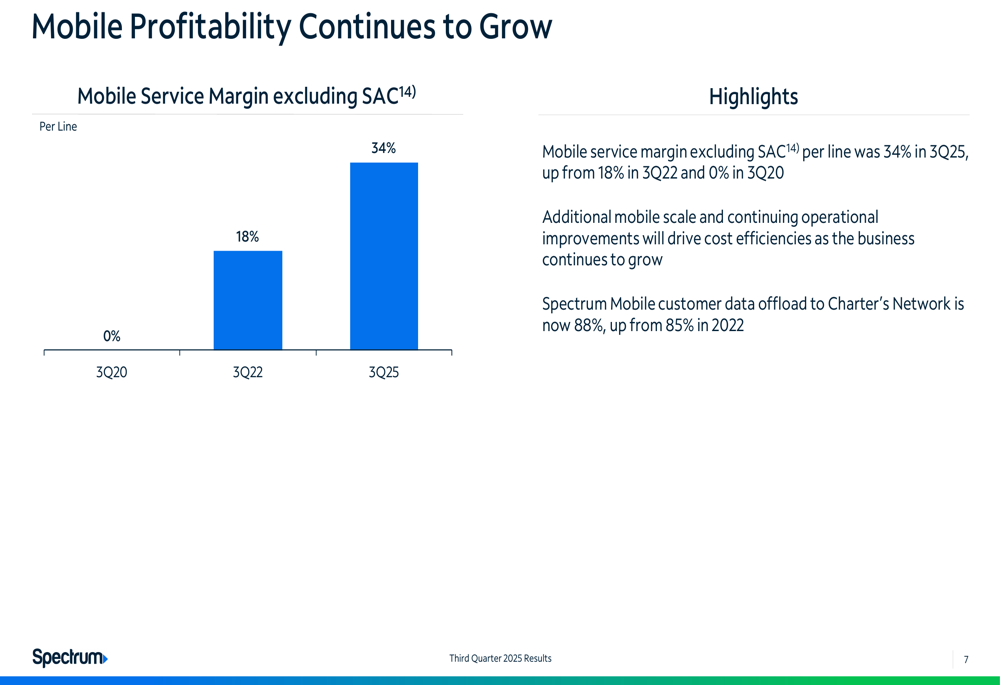

Charter is positioning itself as a value leader in the telecommunications market, emphasizing its competitive pricing compared to major wireless carriers. The company highlighted its mobile profitability improvements, with mobile service margin excluding subscriber acquisition costs reaching 34% in Q3 2025, up from 18% in Q3 2022 and 0% in Q3 2020.

The following chart illustrates Charter’s improving mobile service margins:

A key factor in this margin improvement is the increasing data offload to Charter’s network, which reached 88% in Q3 2025, up from 85% in 2022. This operational efficiency helps reduce the company’s costs for mobile data.

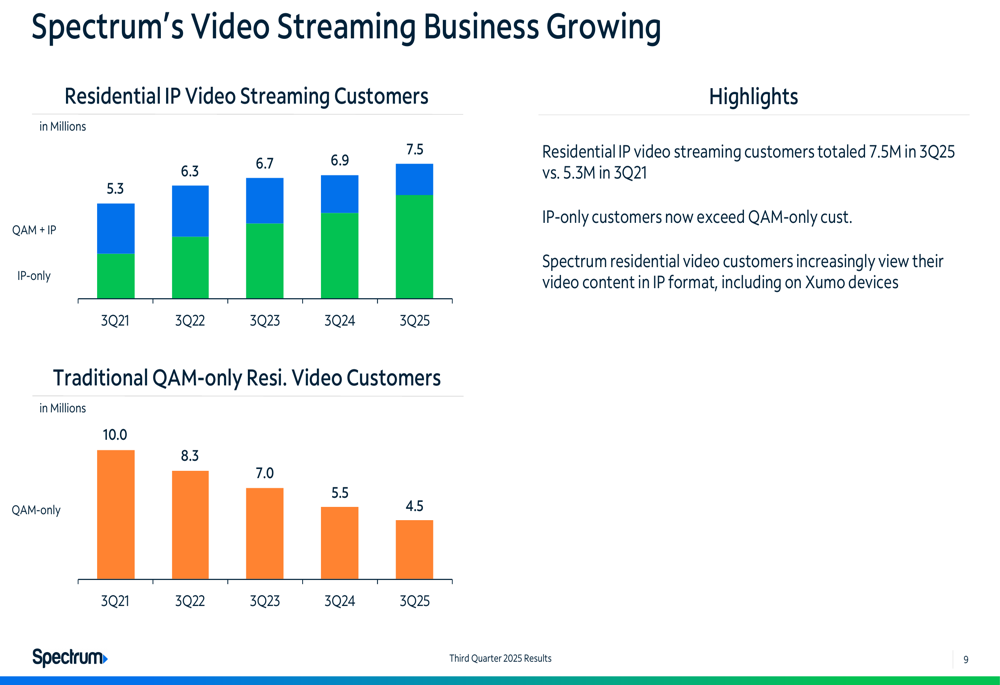

Charter is also successfully transitioning its video business from traditional cable to streaming platforms. Residential IP video streaming customers totaled 7.5 million in Q3 2025, up from 5.3 million in Q3 2021, with IP-only customers now exceeding traditional QAM-only customers.

The following graph shows the growth trajectory of Charter’s streaming video business:

Forward-Looking Statements

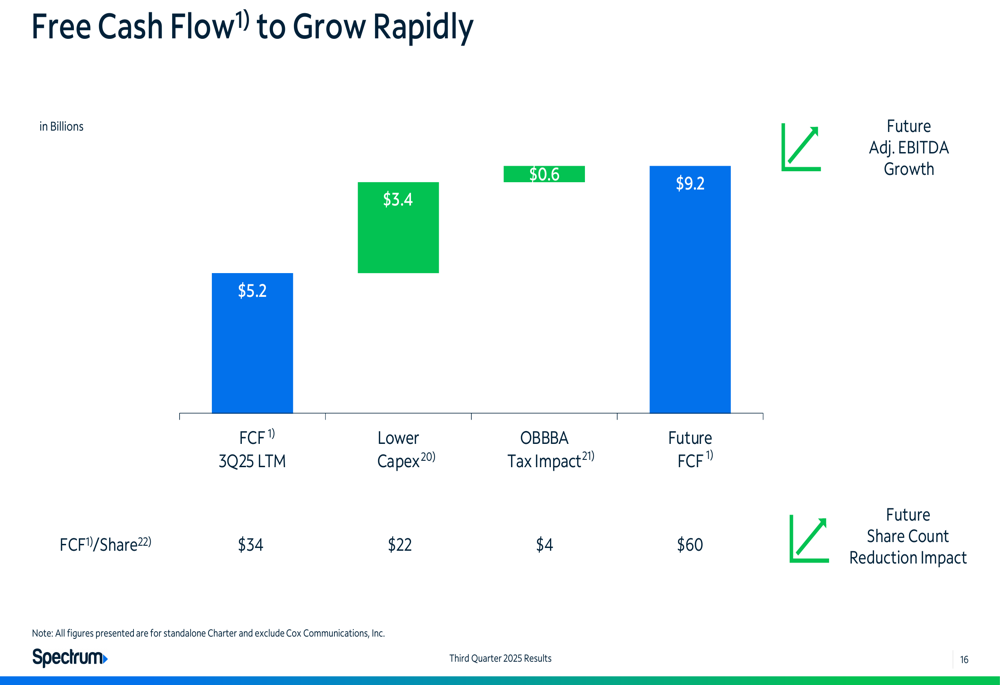

Despite current challenges, Charter is focusing on future free cash flow growth. The company generated $1,621 million in free cash flow during Q3 2025, slightly up from $1,619 million in Q3 2024, while LTM free cash flow increased to $5,215 million from $4,334 million.

As illustrated in the following free cash flow and share repurchase data:

Charter continues to return capital to shareholders through its buyback program, repurchasing 7.6 million shares at an average price of $292, representing 2.4% of fully diluted outstanding shares during the quarter.

Looking ahead, the company expects significant free cash flow growth potential as capital expenditures normalize. Current FCF stands at $5.2 billion, but Charter projects this could increase to $9.2 billion with reduced capex and tax impacts.

The company’s strategy to drive value focuses on three key areas: operating strategy (high-quality products, unique customer value, commitment to service), strategic initiatives (evolution, expansion, execution), and shareholder value (long-term revenue and cash flow growth, leveraged equity returns).

Detailed Financial Analysis

Breaking down Charter’s revenue components, residential revenue was $10.6 billion in Q3 2025, down from $10.8 billion in Q3 2024. Commercial revenue remained flat at $1.8 billion. However, connectivity revenue grew by 3.8% year-over-year, showing strength in the company’s core business.

The following chart details Charter’s revenue breakdown:

On the expense side, total costs remained flat at $8.1 billion in both Q3 2024 and Q3 2025, while adjusted EBITDA was $5.6 billion in both periods. Over the last twelve months, adjusted EBITDA grew by 1.8% year-over-year to $22.8 billion.

The following chart shows Charter’s expense and EBITDA trends:

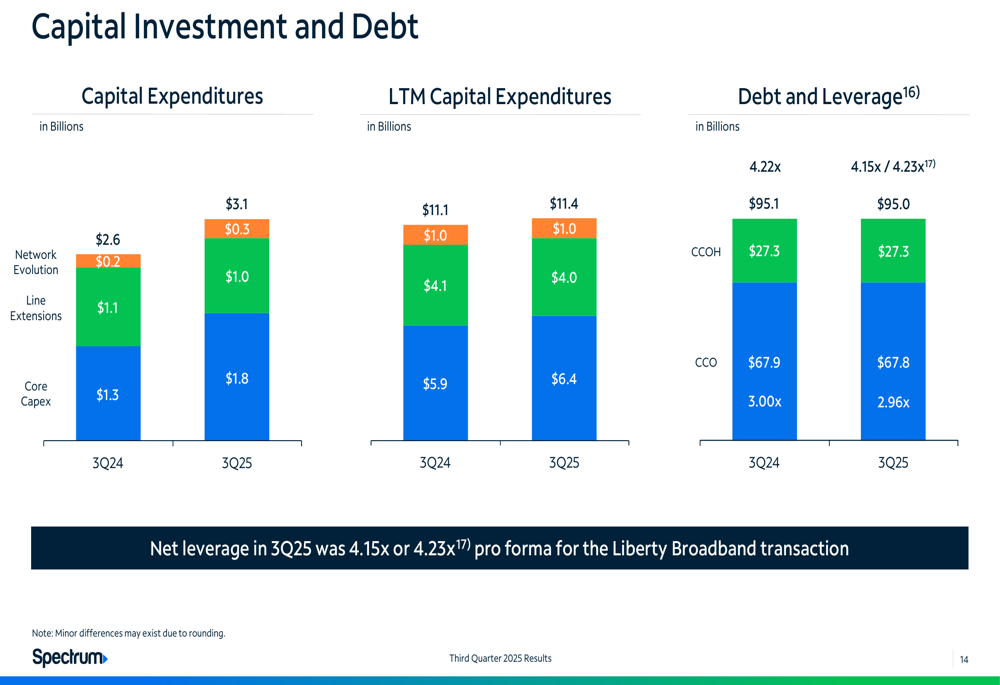

Capital expenditures for Q3 2025 included $1.8 billion in core capex, $1.0 billion in line extensions, and $0.3 billion in network evolution, totaling $3.1 billion. The company’s net leverage ratio stood at 4.15x, or 4.23x pro forma for the Liberty Broadband transaction, with total debt of $95 billion.

CEO Chris Winfrey expressed confidence in Charter’s ability to grow its internet customer base again despite current challenges, emphasizing the company’s unique product offerings and focus on generating free cash flow growth. Looking forward, Charter expects full-year 2025 EBITDA to be flat or marginally positive, with capital expenditures peaking this year.

The company’s pending acquisition of Cox Communications, anticipated by mid-2026, is expected to further enhance its market position as Charter navigates the evolving telecommunications landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.