Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

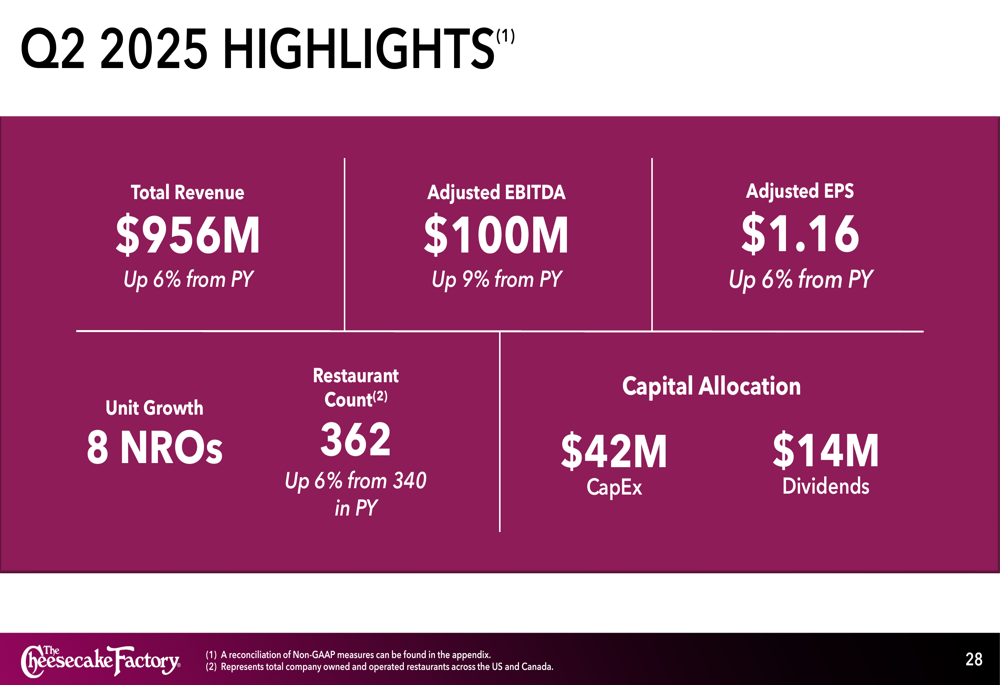

The Cheesecake Factory (NASDAQ:CAKE) presented its Q2 2025 investor presentation on July 29, highlighting solid financial performance and ambitious expansion plans across its diversified restaurant portfolio. The company reported total revenue of $956 million, up 6% year-over-year, with adjusted EBITDA rising 9% to $100 million and adjusted EPS increasing 6% to $1.16.

The results continue the company’s trend of strong earnings growth, following its Q1 2025 performance where it exceeded analyst expectations with EPS of $0.93 against a forecast of $0.81. CAKE shares closed at $65.89 on July 29, down 4.17% in regular trading, but gained 0.53% in after-hours trading following the presentation.

Quarterly Performance Highlights

The Cheesecake Factory’s Q2 2025 performance showed continued momentum across its core financial metrics, with particular strength in its flagship brand.

As shown in the following financial summary:

The company’s Q2 2025 results reflect solid growth across key metrics, with total revenue increasing 6% year-over-year to $956 million. Adjusted EBITDA rose 9% to $100 million, while adjusted EPS grew 6% to $1.16. The company also expanded its restaurant count by 6% to 362 locations, up from 340 in the prior year.

Comparable sales performance varied across brands, with the flagship Cheesecake Factory restaurants posting a 1.2% increase in Q2 2025, while North Italia experienced a 1% decline and Fox Restaurant Concepts saw a 2% increase.

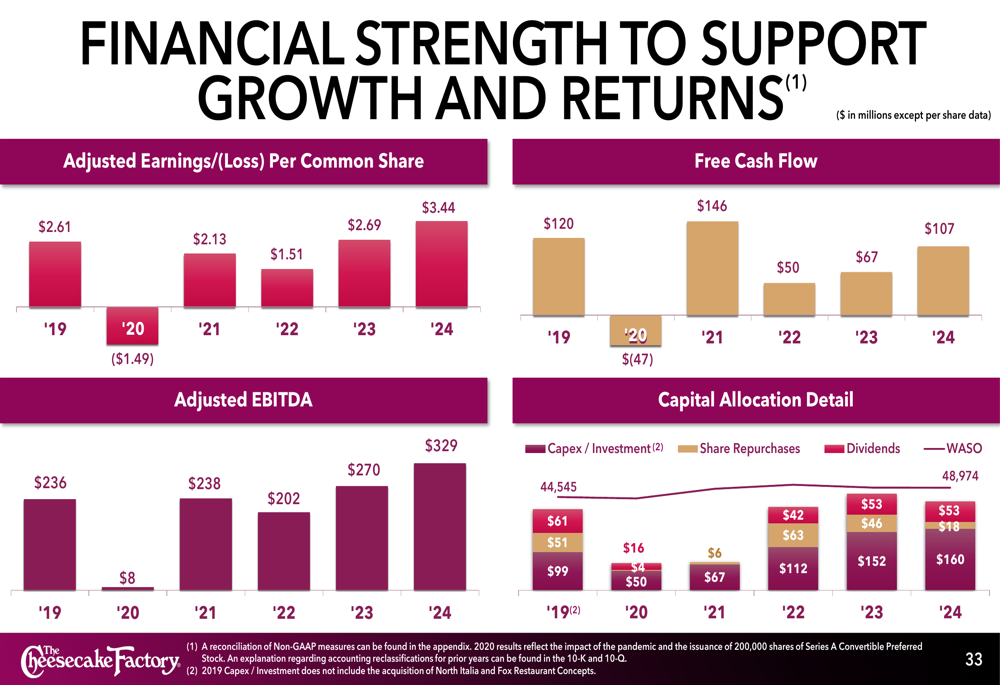

The company’s historical financial performance demonstrates consistent improvement since the pandemic, with adjusted earnings per share growing from -$1.49 in 2020 to $3.44 in 2024:

Strategic Initiatives

The Cheesecake Factory is accelerating its unit growth strategy, with plans to open as many as 25 new restaurants in 2025, representing a significant increase from 13 in 2022, 16 in 2023, and 23 in 2024. The company has already opened 17 new restaurants year-to-date across its portfolio of brands.

As illustrated in the company’s expansion plan:

The expansion strategy includes a diversified approach across the company’s portfolio, with 4 new Cheesecake Factory locations, 6 North Italia locations, 6 Flower Child locations, and 9 Fox Restaurant Concepts restaurants planned for 2025.

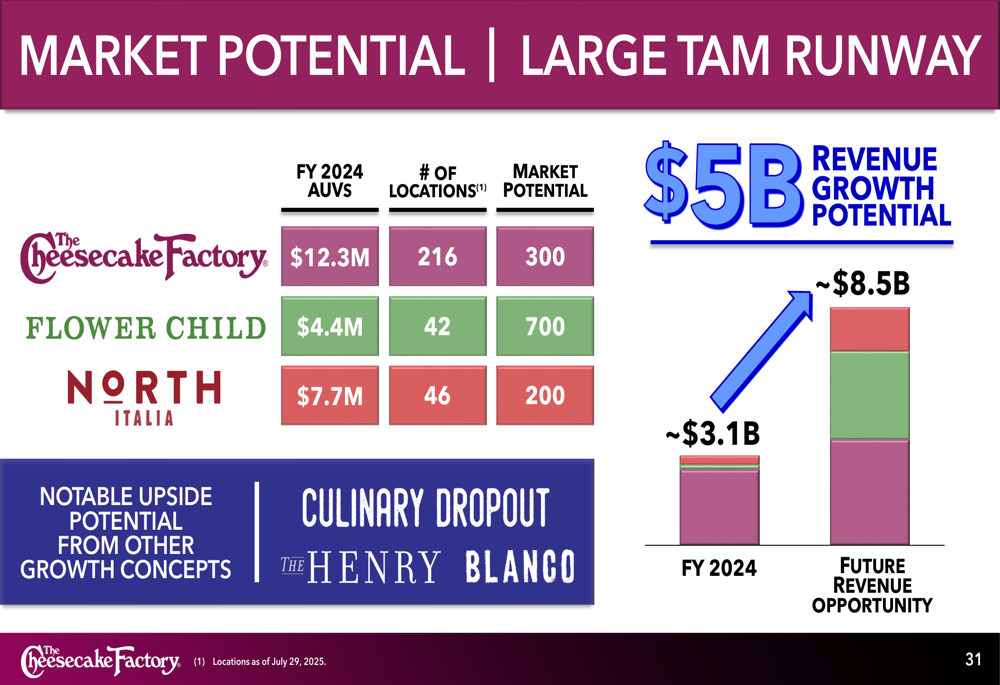

This growth is supported by the company’s assessment of significant market potential across its brands:

The company sees substantial runway for growth, with market potential for 300 Cheesecake Factory locations (currently 216), 200 North Italia locations (currently 46), and 700 Flower Child locations (currently 42). This expansion potential represents approximately $5 billion in additional revenue opportunity, potentially growing from the current $3.1 billion to $8.5 billion over time.

Competitive Industry Position

The Cheesecake Factory maintains several competitive advantages in the casual dining sector, including industry-leading unit economics, strong off-premise sales, and exceptional staff retention.

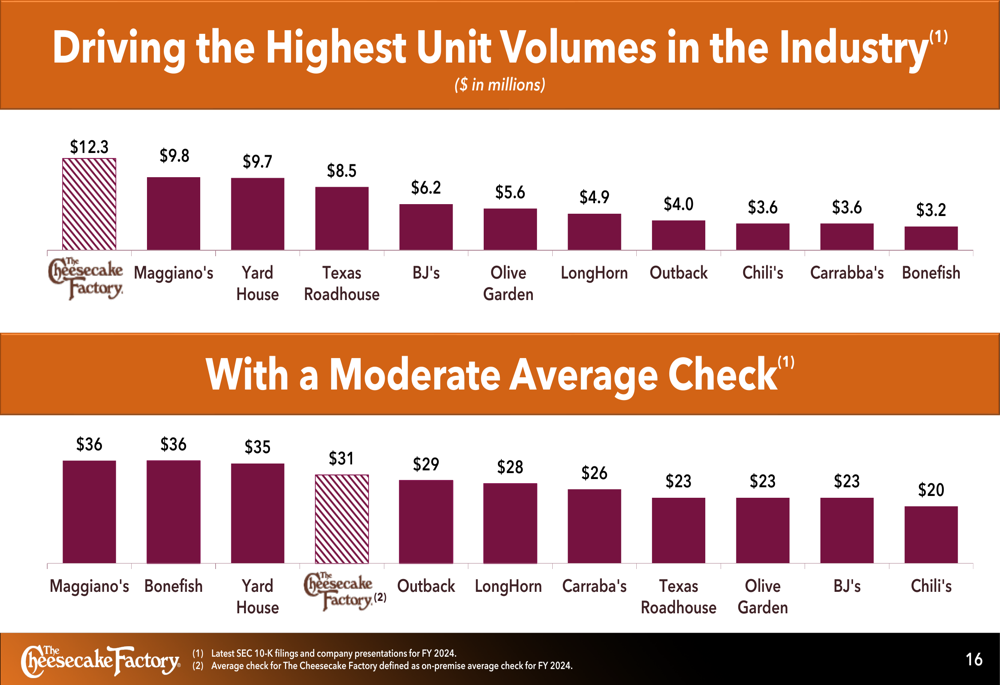

The company’s restaurants generate the highest average unit volumes in the casual dining industry:

With average unit volumes of $12.3 million, Cheesecake Factory significantly outperforms competitors like Maggiano’s ($9.8M), Yard House ($9.7M), and Texas Roadhouse (NASDAQ:TXRH) ($8.5M), despite maintaining a moderate average check of $31.

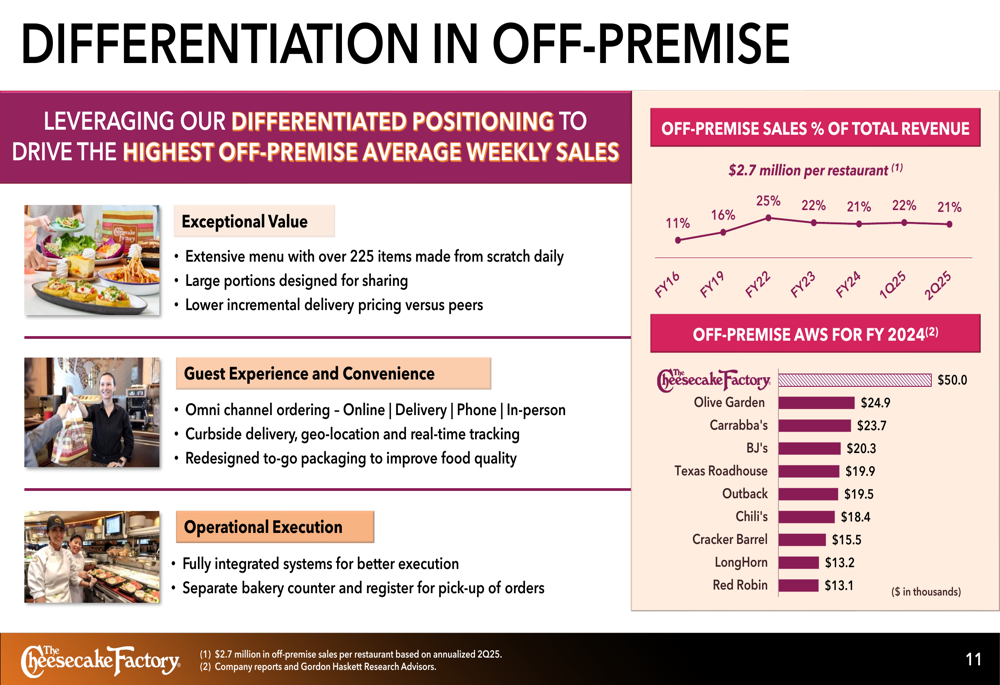

The company has also established a strong position in off-premise dining, which represents 21% of total revenue in Q2 2025:

Cheesecake Factory’s off-premise average weekly sales of $50.0 million substantially exceed competitors like Olive Garden ($24.9M), Carrabba’s ($23.7M), and BJ’s ($20.3M), highlighting the company’s success in adapting to changing consumer preferences for takeout and delivery.

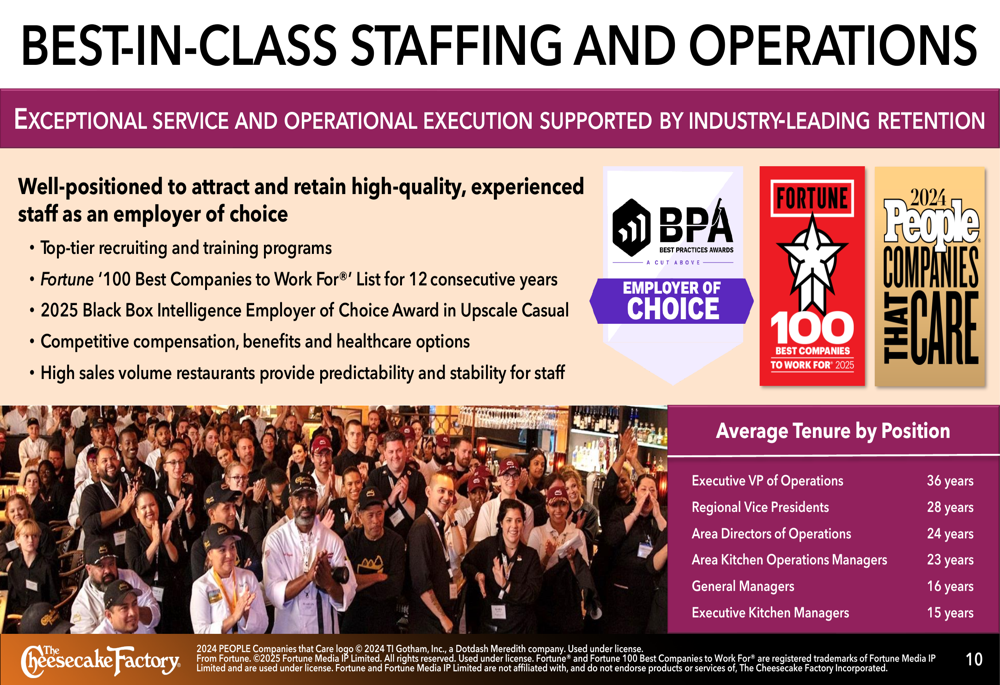

Another key competitive advantage is the company’s ability to attract and retain experienced staff:

The company has been recognized on Fortune’s "100 Best Companies to Work For" list for 12 consecutive years and boasts impressive staff retention, with executive leadership tenure ranging from 15 to 36 years. This stability contributes to operational excellence and consistent guest experiences.

Forward-Looking Statements

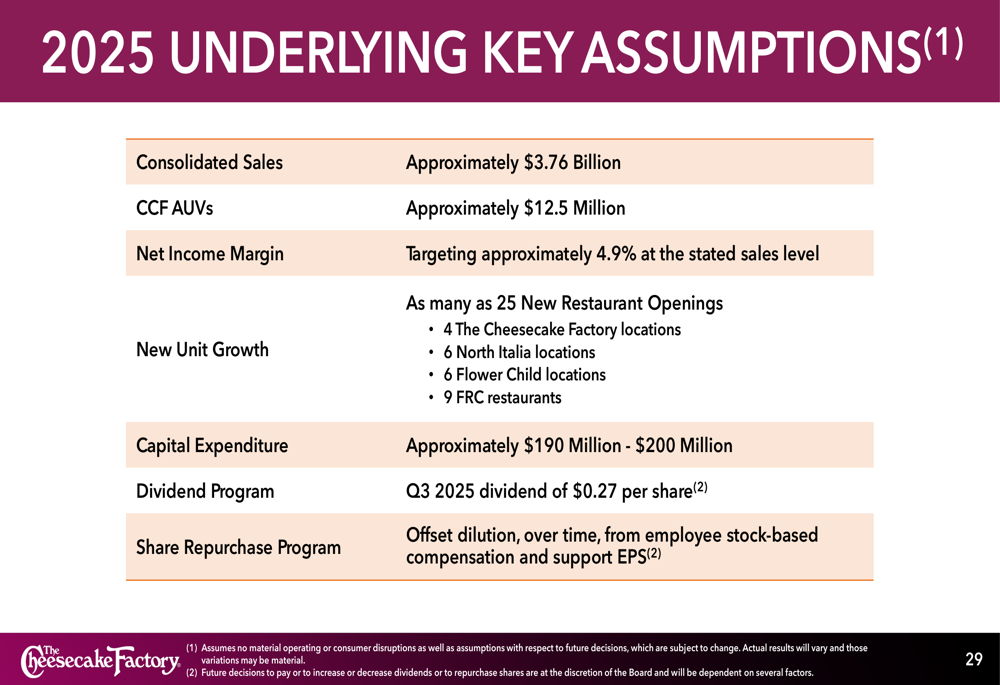

For the full year 2025, The Cheesecake Factory provided the following guidance:

The company expects consolidated sales of approximately $3.76 billion for 2025, with Cheesecake Factory average unit volumes of approximately $12.5 million. Management is targeting a net income margin of approximately 4.9% at the stated sales level, slightly higher than the 4.75% mentioned in previous guidance.

Capital expenditures are projected at $190-200 million to support the planned unit growth of up to 25 new restaurants. The company also announced a Q3 2025 dividend of $0.27 per share and plans to continue its share repurchase program to offset dilution from employee stock-based compensation.

Long-term, the company is targeting average annual growth of 1-2% in comparable sales and 7-8% in top-line revenue, driven by its multi-brand expansion strategy across various dining segments and price points.

The Cheesecake Factory’s diversified portfolio positions it to capitalize on different dining trends and occasions, with a focus on experiential concepts that deliver strong unit economics and growth potential:

With its flagship Cheesecake Factory brand focused on global expansion, North Italia and Flower Child targeted for national growth, and emerging concepts like Culinary Dropout in testing phases, the company has created multiple avenues for sustainable long-term growth in the competitive restaurant industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.