Oil prices push higher amid worries over Russian supply disruptions

Introduction & Market Context

Cherry Hill Mortgage Investment Corporation (NYSE:CHMI) released its second quarter 2025 investor presentation on August 7, revealing continued pressure on book value despite efforts to optimize its portfolio mix. The mortgage REIT, which offers a high-yield dividend currently trading at $2.79 per share (down 3.46% in the latest session), continues to navigate a challenging interest rate environment while maintaining its dividend payments.

The presentation comes after Cherry Hill completed its first full quarter as an internally managed REIT, a transition that was highlighted in its previous earnings call. Despite beating EPS expectations in Q1 2025, the company’s stock has continued to trade closer to its 52-week low of $2.34 than its high of $3.81, reflecting ongoing investor concerns about its financial performance.

Quarterly Performance Highlights

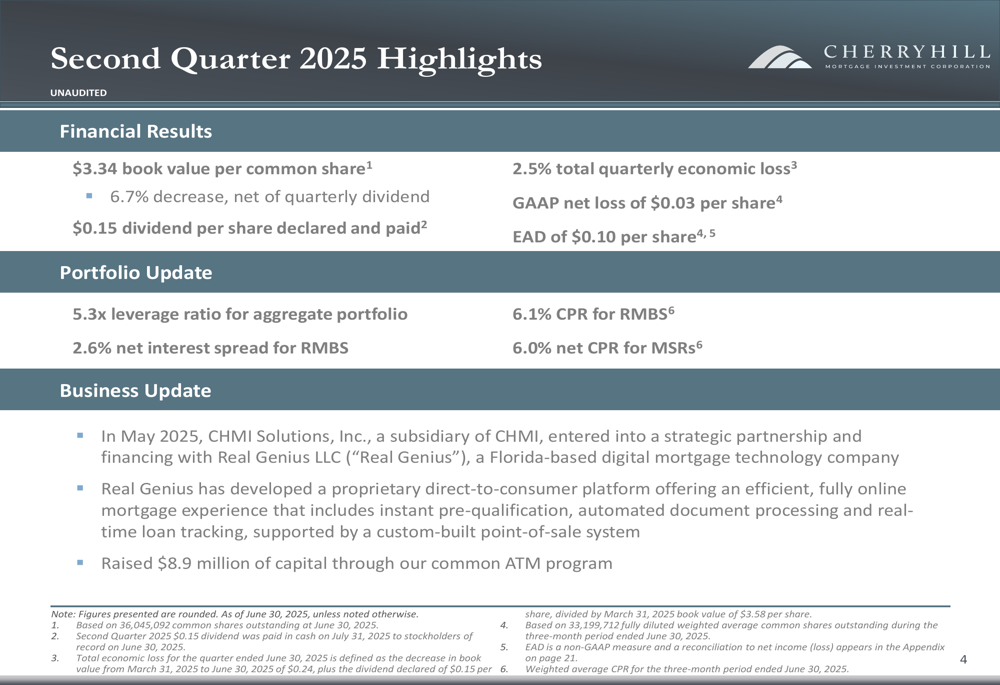

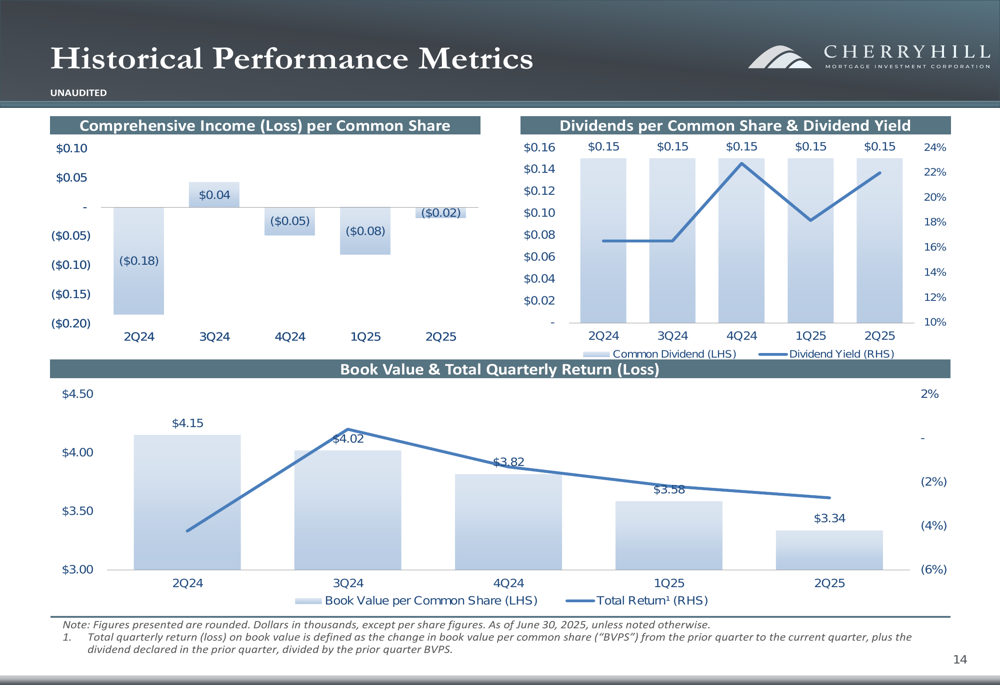

Cherry Hill reported a GAAP net loss per share of $0.03 for Q2 2025, a significant improvement from the $0.29 loss reported in the previous quarter. However, Earnings Available for Distribution (EAD) declined to $0.10 per share from $0.17 in Q1. The company maintained its quarterly dividend at $0.15 per share despite the continued pressure on earnings.

As shown in the following summary of key financial metrics from the second quarter:

Book value per common share fell to $3.34, representing a 6.7% decrease from the previous quarter’s $3.58, continuing a concerning downward trend that has persisted over the past year. The total quarterly economic loss stood at 2.5%, reflecting the combined impact of the dividend payment and book value erosion.

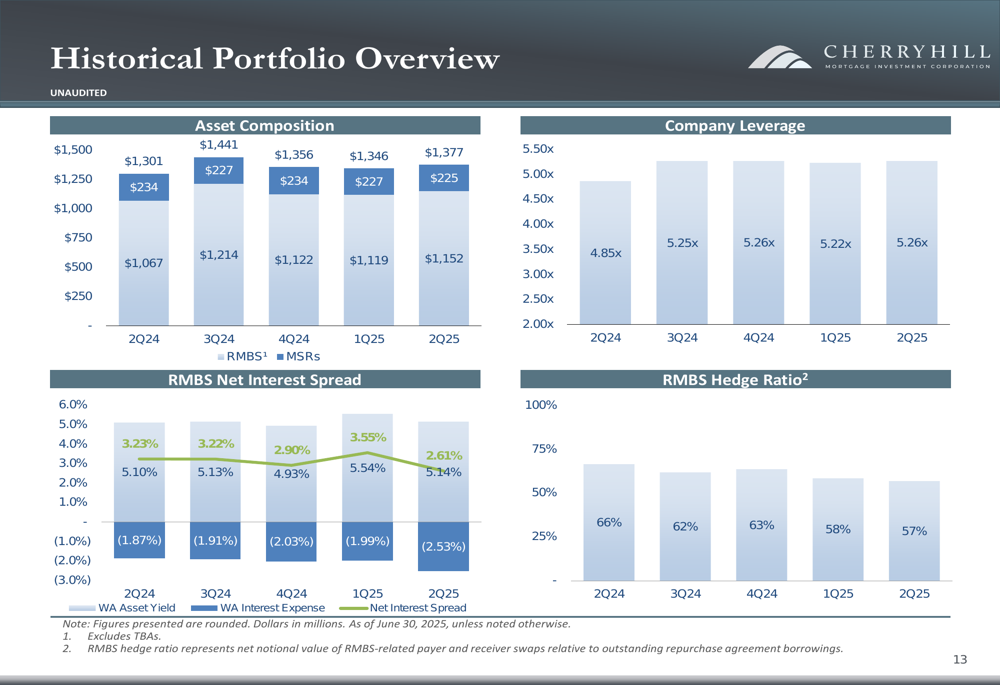

The company’s leverage ratio remained relatively stable at 5.3x, while the net interest spread for RMBS decreased to 2.6% from 3.55% in the previous quarter, indicating compression in profit margins on its mortgage-backed securities portfolio.

Portfolio Composition and Strategy

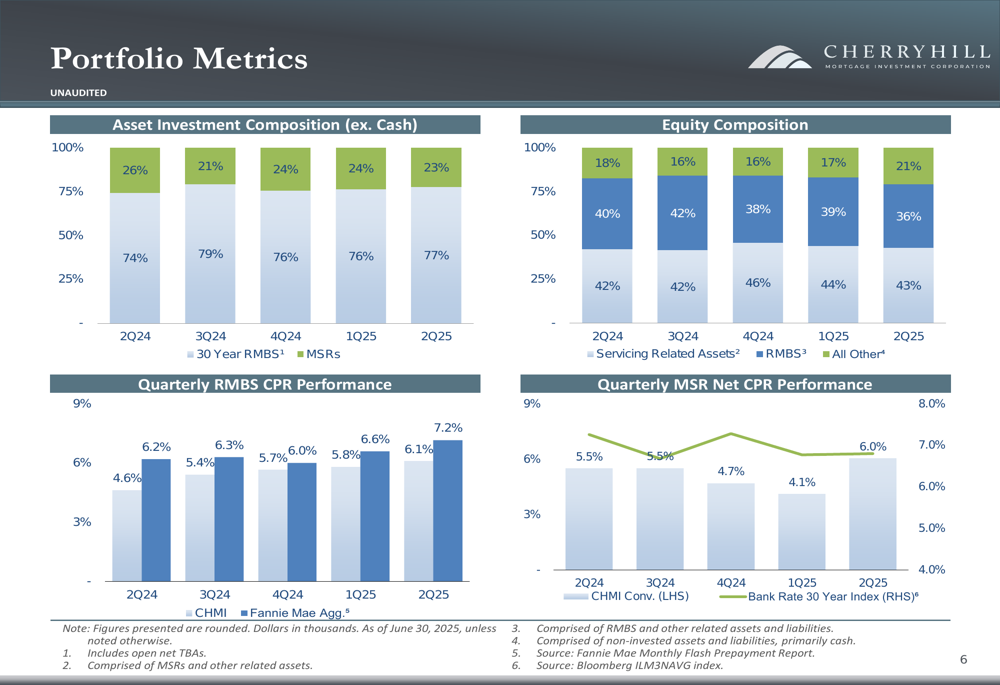

Cherry Hill continues to maintain a balanced approach to its investment portfolio, with 77% allocated to Residential Mortgage-Backed Securities (RMBS) and 23% to Mortgage Servicing Rights (MSRs) as of Q2 2025. This composition has remained relatively stable over recent quarters, as illustrated in the following chart:

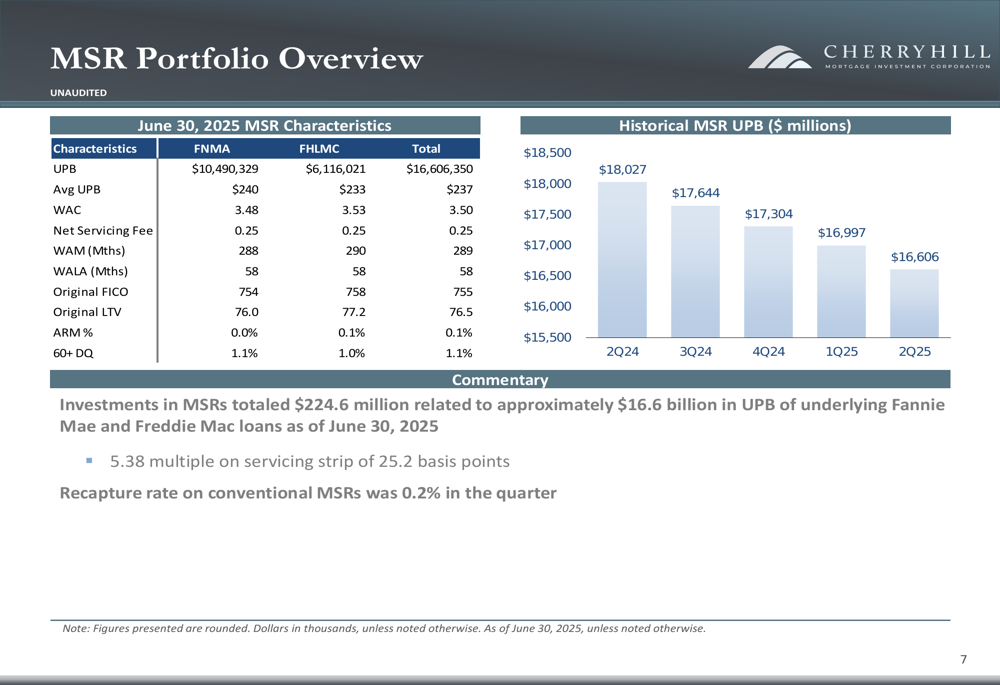

The company’s MSR portfolio totaled $224.6 million related to approximately $16.6 billion in unpaid principal balance (UPB) of underlying Fannie Mae (OTC:FNMA) and Freddie Mac (OTC:FMCC) loans. The portfolio characteristics reveal a weighted average coupon of 3.50% and a weighted average loan age of 58 months, suggesting a seasoned portfolio of mostly fixed-rate mortgages with strong credit metrics (average FICO of 755).

The detailed breakdown of the MSR portfolio shows the following characteristics:

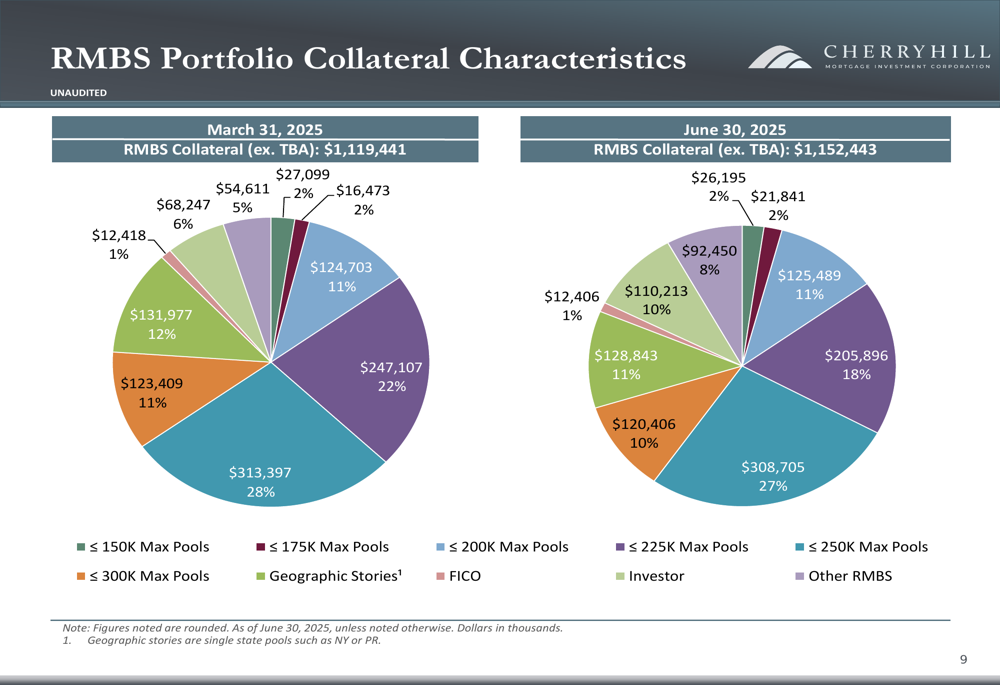

On the RMBS side, Cherry Hill’s portfolio is diversified across various coupon rates, with a fair market value of $755.5 million. The company has strategically positioned its RMBS holdings, as shown in the collateral characteristics comparison between Q1 and Q2 2025:

The shift in allocation between March and June 2025 demonstrates the company’s active management approach, with notable increases in ≤175K Max Pools (from 6% to 11%) and the addition of an 18% allocation to Investor pools, while reducing exposure to ≤250K Max Pools (from 22% to 11%).

Financial Position and Outlook

Cherry Hill’s historical performance metrics reveal a concerning trend of declining book value and inconsistent comprehensive income results. The following chart illustrates these trends over the past five quarters:

The company has maintained its dividend payment at $0.15 per share despite the continued book value erosion, which may raise questions about dividend sustainability if the negative trend continues. The comprehensive loss per common share improved to $(0.02) in Q2 2025 from $(0.08) in the previous quarter.

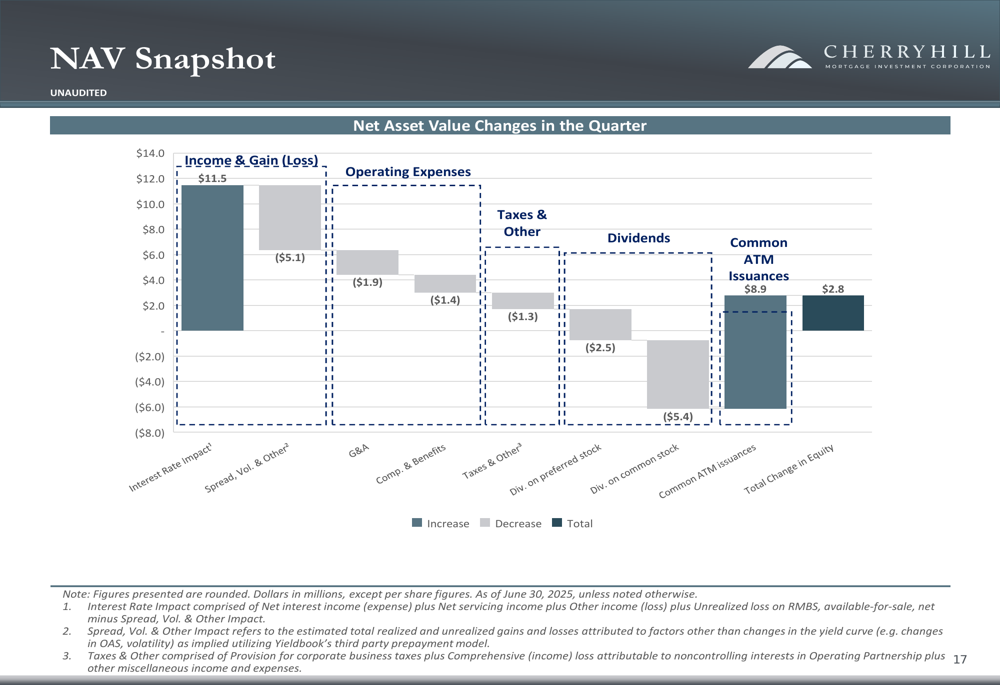

The NAV snapshot provides insight into the factors contributing to the changes in equity during the quarter:

Cherry Hill’s financing arrangements include repurchase agreements with multiple counterparties, with an average repo cost of 4.5% and a weighted average maturity of 26 days. The company has established 35 repo relationships and is currently borrowing from 13 financing counterparties, demonstrating efforts to diversify funding sources.

Risk Factors and Sensitivity

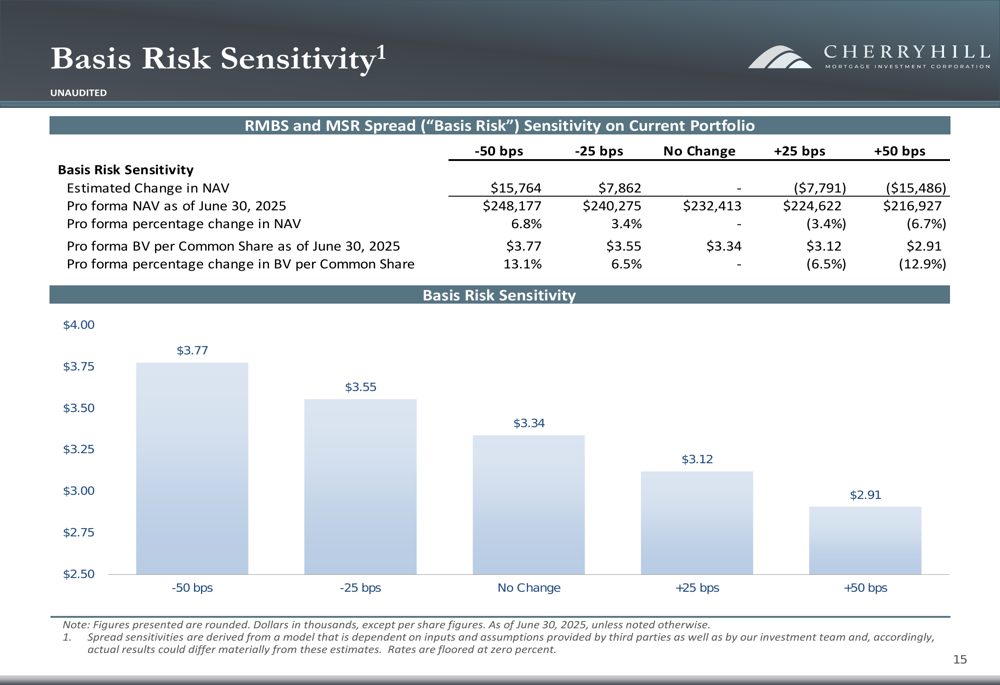

The presentation highlights Cherry Hill’s sensitivity to both basis risk and interest rate fluctuations. The company’s portfolio shows moderate sensitivity to changes in interest rates, with book value per share estimated to change by approximately 0.4-0.5% for every 25 basis point move in rates.

However, the basis risk sensitivity is more pronounced, with a potential 6.5% change in book value per share for a 25 basis point move in mortgage basis spreads, as illustrated in the following analysis:

This sensitivity underscores the challenges Cherry Hill faces in the current volatile interest rate environment. The company’s hedging strategy includes a combination of payer swaps, receiver swaps, and treasury futures, with weighted average durations of 3.0 years and 2.8 years on payer and receiver swaps, respectively.

Cherry Hill’s historical portfolio overview shows that the company has maintained a relatively stable leverage ratio while experiencing fluctuations in net interest spread:

The decline in net interest spread from 3.55% in Q1 2025 to 2.61% in Q2 2025 represents a significant compression that has likely contributed to the reduced earnings available for distribution.

As Cherry Hill continues to navigate the challenging mortgage market, investors will be watching closely to see if the company can stabilize its book value and improve its earnings performance while maintaining its dividend payments. The strategic partnership with Real Genius LLC and the $8.9 million raised through the ATM program may provide additional flexibility, but the persistent downward trend in book value remains a significant concern for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.