Michigan survey ahead; Applied Digital surges; gold dips - what’s moving markets

Cherry SE (ETR:C3RY) presented its Q2/H1 2025 results on July 31, revealing significant revenue challenges across most business segments while its Digital Health & Solutions (DH&S) division continues to show promise. The company reported substantial progress in inventory reduction and financing restructuring as it navigates a challenging German economy.

Quarterly Performance Highlights

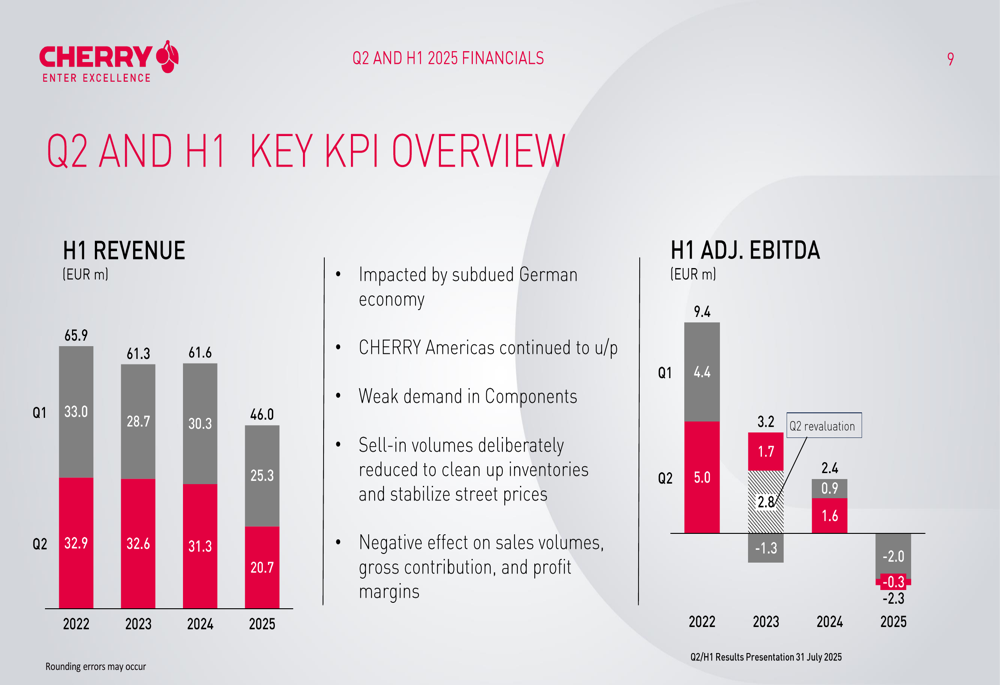

Cherry reported H1 2025 revenue of €46.0 million, representing a 25% year-over-year decline. The adjusted EBITDA margin deteriorated to -5.0%, down 9 percentage points from the previous year. Despite these challenges, the company maintained €7.9 million in cash, up 18% quarter-over-quarter, with an equity ratio of 45.6%.

The company’s performance has been on a downward trend over recent years, with H1 revenue declining from €65.9 million in 2022 to the current €46.0 million in 2025.

As shown in the following chart of quarterly revenue and adjusted EBITDA:

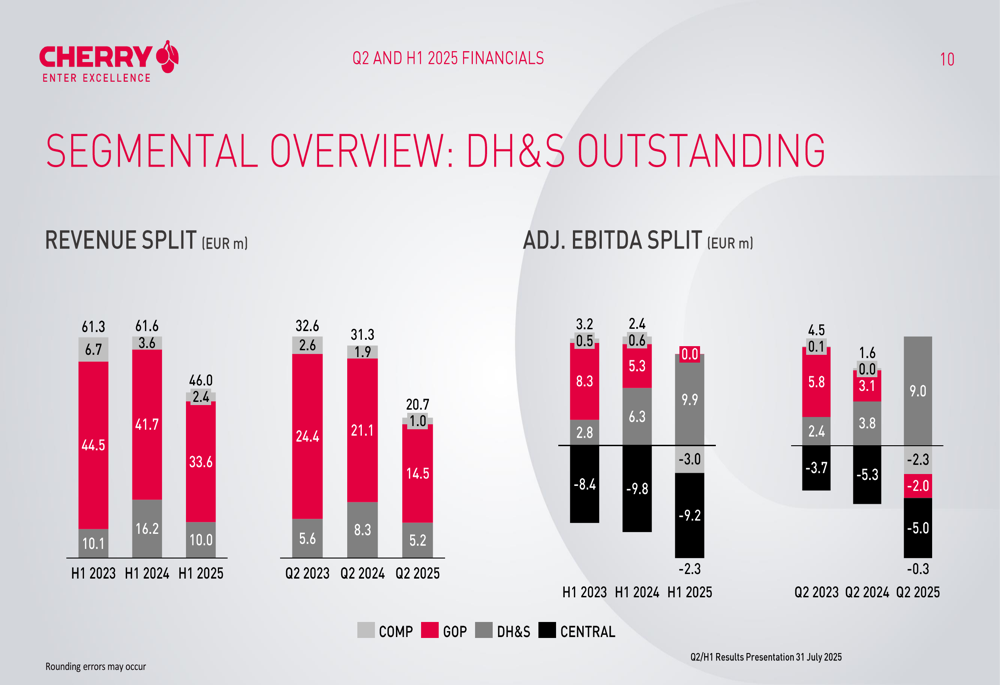

The segmental breakdown reveals stark differences in performance across Cherry’s business units. While the DH&S segment maintained strong profitability with a H1 2025 adjusted EBITDA of €9.9 million, both the Components (COMP) and Gaming/Office Peripherals (GOP) segments struggled to generate positive earnings.

The following chart illustrates the segmental performance:

Strategic Initiatives

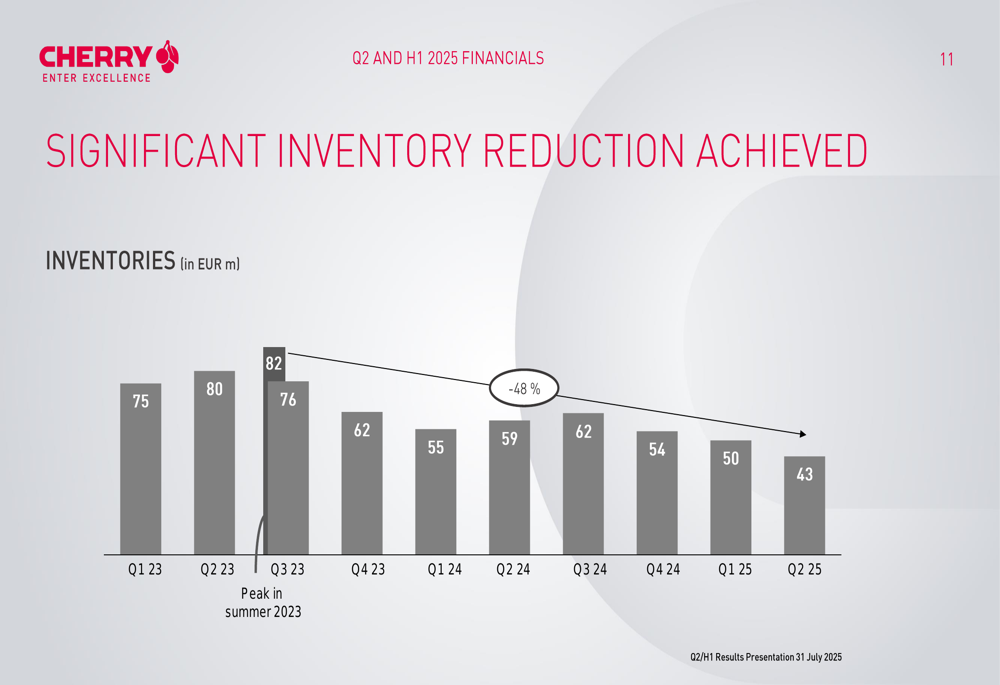

Cherry has made significant progress in reducing inventory levels, which peaked at €82 million in summer 2023 and have since been cut by 48% to €43 million as of Q2 2025. This reduction has been driven by a realigned partner network, identification of balanced distribution channels, and SKU reduction.

The company’s inventory reduction progress is illustrated in this chart:

In April 2025, Cherry extended its loan agreement with UniCredit to December 31, 2027, while reducing the loan amount from €25 million to €23 million. Additionally, in May 2025, the company completed the sale of its Hygiene Peripherals business for €21 million, with €10.4 million paid at closing and the remainder contingent on performance targets through December 2026.

CEO Oliver Kaltner outlined Cherry’s strategic goal to become "an international provider of agnostic, digital ecosystems," with the DH&S segment playing a central role in this transformation. This represents a shift from project-based hardware sales to "multiple predictable and recurring software revenue streams."

Digital Health & Solutions Performance

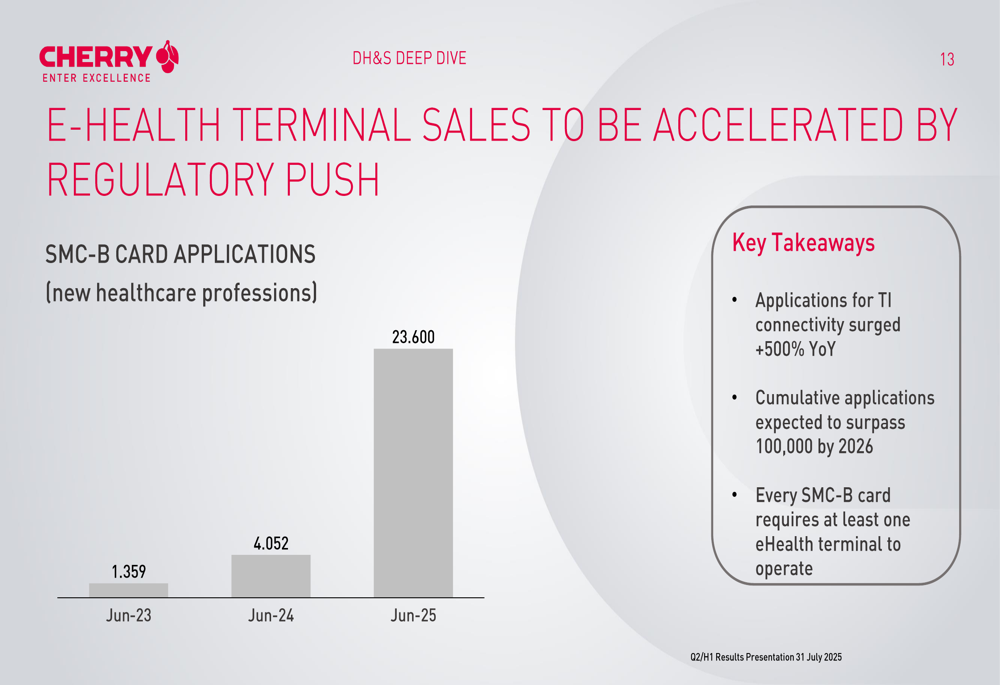

The DH&S segment stands out as Cherry’s most promising business unit. E-health terminal sales have accelerated due to regulatory requirements, with SMC-B card applications surging by 500% year-over-year to 23,600 in June 2025, compared to just 4,052 in June 2024.

The regulatory-driven growth in SMC-B card applications is shown in the following chart:

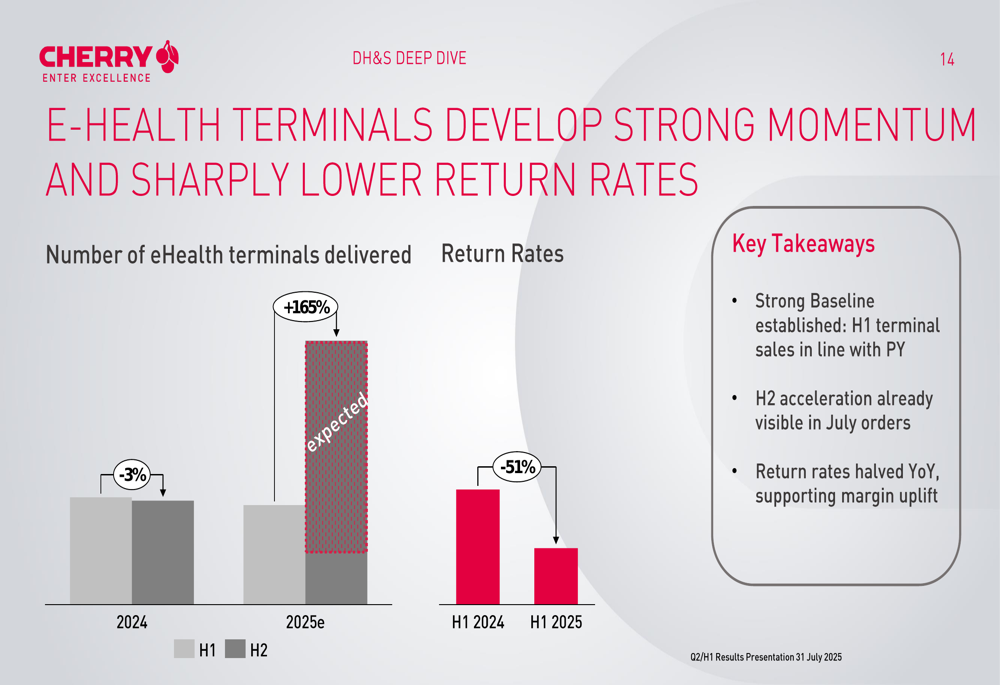

Cherry expects e-health terminal deliveries to increase by 165% in 2025, while return rates have decreased by 51% year-over-year, supporting margin improvement. The company notes that only 30% of elderly care institutions are currently connected to the Telematics Infrastructure (TI), representing a significant growth opportunity with 32,000 institutions still to address in H2 2025.

The company’s e-health terminal momentum is illustrated here:

Cherry is also shifting its strategic focus from Smartlink to TI-Messenger (TI-M) as a "highly scalable platform" with "superior potential." Provider certification is expected within 10-15 days, which would unlock go-to-market opportunities.

Market Position and Outlook

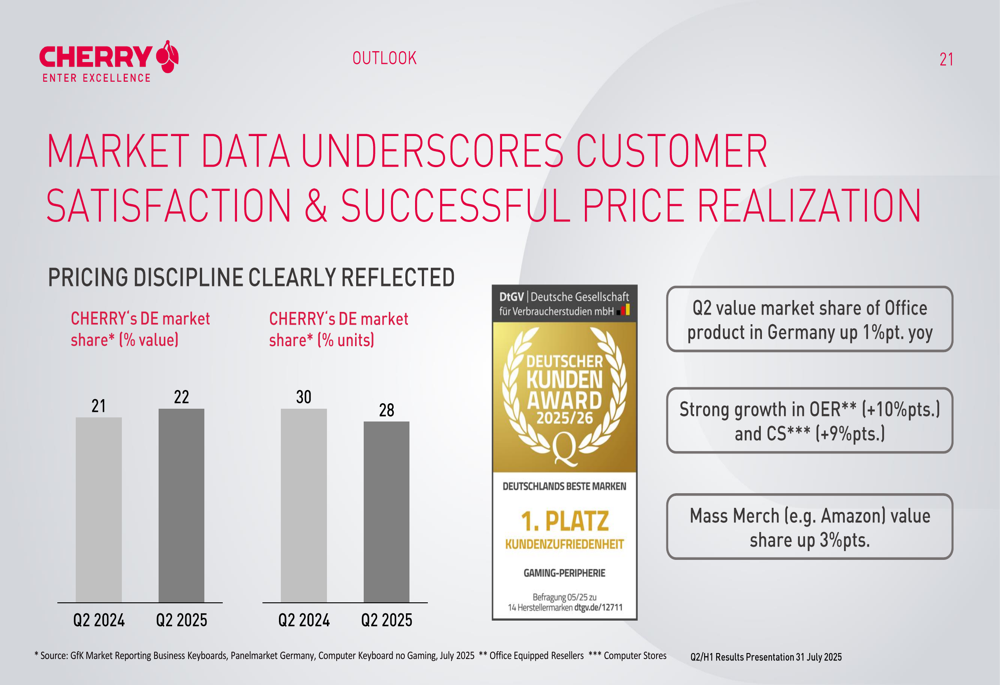

Despite overall market challenges, Cherry maintained its market position in Germany, with its value market share increasing by 1 percentage point year-over-year to 22% in Q2 2025, though its unit market share declined slightly from 30% to 28%.

The company’s market share data is shown in the following chart:

Cherry is navigating significant headwinds, including Germany’s third consecutive year of recession, oversupply in the German office peripherals market, and declining US demand coupled with import tariff challenges. The gaming market has also normalized after the COVID-induced boom.

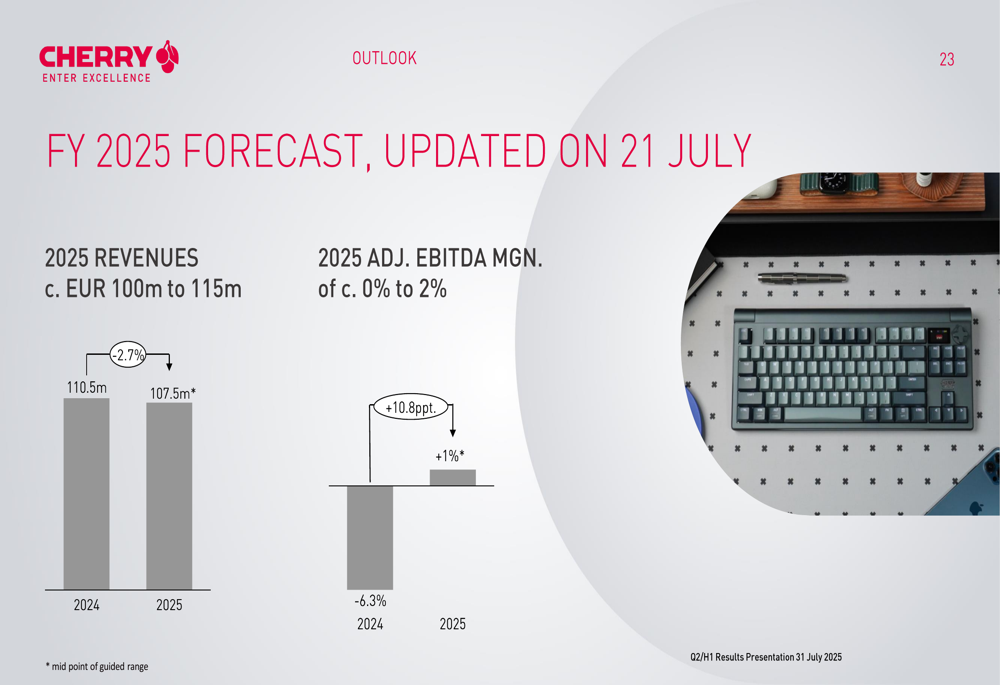

For the full year 2025, Cherry forecasts revenue of approximately €100-115 million with an adjusted EBITDA margin of 0-2%, representing a significant improvement from 2024’s -6.3% margin.

The company also announced the appointment of Jurjen Jongma as its new CFO effective September 1, 2025. Jongma brings over 30 years of international finance leadership experience, having previously held senior roles at Ebusco, Versuni, and Royal Philips.

Cherry’s stock (ETR:C3RY) closed at €0.67 on September 25, 2025, up 3.08% for the day, but remains significantly below its 52-week high of €1.65.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.