Fed Governor Cook sues Trump over firing attempt

Online pet retailer Chewy (NYSE:CHWY) released its first quarter fiscal 2025 results on June 11, showing solid revenue growth and margin expansion, though shares fell in premarket trading despite the positive metrics.

The company reported net sales of $3.12 billion for Q1 2025, representing an 8.3% year-over-year increase, while adjusted EBITDA rose to $192.7 million with a 6.2% margin, up from 5.7% in the same quarter last year.

Despite these improvements, Chewy shares were trading down 8.17% in premarket at $42.05, suggesting investors may have had higher expectations or concerns about future growth.

Quarterly Performance Highlights

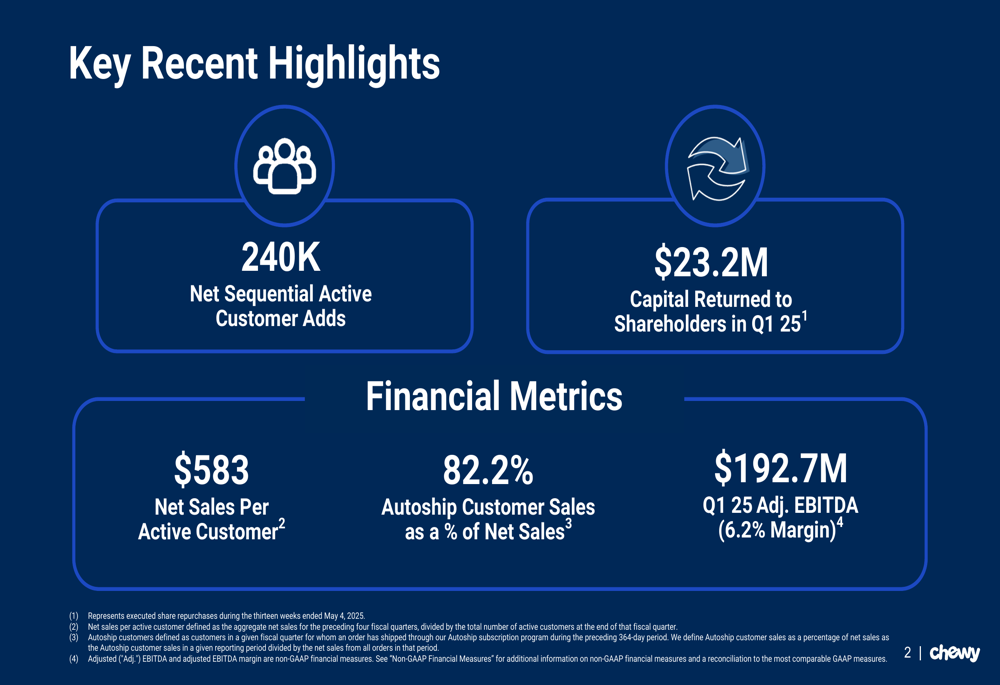

Chewy’s Q1 2025 results showed several positive developments, including the addition of 240,000 net sequential active customers and $23.2 million in capital returned to shareholders.

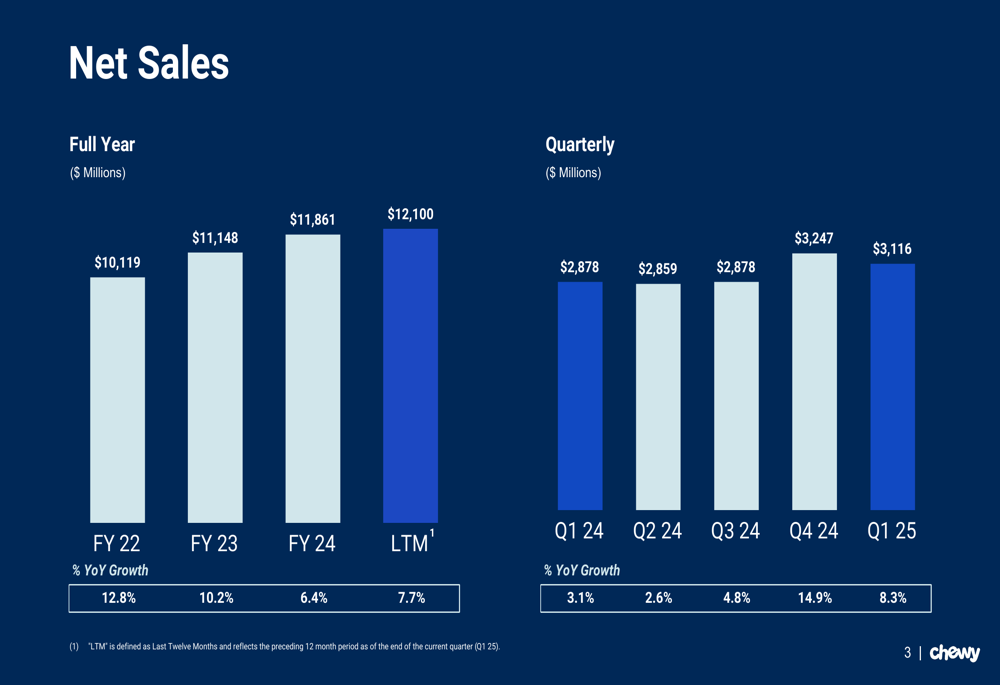

As shown in the following chart of quarterly net sales performance:

The company’s Q1 2025 net sales of $3.12 billion represented an 8.3% year-over-year increase, a significant acceleration from the 3.1% growth seen in Q1 2024. This growth trajectory has been steadily improving over recent quarters, with Q4 2024 showing particularly strong performance at 14.9% year-over-year growth.

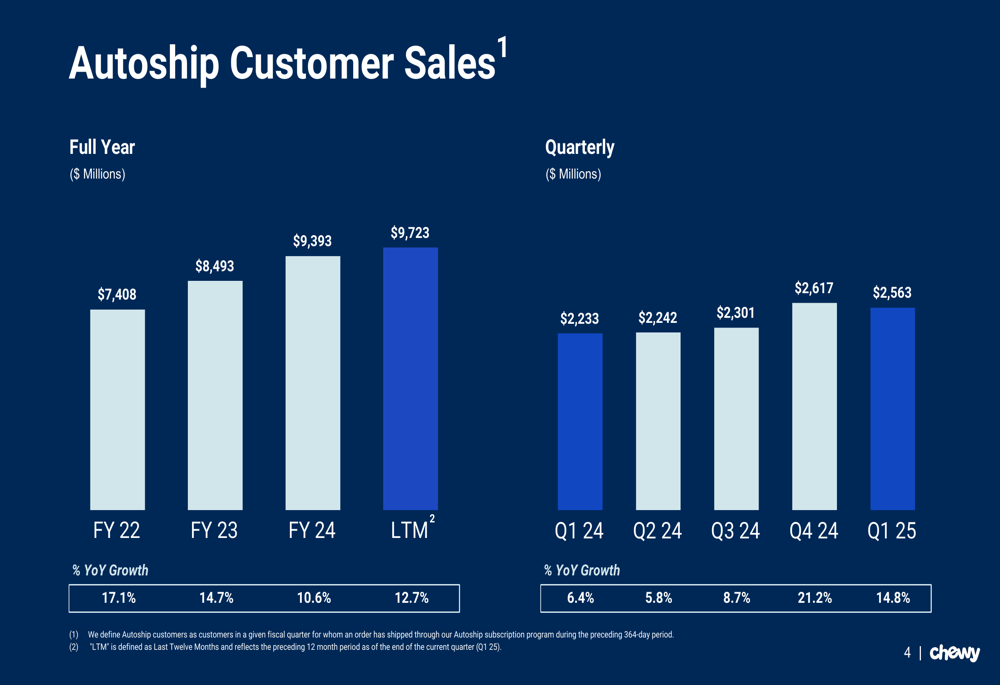

Chewy’s Autoship program, which allows customers to schedule regular deliveries of pet supplies, continues to be a key driver of the company’s business:

Autoship customer sales reached $2.56 billion in Q1 2025, growing 14.8% year-over-year and representing 82.2% of total net sales. This recurring revenue stream provides Chewy with a stable foundation and demonstrates strong customer loyalty.

Detailed Financial Analysis

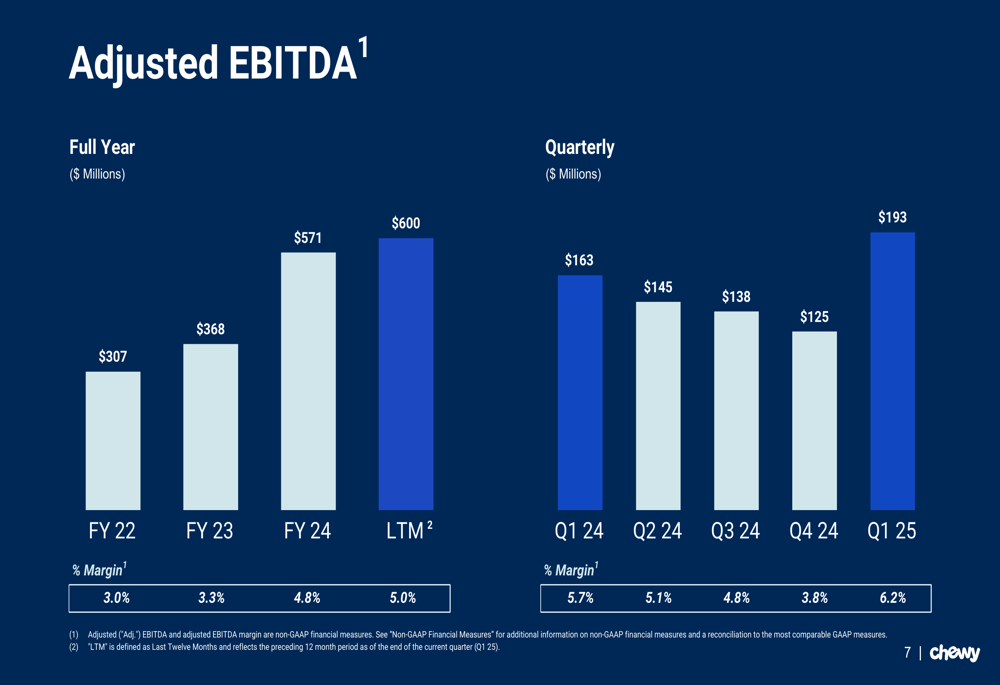

Profitability metrics showed notable improvement in the first quarter, with adjusted EBITDA reaching $192.7 million:

The 6.2% adjusted EBITDA margin in Q1 2025 represents a 50 basis point improvement over the 5.7% reported in Q1 2024. This continues the company’s trend of expanding profitability, with the last twelve months (LTM) adjusted EBITDA reaching $600 million at a 5.0% margin, compared to 4.8% for fiscal year 2024.

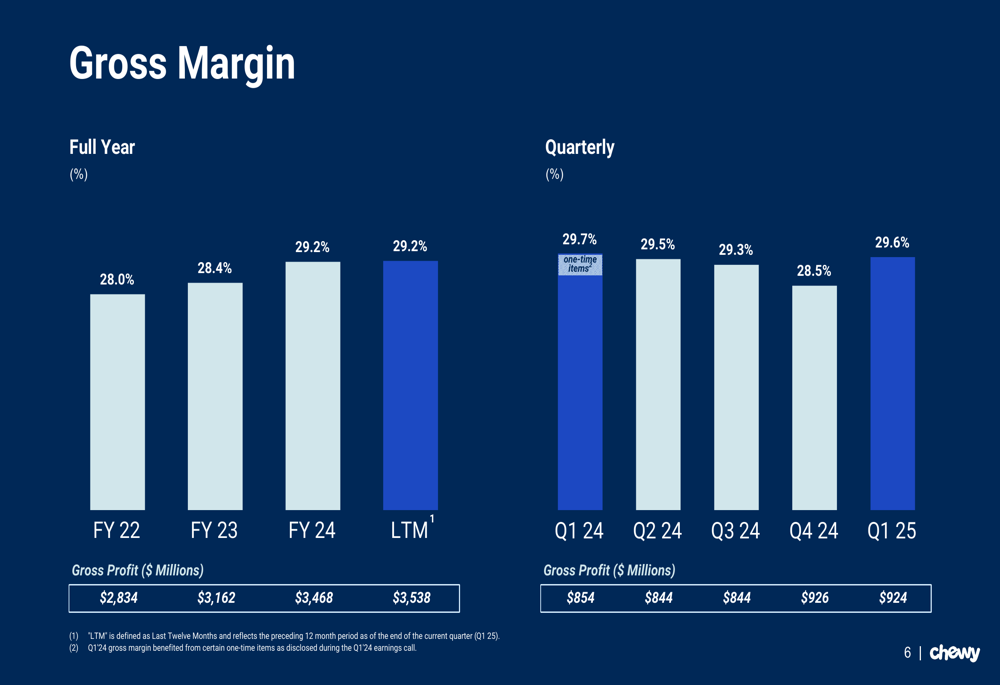

Gross margin performance remained relatively stable:

Q1 2025 gross margin came in at 29.6%, nearly flat compared to 29.7% in Q1 2024, but improved sequentially from 28.5% in Q4 2024. The company has maintained gross margins around 29% in recent quarters, demonstrating consistent operational efficiency despite inflationary pressures in the broader economy.

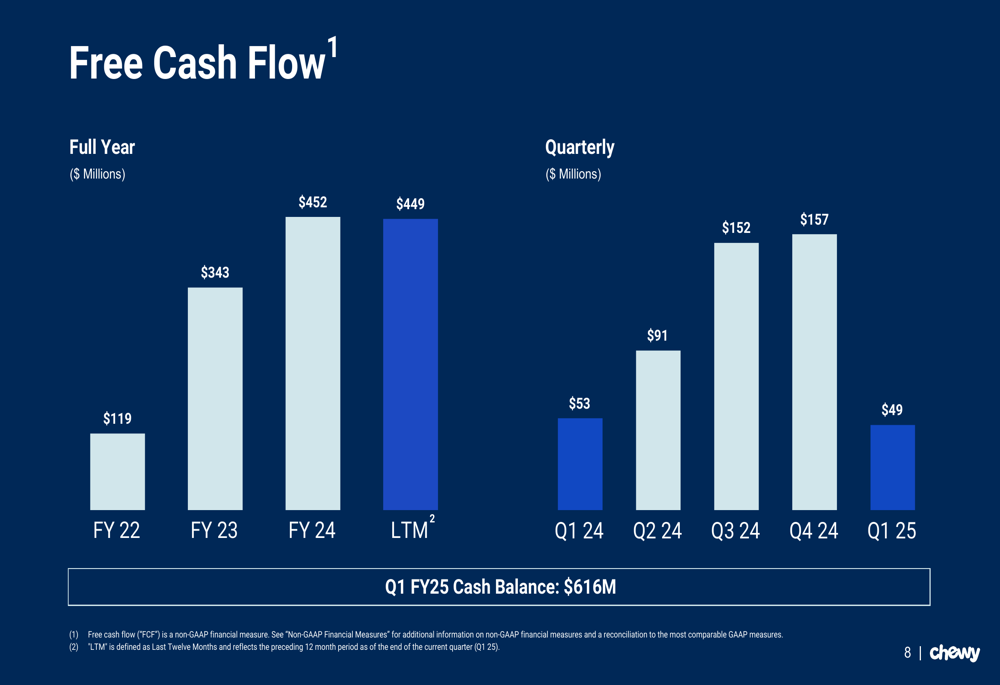

Free cash flow, while positive, showed a slight year-over-year decline:

Chewy generated $49 million in free cash flow during Q1 2025, compared to $53 million in Q1 2024. However, the company’s cash position remains strong with a Q1 FY25 cash balance of $616 million, providing ample resources for continued investment and shareholder returns.

Strategic Initiatives & Customer Metrics

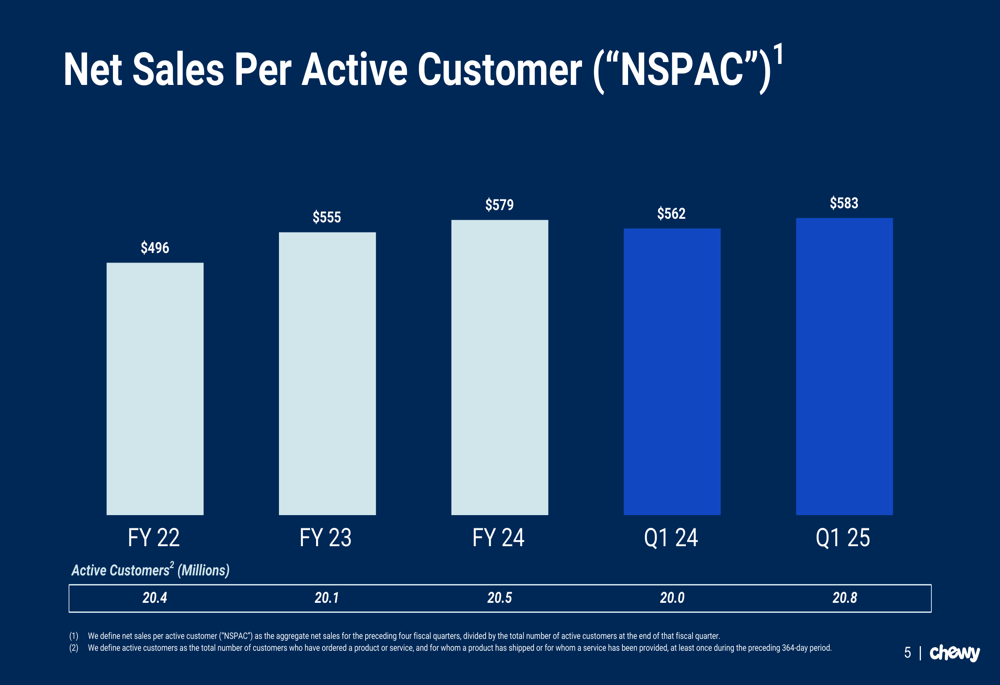

Chewy’s customer metrics continue to show positive momentum, with active customers increasing to 20.8 million in Q1 2025, up from 20.0 million in Q1 2024. More importantly, the company is extracting more value from its customer base:

Net sales per active customer (NSPAC) reached $583 in Q1 2025, a 3.7% increase from $562 in Q1 2024 and continuing the steady upward trend seen over recent years. This metric has grown from $496 in FY22 to $583 currently, demonstrating Chewy’s ability to increase wallet share among its customer base.

The company’s key recent highlights emphasize its focus on both customer acquisition and shareholder returns:

The addition of 240,000 net sequential active customers in Q1 2025 indicates that Chewy is successfully attracting new pet parents to its platform, while the $23.2 million returned to shareholders shows a commitment to delivering value to investors.

Forward-Looking Statements

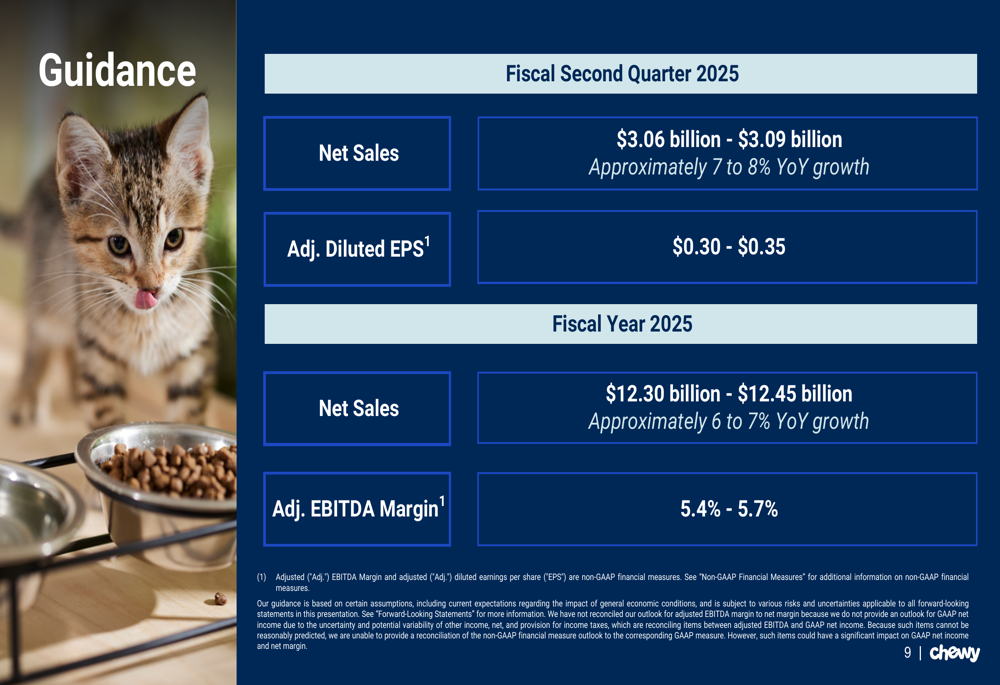

Looking ahead, Chewy provided guidance for both the second quarter and full fiscal year 2025:

For Q2 2025, the company expects net sales between $3.06 billion and $3.09 billion, representing approximately 7-8% year-over-year growth, with adjusted diluted EPS of $0.30-$0.35.

For the full fiscal year 2025, Chewy projects net sales of $12.30-12.45 billion (6-7% year-over-year growth) and an adjusted EBITDA margin of 5.4-5.7%, showing continued confidence in its growth trajectory and profitability improvements.

The premarket stock decline suggests investors may have been looking for even stronger guidance or had concerns about the slight deceleration in projected growth rates compared to the Q1 performance. However, the company’s consistent customer additions, improving profitability metrics, and strong Autoship performance indicate Chewy continues to strengthen its position in the online pet retail market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.